|

|

市場調査レポート

商品コード

1732571

欧州の風力補助推進市場:用途別、技術別、設置タイプ別、船舶タイプ別、国別 - 分析と予測(2024年~2034年)Europe Wind-Assisted Propulsion Market: Focus on Application, Technology, Installation Type, Vessel Type and Country-Level Analysis - Analysis and Forecast, 2024-2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 欧州の風力補助推進市場:用途別、技術別、設置タイプ別、船舶タイプ別、国別 - 分析と予測(2024年~2034年) |

|

出版日: 2025年05月23日

発行: BIS Research

ページ情報: 英文 84 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

欧州の風力補助推進の市場規模は、2024年に9,698万米ドルとなりました。

同市場は、CAGR 71.69%で成長し、2034年には215億8,685万米ドルに達すると予測されています。欧州では、風力補助推進(WAP)がIMOのエネルギー効率既存船指数(EEXI)と炭素原単位指標(CII)に正式に組み込まれ、正真正銘の「エネルギーハーベスティング」技術であることを示しています。船舶は、偏西風を直接推進力に変えるために、フレッツナー・ローター、翼帆、カイト・システムを使用することで、エンジン負荷とCO2排出量を減らすことができます。しかし、地域的な天候の変動は、依然として燃料節減性能に大きな影響を与えます。長期的な凪や横風は、強力な北寄りの強風の利点を否定しかねません。これに対抗するため、運航者は、燃料費最適化手順、船舶固有の性能曲線、リアルタイムの気象予報を組み込んだ高度な気象航路システムにますます依存するようになっています。これらのシステムは、スケジュールを犠牲にすることなく、風力を最適化するコース調整を動的にプロットします。

こうした運用面での進歩にもかかわらず、商業的な導入は、相互に関連する多くの課題によって妨げられています。ローターセイルの設置やリジッドウィングセイルシステムは、数100万米ドル規模の設備投資を必要とすることが多く、投資回収期間は数年かかると予想されます。こうしたスケジュールは、傭船市場の変動や短い契約期間と相反します。各インテグレーターは、構造強度、制御システムのプロトコル、メンテナンス方法について独自の基準を持っており、これが大量生産の妨げとなり、単価を押し上げています。さらに、船級協会の評価や構造補強は、しばしば改装の引き金となり、ドライドックのスケジュールに数週間を追加することになります。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2024年~2034年 |

| 2024年の評価 | 9,698万米ドル |

| 2034年の予測 | 215億8,685万米ドル |

| CAGR | 71.69% |

将来予測によると、WAPハードウェアの開発、生産ラインの拡大、船級協会の標準設計フレームワークの合意により、単価は大幅に低下します。WAPは、グリーンメタノール、先進バイオ燃料、水素燃料電池の試験利用を通じて欧州海運の脱炭素化が進むにつれて、補完的な「ゼロコスト」推力源としてますます機能するようになります。これにより、北海、バルト海、地中海のトレードレーンにおける代替燃料船の航続距離と経済性が向上します。

市場導入

欧州における風力補助推進市場には、商業船舶の追加推力源として風力エネルギーを利用することを目的とした様々な技術が含まれます。燃料を節約し、排出ガスを削減し、運航の回復力を高めるために、船主やインテグレーターは、ここ10年以内にローターセイル、硬質ウィングセイル、インフレータブルカイト、その他の空力装置を研究してきました。ばら積み貨物船、タンカー、コンテナ船、ROROボートの新造と改造の両方向けに設計されたソリューションにより、この拡大する市場セグメントは、海洋工学、再生可能エネルギー、デジタルナビゲーションを結び付けています。

用船者、船級協会、政府の脱炭素化目標は一致しつつあり、北海、バルト海、地中海など欧州の重要な貿易ルートでの実験的な取り組みを後押ししています。テクノロジー企業もまた、風力タービンと蓄電池、陸上電力接続、高度なデータ分析を組み合わせたハイブリッド戦略をテストしています。金融機関や保険会社が大規模配備のリスクプロファイルを評価する一方で、船主、技術プロバイダー、研究機関は、性能モデリングとライフサイクル評価を改善するために協力しています。

将来、この業界は、企業の持続可能性目標、カーボンニュートラルな航路への要望、代替燃料への幅広いシフトによって推進されるであろう。風力アシスト装置は、設計基準が進歩し、デジタルツールが設置計画を簡素化するにつれて、欧州の環境に優しい海運環境の当たり前の特徴となると思われます。風力アシスト装置は燃料転換を支援し、低炭素海上輸送の新たな道を開くと思われます。

欧州の風力推進市場動向と促進要因・課題

動向

- 欧州全域での風力補助推進ソリューションの急速な拡大

- ローターセイル、ウィングセイル、カイトなどのハイブリッドシステムの使用の増加

- 既存船の改造と「風力対応」新造船の両方が増加中

促進要因

- 国際およびEUの排出ガス規制の強化により、燃料使用量の削減が求められている

- 化石燃料コストの上昇が、風力アシストを経済的に魅力的なものにしている

- 政府の補助金や港湾インセンティブが導入を後押し

- より環境に優しい海運を求める投資家や顧客の需要

課題

- 船主にとって高額な先行投資と長い投資回収期間

- 性能と節約を測定するための統一基準の欠如

- 天候に左右されるため、燃費削減効果が変動しやすい

- 新しいシステムを既存の船舶設計に組み込むことの複雑さ

- 特殊部品のサプライチェーン上の制約

欧州の風力補助推進市場は、船舶の種類(ばら積み貨物船、コンテナ船、旅客船など)、風力推進技術(帆、ローター、凧、翼帆)、材料(複合材料、布帆、空気力学)、方法(後付け設置、新設、ハイブリッドシステム)に基づいて利用可能な様々な技術を包括的に理解することができます。欧州の風力補助推進市場は、風力技術の進歩、投資の増加、持続可能な海運に対する意識の高まりにより、大幅な成長が見込まれています。その結果、風力アシスト推進力部門は高投資・高収益の市場であり、拡大のチャンスも大きいです。

成長/マーケティング戦略:欧州の風力補助推進市場は急速な成長を遂げています。同市場は、同業界の既存プレーヤーと新興プレーヤーの双方に大きな機会をもたらしています。各社は競争優位を得るため、提携、協力、技術革新、インフラの拡大といった戦略に注力しています。製品開拓、特に様々な船舶タイプに対応した先進風力推進システムの開発は、市場のリーダーシップを維持し、持続可能な海運を推進するための重要な戦略です。

競合戦略:欧州の風力補助推進市場の主要企業は、船舶向けに様々な風力補助技術を提供しています。企業は、相乗効果の活用、製品提供の改善、未開拓の収益ポテンシャルの開拓を目指し、戦略的パートナーシップや提携を積極的に進めています。環境に優しいソリューションの採用を求める規制圧力の高まりに伴い、欧州の風力補助推進器市場は、海上事業における持続可能性を促進する技術革新の恩恵を受けて、加速度的な成長を示すことになりそうです。

主要市場参入企業と競合情勢

欧州の風力補助推進器市場でプロファイルされている企業は、企業範囲、製品ポートフォリオ、市場浸透度を分析した主要専門家から収集した情報に基づいて選定されています。

当レポートでは、欧州の風力補助推進市場について調査し、市場の概要とともに、用途別、技術別、設置タイプ別、船舶タイプ別、国別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

第1章 市場

- 風力補助推進市場:現状と将来

- 海運業界における技術革新

- 風力補助推進への投資増加

- サプライチェーンの概要

- バリューチェーン分析

- 価格分析

- 研究開発レビュー

- 風力補助推進市場のエコシステム

- コンソーシアムと協会

- 規制機関/認証機関

- 政府プログラム

- プログラム(研究機関・大学別)

- 風力補助推進の経済的影響

- 市場力学:概要

- 市場促進要因

- 市場抑制要因

- 市場機会

- スタートアップの情勢

第2章 地域

- 風力補助推進市場(地域別)

- 欧州

- 市場

- 用途

- 製品

- 欧州(国別)

第3章 市場-競合ベンチマーキングと企業プロファイル

- 今後の見通し

- 企業プロファイル

- Norsepower

- bound4blue

- Econowind

- Anemoi Marine Technologies Ltd.

- Airseas

- GT Green Technologies

- Becker Marine Systems

- Propelwind S.A.S.

- SkySails Marine

- DNV

- OCEANBIRD

第4章 調査手法

List of Figures

- Figure 1: Europe Wind-Assisted Propulsion Market (by Scenario), $Million, 2024, 2027, and 2034

- Figure 2: Wind-Assisted Propulsion Market (by Region), $Million, 2023, 2027, and 2034

- Figure 3: Europe Wind-Assisted Propulsion Market (by Application), $Million, 2023, 2027, and 2034

- Figure 4: Europe Wind-Assisted Propulsion Market (by Technology), $Million, 2023, 2027, and 2034

- Figure 5: Europe Wind-Assisted Propulsion Market (by Installation Type), $Million, 2023, 2027, and 2034

- Figure 6: Europe Wind-Assisted Propulsion Market (by Vessel Type), $Million, 2023, 2027, and 2034

- Figure 7: Key Events

- Figure 8: Supply Chain and Risks within the Supply Chain

- Figure 9: Value Chain Analysis

- Figure 10: Pricing Strategy for Wind-Assisted Propulsion Market, (2023-2034), $Million/Unit

- Figure 11: Patent Analysis (by Patent Office), January 2021-February 2025

- Figure 12: Patent Analysis (by Company), January 2021-February 2025

- Figure 13: Wind Propulsion Savings with Increased Fuel Prices

- Figure 14: Motor Gasoline Energy Prices($/L), 2020-2023

- Figure 15: U.K. Wind-Assisted Propulsion Market, $Million, 2023-2034

- Figure 16: Germany Wind-Assisted Propulsion Market, $Million, 2023-2034

- Figure 17: France Wind-Assisted Propulsion Market, $Million, 2023-2034

- Figure 18: Greece Wind-Assisted Propulsion Market, $Million, 2023-2034

- Figure 19: Norway Wind-Assisted Propulsion Market, $Million, 2023-2034

- Figure 20: Finland Wind-Assisted Propulsion Market, $Million, 2023-2034

- Figure 21: Rest-of-Europe Wind-Assisted Propulsion Market, $Million, 2023-2034

- Figure 22: Data Triangulation

- Figure 23: Top-Down and Bottom-Up Approach

- Figure 24: Assumptions and Limitations

List of Tables

- Table 1: Market Snapshot

- Table 2: Opportunities across Region

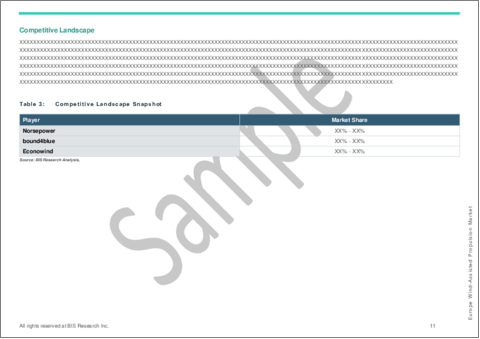

- Table 3: Competitive Landscape Snapshot

- Table 4: Trends: Overview

- Table 5: Consortiums and Associations

- Table 6: Regulatory/Certification Bodies

- Table 7: List of Government Programs for the Wind-Assisted Propulsion Market

- Table 8: List of Programs (by Research Institutions and Universities)

- Table 9: Impact Analysis of Market Navigating Factors, 2024-2034

- Table 10: Government Initiatives Promoting Green Shipping Across Various Countries and Regions

- Table 11: Wind-Assisted Propulsion Market (by Region), $Million, 2023-2034

- Table 12: Europe Wind-Assisted Propulsion Market (by Application), $Million, 2023-2034

- Table 13: Europe Wind-Assisted Propulsion Market (by Technology), $Million, 2023-2034

- Table 14: Europe Wind-Assisted Propulsion Market (by Installation Type), $Million, 2023-2034

- Table 15: Europe Wind-Assisted Propulsion Market (by Vessel type), $Million, 2023-2034

- Table 16: U.K. Wind-Assisted Propulsion Market (by Application), $Million, 2023-2034

- Table 17: U.K. Wind-Assisted Propulsion Market (by Technology), $Million, 2023-2034

- Table 18: U.K. Wind-Assisted Propulsion Market (by Installation type), $Million, 2023-2034

- Table 19: U.K. Wind-Assisted Propulsion Market (by Vessel type), $Million, 2023-2034

- Table 20: Germany Wind-Assisted Propulsion Market (by Application), $Million, 2023-2034

- Table 21: Germany Wind-Assisted Propulsion Market (by Technology), $Million, 2023-2034

- Table 22: Germany Wind-Assisted Propulsion Market (by Installation type), $Million, 2023-2034

- Table 23: Germany Wind-Assisted Propulsion Market (by Vessel type), $Million, 2023-2034

- Table 24: France Wind-Assisted Propulsion Market (by Application), $Million, 2023-2034

- Table 25: France Wind-Assisted Propulsion Market (by Technology), $Million, 2023-2034

- Table 26: France Wind-Assisted Propulsion Market (by Installation Type), $Million, 2023-2034

- Table 27: France Wind-Assisted Propulsion Market (by Vessel type), $Million, 2023-2034

- Table 28: Greece Wind-Assisted Propulsion Market (by Application), $Million, 2023-2034

- Table 29: Greece Wind-Assisted Propulsion Market (by Technology), $Million, 2023-2034

- Table 30: Greece Wind-Assisted Propulsion Market (by Installation Type), $Million, 2023-2034

- Table 31: Greece Wind-Assisted Propulsion Market (by Vessel type), $Million, 2023-2034

- Table 32: Norway Wind-Assisted Propulsion Market (by Application), $Million, 2023-2034

- Table 33: Norway Wind-Assisted Propulsion Market (by Technology), $Million, 2023-2034

- Table 34: Norway Wind-Assisted Propulsion Market (by Installation Type), $Million, 2023-2034

- Table 35: Norway Wind-Assisted Propulsion Market (by Vessel type), $Million, 2023-2034

- Table 36: Finland Wind-Assisted Propulsion Market (by Application), $Million, 2023-2034

- Table 37: Finland Wind-Assisted Propulsion Market (by Technology), $Million, 2023-2034

- Table 38: Finland Wind-Assisted Propulsion Market (by Installation type), $Million, 2023-2034

- Table 39: Finland Wind-Assisted Propulsion Market (by Vessel type), $Million, 2023-2034

- Table 40: Rest-of-Europe Wind-Assisted Propulsion Market (by Application), $Million, 2023-2034

- Table 41: Rest-of-Europe Wind-Assisted Propulsion Market (by Technology), $Million, 2023-2034

- Table 42: Rest-of-Europe Wind-Assisted Propulsion Market (by Installation Type), $Million, 2023-2034

- Table 43: Rest-of-Europe Wind-Assisted Propulsion Market (by Vessel type), $Million, 2023-2034

- Table 44: Market Share, 2023

Introduction to Europe Wind-Assisted Propulsion Market

The Europe wind-assisted propulsion market was valued at $96.98 million in 2024, and it is expected to grow at a CAGR of 71.69%, reaching $21,586.85 million by 2034. In Europe, wind-assisted propulsion (WAP) is formally integrated into the IMO's Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII), indicating that it is a genuine ""energy harvesting"" technology. Vessels can lower engine load and CO2 emissions by using Flettner rotors, wing sails, or kite systems to transform prevailing winds into direct propulsive drive. However, regional weather variability still has a significant impact on fuel-saving performance: long-term calms or crosswinds can negate the benefits of powerful northerly gales. In order to counteract this, operators are depending more and more on advanced weather-routing systems that incorporate fuel-cost optimisation procedures, vessel-specific performance curves, and real-time weather forecasts. These systems dynamically plot course adjustments that optimise wind leverage without sacrificing schedule.

Despite these operational advancements, commercial adoption is still hampered by a number of interconnected challenges. Rotor-sail installations and rigid wing-sail systems often need capital expenditures in the multi-million dollar range, with payback periods expected to be several years. These timelines conflict with the volatility of the charter market and short contract terms. The lack of uniform engineering and certification standards is another obstacle; each integrator has its own standards for structural strength, control system protocols, and maintenance practices, which hinders bulk production and drives up unit costs. Additionally, class-society assessments and structural reinforcements are often triggered by retrofits, which adds weeks to dry-dock timetables.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2024 - 2034 |

| 2024 Evaluation | $96.98 Million |

| 2034 Forecast | $21,586.85 Million |

| CAGR | 71.69% |

Future projections indicate that unit costs will significantly decrease as WAP hardware develops, production lines expand, and classification societies agree on standard design frameworks. WAP will increasingly function as a complementary ""zero-cost"" thrust source as European shipping decarbonises through the use of green methanol, advanced biofuels, and hydrogen fuel-cell trials. This will increase the range and financial feasibility of alternative-fuel vessels on the North Sea, Baltic, and Mediterranean trade lanes.

Market Introduction

The market for wind-assisted propulsion in Europe includes a variety of technologies intended to use wind energy as an additional source of thrust for commercial ships. In order to save fuel, cut emissions, and increase operational resilience, shipowners and integrators have investigated rotor sails, rigid wing sails, inflatable kites, and other aerodynamic devices within the last ten years. With solutions designed for both new construction and retrofit installations on bulk carriers, tankers, container ships, and ro-ro boats, this expanding market segment connects marine engineering, renewable energy, and digital navigation.

The decarbonisation goals of charterers, classification societies, and governments are becoming more aligned, which has encouraged experimental initiatives along important European trade routes like the North Sea, Baltic Sea, and Mediterranean. Technology companies are also testing hybrid strategies that combine wind turbines with battery storage, shore-power connection, and sophisticated data analytics. While financiers and insurers evaluate risk profiles for large-scale deployments, shipowners, technology providers, and research institutes are collaborating to improve performance modelling and lifecycle assessments.

In the future, the industry will be propelled by corporate sustainability goals, the desire for carbon-neutral corridors, and the wider shift to alternate fuels. Wind-assist devices are set to become a commonplace feature of Europe's greener shipping environment as design standards advance and digital tools simplify installation planning. They will support fuel-switch tactics and open up new avenues for low-carbon maritime transportation.

Market Segmentation:

Segmentation 1: by Application

- Cargo Ships

- Passenger Ships

- Fishing Vessels

- Bulk Carriers

Segmentation 2: by Technology

- Towing Kites

- Sails

- Flettner Rotor

- Suction Wing

- Others

Segmentation 3: by Installation Type

- Retrofit

- New Installation

Segmentation 4: by Vessel Type

- Wind-Assisted Motor Vessels

- Purely Wind Vessel

Segmentation 5: by Region

- Europe: France, U.K., Germany, France, Greece, Norway, Finland, and Rest-of-Europe

Europe Wind-Assisted Propulsion Market Trends, Drivers and Challenges

Trends

- Rapid expansion of wind-assisted propulsion solutions across Europe

- Increasing use of hybrid systems such as rotor sails, wing sails and kites

- Both retrofits on existing vessels and "wind-ready" new builds on the rise

Drivers

- Tightening international and EU emission regulations pushing for lower fuel use

- Rising fossil-fuel costs making wind-assist economically attractive

- Government grants and port incentives supporting adoption

- Investor and customer demand for greener shipping practices

Challenges

- High upfront investment and long payback periods for shipowners

- Lack of uniform standards for measuring performance and savings

- Dependence on weather conditions leading to variable fuel-saving results

- Complexity of integrating new systems into existing ship designs

- Supply-chain constraints for specialized components

How can this report add value to an organization?

The Europe wind-assisted propulsion market offers a comprehensive understanding of the various technologies available based on vessel types (bulk carriers, container ships, passenger vessels, etc.), wind propulsion techniques (sails, rotors, kites, and wing sails), materials (composite materials, fabric sails, and aerodynamics), and methods (retrofit installations, new builds, and hybrid systems). The Europe wind-assisted propulsion market is set for substantial growth with advancements in wind technology, increasing investments, and growing awareness of sustainable shipping. As a result, the wind-assisted propulsion sector is a high-investment and high-revenue market with vast opportunities for expansion.

Growth/Marketing Strategy: The Europe wind-assisted propulsion market has been experiencing rapid growth. It presents significant opportunities for both established and emerging players in the industry. Companies are focusing on strategies such as partnerships, collaborations, technological innovations, and expanding infrastructure to gain a competitive edge. Product development, particularly in terms of advanced wind propulsion systems for different vessel types, is a critical strategy for maintaining market leadership and driving sustainable shipping practices.

Competitive Strategy: Key players in the Europe wind-assisted propulsion market offers various wind-assisted technologies for vessels. Companies are actively pursuing strategic partnerships and collaborations to leverage synergies, improve product offerings, and tap into untapped revenue potential. With increasing regulatory pressure to adopt eco-friendly solutions, the Europe wind-assisted propulsion market is set to witness accelerated growth, benefiting from innovations that drive sustainability in maritime operations.

Key Market Players and Competition Synopsis

The companies that are profiled in the Europe wind-assisted propulsion market have been selected based on inputs gathered from primary experts who have analyzed company coverage, product portfolio, and market penetration.

Some of the prominent names in the market are:

- Norsepower

- bound4blue

- Econowind

- Anemoi Marine Technologies Ltd.

- Airseas

- GT Green Technologies

- Becker Marine Systems

- Propelwind S.A.S.

- SkySails Marine

- DNV

- OCEANBIRD

Table of Contents

Executive Summary

Scope and Definition

1 Markets

- 1.1 Wind-Assisted Propulsion Market: Current and Future

- 1.1.1 Technological Innovations in Shipping Industry

- 1.1.2 Increasing Investment in Wind-Assisted Propulsion

- 1.2 Supply Chain Overview

- 1.2.1 Value Chain Analysis

- 1.2.2 Pricing Analysis

- 1.3 Research and Development Review

- 1.3.1 Patent Filing Trend (by Patent Office and Company)

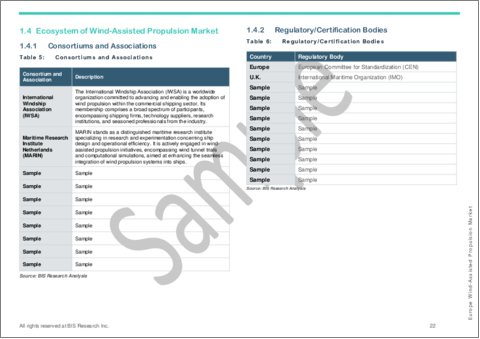

- 1.4 Ecosystem of Wind-Assisted Propulsion Market

- 1.4.1 Consortiums and Associations

- 1.4.2 Regulatory/Certification Bodies

- 1.4.3 Government Programs

- 1.4.4 Programs (by Research Institutions and Universities)

- 1.5 Economic Impact of Wind-Assisted Propulsion

- 1.6 Market Dynamics: Overview

- 1.6.1 Market Drivers

- 1.6.1.1 Fluctuations in Raw Material Prices

- 1.6.1.2 Growing Adoption of Retrofitting Solutions

- 1.6.2 Market Restraints

- 1.6.2.1 Regulatory Barriers to Large-Scale Dual-Fuel Retrofitting

- 1.6.2.2 Space and Structural Limitations on Ships

- 1.6.3 Market Opportunities

- 1.6.3.1 Investments and Government Support for Green Shipping

- 1.6.3.2 Expansion of Green Shipping Corridors

- 1.6.1 Market Drivers

- 1.7 Start-Up Landscape

2 Regions

- 2.1 Wind-Assisted Propulsion Market (by Region)

- 2.2 Europe

- 2.2.1 Market

- 2.2.1.1 Key Market Participants in Europe

- 2.2.1.2 Business Drivers

- 2.2.1.3 Business Challenges

- 2.2.2 Application

- 2.2.3 Product

- 2.2.4 Europe (by Country)

- 2.2.4.1 U.K.

- 2.2.4.1.1 Application

- 2.2.4.1.2 Product

- 2.2.4.2 Germany

- 2.2.4.2.1 Application

- 2.2.4.2.2 Product

- 2.2.4.3 France

- 2.2.4.3.1 Application

- 2.2.4.3.2 Product

- 2.2.4.4 Greece

- 2.2.4.4.1 Application

- 2.2.4.4.2 Product

- 2.2.4.5 Norway

- 2.2.4.5.1 Application

- 2.2.4.5.2 Product

- 2.2.4.6 Finland

- 2.2.4.6.1 Application

- 2.2.4.6.2 Product

- 2.2.4.7 Rest-of-Europe

- 2.2.4.7.1 Application

- 2.2.4.7.2 Product

- 2.2.4.1 U.K.

- 2.2.1 Market

3 Markets- Competitive Benchmarking and Companies Profiled

- 3.1 Next Frontiers

- 3.2 Company Profiles

- 3.2.1 Norsepower

- 3.2.1.1 Overview

- 3.2.1.2 Top Products/Product Portfolio

- 3.2.1.3 Top Competitors

- 3.2.1.4 End-Use Applications

- 3.2.1.5 Key Personnel

- 3.2.1.6 Analyst View

- 3.2.1.7 Market Share, 2023

- 3.2.2 bound4blue

- 3.2.2.1 Overview

- 3.2.2.2 Top Products/Product Portfolio

- 3.2.2.3 Top Competitors

- 3.2.2.4 End-Use Applications

- 3.2.2.5 Key Personnel

- 3.2.2.6 Analyst View

- 3.2.2.7 Market Share, 2023

- 3.2.3 Econowind

- 3.2.3.1 Overview

- 3.2.3.2 Top Products/Product Portfolio

- 3.2.3.3 Top Competitors

- 3.2.3.4 End-Use Applications

- 3.2.3.5 Key Personnel

- 3.2.3.6 Analyst View

- 3.2.3.7 Market Share, 2023

- 3.2.4 Anemoi Marine Technologies Ltd.

- 3.2.4.1 Overview

- 3.2.4.2 Top Products/Product Portfolio

- 3.2.4.3 Top Competitors

- 3.2.4.4 End-Use Applications

- 3.2.4.5 Key Personnel

- 3.2.4.6 Analyst View

- 3.2.4.7 Market Share, 2023

- 3.2.5 Airseas

- 3.2.5.1 Overview

- 3.2.5.2 Top Products/Product Portfolio

- 3.2.5.3 Top Competitors

- 3.2.5.4 End-Use Applications

- 3.2.5.5 Key Personnel

- 3.2.5.6 Analyst View

- 3.2.5.7 Market Share, 2023

- 3.2.6 GT Green Technologies

- 3.2.6.1 Overview

- 3.2.6.2 Top Products/Product Portfolio

- 3.2.6.3 Top Competitors

- 3.2.6.4 End-Use Applications

- 3.2.6.5 Key Personnel

- 3.2.6.6 Analyst View

- 3.2.6.7 Market Share, 2023

- 3.2.7 Becker Marine Systems

- 3.2.7.1 Overview

- 3.2.7.2 Top Products/Product Portfolio

- 3.2.7.3 Top Competitors

- 3.2.7.4 End-Use Applications

- 3.2.7.5 Key Personnel

- 3.2.7.6 Analyst View

- 3.2.7.7 Market Share, 2023

- 3.2.8 Propelwind S.A.S.

- 3.2.8.1 Overview

- 3.2.8.2 Top Products/Product Portfolio

- 3.2.8.3 Top Competitors

- 3.2.8.4 End-Use Applications

- 3.2.8.5 Key Personnel

- 3.2.8.6 Analyst View

- 3.2.8.7 Market Share, 2023

- 3.2.9 SkySails Marine

- 3.2.9.1 Overview

- 3.2.9.2 Top Products/Product Portfolio

- 3.2.9.3 Top Competitors

- 3.2.9.4 End-Use Applications

- 3.2.9.5 Key Personnel

- 3.2.9.6 Analyst View

- 3.2.9.7 Market Share, 2023

- 3.2.10 DNV

- 3.2.10.1 Overview

- 3.2.10.2 Top Products/Product Portfolio

- 3.2.10.3 Top Competitors

- 3.2.10.4 End-Use Application

- 3.2.10.5 Key Personnel

- 3.2.10.6 Analyst View

- 3.2.10.7 Market Share, 2023

- 3.2.11 OCEANBIRD

- 3.2.11.1 Overview

- 3.2.11.2 Top Products/Product Portfolio

- 3.2.11.3 Top Competitors

- 3.2.11.4 Target Customers/End Users

- 3.2.11.5 Key Personnel

- 3.2.11.6 Analyst View

- 3.2.11.7 Market Share, 2023

- 3.2.1 Norsepower

4 Research Methodology

- 4.1 Data Sources

- 4.1.1 Primary Data Sources

- 4.1.2 Secondary Data Sources

- 4.1.3 Data Triangulation

- 4.2 Market Estimation and Forecast