|

|

市場調査レポート

商品コード

1735898

欧州のデータセンターコロケーション市場:用途別、製品別、国別 - 分析と予測(2025年~2034年)Europe Data Center Colocation Market: Focus on Application, Product, and Country - Analysis and Forecast, 2025-2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 欧州のデータセンターコロケーション市場:用途別、製品別、国別 - 分析と予測(2025年~2034年) |

|

出版日: 2025年05月30日

発行: BIS Research

ページ情報: 英文 67 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

欧州のデータセンターコロケーションの市場規模は、2024年に567億2,000万米ドルと評価され、2025年から2034年にかけて13.68%のCAGRで拡大し、2034年には2,267億6,000万米ドルに達すると予測されています。

データセンターコロケーション市場は、安全でスケーラブルかつ手頃な価格のITインフラに対するニーズの高まりにより、欧州で急速に拡大しています。企業がクラウド・コンピューティング、ハイブリッドITアーキテクチャ、デジタルトランスフォーメーション・プロジェクトを採用する中、コロケーション・サービスは、高性能で弾力性があり、エネルギー効率の高い運用を維持しながら、インフラ管理の負荷を軽減するために不可欠となっています。

分散された低レイテンシーデータセンターネットワークのニーズは、エッジコンピューティングの成長によってさらに高まっています。同時に、持続可能性が最重要課題として浮上し、コロケーション・プロバイダーは、冷却システムの改善、環境に配慮した施設設計、再生可能エネルギーの導入への投資を行うようになっています。こうした要因が、欧州の厳格なデータ保護規制や、アップタイムと運用効率に対する企業の需要の高まりと相まって、コロケーションを欧州の進化するデジタルインフラの重要な構成要素として位置づけています。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2025年~2034年 |

| 2025の年評価 | 715億米ドル |

| 2034年の予測 | 2,267億6,000万米ドル |

| CAGR | 13.68% |

欧州のデータセンターコロケーション市場は、クラウドの導入、デジタル化の進展、GDPRのような厳格なデータ保護法などの要因により、急速に拡大しています。コロケーションは、自社データセンターの建設や維持に伴う資本コストをかけずに安全で高性能な施設を提供する戦略的な選択肢となっており、企業はより拡張性が高く経済的な選択肢を求めてオンプレミスのインフラから移行しています。

ハイブリッドITモデルやマルチクラウド構想の結果、特にeコマース、ヘルスケア、金融などデータ集約型の分野でコロケーションサービスのニーズが高まっています。また、AIやモノのインターネットのような低レイテンシーアプリケーションをサポートするためにエッジコンピューティングの利用が増加した結果、地域全体で分散コロケーションサイトの開発が進んでいます。

持続可能性もまた、市場を大きく促進する要因となっています。企業のESG目標を達成し、変化する環境規範を遵守するため、欧州のコロケーション・プロバイダーは、カーボンニュートラルなインフラ、革新的な冷却システム、グリーンエネルギーに多額の投資を行っています。南欧や東欧の新興市場が、コスト面のメリットやデジタル製品への需要の高まりから勢いを増している一方で、西欧市場、特にフランクフルト、アムステルダム、パリ、ロンドンは依然として重要なハブとなっています。技術の進歩、規制の遵守、デジタルインフラへのビジネス依存度の高まりから、欧州のコロケーション市場は安定した成長が見込まれています。

市場セグメンテーション

セグメンテーション1:用途別

- ITおよび電気通信

- 銀行・金融サービス・保険(BFSI)

- 政府・公共部門

- ヘルスケア

- 製造業

- 小売業

- その他

セグメンテーション2:ビジネスモデル別

- 小売

- 卸売

セグメンテーション3:地域別

- 欧州ドイツ、フランス、英国、オランダ、アイルランド、イタリア、その他

欧州データセンターコロケーション市場動向と促進要因・課題

動向

- 低レイテンシー用途をサポートするエッジデータセンターの成長

- ハイブリッドおよびマルチクラウド環境への需要の高まり

- 液体冷却とエネルギー効率の高いインフラの採用増加

- 再生可能エネルギーによるグリーン・コロケーションへの注目の高まり

- 世界クラウドプロバイダーとのハイパースケールコロケーションパートナーシップの拡大

促進要因

- 各業界で加速するデジタルトランスフォーメーションとクラウド移行

- 厳しいデータ主権とGDPRコンプライアンス要件

- オンプレミスインフラに対するコスト効率と拡張性のメリット

- ハイパフォーマンス・コンピューティング(HPC)やAIワークロードに対する需要の高まり

- eコマース、ビデオストリーミング、COVID後のリモートワークの急増

課題

- データセンター施設の新設にかかる高い資本コストと運用コスト

- 都市部における電力供給の制約と送電網の制限

- 欧州各国における環境規制のばらつき

- サイバーセキュリティリスクの増大と強固なデータ保護への圧力

- ITおよびデータセンター業務に特化した人材の不足

製品/イノベーション戦略:欧州のデータセンターコロケーション市場は、多様な用途とビジネスモデルに基づいてセグメント化されており、幅広い使用事例に関する洞察が得られます。主な用途には、IT・通信、銀行、金融サービス、保険(BFSI)、政府、ヘルスケア、製造、小売などがあり、それぞれ拡張性、安全性、信頼性の高いコロケーションサービスの恩恵を受けています。市場はまた、柔軟なソリューションを必要とする中小企業向けのリテールコロケーションと、大量のデータを必要とする大企業向けのホールセール・コロケーションを区別しています。エネルギー効率の高い冷却、自動化、強化されたセキュリティ機能など、継続的な技術進歩が市場の成長を促進すると予想され、業界各社は急速に進化するこの分野で提供サービスを拡大し、市場での地位を強化する大きな機会を得ています。

成長/マーケティング戦略:欧州のデータセンターコロケーション市場は急速なペースで成長しています。同市場は、既存および新興の市場プレーヤーに大きなビジネスチャンスを提供しています。このセグメントで取り上げている戦略には、M&A、製品投入、提携・協力、事業拡大、投資などがあります。企業が市場での地位を維持・強化するために好む戦略には、主に製品開発が含まれます。

競合戦略:本調査で分析・プロファイリングした欧州データセンターコロケーション市場の主要企業プロファイルには、自動車および自動車分野の専門家が含まれています。さらに、パートナーシップ、契約、提携などの包括的な競合情勢は、市場の未開拓の収益ポケットを理解する上で読者を支援するものと期待されます。

当レポートでは、欧州のデータセンターコロケーション市場について調査し、市場の概要とともに、用途別、製品別、国別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

第1章 市場

- コロケーションデータセンター市場の動向:現状と将来への影響評価

- 研究開発レビュー

- 市場力学の概要

第2章 地域

- 地域サマリー

- 欧州

- 地域概要

- 市場成長促進要因

- 市場成長抑制要因

- 用途

- 製品

- 欧州(国別)

第3章 市場-競合ベンチマーキングと企業プロファイル

- 今後の見通し

- 地理的評価

- IPTP Networks

- 365 Data Centers

第4章 調査手法

List of Figures

- Figure 1: Europe Data Center Colocation Market, $Billion, 2024, 2027, and 2034

- Figure 2: Data Center Colocation Market (by Region), $Billion, 2023, 2027, and 2034

- Figure 3: Europe Data Center Colocation Market (by Application), $Billion, 2023, 2027, and 2034

- Figure 4: Europe Data Center Colocation Market (by Business Model), $Billion, 2023, 2027, and 2034

- Figure 5: Key Events

- Figure 6: Estimated Increase in Europe Data Center Capacity, 2023 and 2030, in GW

- Figure 7: HPC Cluster Developments in the Data Center Market

- Figure 8: Share of Total 5G Mobile Connections (by Region) 2023 and 2030

- Figure 9: Increasing Rack Power Density Across Key Data Center Segments

- Figure 10: Comparison of Different Rack Densities in Data Centers

- Figure 11: Patent Analysis (by Country), January 2021-January 2025

- Figure 12: Patent Analysis (by Company), January 2021-January 2025

- Figure 13: End User and Buying Criteria in the Data Center Colocation Market

- Figure 14: North America and Europe: Leading Hubs for Data Center Investments

- Figure 15: Estimated Europe Data Creation, Zettabytes or Billions of Terabytes

- Figure 16: Estimated Increase in IoT Adoption in 2023

- Figure 17: Percentage of Enterprises Buying Cloud Computing Services in Europe and Some Countries in Europe, 2021 and 2023

- Figure 18: Estimated Data Centers Energy Consumption (by Country), 2022

- Figure 19: Germany Data Center Colocation Market, $Billion, 2023-2034

- Figure 20: France Data Center Colocation Market, $Billion, 2023-2034

- Figure 21: U.K. Data Center Colocation Market, $Billion, 2023-2034

- Figure 22: Netherlands Data Center Colocation Market, $Billion, 2023-2034

- Figure 23: Ireland Data Center Colocation Market, $Billion, 2023-2034

- Figure 24: Italy Data Center Colocation Market, $Billion, 2023-2034

- Figure 25: Rest-of-Europe Data Center Colocation Market, $Billion, 2023-2034

- Figure 26: Data Triangulation

- Figure 27: Top-Down and Bottom-Up Approach

- Figure 28: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Opportunities across Region

- Table 3: Trends Overview

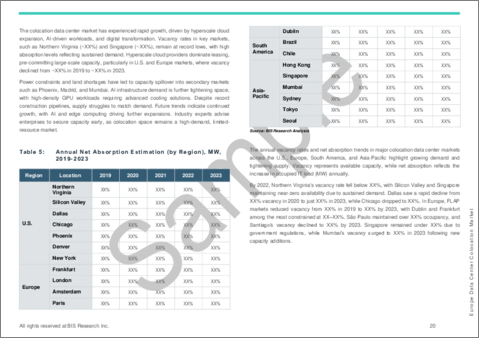

- Table 4: Annual Vacancy Rates, Percentage, by Region, 2019-2023

- Table 5: Annual Net Absorption Estimation (by Region), MW, 2019-2023

- Table 6: Outlook of Data Center Colocation Market (by Location)

- Table 7: Recent Investments and Developments in Data Center Liquid Cooling Innovations

- Table 8: Data Center Colocation Market (by Region), $Billion, 2023-2034

- Table 9: Europe Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 10: Europe Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 11: Germany Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 12: Germany Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 13: France Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 14: France Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 15: U.K. Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 16: U.K. Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 17: Netherlands Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 18: Netherlands Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 19: Ireland Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 20: Ireland Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 21: Italy Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 22: Italy Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 23: Rest-of-Europe Data Center Colocation Market (by Application), $Billion, 2023-2034

- Table 24: Rest-of-Europe Data Center Colocation Market (by Business Model), $Billion, 2023-2034

- Table 25: Market Share,2023

Introduction to Europe Data Center Colocation Market

The Europe data center colocation market was valued at $56.72 billion in 2024 and is projected to grow at a CAGR of 13.68% from 2025 to 2034, reaching $226.76 billion by 2034. The market for data center colocation is expanding quickly in Europe due to the growing need for safe, scalable, and affordable IT infrastructure. Colocation services are now crucial for offloading infrastructure management while maintaining high-performance, resilient, and energy-efficient operations as businesses embrace cloud computing, hybrid IT architectures, and digital transformation projects.

The need for dispersed, low-latency data center networks is being further fuelled by the region's growth in edge computing. At the same time, sustainability has emerged as a top concern, leading colocation providers to make investments in improved cooling systems, ecologically conscious facility design, and the incorporation of renewable energy. These factors, combined with stringent European data protection regulations and growing enterprise demand for uptime and operational efficiency, are positioning colocation as a critical component of Europe's evolving digital infrastructure landscape.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2025 - 2034 |

| 2025 Evaluation | $71.50 Billion |

| 2034 Forecast | $226.76 Billion |

| CAGR | 13.68% |

Market Introduction

The market for data center colocation in Europe is expanding rapidly due to factors including cloud adoption, growing digitisation, and strict data protection laws like GDPR. Colocation has become a strategic alternative that offers safe, high-performance facilities without the capital costs associated with constructing and maintaining in-house data centers, as businesses move away from on-premise infrastructure in favour of more scalable and economical options.

The need for colocation services is growing as a result of hybrid IT models and multi-cloud initiatives, especially in data-intensive sectors like e-commerce, healthcare, and finance. Distributed colocation sites are also being developed throughout the region as a result of the increasing use of edge computing to support low-latency applications like AI and the Internet of Things.

Sustainability is also a significant market driver. In order to achieve corporate ESG goals and adhere to changing environmental norms, European colocation providers are making significant investments in carbon-neutral infrastructure, innovative cooling systems, and green energy. While emerging markets in Southern and Eastern Europe are gaining pace due to cost benefits and increased demand for digital products, Western European markets-particularly Frankfurt, Amsterdam, Paris, and London-remain important hubs. All things considered, the European colocation market is expected to grow steadily due to technological advancements, adherence to regulations, and growing business dependence on digital infrastructure.

Market Segmentation:

Segmentation 1: by Application

- IT and Telecom

- Banking, Financial Services, and Insurance (BFSI)

- Government and Public Sector

- Healthcare

- Manufacturing

- Retail

- Others

Segmentation 2: by Business Model

- Retail

- Wholesale

Segmentation 3: by Region

- Europe: Germany, France, U.K., Netherlands, Ireland, Italy, and Rest-of-Europe

Europe Data Center Colocation Market Trends, Drivers and Challenges

Trends

- Growth of edge data centers to support low-latency applications

- Increased demand for hybrid and multi-cloud environments

- Rising adoption of liquid cooling and energy-efficient infrastructure

- Greater focus on green colocation powered by renewable energy

- Expansion of hyperscale colocation partnerships with global cloud providers

Drivers

- Accelerating digital transformation and cloud migration across industries

- Stringent data sovereignty and GDPR compliance requirements

- Cost-efficiency and scalability benefits over on-premise infrastructure

- Growing demand for high-performance computing (HPC) and AI workloads

- Surge in e-commerce, video streaming, and remote work post-COVID

Challenges

- High capital and operational costs in establishing new data center facilities

- Power availability constraints and grid limitations in urban areas

- Variability in environmental regulations across European countries

- Increasing cybersecurity risks and pressure to ensure robust data protection

- Talent shortages in specialized IT and data center operations

How can this report add value to an organization?

Product/Innovation Strategy: The Europe data center colocation market is segmented based on diverse applications, and business models, providing insights into its broad range of use cases. Key applications include IT and telecom, banking, financial services, insurance (BFSI), government, healthcare, manufacturing, retail, and others, each benefiting from scalable, secure, and reliable colocation services. The market also distinguishes between retail colocation, which caters to smaller businesses requiring flexible solutions, and wholesale colocation, designed for large-scale enterprises with high-volume data needs. Continuous technological advancements, such as energy-efficient cooling, automation, and enhanced security features, are expected to drive the market's growth, providing substantial opportunities for industry players to expand their offerings and strengthen their market position in this rapidly evolving sector.

Growth/Marketing Strategy: The Europe data center colocation market has been growing at a rapid pace. The market offers enormous opportunities for existing and emerging market players. Some of the strategies covered in this segment are mergers and acquisitions, product launches, partnerships and collaborations, business expansions, and investments. The strategies preferred by companies to maintain and strengthen their market position primarily include product development.

Competitive Strategy: The key players in the Europe data center colocation market analyzed and profiled in the study include professionals with expertise in the automobile and automotive domains. Additionally, a comprehensive competitive landscape such as partnerships, agreements, and collaborations are expected to aid the reader in understanding the untapped revenue pockets in the market.

Key Market Players and Competition Synopsis

The companies that are profiled in the Europe data center colocation market have been selected based on inputs gathered from primary experts who have analyzed company coverage, product portfolio, and market penetration.

Some of the prominent names in this market are:

- IPTP Networks

- 365 Data Centers

Table of Contents

Executive Summary

Scope and Definition

1 Markets

- 1.1 Colocation Data Center Market Trends: Current and Future Impact Assessment

- 1.1.1 Data Center Capacities: Current and Future

- 1.1.1.1 Retrofitting and Brownfield Projects

- 1.1.1.2 Green Field Projects and New Installation

- 1.1.2 Data Center Power Consumption Scenario

- 1.1.3 Vacancy Rates and Absorption (by Region)

- 1.1.4 Key Markets to Focus on

- 1.1.5 Other Industrial Trends

- 1.1.5.1 HPC Cluster Developments

- 1.1.5.2 Blockchain Initiatives

- 1.1.5.3 Super Computing

- 1.1.5.4 5G and 6G Developments

- 1.1.5.5 Impact of Server/Rack Density

- 1.1.1 Data Center Capacities: Current and Future

- 1.2 Research and Development Review

- 1.2.1 Patent Filing Trend (by Country, by Company)

- 1.2.2 End User and Buying Criteria

- 1.3 Market Dynamics Overview

- 1.3.1 Market Drivers

- 1.3.1.1 Increasing Data Center Spending

- 1.3.1.2 Growing Integration of AI and Cloud Computing

- 1.3.1.3 Sustainability and Environmental Pressures

- 1.3.2 Market Restraints

- 1.3.2.1 Power and Energy Constraints

- 1.3.2.2 Data Security and Compliance Challenges

- 1.3.3 Market Opportunities

- 1.3.3.1 Growing Demand for Different Business Models

- 1.3.3.2 Growth in AI Workloads

- 1.3.1 Market Drivers

2 Regions

- 2.1 Regional Summary

- 2.2 Europe

- 2.2.1 Regional Overview

- 2.2.2 Driving Factors for Market Growth

- 2.2.3 Factors Challenging the Market

- 2.2.4 Application

- 2.2.5 Product

- 2.2.6 Europe (by Country)

- 2.2.6.1 Germany

- 2.2.6.1.1 Application

- 2.2.6.1.2 Product

- 2.2.6.2 France

- 2.2.6.2.1 Application

- 2.2.6.2.2 Product

- 2.2.6.3 U.K.

- 2.2.6.3.1 Application

- 2.2.6.3.2 Product

- 2.2.6.4 Netherlands

- 2.2.6.4.1 Application

- 2.2.6.4.2 Product

- 2.2.6.5 Ireland

- 2.2.6.5.1 Application

- 2.2.6.5.2 Product

- 2.2.6.6 Italy

- 2.2.6.6.1 Application

- 2.2.6.6.2 Product

- 2.2.6.7 Rest-of-Europe

- 2.2.6.7.1 Application

- 2.2.6.7.2 Product

- 2.2.6.1 Germany

3 Markets - Competitive Benchmarking and Company Profiles

- 3.1 Next Frontiers

- 3.2 Geographic Assessment

- 3.2.1 IPTP Networks

- 3.2.1.1 Overview

- 3.2.1.2 Top Products/Product Portfolio

- 3.2.1.3 Top Competitors

- 3.2.1.4 Target Customers/End Users

- 3.2.1.5 Key Personnel

- 3.2.1.6 Analyst View

- 3.2.1.7 Market Share (by Revenue), 2023

- 3.2.1.8 Market Share (by Number of Colocation Data Centers), 2023

- 3.2.2 365 Data Centers

- 3.2.2.1 Overview

- 3.2.2.2 Top Products/Product Portfolio

- 3.2.2.3 Top Competitors

- 3.2.2.4 Target Customers/End Users

- 3.2.2.5 Key Personnel

- 3.2.2.6 Analyst View

- 3.2.2.7 Market Share (by Revenue), 2023

- 3.2.2.8 Market Share (by Number of Colocation Data Centers), 2023

- 3.2.1 IPTP Networks

4 Research Methodology

- 4.1 Data Sources

- 4.1.1 Primary Data Sources

- 4.1.2 Secondary Data Sources

- 4.1.3 Data Triangulation

- 4.2 Market Estimation and Forecast