|

|

市場調査レポート

商品コード

1484378

欧州の電気自動車用バッテリー形成・試験市場:車両タイプ別、用途別、電池化学別、展開方法別、調達別、試験タイプ別、国別:分析と予測(2023年~2032年)Europe Electric Vehicle Battery Formation and Testing Market: Focus on Vehicle Type, Application, Battery Chemistry, Deployment Method, Sourcing, Testing Type, and Country - Analysis and Forecast, 2023-2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 欧州の電気自動車用バッテリー形成・試験市場:車両タイプ別、用途別、電池化学別、展開方法別、調達別、試験タイプ別、国別:分析と予測(2023年~2032年) |

|

出版日: 2024年05月28日

発行: BIS Research

ページ情報: 英文 95 Pages

納期: 1~5営業日

|

全表示

- 概要

- 図表

- 目次

欧州の電気自動車用バッテリー形成・試験の市場規模(英国を除く)は、2023年に2億2,760万米ドルとなりました。

同市場は今後、16.76%のCAGRで拡大し、2032年には9億1,770万米ドルに達すると予測されています。同市場の成長は、電気自動車(EV)の需要増加とEVバッテリーの安全性、信頼性、性能を検証する必要性によって推進されると予測されています。EVの普及が急速に加速する中、バッテリーメーカーは厳格な安全基準を遵守した高品質のバッテリーを製造するという課題に直面しています。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2023年~2032年 |

| 2023年の評価額 | 2億2,760万米ドル |

| 2032年予測 | 9億1,770万米ドル |

| CAGR | 16.76% |

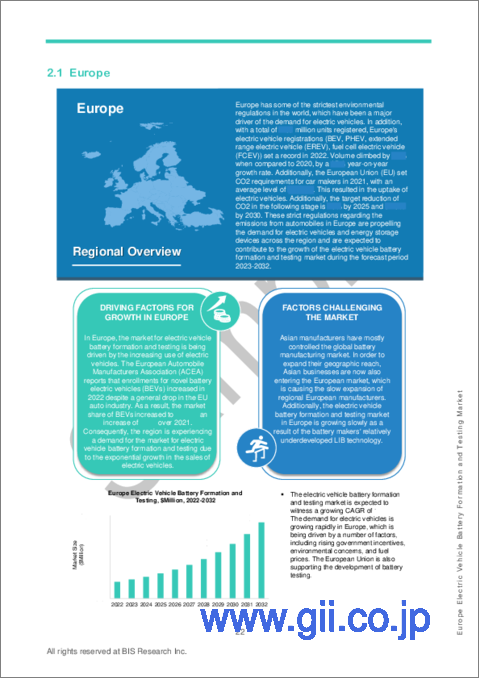

欧州の電気自動車(EV)用バッテリー形成と試験に関する市場は、EUの厳しい排出ガス規制と電動化への強い後押しを受けて、力強い成長を遂げています。欧州諸国がカーボンフットプリントの削減に取り組む中、EVの需要が急増しており、安全性と性能基準を確保するために高度なバッテリー試験と形成プロセスが必要とされています。この地域の主要企業は、バッテリーの寿命と効率を高める試験手法を革新するため、研究開発に多額の投資を行っています。さらに、自動車メーカーと技術プロバイダーとの協力関係が、最先端の試験施設の開発を促進しています。この市場はさらに、EV導入に対する政府の優遇措置やハイテク製造拠点の設立によって支えられており、欧州は持続可能な輸送手段へのシフトにおけるリーダーとしての地位を確立しています。

当レポートでは、欧州の電気自動車用バッテリー形成・試験市場について調査し、市場の概要とともに、車両タイプ別、用途別、電池化学別、展開方法別、調達別、試験タイプ別、国別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

エグゼクティブサマリー

調査範囲

第1章 市場

- 業界展望

- ビジネスダイナミクス

第2章 地域

- 欧州

- 英国

第3章 市場- 競合ベンチマーキングと企業プロファイル

- 競合ベンチマーキング

- 市場シェア分析

- 製品/サービスマトリックス

- 企業プロファイル

- Siemens AG

- ABB

- SAP SE

- Dassault Systemes

- AVEVA Group Limited

- Tulip Batteries

- TUV SUD

- Infineon Technologies AG

- Element Materials Technology

- その他の主要企業

第4章 調査手法

List of Figures

- Figure 1: Europe Electric Vehicle Battery Formation and Testing Market, $Billion, 2022-2032

- Figure 2: Europe Electric Vehicle Battery Formation and Testing Market (by Vehicle Type), $Million, 2022-2032

- Figure 3: Europe Electric Vehicle Battery Formation and Testing Market (by Application), $Million, 2022-2032

- Figure 4: Europe Electric Vehicle Battery Formation and Testing Market (by Battery Chemistry), $Million, 2022-2032

- Figure 5: Europe Electric Vehicle Battery Formation and Testing Market (by Sourcing Type), $Million, 2022-2032

- Figure 6: Europe Electric Vehicle Battery Formation and Testing Market (by Deployment Method), $Million, 2022-2032

- Figure 7: Europe Electric Vehicle Battery Formation and Testing Market (by Testing Type), $Million, 2022-2032

- Figure 8: Electric Vehicle Battery Formation and Testing Market (by Region), 2022

- Figure 9: Technology Roadmap for Electric Vehicle Battery Formation and Testing Market

- Figure 10: Total Number of Patent Filed (by Year), January 2020-October 2023

- Figure 11: Patent Analysis (by Status), January 2020-October 2023

- Figure 12: Electric Vehicle Sales Worldwide, 2020-2028

- Figure 13: Electric Vehicle Battery Formation and Testing Market: Competitive Benchmarking, 2022

- Figure 14: Siemens AG: Product Portfolio

- Figure 15: ABB: Product Portfolio

- Figure 16: SAP SE: Product Portfolio

- Figure 17: Dassault Systemes: Product Portfolio

- Figure 18: AVEVA Group Limited: Product Portfolio

- Figure 19: Tulip Batteries: Product Portfolio

- Figure 20: TUV SUD: Product Portfolio

- Figure 21: Infineon Technologies AG: Product Portfolio

- Figure 22: Element Materials Technology: Product Portfolio

- Figure 23: Research Methodology

- Figure 24: Data Triangulation

- Figure 25: Top-Down and Bottom-Up Approach

- Figure 26: Assumptions and Limitations

List of Tables

- Table 1: Europe Electric Vehicle Battery Formation and Testing Market, Overview

- Table 2: Key Companies Profiled

- Table 3: Consortiums, Associations, and Regulatory Bodies

- Table 4: Government Initiatives

- Table 5: Programs by Research Institutions and Universities

- Table 6: Impact of Business Drivers

- Table 7: Impact of Business Restraints

- Table 8: Electric Vehicle Battery Formation and Testing Market (by Region), $Million, 2022-2032

- Table 9: Electric Vehicle Battery Formation and Testing Market Share Analysis, 2022

- Table 10: Electric Vehicle Battery Formation and Testing Market: Product Matrix

Introduction to Europe Electric Vehicle Battery Formation and Testing Market

The Europe electric vehicle battery formation and testing market (excluding U.K.) was valued at $227.6 million in 2023, and it is expected to grow at a CAGR of 16.76% and reach $917.7 million by 2032. The growth of the electric vehicle battery formation and testing market is anticipated to be propelled by the increasing demand for electric vehicles (EVs) and the necessity to verify the safety, reliability, and performance of EV batteries. With the rapid acceleration in EV adoption, battery manufacturers face the challenge of producing high-quality batteries that adhere to rigorous safety standards.

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2023 - 2032 |

| 2023 Evaluation | $227.6 Million |

| 2032 Forecast | $917.7 Million |

| CAGR | 16.76% |

Market Introduction

The Europe market for electric vehicle (EV) battery formation and testing is experiencing robust growth, driven by stringent EU regulations on emissions and a strong push towards electrification. As European nations commit to reducing their carbon footprint, the demand for EVs has surged, necessitating advanced battery testing and formation processes to ensure safety and performance standards. Key players in the region are investing heavily in R&D to innovate testing methodologies that enhance battery life and efficiency. Moreover, collaborations between automotive manufacturers and technology providers are fostering the development of state-of-the-art testing facilities. This market is further supported by government incentives for EV adoption and the establishment of high-tech manufacturing hubs, positioning Europe as a leader in the shift towards sustainable transportation.

Market Segmentation:

Segmentation 1: by Application

- Manufacturing

- Testing

Segmentation 2: by Vehicle Type

- Passenger Vehicle

- Commercial Vehicle

Segmentation 3: by Battery Chemistry

- Lithium-Ion

- Others

Segmentation 4: by Sourcing Type

- In-house

- Outsourcing

Segmentation 5: by Deployment Method

- Cloud-Based

- On-Premises

Segmentation 6: by Testing Type

- Mechanical Tests

- Thermal Tests

- Electrical Tests

- Others

Segmentation 7: by Country

- Germany

- Hungary

- Poland

- Sweden

- Rest-of-Europe

How can this report add value to an organization?

Product/Innovation Strategy: The product/innovation strategy for companies in the electric vehicle battery formation and testing market should focus on continuous improvement, differentiated solutions, collaboration, automation, cost reduction, regulatory compliance, talent acquisition, and intellectual property protection. Companies should continuously invest in research and development to stay ahead of the curve, develop specialized testing equipment, partner with industry stakeholders, leverage automation and data analytics, focus on cost-effective battery chemistries, stay informed on regulatory standards, attract, and retain top talent, and protect their intellectual property. By following these key strategies, companies can position themselves for success in this growing and dynamic market.

Growth/Marketing Strategy: The electric vehicle battery formation and testing market has been growing at a rapid pace. The market offers enormous opportunities for existing and emerging market players. Some of the strategies covered in this segment are mergers and acquisitions, product launches, partnerships and collaborations, business expansions, and investments. The strategies preferred by companies to maintain and strengthen their market position primarily include partnerships, agreements, and collaborations.

Competitive Strategy: The competitive strategy for companies in the electric vehicle battery formation and testing market should be focused on differentiation, cost leadership, and customer focus. Companies should differentiate their products and services by developing specialized testing equipment, offering value-added services, and collaborating with industry partners. They should also focus on cost reduction by developing more efficient manufacturing processes and using less expensive materials. Finally, companies should focus on providing excellent customer service and support to build strong customer relationships. By focusing on these three key areas, companies can gain a competitive edge in the electric vehicle battery formation and testing market.

Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on inputs gathered from primary experts and analyzing company coverage, product portfolio, and regional presence.

Some of the prominent names in this market are:

- Siemens AG

- ABB

- SAP SE

- Dassault Systemes

- Tulip Batteries

- TUV SUD

- Infineon Technologies AG

Table of Contents

Executive Summary

Scope of the Study

1 Markets

- 1.1 Industry Outlook

- 1.1.1 Trends: Current and Future

- 1.1.1.1 Growing Demand for High-Performance and Reliable Electric Vehicle (EV) Batteries

- 1.1.1.2 Strategic Business Strategies to Enhance Presence in the Electric Vehicle Battery Formation and Testing Market

- 1.1.2 Technology Roadmap

- 1.1.3 Ecosystem/Ongoing Programs

- 1.1.3.1 Consortiums, Associations, and Regulatory Bodies

- 1.1.3.2 Government Initiatives

- 1.1.3.3 Programs by Research Institutions and Universities

- 1.1.4 Key Patent Mapping

- 1.1.4.1 Patent Analysis (by Status)

- 1.1.1 Trends: Current and Future

- 1.2 Business Dynamics

- 1.2.1 Business Drivers

- 1.2.1.1 Growing Adoption and Utilization of Electric Vehicles

- 1.2.1.2 Improving Electric Vehicle Performance through Accurate Battery Testing

- 1.2.1.3 Stringent Government Regulations on EV Battery Safety and Performance

- 1.2.2 Business Restraints

- 1.2.2.1 Less Adoption of EVs in Many Underdeveloped and Developing Countries

- 1.2.2.2 Supply Chain Uncertainties and Lack of Charging Infrastructure

- 1.2.3 Business Opportunities

- 1.2.3.1 Growing Usage of Emerging Technologies for Battery Testing

- 1.2.3.2 Increase in the Number of Battery Failure Cases in Electric Vehicles

- 1.2.1 Business Drivers

2 Regions

- 2.1 Europe

- 2.1.1 Europe: Country-Level Analysis

- 2.1.1.1 Germany

- 2.1.1.2 Sweden

- 2.1.1.3 Poland

- 2.1.1.4 Hungary

- 2.1.1.5 Rest-of-Europe

- 2.1.1 Europe: Country-Level Analysis

- 2.2 U.K.

3 Markets - Competitive Benchmarking & Company Profiles

- 3.1 Competitive Benchmarking

- 3.2 Market Share Analysis

- 3.3 Product/Service Matrix

- 3.4 Company Profiles

- 3.4.1 Siemens AG

- 3.4.1.1 Company Overview

- 3.4.1.2 Product Portfolio

- 3.4.1.3 Analyst View

- 3.4.1.3.1 Regions of Growth

- 3.4.2 ABB

- 3.4.2.1 Company Overview

- 3.4.2.2 Product Portfolio

- 3.4.2.3 Analyst View

- 3.4.2.3.1 Regions of Growth

- 3.4.3 SAP SE

- 3.4.3.1 Company Overview

- 3.4.3.2 Analyst View

- 3.4.3.2.1 Regions of Growth

- 3.4.4 Dassault Systemes

- 3.4.4.1 Company Overview

- 3.4.4.2 Product Portfolio

- 3.4.4.3 Analyst View

- 3.4.4.3.1 Regions of Growth

- 3.4.5 AVEVA Group Limited

- 3.4.5.1 Company Overview

- 3.4.5.2 Product Portfolio

- 3.4.5.3 Analyst View

- 3.4.5.3.1 Regions of Growth

- 3.4.6 Tulip Batteries

- 3.4.6.1 Company Overview

- 3.4.6.2 Product Portfolio

- 3.4.6.3 Analyst View

- 3.4.6.3.1 Regions of Growth

- 3.4.7 TUV SUD

- 3.4.7.1 Company Overview

- 3.4.7.2 Product Portfolio

- 3.4.7.3 Analyst View

- 3.4.7.3.1 Regions of Growth

- 3.4.8 Infineon Technologies AG

- 3.4.8.1 Company Overview

- 3.4.8.2 Product Portfolio

- 3.4.8.3 Analyst View

- 3.4.8.3.1 Regions of Growth

- 3.4.9 Element Materials Technology

- 3.4.9.1 Company Overview

- 3.4.9.2 Product Portfolio

- 3.4.9.3 Analyst View

- 3.4.9.3.1 Regions of Growth

- 3.4.1 Siemens AG

- 3.5 Other Key Companies

4 Research Methodology

- 4.1 Data Sources

- 4.1.1 Primary Data Sources

- 4.1.2 Secondary Data Sources

- 4.2 Data Triangulation

- 4.3 Market Estimation and Forecast

- 4.3.1 Factors for Data Prediction and Modeling