|

|

市場調査レポート

商品コード

1644937

欧州の大型風力タービン-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Europe Large Wind Turbine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州の大型風力タービン-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

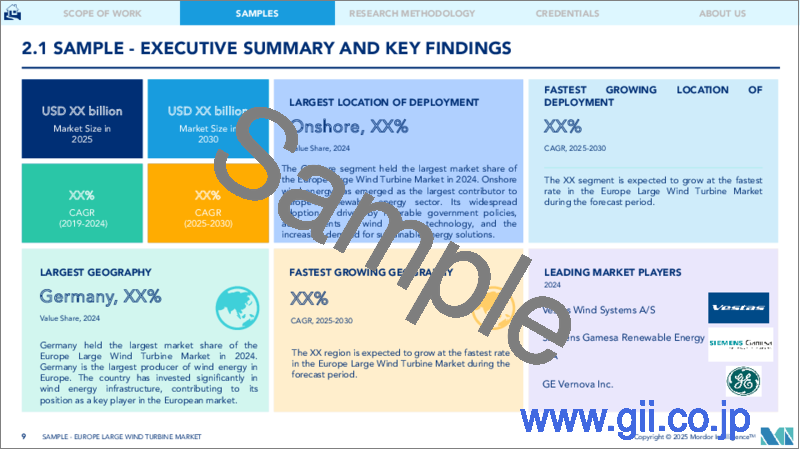

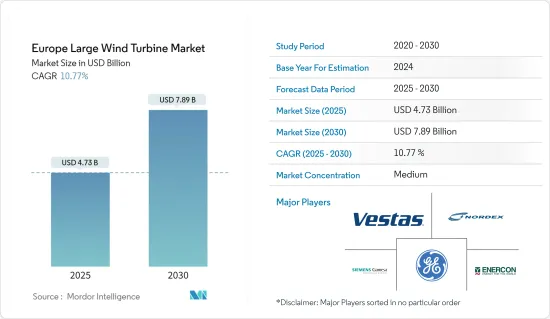

欧州の大型風力タービン市場規模は2025年に47億3,000万米ドルと推定され、2030年には78億9,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは10.77%です。

主要ハイライト

- 中期的には、風力発電プロジェクトに対する投資の増加や有利な政府施策などの要因が、予測期間中の欧州の大型風力タービン市場を牽引すると予測されます。

- 一方、クリーン発電の代替電源、主に天然ガス発電や太陽光発電の採用が増加しており、予測期間中の欧州の大型風力タービン市場の需要を妨げると予想されます。

- 洋上風力発電プロジェクトの開発は、予測期間中、欧州の大型風力タービン市場に大きなビジネス機会をもたらすと期待されています。

- ドイツは近年、大型風力タービン市場を独占しています。政府の施策と相まって風力発電プロジェクトが増加しているため、予測期間中に大きな市場成長が見込まれます。

欧州の大型風力タービン市場動向

市場を独占する陸上セグメント

- 陸上風力発電技術は、設置されたメガワット容量あたりの発電量を最大化し、風速の低い場所をより多くカバーするために、過去5年間で進化してきました。これに加え、近年では、風力タービンのハブ高が高くなり、直径が広くなり、風力タービンのブレードが大きくなっています。

- 欧州では、新規風力発電の81%以上が陸上風力発電で、約1405万kWです。スウェーデン、ドイツ、トルコが最も多くの陸上風力発電設備を建設しています。2022年、ドイツは新規風力発電所への投資において欧州のリーダーでした。同年、ドイツは新規風力発電プロジェクトに26億米ドルを投資し、そのすべてが陸上風力発電設備に向けられました。

- 過去1年間、スウェーデンの陸上風力発電設備は前年比2倍以上に増加し、記録的な風力発電設備数となりました。現在、スウェーデンの陸上風力発電容量は欧州で最も多く、210万kWの陸上風力発電設備が新たに設置されています。

- 2022年7月、スウェーデンでは2025年から新たに277MWの風力発電所を建設するプロジェクトが発表されました。プロジェクトを担当するのは3社で、Siemens・ガメサ、アライズ、フォーサイトがスウェーデンの新規プロジェクトで協力するようです。

- スウェーデン政府は、2030年までに電力ミックスに占める再生可能エネルギーの割合を40%まで引き上げることを計画しています。政府は、再生可能エネルギーへの支出を年間54億米ドルから87億米ドルに増やすと発表しました。このことが、予測期間中の大型風力タービンローター市場の成長を後押しすることになりそうです。

- さらに、WindEuropeによると、陸上風力エネルギーは、2030年までに正味炭素排出量ゼロを達成するために、欧州の市場需要をリードするといいます。GWECによると、陸上風力エネルギー容量は風力エネルギー全体の約90%を占めています。二酸化炭素排出量を削減し、従来の電力システムを段階的に廃止するための厳しい政府規制が、市場を牽引すると予想されます。

- したがって、この地域のこうした開発は、予測期間中、大型風力タービン市場をサポートすると予想されます。

市場を独占するドイツ

- ドイツは風力発電が盛んです。洋上風力発電所の増加は、陸上風力発電に比べて風速が速いため、有利な市場となっています。そのため、洋上風力発電は大きな成長が見込まれています。

- また、ドイツ政府、沿岸諸国、送電システムオペレーター(TSOs)は、北海とバルト海における洋上風力開発を拡大し、同国の洋上設備容量目標を2030年までに20GWに引き上げる共同計画に合意しました。これは、大型風力タービンのローター市場の成長につながります。

- WindEuropeによると、2021年時点で欧州には236GWの風力発電容量が設置されています。ドイツが引き続き最大の設置容量を持ち、スペイン、英国、フランス、スウェーデンがこれに続きます。

- 2022年末時点で、ドイツの陸上風力タービンの総数は28,443基です。また、2022年には2.4GWの容量を持つ551基の陸上風力タービンが新たに設置されました。陸上風力発電の総設備容量は5816万kWです。

- 欧州連合(EU)の風力発電による発電量は、2022年には合計419.5テラワット時となりました。これは前年比で約8.4%の増加です。EU加盟国の中で風力発電による発電量が最も多かったのはドイツで、同年の発電量は約125テラワット時でした。

- 2022年6月、ドイツ議会は新しい陸上風力発電法、i.WindLandGを採択し、2025年から年間10GWの大規模な陸上風力発電所の開発を目指しました。これはドイツの「イースター包装」と呼ばれる施策の一部であり、自然エネルギーの拡大が最優先の公共の利益であるという原則を明文化したものです。

- したがって、上記の点を考慮すると、予測期間中はドイツが市場を独占する可能性が高いです。

欧州の大型風力タービン産業概要

欧州の大型風力タービン市場は半セグメント化しています。バイオガス市場の主要企業(順不同)には、Vestas Wind Systems A/S、Nordex SE、Siemens Gamesa Renewable Energy S.A.、Enercon GmbH、General Electric Companyなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 風力発電プロジェクトへの投資の増加

- 有利な政府施策

- 抑制要因

- クリーンな発電のための代替電源の採用拡大

- 促進要因

- サプライチェーン分析

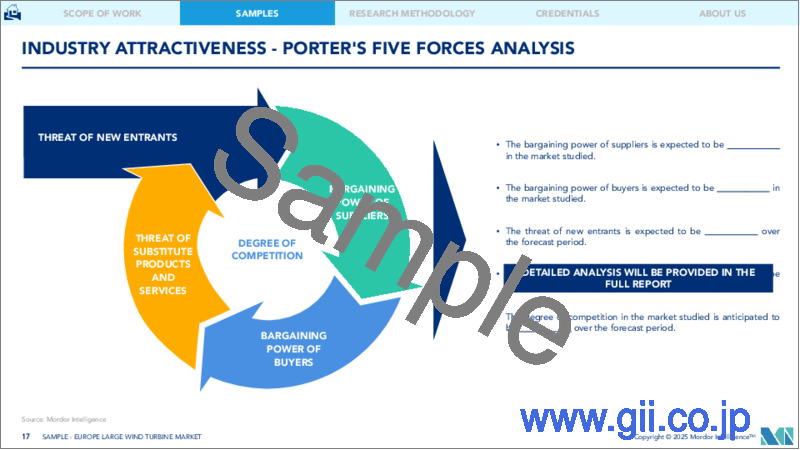

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 展開場所

- 陸上

- 洋上

- 地域

- ドイツ

- フランス

- スペイン

- 北欧

- トルコ

- ロシア

- その他の欧州

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Vestas Wind Systems A/S

- Nordex SE

- Siemens Gamesa Renewable Energy S.A

- Enercon GmbH

- General Electric Company

- Suzlon Energy Limited

- Vensys Energy AG

- Xinjiang Goldwind Science & Technology Co., Ltd.

- JSC NovaWind

- Envision Energy

- Market Player Ranking

第7章 市場機会と今後の動向

- 洋上風力エネルギーの積極的成長

目次

Product Code: 93219

The Europe Large Wind Turbine Market size is estimated at USD 4.73 billion in 2025, and is expected to reach USD 7.89 billion by 2030, at a CAGR of 10.77% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as increasing investments in wind power projects and favorable government policies are anticipated to drive the Europe large wind turbine market during the forecast period.

- On the other hand, the growing adoption of alternate sources of clean power generation, mainly natural gas power and solar power is expected to hamper the demand for the Europe large wind turbine market during the forecast period.

- Nevertheless, the offoshore wind energy projects development are expected to create considerable opportunities for the Europe large wind turbine market during the forecast period.

- Germany is expected to dominate the large turbine wind market in recent years. It is expected to witness significant market growth in the forecast period due to the increasing wind energy projects coupled with the government's policies.

Europe Large Wind Turbine Market Trends

Onshore Segment to Dominate the Market

- Onshore wind energy power generation technology has evolved over the last five years to maximize electricity produced per megawatt capacity installed and to cover more sites with lower wind speeds. Besides this, in recent years, wind turbines have become more extensive with taller hub heights, broader diameters, and larger wind turbine blades.

- In Europe, over 81% of the new wind installations were the onshore wind, with around 14.05 GW. Sweden, Germany, and Turkey are building the most onshore wind installations. In 2022, Germany was the European leader in terms of investment in new wind farms. That year, Germany invested USD 2.6 billion in new wind projects, all of which went toward onshore wind installations.

- During the past year, Sweden has seen a record number of wind installations as onshore installations have more than doubled year-over-year. Sweden now has the most onshore wind capacity in Europe, with 2.1 GW of new onshore installations.

- In July 2022, a project was announced in Sweden to build a new 277 MW wind farm starting in 2025. Three companies will be in charge of the project; Siemens Gamesa, Arise and Foresight are likely to collaborate on a new project in Sweden.

- Sweden government has planned to increase the share of renewable energy in the power mix to 40% by 2030. The government announced an increase in the expenditure on renewables, from USD 5.4 billion to USD 8.7 billion annually. This, in turn, is likely to aid the growth of the large wind turbine rotor market during the forecast period.

- Furthermore, according to WindEurope, onshore wind energy will lead the market demand in the European region to achieve net-zero carbon emissions by 2030. According to GWEC, onshore wind energy capacity takes around 90% of the total wind energy. The strict government regulations to reduce carbon emissions and phase out conventional power systems are expected to drive the market.

- Thus, such developments in the region are expected to support the large wind turbine market during the forecast period.

Germany to Dominate the Market

- Germany is rich in wind power generation. Growing wind power plants in the offshore area are becoming a lucrative market due to higher wind speed in comparison to onshore wind. Thus, offshore wind-based electricity generation is expected to witness significant growth.

- Also, the German government, coastal states, and transmission system operators (TSOs) have agreed on a joint plan to expand offshore wind development in the North and Baltic Seas and lift the country's offshore installed capacity target to 20 GW by 2030. This in turn culminates in the growth of the large wind turbine rotor market.

- According to WindEurope, as of 2021, 236 GW of wind energy capacity is installed in Europe. Germany continues to have the largest installed capacity, followed by Spain, the United Kingdom, France, and Sweden.

- At the end of the year 2022, there were a total of 28,443 onshore wind turbines in Germany. Also, 551 new onshore wind turbines with a capacity of 2.4 GW were newly installed in the year 2022. The total installed capacity of onshore wind energy is 58.106 GW.

- The amount of electricity generated from wind power in the European Union (EU) totaled 419.5 terawatt hours in 2022. This was an increase of about 8.4 percent in comparison to the previous year. Among EU member states, Germany produced the most electricity from wind power, generating nearly 125 terawatt hours that same year..

- In June 2022, the German Parliament adopted a new Onshore Wind Law, i.e., WindLandG, which aims to develop onshore wind-based power plants by a massive 10 GW a year starting from 2025. It's part of Germany's "Easter Package" of measures that enshrines the principle that the expansion of renewables is a matter of overriding public interest.

- Therefore considering the above-mentioned points, Germany is likely to dominate the market during the forecast period.

Europe Large Wind Turbine Industry Overview

Europe Large Wind Turbine Market is semi fragmented. Some of the key players in the biogas market (not in particular order) include Vestas Wind Systems A/S, Nordex SE, Siemens Gamesa Renewable Energy S.A., Enercon GmbH, and General Electric Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 The Increasing Investments in Wind Power Projects

- 4.5.1.2 Favorable Government Policies

- 4.5.2 Restraints

- 4.5.2.1 The Growing Adoption of Alternate Sources of Clean Power Generation

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Geography

- 5.2.1 Germany

- 5.2.2 France

- 5.2.3 Spain

- 5.2.4 NORDIC

- 5.2.5 Turkey

- 5.2.6 Russia

- 5.2.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Vestas Wind Systems A/S

- 6.3.2 Nordex SE

- 6.3.3 Siemens Gamesa Renewable Energy S.A

- 6.3.4 Enercon GmbH

- 6.3.5 General Electric Company

- 6.3.6 Suzlon Energy Limited

- 6.3.7 Vensys Energy AG

- 6.3.8 Xinjiang Goldwind Science & Technology Co., Ltd.

- 6.3.9 JSC NovaWind

- 6.3.10 Envision Energy

- 6.4 Market Player Ranking

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Aggressive Growth of Offshore Wind Energy