|

|

市場調査レポート

商品コード

1850129

ADAS(先進運転支援システム):市場シェア分析、産業動向、統計、成長動向予測(2025~2030年)Advanced Driver Assistance Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ADAS(先進運転支援システム):市場シェア分析、産業動向、統計、成長動向予測(2025~2030年) |

|

出版日: 2025年06月25日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

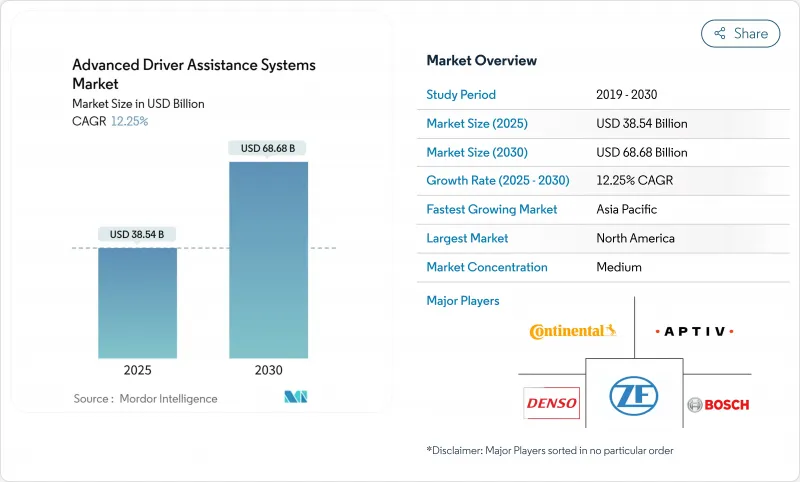

世界のADAS(先進運転支援システム)市場の2025年の売上は385億4,000万米ドル、2030年には686億8,000万米ドルに達し、CAGR 12.25%で拡大する見通しです。

米国、欧州連合(EU)、中国における強力な規制義務付け、レーダー、カメラ、LiDARセンサーの急速なコスト・デフレ、自動車セクターのソフトウェア定義車両(SDV)プラットフォームへの移行が、この成長を支える主要な力となっています。自動車メーカーはミッドセグメント車にレベル2+の機能をバンドルする一方、OTA(over-the-air)アップグレードの経路は、経常的なソフトウェア収益を生み出すようになっています。同時に、アジアにおける半導体能力の拡大と新しい4ナノメーター車載システムオンチップは、より高いセンサーフュージョン精度を可能にし、ADAS市場を大量生産モデルへと押し上げています。競合勢力は、ティア1サプライヤー、クラウド・ハイパースケーラー、ファブレス・チップ設計者が、知覚スタック、トレーニング・データ、収益化可能なソフトウェア・サービスを制御するために協業する垂直プラットフォーム・プレイへとシフトしています。

世界のADAS(先進運転支援システム)市場の動向と洞察

厳しい安全規制が市場成長を支える

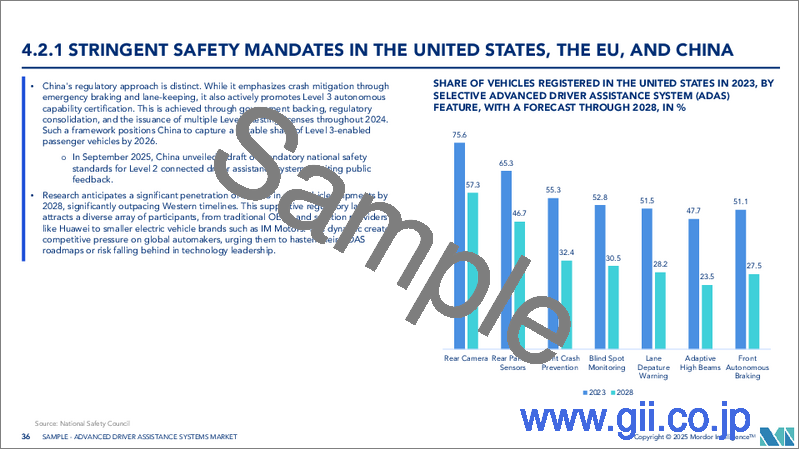

現在、運転支援は必須のインフラとして規制で扱われています。NHTSAは、2029年9月から米国のすべての新型軽自動車に自動緊急ブレーキを義務付け、年間約1,700万台を基準としています。欧州の一般安全規則IIは、2024年7月以降、すべての新型車にインテリジェント・スピード・アシスタンス、レーンキーピング・アシスタンス、緊急ブレーキを義務付けており、OEMは標準化されたADAS機能のために電気アーキテクチャーを再設計することを余儀なくされています。中国は、ADASの性能を新車アセスメントプログラムに統合し、5つ星の安全スコアをセンサーの構成とアルゴリズムの精度にリンクさせました。これらのルールは、裁量的な購買決定を排除し、ADAS市場をコンプライアンス主導のボリューム・ビジネスへと変貌させ、あらゆる価格帯での装着率を加速させる。

AIベースのセンサー・フュージョンがフィーチャー・バンドリングを解き放つ

オンチップ・ニューラル・ネットワークの進歩により、安価なプロセッサで高度な知覚が可能になりました。モービルアイのEyeQ6 Liteは、8つのカメラストリームと4Dレーダー入力を1つの5ワットデバイスに統合し、L2+ハイウェイパイロットパッケージの部品コストを削減しました。ボッシュがマイクロソフトのジェネレーティブAIサービスを統合することで、ドライバーの意図と交差交通操作を予測する予測進路計画が可能になります。これらの開発により、OEMはアダプティブ・クルーズ・コントロール、車線中央維持、交通標識認識を1つのサブスクリプションにパッケージ化し、機能ごとのハードウェアの冗長性を減らし、ソフトウェアのマージンを増やすことができます。

高いセンサー・スイート・コストが依然として障壁

価格が急落しても、L2+センサーパック一式はBセグメントハッチバックの製造コストに2,000~4,000米ドルを上乗せします。保険業界のデータによると、軽度の衝突事故後のレーダー交換は1台当たり900米ドルを超え、カメラの再校正は平均450米ドルです。こうしたコストは、プレミアム価格帯以外の消費者の購買意欲を減退させ、修理インフラが整っていない新興経済諸国では後付け需要を鈍らせる。

セグメント分析

システム・レベル・ソリューションのADAS(先進運転支援システム)市場規模は、既存の電子ブレーキ・モジュールとの互換性と長距離移動時の消費者の受け入れにより、2024年の売上高の22.41%を創出したアダプティブ・クルーズ・コントロールに支えられています。自動緊急ブレーキは、すべての新車に前方衝突軽減を求める規制に後押しされ、CAGR 16.21%で加速しています。サプライヤーは現在、歩行者と自転車の検知を同じ制御ユニットに統合し、セグメントを超えたスケールメリットを生み出しています。2030年までの間に、OEMは都市型緊急ブレーキを二輪車と小型商用バンにも拡大し、安全性の適用範囲を広げ、装着台数を増加させると予想されます。

過去のデータでは、2020年から2024年にかけてのサブセグメントの複合成長率は8.5%であったが、NHTSAとEUの義務化によって予測期間中はこのペースが2倍になります。車線逸脱や前方衝突警報のようなエントリーレベルの警告機能は低価格トリムで存続しているが、先進プレミアムパッケージには360度カメラ、HDマップ、交差点旋回時のAI対応予測ブレーキが統合されています。このような段階的なアップグレードの経路は、定期的なOTA収入を促し、知覚スタックを所有するTier-1サプライヤーにとってプラットフォームの粘着性を深める。

レーダーの46.07%のシェアは、雨、霧、雪に強いという特性を強調しており、自動緊急ブレーキの主要なトリガーとしての地位を確実なものにしています。ADAS市場は、28ナノメートルRF CMOSで生産されるようになった77GHzフロントコーナー・レーダー・モジュールのコモディティ化から恩恵を受けています。10ナノメートル以下の画像信号プロセッサを搭載したカメラ・センサは、ディープ・ラーニングによる知覚アーキテクチャをコスト効率よく実現することでこれに追随しています。

LiDARの市場シェアはまだわずかだが、CAGRが21.35%と予測される急成長要素です。ソリッドステート、ムービングパーツなしのアーキテクチャ、ウエハーレベルの光学系により、変動コストは350米ドルに下がり、ミッドセグメントSUVが次のターゲットとなります。ADAS市場のシェア拡大のため、LiDARサプライヤーはOEM設計スタジオと提携し、美観を損なうルーフトップ・ドームを避けてヘッドランプクラスターにセンサーを埋め込みます。超音波と赤外線は、駐車と暗視のためのニッチな任務を維持しています。一元的に融合された信号処理のクロス動向が台頭しており、配線量を削減し、OTAベースのアルゴリズム改良を可能にしてハードウェアサイクルを延長しています。

地域分析

北米は、連邦政府の義務付け、保険優遇措置、SUV普及率の高さにより、レベル2+バンドルへの受容基盤を形成したため、2024年の世界売上高の34.33%を占めました。米国は、自賠責保険料の引き下げとNCAPの採点でADAS導入のインセンティブを高め、カナダは自動車安全規制を米国の基準に合わせ、国境を越えたモデルの整合性を確保しています。主要サプライヤーは、アリゾナ州、ミシガン州、オンタリオ州で検証フリートを走らせ、雪やまぶしさの条件に対するセンサー融合アルゴリズムを改良するエッジケース・データを収集しています。

アジア太平洋は2030年までのCAGRが14.55%で最も急成長している地域であり、2023年第3四半期に30万以上のL2+ライセンスを授与した中国の積極的な「スマートビークル」ロードマップが後押ししています。HDマップのクラウドソーシングに関する北京のガイドラインは、BYDやXpengのような国内OEMに利益をもたらすデータネットワーク効果を促進します。インドの半導体工場と電子部品に対する生産連動インセンティブは、現地でのADAS ECU製造を奨励し、材料費を削減し、コンパクトハッチバックの装着を早める。

欧州では、自動車メーカーがすべての新型車に9つの安全機能を統合することを義務付ける一般安全規制IIの下、着実な成長が続いています。ドイツ連邦参議院は、時速60kmまでの制限付きハンズオフ高速道路走行を承認し、レベル3のデビュー時期を早めました。フランスとスペインは、Vision Zeroの事故目標を達成するため、大型トラック車両への改修助成を優先。南米では、ブラジルがすべての新車にエレクトロニック・スタビリティ・コントロールを義務付け、2027年に向けて車線逸脱警報の評価を行うなど、2030年までの可能性を示しています。チリとコロンビアは、AEBの装着に関連した自動車税リベートを展開し、輸入業者がエントリーモデルにレーダーを指定するよう促しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 米国、欧州連合、中国における厳格な安全規制

- AIベースのセンサー融合によりL2+機能のバンドルが可能

- SDV/OTAアーキテクチャが販売後の収益を解き放つ

- 急速なセンサーコスト削減とモジュール統合

- 新興市場におけるSUVと高級車の普及率の拡大

- 使用状況に基づく保険割引がOEM装備を加速

- 市場抑制要因

- LiDAR/レーダーシステムの高コスト

- 悪天候や照明による機能制限

- サイバーセキュリティ責任とデータプライバシーリスク

- mmWaveチップセットと基板供給のボトルネック

- バリューチェーン/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- システムタイプ別

- 駐車支援システム

- アダプティブフロントライティング

- 暗視システム

- 死角検知

- 自動緊急ブレーキ

- 前方衝突警報

- ドライバーの眠気警告

- 交通標識認識

- 車線逸脱警報

- アダプティブクルーズコントロール

- センサータイプ別

- レーダー

- LiDAR

- カメラ

- 超音波

- 赤外線

- 車両タイプ別

- 二輪車

- 乗用車

- 中型および大型商用車

- 自律性レベル別

- L1

- L2

- L3

- L4

- L5

- 販売チャネル別

- OEM装着

- アフターマーケットの改造

- 地域別

- 北米

- 米国

- カナダ

- その他北米地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- インドネシア

- その他アジア太平洋地域

- 中東・アフリカ

- トルコ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- ナイジェリア

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Continental AG

- Robert Bosch GmbH

- DENSO Corporation

- Aptiv PLC

- ZF Friedrichshafen AG

- Magna International

- Valeo SA

- Hyundai Mobis

- Aisin Corporation

- Mobileye(Intel)

- NVIDIA Corporation

- NXP Semiconductors

- Infineon Technologies

- Renesas Electronics

- ON Semiconductor

- STMicroelectronics

- Hitachi Astemo

- Autoliv Inc.