|

市場調査レポート

商品コード

1644986

北米の大型風力タービン:市場シェア分析、産業動向・統計、成長予測(2025~2030年)North America Large Wind Turbine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の大型風力タービン:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

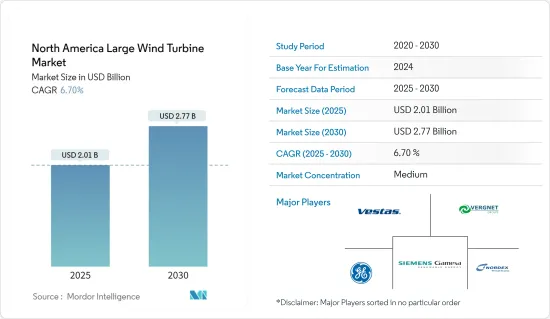

北米の大型風力タービン市場規模は2025年に20億1,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは6.7%で、2030年には27億7,000万米ドルに達すると予測されます。

主なハイライト

- 中期的には、コスト削減と風力エネルギーへの投資の増加が市場の成長を牽引するとみられます。

- 一方、太陽光などの代替クリーンエネルギーの採用が大型風力タービン市場の成長を抑制する可能性が高いです。

- とはいえ、世界風力エネルギー協議会(Global Wind Energy Council)は、2030年までに380GW、2050年までに2,000GWの洋上風力発電を世界で実現することを約束しており、市場関係者にとっては大きなチャンスとなりそうです。

- 米国は市場を独占しており、風力エネルギー投資の増加と電力需要の増加により、予測期間中に最も高いCAGRで推移する可能性が高いです。

北米の大型風力タービン市場動向

オフショアセグメントが急成長

- クリーンエネルギーへの需要が高まる中、国や企業は再生可能エネルギー、特に風力エネルギーを採用しています。

- 洋上風力タービンは、陸上風力タービンよりもはるかに頑丈な素材を必要とし、一般に陸上風力タービンよりも大型です。したがって、洋上風力タービン産業の成長は市場に大きな影響を与えると予想されます。

- カナダ政府は、2025年までに風力発電容量を55GWまで増やし、同国のエネルギー需要の20%を満たすことを目指しています。しかし、目標を達成するためには、まだ42GW以上の新規容量を追加しなければならないです。このことは、風力発電プロジェクト開発者にとって投資機会となることが期待されます。

- カリフォルニア州のフンボルト湾港は、フンボルト・コール地区で予定されている160万kWの洋上風力発電開発を支援するため、港の改修に1,050万米ドルの投資を受けました。

- 国際再生可能エネルギー機関(IRENA)によると、2022年の洋上風力発電設備容量は41MWでした。

- したがって、上記の点から、オフショア分野への投資の増加が予測期間中の市場を牽引すると思われます。

市場を独占する米国

- 米国風力エネルギー協会によると、米国の風力発電設備容量は大幅に増加しました。この拡大は、主にテキサス州の顕著かつ継続的な陸上風力発電ブームによるものです。テキサス州は全米の風力発電容量の4分の1以上を占めています。

- 米国の風力発電部門は、国内エネルギー生産の拡大を目指すアメリカ・ファースト政策により、政府から絶大な支援を受けています。洋上風力発電分野は、同国が広大な沿岸域をリース対象としていることから、重要な開発分野と考えられています。

- 2021年3月、米国は内務省(DOI)、エネルギー省(DOE)、商務省(DOC)の共同発表によると、2030年までに30GWの洋上風力を導入することを決定しました。さらに、7,800万トンのCO2排出量を削減し、1,000万世帯以上のアメリカの家庭の1年分の電力を賄うことができます。

- 多くの風力発電プロジェクトを後押しする政府の好意的な政策は、この地域の風力タービン市場を拡大すると予想されます。例えば、2021年11月、シーメンス・エナジーはオーステッド社とエバーソース社から、924メガワットの洋上風力発電所にトランスミッションを提供することを承認されました。モントーク・ポイントから30マイル以上東に位置するこの施設からは、ニューヨークの約60万世帯に電力が供給される予定です。運転開始は2025年の予定。

- 2022年末現在、米国で最も風力発電の累積容量が多い州はテキサス州です。当時、テキサス州の設備容量は約4000万kWで、次点のアイオワ州の3倍以上だった。同年の風力発電設備容量が10GWを超えたのは、わずか3州だけだった。

- 以上のことから、米国は予測期間中、大型風力タービン市場で大きな成長を遂げると予想されます。

北米の大型風力タービン産業概要

北米の大型風力タービン市場は半断片化しています。この市場の主要企業(順不同)には、General Electric Company、Vestas Wind Systems AS、Siemens Gamesa Renewable Energy SA、Nordex SE、Vergnet VSA SAなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 風力エネルギーのコスト削減

- 風力エネルギーへの投資の増加

- 抑制要因

- 太陽光などの代替クリーンエネルギー源の採用

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 展開場所別

- オンショア

- オフショア

- 地域別

- 米国

- カナダ

- その他北米地域

第6章 競争情勢

- 合併、買収、提携、合弁事業

- 主要企業の戦略

- 企業プロファイル

- Vestas Wind Systems A/S

- Siemens Gamesa Renewable Energy, S.A.

- General Electric Company

- Nordex SE

- Envision Group

- Enercon GmbH

- Hitachi, Ltd.

- Vergnet VSA SA

- Orsted AS

- Duke Energy Corporation

- NextEra Energy Inc.

第7章 市場機会と今後の動向

- 野心的な風力エネルギー目標

目次

Product Code: 5000235

The North America Large Wind Turbine Market size is estimated at USD 2.01 billion in 2025, and is expected to reach USD 2.77 billion by 2030, at a CAGR of 6.7% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, reducing costs and increasing investment in wind energy is likely to drive the market's growth.

- On the other hand, adoption of alternative clean energy sources like solar and other alternatives will likely restrain the growth of the large wind turbine market.

- Nevertheless, the Global Wind Energy Council committed to achieving 380 GW of offshore wind by 2030 and 2,000 GW by 2050 worldwide, likely providing significant opportunities for the market player.

- The United States dominates the market and is also likely to witness the highest CAGR during the forecast period, owing to the increasing wind energy investments and growing electricity demand.

North America Large Wind Turbine Market Trends

Offshore Segment Is the Fastest Growth Segment

- With the increasing demand for clean energy, countries and companies are adopting renewable energy sources, especially wind energy, as they can provide clean energy and help carbon emission missions by 2050.

- Offshore wind turbines require a much sturdier material than onshore wind turbines and are generally larger than onshore wind turbines. Hence, the offshore wind turbine industry's growth is expected to significantly impact the market.

- In Canada, the government aims to increase the wind power capacity to 55 GW by 2025 to meet 20% of the country's energy needs. However, the country must still add more than 42 GW of new capacity to meet the targets. This, in turn, is expected to provide investment opportunities for wind project developers.

- The Port of Humboldt Bay in California has received USD 10.5 million in investment for the port's renovation to support the intended 1.6 GW of offshore wind development in the Humboldt Call area.

- According to International Renewable Energy Agency (IRENA), the total offshore installed wind capacity was 41 MW in 2022.

- Hence, owing to the above points, increasing investment in the offshore segment is likely to drive the market during the forecast period.

United States to Dominate the Market

- According to the American Wind Energy Association, the total installed wind generating capacity in the United States increased significantly. This expansion was caused mainly by Texas's remarkable and ongoing onshore wind boom. Texas has over a quarter of the nation's total wind energy capacity.

- The United States wind power sector is receiving immense support from the government due to the America First policy, which aims to boost domestic energy production. The offshore wind power sector is considered a significant development area, as the country has a large coastal area for leasing.

- In March 2021, the United States decided to deploy 30 GW of offshore wind by 2030, according to a joint announcement from the Departments of Interior (DOI), Energy (DOE), and Commerce (DOC). Additionally, it produces 78 million metric tons less CO2 emissions and enough electricity to provide more than 10 million American homes for a whole year.

- Favorable government policies raising many wind power projects are expected to increase the wind turbine market in the region. For instance, in November 2021, Siemens Energy was approved by Orsted and Eversource to provide the transmission system for a 924-Megawatt offshore wind farm. Nearly 600,000 New York homes will be powered by the facility more than 30 miles east of Montauk Point. It is scheduled to begin operating in 2025.

- As of the end of 2022, Texas was the United States state with the highest cumulative wind power capacity. At the time, it had around 40 GW of installed capacity, over three times that of runner-up Iowa. Only three states had more than 10 GW of installed wind capacity in the same year.

- Hence, owing to the above points, the United States is expected to see significant growth in the Large Wind Turbine market during the forecast period.

North America Large Wind Turbine Industry Overview

The North American Large Wind Turbine market is semi fragmented. Some of the key players in this market (in no particular order) include General Electric Company, Vestas Wind Systems AS, Siemens Gamesa Renewable Energy SA, Nordex SE, and Vergnet VSA SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Reducing Costs of Wind Energy

- 4.5.1.2 Increasing Investment in Wind Energy

- 4.5.2 Restraints

- 4.5.2.1 Adoption of Alternative Clean Energy Sources like Solar and Others

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Force Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.2 Geography

- 5.2.1 United States

- 5.2.2 Canada

- 5.2.3 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Collaboration and Joint Ventures

- 6.2 Strategies Adopted by Key Players

- 6.3 Company Profiles

- 6.3.1 Vestas Wind Systems A/S

- 6.3.2 Siemens Gamesa Renewable Energy, S.A.

- 6.3.3 General Electric Company

- 6.3.4 Nordex SE

- 6.3.5 Envision Group

- 6.3.6 Enercon GmbH

- 6.3.7 Hitachi, Ltd.

- 6.3.8 Vergnet VSA SA

- 6.3.9 Orsted AS

- 6.3.10 Duke Energy Corporation

- 6.3.11 NextEra Energy Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Ambitious Wind Energy Targets