概要

当レポートのランキングは、ADASティア1のトップ20社 (APTIV、Bosch、Continental、Denso、Mobileye、Valeo、ZF、Baidu、Alibaba、Amazon、Huawei、Foxconnなど) をカバーしています。

- レベル1~4の走行・駐車を実現するためのセンサー・機能・コンピューティング・ソフトウェア関する、サプライヤー各社の技術的対応力について学びます。

- パートナーシップ、投資、M&A、新製品発表、サプライチェーン、ビジネスモデルなどの戦略を理解します。

- 市場考察:市場における優位性、各社のADASからの収益、新規参入による競合情勢の変化。

どのADASサプライヤーが、レベル4の自動運転に対応しているのか?

主な分析結果

- 既存のティア1サプライヤーがADAS市場をリードしているが、変革と競争への課題に直面している

- 中国の新興サプライヤーと新規参入の技術企業が、ADASと電動化における主要ティア1のリーダーシップを脅かす

- 知覚、コンピューティング、AI、SDV、新規市場における新たな機会

- サプライヤーは技術投資を継続し、パートナーシップを強化し、顧客中心のビジネスモデルを構築すべき

Auto2xでは、「レベル4自動運転におけるサプライヤーの準備状況ランキング」レポートを発表しました。その中で、ADAS (先進運転支援システム) の競合情勢の進化や、技術プロバイダーによるレベル4自動運転へのロードマップに関する分析内容を提供しています。

本ランキングは、APTIV、Bosch、Continental、Denso、Mobileye、Valeo、ZFに加え、Baidu、Alibaba、Amazon、Huawei、Foxconnなど、ADASティア1の上位20社を対象としています。

サプライヤーの準備態勢を評価するために、当レポートでは以下の項目を数値化しました。

- レベル1~4の走行・駐車を実現するためのセンサー・機能・コンピューティング・ソフトウェアに対する、サプライヤーの技術対応力。

- サプライヤー各社の戦略:パートナーシップ、投資、M&A、新製品発表、サプライチェーン、ビジネスモデルなど

- サプライヤー各社の市場での位置づけ、ADASからの収益

対象読者

- 自動車OEMおよびティア1/2サプライヤーのエンジニアリング・戦略・マーケティング・R&D・イノベーション担当者

- 自動車市場への参入を検討している技術企業のイノベーションマネージャー

- 自動車業界を専門とする投資家・金融アナリスト

- 自動車業界のコンサルタント・ストラテジスト

読者のメリット

- ADASサプライヤーの状況を包括的に理解することができます。

- 自動運転技術のパートナーや買収目標を特定できます。

- 既存プレーヤーと新規参入プレーヤーの競争力の評価

- 研究開発投資と市場でのポジショニングに関する戦略的決定を導くことができます。

- 自動運転の未来を形作る新たな動向と技術を理解することができます。

なぜ対応力レベルが重要なのか?

自動運転のレースで成功するためには、サプライヤーは3つのパラメーターにおいて競争力を持つ必要があります:

- 技術競争力

- 戦略の実行力 (パートナーシップと投資の強力なネットワーク)、そして

- 市場シェアを獲得するための強力な市場ポジショニング

戦略

- 適切なタイミングで適切な技術・市場に投資することで、不安定性の中で変化する市場ニーズを予見します。

- 市場再編 (新規イノベーション、アジアにおける収益プールのシフトなど) による新たな収益プールを特定します。

将来を見据えたテクノロジー

- レベル3/4自動運転に必要な次世代型ソフト/ハード (DC、コンピュート、4Dイメージング・レーダーなど):誰が優位に立つか?

- 新しい走行・駐車機能が登場:競争力のあるソリューションを提供するために、誰がイノベーションを起こしているのか?

市場のリーダーシップ

- ニーズの変化や新興市場への適応:新たな収益を構築または維持

- リーダーを脅かす新規参入企業:AI・クラウドや社内開発部門を持つ大手テック企業の存在

戦略の実行には、強力なビジョン・パートナーシップ・投資・M&Aが含まれます

インタラクティブ型グラフを利用して、主要サプライヤーと自動車メーカーの戦略について学ぶことができます。

技術競争力の内容:

- 自家用車・自動運転トラック・シェアードモビリティなど使用事例向けの、レベル1~4機能の強力なポートフォリオ (ハイウェイショーファー、都市用バレットパーキングなどのレベル4機能は開発中) ;

- 包括的で堅牢なセンサーセット (画像レーダー、固体LiDARなど) 。

- 集中化されたE/Eアーキテクチャ、ソフトウェアスタック、検証・認証などの能力。

Boschの事例 - 世界最大の自動車部品サプライヤー

- ADAS機能:BoschはL4-Highway機能を開発していますが、現時点ではAPTIVのような他のティア1がこの機能においてより強力な能力を持っていると評価しています。

- センサー:BoschはADASで強いポジションにありますが、レベル3/4ではさらなるイノベーションが必要です。LiDARとスーパーコンピューターをポートフォリオに加えたことは正しい方向ですが、同社はLiDARで他のティア1 (Mercedes-BenzのL3向けValeo) との競合に直面しています。

- 検証:Boschは'VVM' と呼ばれる調査プロジェクトを主導しました。VVMとは、レベル4およびレベル5の自動運転車の検証・認証方法の略で、2019年7月11日に開始され、期間は4年間です。BoschとBMWの2つのコンソーシアムリーダーの下、連邦経済・研究開発省からの資金提供を受け、23の著名な産業・研究パートナーが共同で、法的に実行可能で、時間効率が高く、費用対効果の高い検証・妥当性確認方法を開発します。複雑な都市交差点での利用を例に、VVMは仮想テストと実地テストを組み合わせた本質的なイノベーションを開発します。

- ロボタクシー:DaimlerとBoschは、都市環境におけるL4ロボタクシーのコンソーシアムを組んでいたが、21年8月に終了しました。Boschはセンサーサプライヤーであり、センサーを開発し、ダイムラーとのパートナーシップの一環としてコンピューティング・プラットフォームを開発しています。BoschはL3+向けソフトウェアを独自に開発しています (現時点では他のL4には対応していません) 。

市場でのポジショニング

このパラメーターは、以下の内容を反映しています:

- ADASセンサー・機能の顧客数:自動車メーカー、トラックメーカー、AMODを含む

- 上位4つの主要市場における顧客数:中国、米国、EU、日本

- ADAS収益

- 市場シェア:センサー別・機能別・地域別

- ADAS対売上高比率:ADASへの注力を反映

ADASサプライヤーの市場リーダーシップの動向

- 上位15社の2023年の自動車売上高は3,600億ユーロでした。

- 上位10社の2023年の研究開発費は257億ユーロでした。研究開発費はBoschがトップで、ZF、Densoと続きます。

- Mobileyeはティア1全体で最も研究開発強度が高く、Bosch、Valeoがこれに続きます。

自動運転モビリティの新時代に向けた準備が整っているサプライヤーはどれか?

「Auto2xでは、技術競争力・戦略実行力・市場ポジショニングに基づいて、主要なティア1サプライヤーと新規企業の対応力レベルを評価しました」

最初のパラメータである技術競争力は、センサー・機能・アーキテクチャ・ソフトウェアスタック・イノベーション (特許) などの製品ポートフォリオを反映しています。

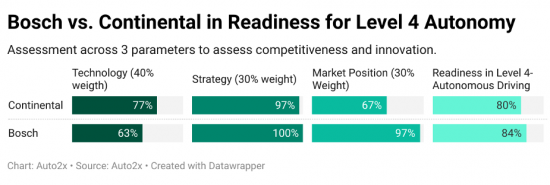

Auto2xでは、APTIVとContinentalは、LiDAR、ソフトウェアスタック、コンピューティン・プラットフォームにおける成熟した艇品/サービス提供により、レベル4の自動運転技術において高い準備レベルを有していると評価しています。

BaiduはApolloの強みにより競争力のある技術を提供しています。

- 2つ目のパラメータの戦略実行力は、サプライヤーのパートナーシップ、投資、ADAS人材、自動運転モビリティにおける活動などをカバーします。

BoschとMobileyeは、強力な自社能力、高成長分野でのパートナーエコシステム、主要市場への投資で、このパラメータをリードしています。

Continentalは、設計・製造から検証・システム統合や機能における新サービスへの拡張に至るまで、100%システムサプライヤーです。そのため、Continentalは有利な立場にあります。

- 第3のパラメータである市場ポジショニングは、センサーと機能によるADASの収益、センサーの市場シェア、顧客基盤、地理的プレゼンスを反映しています。

Bosch、ZF、Valeo、Denso、Continentalのような主要な自動車用ティア1サプライヤーは、自動車の収益において依然として大きなシェアを維持しています。

さらに、ADAS、電動化、新しいモビリティ・ビジネスモデルからの収益も増加しています。上位サプライヤー12社のADAS売上高は、2021年に前年比12.5%増の160億ユーロとなりました。Auto2xでは、2025年までに倍増の350億ユーロになると予想しています。

Continentalは、主にカメラ市場での優位性を活かして、2015年から2018年にかけてADAS市場を売上高でリードしました。

しかし、2019年にはBoschに抜かれ、それ以降はADASの収益で市場をリードしています。ADASに関するOEMとの契約や、より高度な自動化のための運転・駐車機能をサポートする能力が同社の強みです。

- 総合的な対応度:レベル4の自動運転におけるサプライヤーの対応度ランキングは、戦略 (30%ウエイト)、技術 (40%)、市場ポジション (30%) の3つのパラメータの能力に基づいています。

Auto2xによると、Boschはレベル1-2機能のセンサーからの収益でADAS市場をリードしていますが、レベル4の自動運転に対する技術準備では遅れをとっています。

もう一つの成功例は、Intelの自動運転戦略を先導し、ADASで大きなシェアを獲得しているMobileyeです。Mobileyeは、レベル4自動運転への対応度別のサプライヤー・ランキングでトップ3にランクされています。

欧州系サプライヤーがレースを主導するも、中国系サプライヤーが追い上げる

ZFとContinentalのADAS売上高が20億ユーロを突破するも、課題は残されている

ADAS世界売上高ランキングによると、ADASの自動車部品サプライヤー上位4社は、いずれも欧州のBosch、Valeo、ZF、Continentalです。2022年の自動車生産台数が4%増加し、レベル2-3システムのセンサー装着率が高まったことが、ADASの売上高と受注高に貢献しました。

- ZFは、2022年のADAS売上高が2021年の18億ユーロから33%増の24億ユーロを達成しました。ZFは、Auto2xが発表した2021年のADAS売上高世界ランキングで11%の市場シェアを獲得し、第3位にランクインしました。

- ContinentalのADAS売上高は、2021年の17億ユーロから2022年には21億ユーロへと23%増加しました。ADASはContinentalの自動車部門売上高の11%を占めています。

しかし、主要な自動車部品メーカーは、AIとソフトウェアの能力を開発し、ソフトウェアビジネスモデルに進出し、新たな競争に直面するために、さらなる変革に直面しています。

レベル4の自律性を達成するために、自動車企業はどのような課題に直面しているのか?

自動車メーカーは、レベル4の自律性を実現する上で、高度なセンサー技術や膨大なデータをリアルタイムで処理する高性能コンピューティング・プラットフォームの必要性など、いくつかの課題に直面しています。

自動運転車のコンプライアンスと社会的受容性を確保するためには、規制上のハードルと安全基準を乗り越えなければなりません。

配備を成功させるために必要なインフラと技術エコシステムを構築するには、多額の投資・研究開発・パートナーシップが必要です。

主要な自動車ADASサプライヤーは、どのようなリスクに直面しているのか?

サプライヤーは、競争の激化、特にAIやクラウド技術を活用する大手ハイテク企業や新規企業との競争激化によるリスクに直面しており、従来のサプライチェーンを破壊する可能性があります。

自動車メーカーがモビリティサービスプロバイダーへと変貌を遂げることで、サプライヤーはソフトウェア主導のモデルへの迅速な適応を迫られていますが、これには多額の投資と再編が必要になる可能性があります。

さらに、ハードウェアからソフトウェアへの収益化のシフトは、従来の収益源に依存しているサプライヤーに課題を突きつけ、競争力を維持するために事業戦略の厳選を必要とします。

自動運転における新たな機会

ソフトウェア・オン・ホイール革命がモビリティの未来を決める

電動化や自動運転・共有モビリティ・コネクティビティは、より専門的なソフトウェア開発を推し進めます。ハードウェア指向のシステムの大部分が標準化され、コモディティ化します。

高度なソフトウエアを搭載したECUの増加は、大幅なコスト増、車載ソフトウエアの複雑化、車両機能の最適化における制約につながります。

次世代のデジタル自動車は、新しく多様な技術と複雑な論理運用を統合する必要があり、ハードウェアアーキテクチャは高度なソフトウェア機能と更新性をサポートする必要があります。

新たなパートナーシップと新たなビジネスモデルが生まれつつあります。

高い可能性を秘めたソフトウェア主導の新機能には、どのようなものがありますか?

ソフトウェアは自動車産業のデジタル化に対する答えですが、その実現には課題があります。

SDVの主要な技術構成要素における主要なイノベーションクラスターは、下記の通りです。

- EEアーキテクチャ:集中型アーキテクチャの開発における主要自動車メーカーとサプライヤのロードマップとそのパートナーシップを評価します

- BMWが統合したAptivのActive Safety Domain Controller

- VisteonのDomain Controller SmartCore - Mercedes Benzが発売;

- ゾーン指向コントロールユニット (ZCU) :車両をゾーンに分割し、各ゾーンをゾーンECUに統合します (サブECUは車両機能を実現するための処理を行わない) 、Boschのゾーン指向E/Eアーキテクチャ;

- クロスドメイン集中ユニット (CDCU) :複数のドメインの機能を1つのECUに統合したもの (DCUのアーキテクチャに類似)、例:Boschの車両中心型ECU 。

- CarOS:GoogleのAndroid Automotive OSの採用が増加し、MBUXやその他のプレーヤーが提供する競合製品について学ぶ;

- オープンソースソフトウェア開発

- クラウド:クラウドベースのADAS開発を可能にする車載クラウドの出現、自動車メーカー各社の製品開発、マイクロソフトやアマゾンなどの役割;

- OTA (Over-the-Air) アップデートとfeatures-on-demandの機会;

- デジタルツイン

AIとクラウドコンピューティングの革新は自動運転にどのような影響を与えるか?

AIやクラウドコンピューティングのような新技術は、高度なデータ処理、リアルタイムの意思決定、スケーラブルなソフトウェア更新を可能にするため、自動運転の将来にとって極めて重要です。

AIは機械学習と車載アシスタントを通じて車両の知覚と自律性を強化し、クラウドコンピューティングは効率的な機能開発とシステム統合をサポートします。

クラウドコンピューティングは、効率的な機能開発とシステム統合をサポートします。両者が一体となることで、より高度な自動化への移行が促進され、車両全体の性能と安全性が向上します。

AIとクラウドコンピューティングの統合は、自動運転車の消費者体験を変えるでしょう。

AIとクラウドコンピューティングを統合することで、個別化された社内サービス (オーダーメイド・エンターテインメントやリアルタイムナビゲーション支援など) が可能になり、自動運転車における消費者体験が大幅に向上します。

クラウドコンピューティングは、継続的な更新と機能強化を可能にし、車両が最新のテクノロジーと安全機能を確実に維持できるようにします。

さらに、AIを搭載したバーチャルアシスタントは、シームレスなインタラクションを提供し、移動中の利便性と全体的な満足度を向上させることができます。

新規サプライヤーや大手テック企業は、どのように大手ティア1を混乱させる可能性があるのか?

伝統的なADASサプライヤーは、依然として自動車サプライヤーの収益の大部分を占めています。しかし、自動車を刷新するようなAI・クラウド・ソフトウェアの専門知識を活用する米国・中国などの大手テック企業との競争に直面しています。

2020年代には、自動車メーカーがコスト削減を達成するためにより一般的なプラットフォームへとシフトし、既存企業は新規参入企業と競争するために垂直統合型の資産偏重型ビジネスモデルからの脱却を余儀なくされるため、自動車のソフトウェア価値はハードウェアを上回ると思われます。

ソフトウェアは、新機能、コンテンツ、パーソナライズされた新体験など、製品の差別化にとって極めて重要になります。

当レポートでは、ハイテク企業が既存のサプライチェーンに参入したり、破壊したりする機会をいくつか特定しています。

- 自動運転用の次世代認知ハードウェア

- 自動運転用Peta-Opsチップなどのコンピューティング

必要とされる処理能力:

- Lv.2:10TOPS (tera operations per second) の処理能力を必要とする

- Lv.4:100TOPS以上

- Lv.5:1,000TOPSの処理能力が必要となる

- AI:無人運転とHMIのためのAI - 車載AIアシスタントなど

- データに基づくビジネスモデル (車載eコマースなど)

- 5G-6G、コネクテッドインフラ、スマートシティ

- 自律型シェアードモビリティと無人配送

サプライヤーはどうやって競争力を維持し、優位性を獲得するのか?

自動運転において関連性を維持し、競争優位性と市場シェアを獲得するために、サプライヤーは何をすべきか?

サプライヤーは、進化する自動運転の需要に対応するため、高度な知覚ハードウェア、AI、クラウドコンピューティングなどの次世代技術に投資する必要があります。

もう1つの重要な側面は、自動車メーカーが、より高い自律性を開発するために必要な自動運転ソフトウェアとセンサーの能力を構築することです。

また戦略を適応させて、新たな収益源を特定し、革新的なパートナーと協業して高成長の機会を獲得するべきです。

大手自動車メーカーと商業・製品開発パートナーシップを結び、コネクテッド、電気自動車、ADASのロードマップをサポートします。急成長する中国市場におけるAIとコネクティビティの領域は、新しいADサプライヤーが世界のティア1から市場シェアを奪うために極めて重要です。

さらに、サプライヤーは市場における競争力を維持するために、継続的に競合を評価し、製品提供を強化する必要があります。

最後に、ロボットタクシーやラストマイル・デリバリーなど、革新的な技術やビジネスモデルへの投資を促進することです。

新規市場参入者への提言

新規サプライヤーにとっての市場参入戦略のポイントは?

新規サプライヤーの主な市場参入戦略には、既存企業との戦略的パートナーシップの形成、革新的技術への投資、自動運転分野のニッチ市場への注力などがあります。

参入の可能性がある技術には、次世代知覚ハードウェア、自動運転向けAI、高度コンピューティングソリューションなどがあります。

- LenovoはNVIDIAやValeoと提携し、ティア1サプライヤーとしてAD-DC市場に参入しました。

- HuaweiはL2+向けにLiDARとカーネットワーキングをBAICに供給しています。Huaweiは最近、「Focused Innovation for Intelligent Vehicles」と題した製品発表会で、ADASセンサー (4Dイメージング・レーダー)、HMI (AR-HUD) に焦点を当てた自動運転分野の新製品を発表しました。

- Samsung ElectronicsはTeslaと共同でHW4.0用チップを開発します;

Samsung Electronicsが参入する可能性のある技術と国は?

新規サプライヤーにとって有望な国としては、中国、米国、そして自動運転ソリューションの需要が急増している欧州が挙げられます。

目次

第1章 レベル4の自動運転に対するサプライヤーの対応状況

- 1. サプライヤーの対応状況レベル:調査手法

- 2. レベル4自動運転 (AD) への対応状況:総合ランキングの結果

- 3. 戦略実行ランキング:概要

- 4. 市場競争力ランキング

- 5. 市場リーダーシップランキング:概要

- 6. ADAS-ADサプライヤーにとっての機会

- 7. 機会レーダー:行動・対応・観察によるランキング

- 8. 既存企業・新規参入企業への提言

- 9. ティア1サプライヤーのポートフォリオのギャップ

- 10. リーダーシップを脅かすリスク

第2章 戦略と実行

- 1. サプライヤーのADAS-AD戦略の動向

- 2. サプライヤーのレベル4-ADへのロードマップ

- 3. AD用ソフトの推進のためのサプライヤーの研究開発 (R&D) (2023年)

- 4. 新製品の発売 (2024年)

- 5. 主なコラボレーション (2024年)

- 6. AMOD (オンデマンド自動モビリティ) 戦略

- 7. レベル3~4自動運転プラットフォームのサプライヤー

- 8. 自動運転への投資同区 (2024年)

- 9. 新しいビジネスモデル:SaaS、CaaS、DaaS、VaaS、Tier-X

- 10. Continentalの自動車部門のスピンオフ

- 11. Lenovoが新たなDCティア1としてAD市場に参入

- 12. Mobileyeのイメージングレーダー

- 13. Valeoのブレインセグメント

- 14. Qualcomm

- 15. AI規制と倫理の動向

第3章 技術競争力

- 1. 技術競争力ランキング

- 2. 主要ティア1サプライヤーにおけるADAS L0-L4機能の可用性

- 3. 主要ティア1サプライヤーのセンサー・ポートフォリオ

- 4. ADASレーダーとカメラのベンチマーク

- 5. 次世代レーダー・カメラ・LiDAR

- 6. ドライバーと乗客/乗員のモニタリング (DMS-OMS-PMS)

- 7. 車載コンピューティングの台頭

- 8. レベル3~4自動運転のためのデータ記録

- 9. コネクテッド自動運転に向けたE/Eアーキテクチャの進化

- 10. ソフトウェア定義車両 (SDV) におけるイノベーション

- 11. ADASと自動運転におけるローコード/ノーコード・ソリューション

- 12. 特許・知的財産・科学的文献のイノベーター

- 13. Auto2x AD RadarによるADAS機能の将来

- 14. 自動運転における生成AIと新たな応用

- 15. 車両対車両通信 (V2V、V2I、V2X)

第3章 市場リーダーシップとポジショニング

- 1. 自動車収益によるサプライヤーランキング (2023年)

- 2. サプライヤー収益:ADASソフトウェアの分類別

- 3. ADAS収益によるサプライヤーランキング (2015~2023年)

- 4. 77GHzレーダーのサプライヤー市場シェア

- 5. 主要なADハブになるための中国の強み

- 6. インドにおけるレベル2-ADASの台頭

第5章 ADASと自動運転におけるサプライヤーの機会

- 1. ADASセンサーのコンテンツの増加

- 2. センサー市場の予測とTAM

- 3. L3/L4向けLiDARの収益予測

- 4. ADAS向けソフトウェアの需要増加

- 5. ソフトウェア定義車両 (SDV)

- 6. ADASのサブスクリプション

- 7. AMOD (オンデマンド自動モビリティ)

- 8. レベル3-4の規制

- 9. 自動車メタバース

- 10. 自動配達

- 11. レベル3/4の自動運転向け保険

- 12. 自動採掘

目次

The rankings cover the Top-20 ADAS Tier-1s, including APTIV, Bosch, Continental, Denso, Mobileye, Valeo, and ZF, Baidu, Alibaba, Amazon, Huawei, Foxconn and others.

- Learn about the technological capabilities of suppliers in sensors, features, computing and software to deliver Level 1-4 cruising and parking.

- Understand the strategies, including partnerships, investments, M&A, new product launches, supply chain and business models.

- Get insights on who is better positioned in the marketplace, their revenues from ADAS and how new entrants will shape competition.

Which ADAS Suppliers are Ready for Level 4 Autonomous Driving?

Key findings

- Incumbent Tier-1 suppliers lead the ADAS market, but they face challenges to transform and fight the competition

- Emerging Chinese Suppliers and tech entrants threaten the leadership of major Tier-1s in ADAS & Electrification

- New opportunities in perception, computing, AI, SDVs and new markets

- Suppliers should continue investing in tech, strengthen partnerships and build customer-centric business models

Auto2x has released its "Supplier Readiness in Level 4 Autonomous Driving Rankings" report, offering insights into the evolution of the competitive landscape of Advanced Driver Assistance Systems (ADAS) and the roadmaps to Level 4 autonomous driving from technology providers.

The rankings cover the Top-20 ADAS Tier-1s, including APTIV, Bosch, Continental, Denso, Mobileye, Valeo, and ZF, in addition to Baidu, Alibaba, Amazon, Huawei, Foxconn and others.

To assess the Supplier Readiness we quantify

- their technological capabilities of suppliers in sensors, features, computing and software to deliver Level 1-4 cruising and parking.

- their strategies, including partnerships, investments, M&A, new product launches, supply chain and business models.

- how they are positioned in the marketplace, their revenues from ADAS

Who Should Read This Report:

- Engineering, Strategy, Marketing, R&D and Innovation functions in Automotive OEMs and Tier 1-2 Suppliers

- Innovation Managers in Technology companies exploring automotive market entry

- Investors and financial analysts focused on the automotive sector

- Automotive industry consultants and strategists

How Readers Will Benefit:

- Gain a comprehensive understanding of the ADAS supplier landscape

- Identify partners or acquisition targets for autonomous driving technology

- Assess competition from both established players and new entrants

- Guide strategic decisions around R&D investments and market positioning

- Understand emerging trends and technologies shaping the future of autonomous driving

Why does a Readiness Level matter?

To succeed in the Autonomous Driving race suppliers must be competitive across 3 parameters:

- technological competitiveness,

- strategy execution (strong network of partnerships and investments), and

- strong market positioning to capture market share.

Strategy

- Foresee changing market needs amid volatility by investing in the right tech, market at the right time.

- Identify new revenue pools from new innovation, market consolidation, such as shift of revenue pools in Asia.

Future-proof Technology

- Next-gen SW-HW needed for Level 3/4 autonomy e.g., DC, compute, 4D imaging radar. Who has an edge?

- New cruising and parking features emerge: Who is innovating to offer competitive solutions?

Market Leadership

- Adapt to changing needs and emerging markets to build new revenues or maintain.

- Leaders are threatened by new entrants such as Tech Giants with AI, Cloud or in-house

Strategy execution includes a powerful vision, partnerships, investments and M&A

Use the interactive graph to learn about the strategies of major suppliers and carmakers.

Technological competitiveness includes

- a strong portfolio of Level 1-4 features for private cars, autonomous trucks, shared mobility and other use cases (Level 4 features, such as Highway Chauffeur, City and Valet Parking are in development);

- a comprehensive and robust set of sensors (e.g. imaging radar, solid-state lidar).

- capabilities in centralised E/E Architecture, SW Stack, Validation-Verification and others.

Let's have a look at some of them taking the example of Bosch, the world's biggest automotive supplier by revenue.

- ADAS Features: Bosch is developing L4-Highway features but we assess that other Tier-1s, such as APTIV, have stronger capabilities at the moment in this feature.

- Sensors: Bosch has a strong position in ADAS but needs further innovation for L3-4. The addition of Lidar and supercomputers to its portfolio is in the right direction but the company faces competition for Lidar from other Tier 1s, such as Valeo for Mercedes-Benz's L3.

- Validation: Bosch led a research project called 'VVM' , short for verification and validation methods of Level 4 and Level 5 autonomous vehicles, launched on 11 July 2019 with a duration of 4 years. Under the leadership of two consortium leaders Bosch and BMW, with funding from the Federal Ministry for Economic Affairs and Energy, 23 well-known industry & research partners will jointly develop legally viable, time-efficient and cost-effective verification and validation methods. Using the example of a complex urban crossroads application, VVM will develop essential innovations combining virtual and real-life tests.

- Robotaxis: Daimler - Bosch had a consortium for L4 robotaxis in urban environments that ended in Aug'21. Bosch is the sensor supplier, i.e. developing the sensors, and computing platforms as part of its partnership with Daimler who is the lead partner and developer of the SW. Bosch is developing SW on their own for L3+ (not any other L4 as of today).

Market Positioning

This parameter captures:

- Number of clients in ADAS sensors and features, incl. Carmakers, Trucks, AMOD

- Clients in Top-4 major markets: China, USA, EU, Japan

- ADAS revenues

- Market shares in sensors, features and regional

- ADAS-to-Sales ratio to show their focus on AD

Trends in Market Leadership of ADAS Suppliers

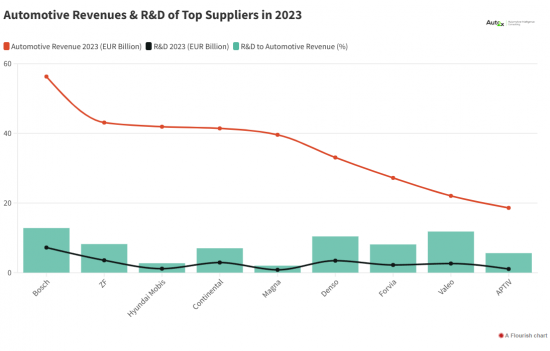

- The Top-15 Suppliers recorded Euro-360 Billion in Automotive revenue in 2023.

- The Top-10 Suppliers recorded Euro-25.7 Billion in R&D spending in 2023. Bosch led R&D expenditure followed by ZF and Denso.

- Mobileye has the highest R&D intensity across Tier-1s, followed by Bosch and Valeo

Which suppliers are better prepared for the new era of Autonomous Mobility?

"Auto2x assessed the readiness levels of major Tier-1 suppliers and emerging players based on their technological competitiveness, their strategy execution and their market positioning."

The first parameter, Technology Competitiveness, captures the product portfolio of sensors, features, architecture, software stack and innovation (patents).

Auto2x assesses that APTIV and Continental have high readiness levels in Level 4 Autonomous Driving Technology due to their mature offering in Lidar, Software stack and Computing Platforms.

Baidu offers competitive technology due to Apollo's strengths.

- Strategy Execution, the 2nd parameter, covers a supplier's partnerships, investments, ADAS manpower, activities in autonomous mobility and more.

Bosch and Mobileye lead the pack in this parameter, with strong in-house capabilities, a partner ecosystem in high-growth areas and investments in key markets.

Continental is a 100% system supplier from design and manufacturing to validation and expansion to new services in system integration and functions. This makes them well-positioned.

- Market Positioning, the 3rd parameter, captures the volume of ADAS revenues from sensors and features, sensor market share, client base and geographical presence.

Major Automotive Tier-1 Suppliers like Bosch, ZF, Valeo, Denso and Continental still maintain the lion's share in terms of automotive revenues.

Furthermore, their revenues from ADAS, electrification and new mobility business models are increasing. ADAS revenues from the Top-12 Suppliers rose 12.5% in 2021 y-y to Euro-16 Billion. Auto2x expects it will double by 2025 to Euro-35 Billion.

Continental led the ADAS market by revenues between 2015 and 2018, mainly by capitalising on its dominance in the camera market.

But they were overtaken by Bosch in 2019, who leads the market by ADAS revenues since then. The contracts with OEMs for ADAS and the ability to support driving and parking features for higher levels of automation are strengths.

- Overall Readiness Level: The Ranking of Suppliers Readiness in Level 4 Autonomous Driving is based on their competence in three parameters, Strategy (30% weight), Technology (40%) and Market Position (30%).

Auto2x found that Bosch leads the ADAS market by revenues from sensors for Level 1-2 features, but they lag in Technology Readiness for Level 4 Autonomous Driving.

Another success story is Mobileye which spearheads INTEL's Autonomous Driving strategy and has captured a large share in ADAS. Mobileye ranks at the Top-3 of Auto2x's Ranking of Suppliers by Readiness in level-4 Automated Driving.

European suppliers lead the race but Chinese Suppliers are catching up

ZF and Continental broke the Euro-2 Billion mark in ADAS revenues, but challenges remain

The Top-4 Automotive Suppliers of ADAS are all European, Bosch, Valeo, ZF and Continental, according to Global ADAS Ranking by Revenues. The 4% growth in automotive production in 2022 and the higher sensor fitment for Level 2-3 systems benefited their ADAS sales and Order Books.

- ZF achieved 33% growth in ADAS revenues in 2022 to Euro-2.4 Billion, from Euro-1.8B in 2021. ZF ranked 3rd in the Global ADAS Ranking by Revenues in 2021 from Auto2x with an 11% market share.

- Continental saw 23% growth in ADAS sales to Euro-2.1 Billion in 2022, from Euro-1.7B in 2021. ADAS accounted for 11% of Continental's Automotive revenues.

But major automotive suppliers face further transformation to develop capabilities in AI and software, expand into software business models and face new competition.

What challenges do automotive companies face in achieving Level 4 autonomy?

Automotive companies face several challenges in achieving Level 4 autonomy, including the need for advanced sensor technology and high-performance computing platforms to process vast amounts of data in real time.

Regulatory hurdles and safety standards must be navigated to ensure compliance and public acceptance of autonomous vehicles.

Significant investments, research and development, and partnerships are required to build the necessary infrastructure and technology ecosystem for successful deployment.

What risks do leading Automotive ADAS Suppliers face?

Suppliers face risks from increased competition, particularly from tech giants and emerging players that leverage AI and cloud technologies, potentially disrupting traditional supply chains.

The transformation of carmakers into mobility service providers pressures suppliers to adapt quickly to software-driven models, which may require significant investment and restructuring.

Additionally, the shift from hardware to software monetization poses challenges for suppliers reliant on traditional revenue streams, necessitating the refinement of their business strategies to remain competitive.

New opportunities in Autonomous Driving

Software-on-Wheels revolution will determine Mobility's future

Electrification, automated driving, shared mobility and connectivity push for more dedicated software development. A large part of hardware-oriented systems becomes more standardized and commoditized.

The growing number of ECUs with sophisticated software leads to significant cost increases, higher in-vehicle software complexity and constraints in optimising vehicular functions.

Next-generation Digital vehicles must integrate new, diverse technologies and complex logical operations; the hardware architecture has to support advanced software functionality and upgradability.

New partnerships and new business models are emerging.

What are some key new Software-driven features with high potential?

Software is the answer to the Digitization of the Automotive Industry but delivery is challenging.

Learn about top innovation clusters across major technological building blocks of SDVs.

- EE Architectures: Assess the roadmaps of leading carmakers and suppliers in the development of centralized architectures and their partnerships;

- Aptiv's Active Safety Domain Controller integrated by BMW,

- Visteon's Domain Controller SmartCore, launched by Mercedes Benz;

- zone-oriented control units (ZCUs), where the vehicle is divided into zones and each zone integrates into a zone-ECU (the sub-ECUs do not perform any processing to realize a vehicle function) e.g. Bosch's zone-oriented E/E architecture;

- cross-domain centralized units (CDCUs), where the functions of more than one domain are consolidated onto a single ECU (similar to the DCU's architecture) e.g. Bosch's vehicle-centralized ECU.

- CarOS: Learn about the rising adoption of Google's Android Automotive OS and the competitive offerings from MBUX and other players;

- Open-source software development

- Cloud: the emergence of automotive cloud as an enabler for cloud-based ADAS development, development of offerings from carmakers and the role of Microsoft, Amazon among others;

- Over-the-Air-updates and the opportunities for features-on-demand;

- Digital Twin

How could innovation in AI and cloud computing impact autonomous driving?

New technologies like AI and cloud computing are crucial for the future of autonomous driving as they enable advanced data processing, real-time decision-making, and scalable software updates.

AI enhances vehicle perception and autonomy through machine learning and in-car assistants, while cloud computing supports efficient feature development and system integration.

Together, they facilitate the transition to higher levels of automation and improve overall vehicle performance and safety.

The integration of AI and cloud computing will change the consumer experience in autonomous vehicles

Integrating AI and cloud computing will significantly enhance the consumer experience in autonomous vehicles by enabling personalized in-car services, such as tailored entertainment and real-time navigation assistance.

Cloud computing allows for continuous updates and feature enhancements, ensuring vehicles remain up-to-date with the latest technology and safety features.

Additionally, AI-powered virtual assistants can provide seamless interaction, improving convenience and overall satisfaction during travel.

How could new suppliers and Tech Giants disrupt major Tier-1s?

Traditional ADAS suppliers still maintain the lion's share in automotive supplier revenues. But they face competition from US, Chinese and other Tech giants who capitalize on their expertise in AI, Cloud and Software transforming automotive.

In the 2020s the vehicle's software value will exceed that of hardware as carmakers shift to more common platforms to achieve cost savings and existing players are forced to move away from vertically integrated, asset-heavy business models to compete with new entrants.

Software will be crucial for product differentiation such as new features, content, and new personalized experiences.

We have identified several opportunities for Tech Companies to enter or disrupt the existing supply chain.

- Next-gen Perception Hardware for Autonomous Driving

- Computing, e.g. Peta-ops chips for Autonomous Driving

"The computing power required for a

- Lv.2 vehicle is 10 TOPS (tera operations per second),

- Lv.4 exceeds 100 TOPS,

- Lv.5 vehicle will require a 1,000 TOPS computing processing power."

- AI: AI for Autonomy and HMI such as in-car AI assistants

- Data-based Business models such as in-car e-commerce

- 5G-6G, Connected Infrastructure and Smart Cities

- Autonomous Shared Mobility and autonomous deliveries

How can Suppliers stay competitive and gain competitive advantage?

What should suppliers do to stay relevant in autonomous driving, gain competitive advantage and market share?

Suppliers should invest in next-generation technologies, such as advanced perception hardware, AI, cloud computing to meet the evolving demands of autonomous driving.

Another important aspect is building competence in Autonomous Driving software and sensors needed by carmakers to develop higher autonomy.

They should also adapt their strategies to identify new revenue pools and collaborate with innovative partners to tap into high-growth opportunities.

By forming commercial and product development partnerships with volume carmakers to support their connected, electric and ADAS roadmaps. The AI and connectivity domains in the booming Chinese market are crucial for new AD Suppliers to claim market share from global Tier-1s.

Additionally, suppliers must continuously assess competition and enhance their product offerings to maintain a competitive edge in the market.

Finally, fuel investments in innovative technologies and business models incl. robotaxis, and last-mile delivery.

Recommendations for new market entrants

What are some key market entry strategies for new suppliers?

Key market entry strategies for new suppliers include forming strategic partnerships with established players, investing in innovative technologies, and focusing on niche markets within the autonomous driving sector.

Technologies with potential for entry include next-gen perception hardware, AI for autonomy, and advanced computing solutions.

- Lenovo has entered the AD-DC market as a Tier-1 Supplier with partnerships with NVIDIA and Valeo.

- Huawei supplies LIDAR and car networking to BAIC for L2+. Huawei has recently launched new products in Autonomous Driving focusing on ADAS sensors (4D imaging radar), HMI (AR-HUD) during their product launch titled 'Focused Innovation for Intelligent Vehicles'.

- Samsung Electronics will work together with Tesla to develop chips for their HW 4.0;

Which technologies show potential for them to enter and which countries?

Countries with promising opportunities for new suppliers include China, the USA, and in Europe, where demand for autonomous driving solutions is rapidly growing.

Table of Contents

1. Supplier Readiness in Level 4 Autonomous Driving

- 1. Methodology for the Supplier Readiness Level

- 2. Findings from the overall ranking of Readiness in Level 4-AD

- 3. Strategy Execution ranking summary

- 4. Technology Competitiveness ranking

- 5. Market Leadership ranking summary

- 6. Opportunities for ADAS-AD Suppliers

- 7. Opportunity Radar: rankings by Act, Prepare, Watch

- 8. Recommendations for incumbents and new market entrants

- 9. Gaps in the portfolios of Tier-1 Suppliers

- 10. Risks that threaten their leadership

2. Strategies and execution

- 1. Trends in Supplier ADAS-AD Strategy

- 2. Supplier roadmaps to Level 4-AD

- 3. R&D of Suppliers in 2023 to drive AD-SW

- 4. New Product Launches in 2024

- 5. Key collaborations in 2024

- 6. Strategies in AMOD (Automated-Mobility-on-Demand)

- 7. Suppliers of Level 3-4 Autonomous Driving Platforms

- 8. Investments in Autonomous Driving in 2024

- 9. New Business Models: SaaS, CaaS, DaaS, VaaS, Tier-X

- 10. Continental's Spin-off of the Automotive Segment

- 11. Lenovo's entry in the AD markets as a new DC Tier-1

- 12. Mobileye's Imaging Radar

- 13. Valeo's Brain segment

- 14. Qualcomm

- 15. AI Regulation and developments of Ethics

3. Technology Competitiveness

- 1. Ranking by Technology Competitiveness r

- 2. ADAS L0-L4 Feature Availability across major Tier-1 Suppliers

- 3. Sensor portfolio of leading Tier-1 Suppliers

- 4. ADAS Radar and Camera benchmarking

- 5. Next-generation radars, camera, lidar

- 6. Driver and passenger / occupant monitoring (DMS-OMS-PMS)

- 7. Rise of on-board vehicle Computing

- 8. Data recording for Level 3-4 Autonomous Driving

- 9. The evolution of E/E Architecture for connected and automated driving

- 10. Innovation in Software-Defined Vehicles (SDV)

- 11. Low-No Code solutions in ADAS and autonomy

- 12. Innovators in Patents, Intellectual Property and Scientific Literature

- 13. Future of ADAS features from Auto2x AD Radar

- 14. Generative AI and new applications in Autonomous Driving

- 15. Vehicle-to-Everything Communications (V2V, V2I, V2X)

3. Market Leadership and Positioning

- 1. Supplier Rankings by Automotive Revenue in 2023

- 2. Supplier Revenues by ADAS-Software divisions

- 3. Ranking of Suppliers by ADAS Revenues 2015-2023

- 4. Supplier market shares in 77GHz radar

- 5. China's strengths to become Top AD Hub

- 6. Rise of Level 2-ADAS in India

5. Opportunities in ADAS and Autonomous Driving for Suppliers

- 1. Rising ADAS sensor content

- 2. Sensor Forecast and TAM

- 3. Forecast of revenues from Lidar for L3/L4

- 4. Rising demand for SW for ADAS

- 5. (SDV) Software-Defined Vehicles

- 6. Subscriptions for ADAS

- 7. AMOD (Automated-Mobility-on-Demand)

- 8. Regulation for Level 3-4

- 9. CarMetaverse

- 10. Autonomous Deliveries

- 11. Insurance for Level 3-4 Automated Driving

- 12. Autonomous mining

- 発行日

- 発行

- Auto2x

- ページ情報

- 英文 100 Pages

- 納期

- 即日から翌営業日