|

市場調査レポート

商品コード

1715447

バウンダリスキャンテストシステムの世界市場(2025年~2035年)Global Boundary Scan Test Systems Market 2025-2035 |

||||||

|

|||||||

| バウンダリスキャンテストシステムの世界市場(2025年~2035年) |

|

出版日: 2025年04月30日

発行: Aviation & Defense Market Reports (A&D)

ページ情報: 英文 150+ Pages

納期: 3営業日

|

全表示

- 概要

- 図表

- 目次

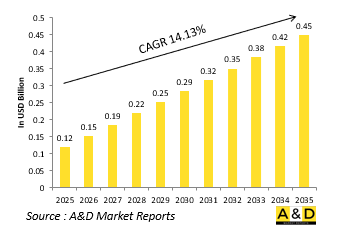

世界のバウンダリスキャンテストシステムの市場規模は、2025年に推定1億2,000万米ドルであり、2035年までに4億5,000万米ドルに達すると予測され、2025年~2035年の予測期間にCAGRで14.13%の成長が見込まれます。

バウンダリスキャンテストシステム市場のイントロダクション

世界の軍用バウンダリスキャンテストシステムは、すべてのコンポーネントに物理的にアクセスすることなく、複雑な電子アセンブリの構造的完全性と機能性を検証するために使用される重要なツールです。IEEE 1149.1規格に基づくバウンダリスキャン技術は、集積回路内に組み込まれたスキャンパスを使用することで、相互接続、論理素子、メモリ素子のテストを可能にします。このアプローチは、高密度基板や多層システムがしばしばカプセル化されたり、従来のプローブベースのアクセスが制限されるような苛酷な環境に展開される軍用電子機器において特に有用です。バウンダリスキャンシステムは、製造、統合、フィールドメンテナンスの各段階における効率的な故障検出と診断を促進し、システムの信頼性とライフサイクル性能を向上させます。その非侵襲的な性質は、ミサイルシステム、レーダーユニット、航空電子モジュール、セキュア通信機器など、再加工や分解が現実的でなかったり、ダメージを与える可能性のある最新の防衛プラットフォームに適しています。戦術的・戦略的システムにおける電子的な複雑性が増すにつれて、バウンダリスキャンテストは性能保証の重要な手段となります。この技術は、単体試験だけでなく、組み込み試験戦略もサポートし、予知保全と作戦の即応性に寄与します。世界の防衛サプライチェーンで採用が進むバウンダリスキャンシステムは、軍用電子機器の品質管理と運用保証の水準を高める役割を担っています。

バウンダリスキャンテストシステム市場における技術の影響

技術の進歩により、軍用バウンダリスキャンテストシステムの機能と用途が大幅に拡大し、最新の防衛電子機器に不可欠な先進の診断ツールへと変貌を遂げました。スキャンチェーン管理、パターン生成、故障分離アルゴリズムの強化により、高集積システムオンチップ(SoC)やフィールドプログラマブルゲートアレイ(FPGA)ベースの設計でも、診断の精度と速度が向上しています。バウンダリスキャンシステムは、継続的なヘルスモニタリングをサポートし、外部テスト環境の必要性を低減するため、自動テスト機器に統合されたり、組み込みテスト機能としてシステム内に組み込まれることが増えています。バウンダリスキャンとインサーキットテストやファンクショナルテストなどの他のテストプロトコルを組み合わせることで、物理的な侵入を最小化しながら包括的な診断を提供するハイブリッドソリューションが誕生しています。最新のバウンダリスキャンツールは現在、GUIとAPIによる自動化を提供し、エンジニアと技術者の両方がアクセスできるようになっています。システムオンモジュール(SoM)テストの進歩により、最小限のハードウェアを追加するだけで、サブシステム全体をカバーするバウンダリスキャンが可能になりました。さらに、サイバーセキュリティフレームワークとの統合により、セキュアな認証済みのテスト方法が可能になり、機密性の高い軍事環境におけるデータの完全性が保護されます。このような技術的進歩により、バウンダリスキャンは製造に特化したプロセスから、防衛用電子機器の長期的な信頼性と運用効率を実現する戦略的な手段へと昇華しました。

バウンダリスキャンテストシステム市場の主な促進要因

軍用電子機器におけるバウンダリスキャンテストシステムの採用の増加は、複数の要因によるものです。電子部品の小型化と複雑化に加え、プリント基板の高密度化、多層化が進むにつれて、従来のアクセスベースのテストは効果的でなくなるか、まったく実用的でなくなっています。バウンダリスキャン技術は、組み込み部品への非侵入的なアクセスを可能にすることでこの課題に対処し、最新の防衛用電子機器のテストに不可欠なものとなっています。平均復旧時間(MTTR)を短縮し作戦の即応性を確保するための、より迅速で正確な診断へのニーズも重要な促進要因となっています。

当レポートでは、世界のバウンダリスキャンテストシステム市場について調査分析し、成長促進要因、今後10年間の見通し、各地域の動向などの情報を提供しています。

目次

世界の航空宇宙・防衛向けバウンダリスキャンテストシステム市場レポートの定義

世界の航空宇宙・防衛向けバウンダリスキャンテストシステム市場のセグメンテーション

地域別

コンポーネント別

技術別

用途別

今後10年間の航空宇宙・防衛向けバウンダリスキャンテストシステム市場の分析

世界の航空宇宙・防衛向けバウンダリスキャンテストシステム市場の市場の技術

世界の航空宇宙・防衛向けバウンダリスキャンテストシステム市場の予測

世界の航空宇宙・防衛向けバウンダリスキャンテストシステム市場の動向と予測

北米

促進要因、抑制要因、課題

PEST

市場予測とシナリオ分析

主要企業

サプライヤーのTierの情勢

企業ベンチマーク

欧州

中東

アジア太平洋

南米

世界の航空宇宙・防衛向けバウンダリスキャンテストシステム市場の国の分析

米国

防衛プログラム

最新ニュース

特許

市場予測とシナリオ分析

カナダ

イタリア

フランス

ドイツ

オランダ

ベルギー

スペイン

スウェーデン

ギリシャ

オーストラリア

南アフリカ

インド

中国

ロシア

韓国

日本

マレーシア

シンガポール

ブラジル

世界の航空宇宙・防衛向けバウンダリスキャンテストシステム市場の機会マトリクス

世界の航空宇宙・防衛向けバウンダリスキャンテストシステム市場レポートに関する専門家の意見

結論

Aviation and Defense Market Reportsについて

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Technology, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 20: Scenario Analysis, Scenario 1, By Component, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Technology, 2025-2035

- Table 23: Scenario Analysis, Scenario 2, By Application, 2025-2035

- Table 24: Scenario Analysis, Scenario 2, By Component, 2025-2035

List of Figures

- Figure 1: Global Boundary Scan Test Systems Market Forecast, 2025-2035

- Figure 2: Global Boundary Scan Test Systems Market Forecast, By Region, 2025-2035

- Figure 3: Global Boundary Scan Test Systems Market Forecast, By Technology, 2025-2035

- Figure 4: Global Boundary Scan Test Systems Market Forecast, By Application, 2025-2035

- Figure 5: Global Boundary Scan Test Systems Market Forecast, By Component, 2025-2035

- Figure 6: North America, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 7: Europe, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 8: Middle East, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 9: APAC, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 10: South America, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 11: United States, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 12: United States, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 13: Canada, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 14: Canada, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 15: Italy, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 16: Italy, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 17: France, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 18: France, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 19: Germany, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 20: Germany, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 21: Netherlands, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 22: Netherlands, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 23: Belgium, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 24: Belgium, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 25: Spain, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 26: Spain, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 27: Sweden, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 28: Sweden, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 29: Brazil, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 30: Brazil, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 31: Australia, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 32: Australia, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 33: India, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 34: India, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 35: China, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 36: China, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 37: Saudi Arabia, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 38: Saudi Arabia, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 39: South Korea, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 40: South Korea, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 41: Japan, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 42: Japan, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 43: Malaysia, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 44: Malaysia, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 45: Singapore, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 46: Singapore, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 47: United Kingdom, Boundary Scan Test Systems Market, Technology Maturation, 2025-2035

- Figure 48: United Kingdom, Boundary Scan Test Systems Market, Market Forecast, 2025-2035

- Figure 49: Opportunity Analysis, Boundary Scan Test Systems Market, By Region (Cumulative Market), 2025-2035

- Figure 50: Opportunity Analysis, Boundary Scan Test Systems Market, By Region (CAGR), 2025-2035

- Figure 51: Opportunity Analysis, Boundary Scan Test Systems Market, By Technology (Cumulative Market), 2025-2035

- Figure 52: Opportunity Analysis, Boundary Scan Test Systems Market, By Technology (CAGR), 2025-2035

- Figure 53: Opportunity Analysis, Boundary Scan Test Systems Market, By Application (Cumulative Market), 2025-2035

- Figure 54: Opportunity Analysis, Boundary Scan Test Systems Market, By Application (CAGR), 2025-2035

- Figure 55: Opportunity Analysis, Boundary Scan Test Systems Market, By Component (Cumulative Market), 2025-2035

- Figure 56: Opportunity Analysis, Boundary Scan Test Systems Market, By Component (CAGR), 2025-2035

- Figure 57: Scenario Analysis, Boundary Scan Test Systems Market, Cumulative Market, 2025-2035

- Figure 58: Scenario Analysis, Boundary Scan Test Systems Market, Global Market, 2025-2035

- Figure 59: Scenario 1, Boundary Scan Test Systems Market, Total Market, 2025-2035

- Figure 60: Scenario 1, Boundary Scan Test Systems Market, By Region, 2025-2035

- Figure 61: Scenario 1, Boundary Scan Test Systems Market, By Technology, 2025-2035

- Figure 62: Scenario 1, Boundary Scan Test Systems Market, By Application, 2025-2035

- Figure 63: Scenario 1, Boundary Scan Test Systems Market, By Component, 2025-2035

- Figure 64: Scenario 2, Boundary Scan Test Systems Market, Total Market, 2025-2035

- Figure 65: Scenario 2, Boundary Scan Test Systems Market, By Region, 2025-2035

- Figure 66: Scenario 2, Boundary Scan Test Systems Market, By Technology, 2025-2035

- Figure 67: Scenario 2, Boundary Scan Test Systems Market, By Application, 2025-2035

- Figure 68: Scenario 2, Boundary Scan Test Systems Market, By Component, 2025-2035

- Figure 69: Company Benchmark, Boundary Scan Test Systems Market, 2025-2035

The Global Boundary Scan Test Systems market is estimated at USD 0.12 billion in 2025, projected to grow to USD 0.45 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 14.13% over the forecast period 2025-2035.

Introduction to Boundary Scan Test Systems Market:

Global military boundary scan test systems are critical tools used in verifying the structural integrity and functionality of complex electronic assemblies without requiring physical access to every component. Based on the IEEE 1149.1 standard, boundary scan technology enables testing of interconnections, logic devices, and memory elements by using built-in scan paths within integrated circuits. This approach is especially valuable in military electronics, where high-density boards and multi-layered systems are often encapsulated or deployed in rugged environments that limit traditional probe-based access. Boundary scan systems facilitate efficient fault detection and diagnostics during manufacturing, integration, and field maintenance stages, improving system reliability and lifecycle performance. Their non-invasive nature is well-suited for modern defense platforms, including missile systems, radar units, avionics modules, and secure communication equipment, where rework or teardown can be impractical or damaging. As electronic complexity grows within tactical and strategic systems, boundary scan testing becomes a key enabler of performance assurance. The technology supports not only standalone tests but also embedded test strategies, contributing to predictive maintenance and mission readiness. Increasing adoption across global defense supply chains highlights the role of boundary scan systems in elevating the standard of quality control and operational assurance in military electronics.

Technology Impact in Boundary Scan Test Systems Market:

Technological progress has significantly expanded the capabilities and applications of military boundary scan test systems, transforming them into advanced diagnostic tools essential for modern defense electronics. Enhancements in scan chain management, pattern generation, and fault isolation algorithms have improved the accuracy and speed of diagnostics, even in highly integrated system-on-chip (SoC) and field-programmable gate array (FPGA)-based designs. Boundary scan systems are increasingly being integrated into automated test equipment and embedded within systems as built-in test capabilities, supporting continuous health monitoring and reducing the need for external test setups. The combination of boundary scan with other test protocols-such as in-circuit testing and functional testing-has created hybrid solutions that offer comprehensive diagnostics with minimal physical intrusion. Modern boundary scan tools now offer graphical user interfaces and API-driven automation, making them accessible to both engineers and technicians. Advances in system-on-module (SoM) testing have enabled boundary scan coverage across subsystems with minimal additional hardware. Furthermore, integration with cybersecurity frameworks allows secure, authenticated test procedures, safeguarding data integrity in sensitive military environments. These technological strides have elevated boundary scan from a manufacturing-focused process to a strategic enabler of long-term reliability and operational efficiency in defense electronics.

Key Drivers in Boundary Scan Test Systems Market:

Several key factors are propelling the increasing adoption of boundary scan test systems in military electronics. The miniaturization and increased complexity of electronic components, coupled with the shift toward densely populated, multi-layer printed circuit boards, make traditional access-based testing less effective or entirely impractical. Boundary scan technology addresses this challenge by enabling non-intrusive access to embedded components, making it indispensable for testing modern defense electronics. The need for faster, more accurate diagnostics to reduce mean time to repair (MTTR) and ensure mission readiness is also a significant driver. As military systems become more interconnected and software-defined, early and precise detection of interconnect faults is essential to prevent cascading failures. Additionally, the defense sector's push toward embedded diagnostics and condition-based maintenance aligns well with boundary scan's capability to support built-in self-test and continuous monitoring features. Increasing global standards compliance and lifecycle cost reduction goals further encourage investment in boundary scan infrastructure. Finally, the demand for high-reliability electronics in mission-critical applications, such as avionics, unmanned systems, and secure communications, underscores the importance of adopting test methods that provide comprehensive fault coverage without physical intrusion or system disassembly.

Regional Trends in Boundary Scan Test Systems Market:

Regional trends in military boundary scan test systems reflect the global nature of defense electronics manufacturing and the push for increased testing sophistication. In North America, particularly the United States, boundary scan is widely utilized in aerospace and defense sectors to support high-reliability standards in embedded systems, avionics, and command-control platforms. Its integration into automated test equipment used by prime contractors and tier-one suppliers reflects a mature ecosystem focused on lifecycle assurance and rapid diagnostics. In Europe, defense organizations are adopting boundary scan as part of broader digitalization and modular open systems approaches, emphasizing interoperability and in-field supportability across multinational programs. The Asia-Pacific region is experiencing strong growth, driven by indigenous platform development in countries such as China, India, South Korea, and Japan. These nations are incorporating boundary scan into their production and maintenance workflows to improve yield rates, lower defect risks, and reduce dependency on traditional test methods. In the Middle East, the deployment of modern electronics in new air defense and communications systems is increasing the need for reliable, automated test solutions that boundary scan technology offers. Latin America and Africa, while slower in adoption, are gradually integrating boundary scan into local defense manufacturing as part of modernization efforts and collaborative programs with global defense technology providers.

Key Boundary Scan Test Systems Program:

The European Commission has announced €60 million in funding for the Common Armoured Vehicle System (CAVS) project under the EDIRPA program (European Defense Industry Reinforcement Instrument through Joint Procurement). This ambitious initiative seeks to develop a modern, standardized armored vehicle to strengthen the operational capabilities of the armed forces in Finland, Latvia, Sweden, and Germany. The CAVS project aims to meet increasing demands for troop mobility and protection, while promoting defense collaboration and equipment standardization among European nations.

Table of Contents

Global Aerospace and Defense Boundary Scan Test Systems Market - Table of Contents

Global Aerospace and Defense Boundary Scan Test Systems Market Report Definition

Global Aerospace and Defense Boundary Scan Test Systems Market Segmentation

By Region

By Component

By Technology

By Application

Global Aerospace and Defense Boundary Scan Test Systems Market Analysis for next 10 Years

The 10-year Global Aerospace and Defense Boundary Scan Test Systems market analysis would give a detailed overview of Global Aerospace and Defense Boundary Scan Test Systems market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Global Aerospace and Defense Boundary Scan Test Systems Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Global Aerospace and Defense Boundary Scan Test Systems Market Forecast

The 10-year Global Aerospace and Defense Boundary Scan Test Systems market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Global Aerospace and Defense Boundary Scan Test Systems Market Trends & Forecast

The regional Global Aerospace and Defense Boundary Scan Test Systems market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Global Aerospace and Defense Boundary Scan Test Systems Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Global Aerospace and Defense Boundary Scan Test Systems Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Global Aerospace and Defense Boundary Scan Test Systems Market Report

Hear from our experts their opinion of the possible analysis for this market.