|

|

市場調査レポート

商品コード

1426146

機能性ミルク市場:世界の展望と予測 (2024-2029年)Functional Milk Market - Global Outlook & Forecast 2024-2029 |

||||||

|

|||||||

|

|||||||

| 機能性ミルク市場:世界の展望と予測 (2024-2029年) |

|

出版日: 2024年02月15日

発行: Arizton Advisory & Intelligence

ページ情報: 英文 317 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

世界の機能性ミルクの市場規模は、2023年の270億米ドルから、予測期間中は7.53%のCAGRで成長すると予測されています。

市場動向と促進要因

機能性ミルクにおけるクリーンラベル製品の導入

クリーンラベル製品に対する消費者の嗜好の高まりにより、機能性ミルクの需要が大幅に増加しています。クリーンラベル製品は、人工添加物や保存料を使用せず、シンプルで分かりやすい成分表を特徴としています。消費者が健康志向を強め、食品の選択に透明性を求めるようになるにつれ、必須栄養素を供給し、クリーンな食生活の嗜好に沿った機能性ミルクに注目が集まっています。さらに、ビタミン、ミネラル、その他の生物活性化合物で改良された機能性ミルクは、消費者の健康とウェルネスのニーズに応えています。これらの製品は、消化の改善、免疫サポートの強化、より優れた栄養プロファイルを誇ることが多いです。こうした機能性ミルクの明確でわかりやすい表示は、健康的で加工度の低い選択肢を求める消費者の共感を呼んでいます。

ベンダーは製品イノベーションに注力

製品イノベーションは機能性ミルク市場のダイナミクスを形成する上で極めて重要であり、消費者の嗜好や業界の競争に大きな影響を与えています。新しい成分、配合、技術の導入は、消費者の機能性ミルク製品に対する認識や関わり方を一変させる可能性を秘めています。ビタミン、ミネラル、プロバイオティクス、その他の健康増進成分で強化するようなイノベーションは、ウェルネスと栄養面での利点に対する消費者の要求の進化に対応することができます。こうした進歩は健康志向の消費者に対応し、競合他社との差別化の機会を提供します。さらに、製品イノベーションは消費者の関心を刺激し、市場の成長を促進し、業界のリーダーとしてのブランドの評判を確立することができます。機能性ミルク市場が進化するにつれて、革新的な戦略を取り入れて実行に移す企業は競争上の優位性を獲得し、ますますダイナミックになる市場情勢の中で持続可能性と成長を促進する可能性が高いです。

当レポートでは、世界の機能性ミルクの市場を調査し、市場の定義と概要、市場機会・市場動向、市場影響因子の分析、市場規模の推移・予測、各種区分・地域別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

第1章 調査対象・調査範囲

第2章 重要考察

- 市場機会ポケット

- 市場の定義

- レポート概要

- 機会と課題の分析

- 部門別分析

- 地域分析

- 競合情勢

第3章 市場概要

第4章 イントロダクション

- 概要

- 機能性食品の需要の高まり

- バリューチェーン分析

第5章 市場機会・動向

- 機能性ミルクのクリーンラベル製品の導入

- ラクトースフリーミルクの需要の増加

- プロバイオティクスと消化器の健康

第6章 市場成長の実現要因

- 肥満の有病率の増加

- 可動性を高める機能性ミルクに対する需要の高まり

- ベンダーによる製品イノベーションへの注力

第7章 市場抑制要因

- 機能性ミルクの代替品の増加

- 機能性ミルクの高い生産コスト

- 厳しい政府規制

第8章 市場情勢

- 市場概要

- 市場規模・予測

- ベンダー分析

- 需要に関する洞察

- ファイブフォース分析

第9章 形態

- 市場のスナップショットと成長促進要因

- 市場概要

- 粉末

- 液体

- 市場概要

- 市場規模・予測

- 地域別市場

第10章 用途

- 市場のスナップショットと成長促進要因

- 市場概要

- 免疫・疾患管理

- 体重管理

- 臨床栄養

- その他

- 市場概要

- 市場規模・予測

- 地域別市場

第11章 年齢

- 市場のスナップショットと成長促進要因

- 市場概要

- 14~19歳

- 20~64歳

- 1~13歳

- 64歳以上

- 市場概要

- 市場規模・予測

- 地域別市場

第12章 流通チャネル

- 市場のスナップショットと成長促進要因

- 市場概要

- スーパーマーケット

- コンビニエンスストア

- オンライン

- 食料品店

- 専門店

- 機関向け販売

- 市場概要

- 市場規模・予測

- 地域別市場

第13章 地域

- 市場のスナップショットと成長促進要因

- 地理的概要

第14章 アジア太平洋

第15章 北米

第16章 欧州

第17章 ラテンアメリカ

第18章 中東・アフリカ

第19章 競合情勢

- 競合概要

第20章 主要企業プロファイル

- ABBOTT

- DANONE

- LACTALIS INTERNATIONAL

- NESTLE

第21章 他の有力ベンダー

- AROMA MILK PRODUCTS

- ARLA FOODS AMBA

- AGROPUR

- BEST WAY INGREDIENTS

- BEST HEALTH FOODS

- BRIGHT LIFECARE

- CAPSA

- CREDITON DAIRY

- CAYUGA MILK INGREDIENTS

- CLOVER SONOMA

- DAIRY FARMERS OF AMERICA

- DARIGOLD

- EHRMANN

- FONTERRA

- F&N DAIRIES

- FAIRLIFE

- FRIESLANDCAMPINA

- GLANBIA

- GCMMF

- GAY LEA FOODS

- HERITAGE FOODS

- HP HOOD

- INGREDIA

- LAND O' LAKES

- LYCOTEC

- MCNELL NUTRITIONALS

- MEGMILK SNOW BRAND

- MILLIGANS FOOD GROUP

- MOTHER DAIRY FRUIT & VEGETABLE

- ORGANIC VALLEY

- PROCAL DAIRIES

- PARAG MILK FOODS

- SADAFCO

- SLEEPWELL

- STOLLE MILK BIOLOGICS

- SYNLAIT

- TIRLAN

- TESCO

- VINDIJA D. D.

- VALFOO

- VINAMILK

第22章 レポートサマリー

- 重要ポイント

- 戦略的推奨事項

第23章 定量的サマリー

- 地域別市場

- 形態別市場

- 用途別市場

- 年齢別市場

- 流通チャネル別市場

- アジア太平洋

- 北米

- 欧州

- ラテンアメリカ

- 中東・アフリカ

第24章 付録

List Of Exhibits

LIST OF EXHIBITS

- EXHIBIT 1 MARKET SIZE CALCULATION APPROACH 2023

- EXHIBIT 2 GLOBAL CONSUMER PREFERENCES: FUNCTIONAL PRODUCT PURCHASES DURING COVID-19 (2021) (%)

- EXHIBIT 3 VALUE CHAIN ANALYSIS OF FUNCTIONAL MILK

- EXHIBIT 4 IMPACT OF INTRODUCTION OF CLEAN LABEL PRODUCTS IN FUNCTIONAL MILK

- EXHIBIT 5 PREFERENCE OF CLEAN LABEL PRODUCTS TOWARD CONSUMERS

- EXHIBIT 6 IMPACT OF INCREASED DEMAND FOR LACTOSE-FREE MILK

- EXHIBIT 7 LACTOSE INTOLERANCE BY COUNTRY WISE 2023 (%)

- EXHIBIT 8 IMPACT OF PROBIOTICS AND DIGESTIVE HEALTH

- EXHIBIT 9 PREVALENCE OF DIGESTIVE DISORDERS IN SOUTH KOREA, SAUDI ARABIA, AND THE US

- EXHIBIT 10 IMPACT OF RISE IN PREVALENCE OF OBESITY

- EXHIBIT 11 IMPACT OF GROWING DEMAND FOR FUNCTIONAL MILK ENHANCING MOBILITY

- EXHIBIT 12 GLOBAL WORLD POPULATION AGE WISE IN 2025, 2050, 2075 AND 2100 ($ BILLION)

- EXHIBIT 13 KEY STATISTICS ON PROTEIN CONSUMPTION, CALCIUM BENEFITS, AND AGING MOBILITY MARKET

- EXHIBIT 14 IMPACT OF VENDORS FOCUS ON PRODUCT INNOVATION

- EXHIBIT 15 IMPACT OF INCREASING ALTERNATIVES FOR FUNCTIONAL MILK

- EXHIBIT 16 SALES OF PLANT BASED MILK IN THE US AND INDIA: 2021 AND 2022

- EXHIBIT 17 IMPACT OF HIGH PRODUCTION COST OF FUNCTIONAL MILK

- EXHIBIT 18 GLOBAL MILK PRICE FROM JANUARY 2023 TO NOVEMBER 2023 ($ /HUNDREDWEIGHT [CWT])

- EXHIBIT 19 IMPACT OF STRINGENT GOVERNMENT REGULATIONS

- EXHIBIT 20 FACTORS DRIVING GROWTH OF FUNCTIONAL MILK

- EXHIBIT 21 COMPARISON OF CAGR OF REGIONS IN GLOBAL FUNCTIONAL MILK MARKET: 2024-2029 (%)

- EXHIBIT 22 GLOBAL FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 23 FIVE FORCES ANALYSIS 2023

- EXHIBIT 24 INCREMENTAL GROWTH BY FORM 2023 & 2029

- EXHIBIT 25 GLOBAL FUNCTIONAL MILK MARKET BY PRODUCT 2023 AND 2029 (% SHARE)

- EXHIBIT 26 GLOBAL AVERAGE PRICE OF SKIMMED MILK POWDER IN 2022 ($ PER TONNE)

- EXHIBIT 27 PRODUCTION OF SKIMMED MILK POWDER IN THE EU 27: JANUARY 2023 TO SEPTEMBER 2023 (THOUSAND TONNES)

- EXHIBIT 28 EXPORT OF SKIM MILK POWDER: 2019-2021 & 2031 (%)

- EXHIBIT 29 SKIM MILK POWDER PRODUCTION AND CONSUMPTION: 2024 TO 2032 (KW PW)

- EXHIBIT 30 GLOBAL POWDER FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 31 VOLUME SALES OF VALUE-ADDED MILK & PLANT-BASED ALTERNATIVES IN THE US: 2019-2022 ($ MILLION)

- EXHIBIT 32 GLOBAL LIQUID FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 33 INCREMENTAL GROWTH BY APPLICATION 2023 & 2029

- EXHIBIT 34 GLOBAL FUNCTIONAL MILK MARKET BY APPLICATION 2023 AND 2029 (% SHARE)

- EXHIBIT 35 GLOBAL PREVALENCE OF AUTOIMMUNE DISEASE

- EXHIBIT 36 GLOBAL PREVALENCE OF HEART DISEASES IN 2019, 2021, AND 2023

- EXHIBIT 37 GLOBAL PREVALENCE OF OSTEOPOROSIS

- EXHIBIT 38 GLOBAL IMMUNITY & DISEASE MANAGEMENT FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 39 PREVALENCE OF OBESITY AND OVERWEIGHT GLOBALLY BY 2035

- EXHIBIT 40 GLOBAL WEIGHT MANAGEMENT FUNCTIONAL MARKET 2023-2029 ($ BILLION)

- EXHIBIT 41 CANCER STATISTICS IN THE US & GLOBAL: 2022 & 2040

- EXHIBIT 42 GLOBAL PREVALENCE OF NUTRITION DEFICIENCY IN KIDS 2020, 2021, AND 2030

- EXHIBIT 43 GLOBAL CLINICAL NUTRITION FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 44 GLOBAL IMPACT OF ACNE PREVALENCE AND STATISTICS IN THE US AND EUROPE: (2022)

- EXHIBIT 45 GLOBAL OTHERS FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 46 INCREMENTAL GROWTH BY AGE 2023 & 2029

- EXHIBIT 47 GLOBAL 14-19 AGE GROUP FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 48 GLOBAL PREVALENCE OF DIABETES IN THE 20 AND ABOVE AGE GROUP IN 2021 ($ MILLION)

- EXHIBIT 49 GLOBAL 20-64 AGE GROUP FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 50 KEY STATISTICS ON CANCER AND UNDERNUTRITION IN THE US AND GLOBALLY

- EXHIBIT 51 GLOBAL CHILDREN UNDER 5 YEARS AFFECTED BY STUNTING, WASTING, AND OBESITY IN 2022 (MILLION)

- EXHIBIT 52 PREVALENCE OF SEVERE WASTING AND OBESITY IN INDIA, INDONESIA, NEW ZEALAND & AUSTRALIA

- EXHIBIT 53 GLOBAL 1-13 AGE GROUP FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 54 AGING POPULATION AND HIP FRACTURES IN APAC & LATIN AMERICA

- EXHIBIT 55 GLOBAL 64 & ABOVE AGE GROUP FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 56 INCREMENTAL GROWTH BY DISTRIBUTION CHANNEL 2023 & 2029

- EXHIBIT 57 GLOBAL HYPERMARKET FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 58 GLOBAL CONVENIENCE STORES FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 59 GLOBAL ONLINE FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 60 GLOBAL GROCERY STORES FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 61 GLOBAL SPECIALTY STORES FUNCTIONAL MILK MARKET 2023-2029 ($ BILLION)

- EXHIBIT 62 GLOBAL FUNCTIONAL MILK MARKET BY INSTITUTIONAL SALES 2023-2029 ($ BILLION)

- EXHIBIT 63 INCREMENTAL GROWTH BY GEOGRAPHY 2023 & 2029

- EXHIBIT 64 MARKET SHARE OF REGIONS: 2029 (%)

- EXHIBIT 65 FUNCTIONAL MILK MARKET IN APAC 2023-2029 ($ BILLION)

- EXHIBIT 66 INCREMENTAL GROWTH IN APAC 2023 & 2029

- EXHIBIT 67 PREVALENCE OF OVERWEIGHT AND DIABETES IN CHINA, 2022 & 2023

- EXHIBIT 68 FUNCTIONAL MILK MARKET IN CHINA 2023-2029 ($ BILLION)

- EXHIBIT 69 KEY STATISTICS OF BONE DENSITY, CALCIUM INTAKE, AND AGEING POPULATION IN JAPAN 2023 (%)

- EXHIBIT 70 FUNCTIONAL MILK MARKET IN JAPAN 2023-2029 ($ BILLION)

- EXHIBIT 71 PROJECTION OF OBESITY IN ADULTS AND CHILDREN IN SOUTH KOREA BY 2030

- EXHIBIT 72 FUNCTIONAL MILK MARKET IN SOUTH KOREA 2023-2029 ($ BILLION)

- EXHIBIT 73 PREVALENCE OF DIABETES IN AUSTRALIA: 2021

- EXHIBIT 74 FUNCTIONAL MILK MARKET IN AUSTRALIA 2023-2029 ($ BILLION)

- EXHIBIT 75 FUNCTIONAL MILK MARKET IN INDIA 2023-2029 ($ BILLION)

- EXHIBIT 76 PREVALENCE OF OBESITY & DIABETES IN WOMEN AND MEN IN THAILAND, 2022 (%)

- EXHIBIT 77 FUNCTIONAL MILK MARKET IN THAILAND 2023-2029 ($ BILLION)

- EXHIBIT 78 PROJECTED LIVES SAVED ANNUALLY FROM CANCER IN INDONESIA: 2024-2030

- EXHIBIT 79 PREVALENCE OF OVERWEIGHT IN SCHOOL AGE CHILDREN, ADOLESCENTS, AND ADULTS 2018 (MILLION)

- EXHIBIT 80 FUNCTIONAL MILK MARKET IN INDONESIA 2023-2029 ($ BILLION)

- EXHIBIT 81 FUNCTIONAL MILK MARKET IN THE PHILIPPINES 2023-2029 ($ BILLION)

- EXHIBIT 82 PREVALENCE OF OBESITY IN CHILDREN AND ADULTS IN MALAYSIA FROM 2020-2035

- EXHIBIT 83 FUNCTIONAL MILK MARKET IN MALAYSIA 2023-2029 ($ BILLION)

- EXHIBIT 84 PREVALENCE OF OBESITY IN CHILDREN AND ADULTS IN VIETNAM: 2021

- EXHIBIT 85 FUNCTIONAL MILK MARKET IN VIETNAM 2023-2029 ($ BILLION)

- EXHIBIT 86 FUNCTIONAL MILK IN NORTH AMERICA 2023 & 2029 (% MARKET SHARE)

- EXHIBIT 87 FUNCTIONAL MILK MARKET IN NORTH AMERICA 2023-2029 ($ BILLION)

- EXHIBIT 88 INCREMENTAL GROWTH IN NORTH AMERICA 2023 & 2029

- EXHIBIT 89 PREVALENCE OF DIABETES IN US: 2021 (MILLION)

- EXHIBIT 90 KEY STATISTICS OF OBESITY IN THE US, 2021

- EXHIBIT 91 FUNCTIONAL MILK MARKET IN THE US 2023-2029 ($ BILLION)

- EXHIBIT 92 FUNCTIONAL MILK MARKET IN CANADA 2023-2029 ($ BILLION)

- EXHIBIT 93 FUNCTIONAL MILK MARKET IN EUROPE 2023-2029 ($ BILLION)

- EXHIBIT 94 INCREMENTAL GROWTH IN EUROPE 2023 & 2029

- EXHIBIT 95 KEY STATISTICS OF OVERWEIGHT AND HEALTHY DRINK IN GERMANY, 2022 (%)

- EXHIBIT 96 FUNCTIONAL MILK MARKET IN GERMANY 2023-2029 ($ BILLION)

- EXHIBIT 97 PREVALENCE OF OVERWEIGHT AND OBESITY IN FRANCE BY 2040

- EXHIBIT 98 FUNCTIONAL MILK MARKET IN FRANCE 2023-2029 ($ BILLION)

- EXHIBIT 99 PREVALENCE OF OBESITY IN ENGLAND FROM 2021-2022 (%)

- EXHIBIT 100 FUNCTIONAL MILK MARKET IN THE UK 2023-2029 ($ BILLION)

- EXHIBIT 101 PREVALENCE OF OBESITY IN SPAIN, 2023 AND 2030

- EXHIBIT 102 FUNCTIONAL MILK MARKET IN SPAIN 2023-2029 ($ BILLION)

- EXHIBIT 103 KEY STATISTICS OF OBESITY IN ITALY, 2020-2035 (%)

- EXHIBIT 104 FUNCTIONAL MILK MARKET IN ITALY 2023-2029 ($ BILLION)

- EXHIBIT 105 PREVALENCE OF OBESITY IN RUSSIA, 2010 TO 2030 (%)

- EXHIBIT 106 FUNCTIONAL MILK MARKET IN RUSSIA 2023-2029 ($ BILLION)

- EXHIBIT 107 FUNCTIONAL MILK MARKET IN LATIN AMERICA 2023-2029 ($ BILLION)

- EXHIBIT 108 INCREMENTAL GROWTH IN LATIN AMERICA 2023 & 2029

- EXHIBIT 109 PREVALENCE OF OBESITY IN ADULTS AND CHILDREN IN BRAZIL, 2020 AND 2021

- EXHIBIT 110 FUNCTIONAL MILK MARKET IN BRAZIL 2023-2029 ($ BILLION)

- EXHIBIT 111 FUNCTIONAL MILK MARKET IN MEXICO 2023-2029 ($ BILLION)

- EXHIBIT 112 KEY STATISTICS OF OBESITY IN CHILDREN IN ARGENTINA 2022 AND 2030

- EXHIBIT 113 FUNCTIONAL MILK MARKET IN ARGENTINA 2023-2029 ($ BILLION)

- EXHIBIT 114 FUNCTIONAL MILK MARKET IN MIDDLE EAST AND AFRICA 2023-2029 ($ BILLION)

- EXHIBIT 115 INCREMENTAL GROWTH IN THE MIDDLE EAST AND AFRICA 2023 & 2029

- EXHIBIT 116 PROJECTION OF POPULATION BY AGE GROUP IN TURKEY FROM 2040 AND 2080 (%)

- EXHIBIT 117 FUNCTIONAL MILK MARKET IN TURKEY 2023-2029 ($ BILLION)

- EXHIBIT 118 FUNCTIONAL MILK MARKET IN SOUTH AFRICA 2023-2029 ($ BILLION)

- EXHIBIT 119 SAUDI ARABIA KEY STATISTICS OF CHRONIC DISEASES, AGING POPULATION AND OBESITY IN 2050, 2022 (%)

- EXHIBIT 120 PREVALENCE OF CHRONIC DISEASES IN SAUDI ARABIA MEN, 2022 (%)

- EXHIBIT 121 FUNCTIONAL MILK MARKET IN SAUDI ARABIA 2023-2029 ($ BILLION)

- EXHIBIT 122 COMPETITIVE FACTORS IN GLOBAL FUNCTIONAL MILK MARKET

- EXHIBIT 123 KEY CAVEATS

List Of Tables

LIST OF TABLES

- TABLE 1 AGE-WISE DAILY CALCIUM INTAKE

- TABLE 2 ESTIMATED GLOBAL PREVALENCE & NUMBER OF ADULTS TO LIVE WITH OBESITY (2025-2030)

- TABLE 3 GLOBAL PREVALENCE OF OBESITY BY 2025, 2030, AND 2035 (MILLION)

- TABLE 4 COMPANIES LAUNCHING NEW PRODUCTS WITH INNOVATIVE FEATURES

- TABLE 5 KEY MANUFACTURER COMPANIES OF SKIMMED MILK POWDER

- TABLE 6 POWDER FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 7 KEY MANUFACTURER COMPANIES OF LIQUID MILK

- TABLE 8 LIQUID FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 9 IMMUNITY AND DISEASE MANAGEMENT FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 10 WEIGHT MANAGEMENT FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 11 CLINICAL NUTRITION FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 12 OTHERS FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 13 DAILY CALCIUM INTAKE BY AGE GROUP

- TABLE 14 DAILY PROTEIN INTAKE FOR INDIVIDUALS BETWEEN AGES 14-18

- TABLE 15 GLOBAL 14-19 AGE GROUP FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 16 GLOBAL 20-64 AGE GROUP FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 17 KEY MANUFACTURERS OF FUNCTIONAL MILK FOR CHILDREN SEGMENT

- TABLE 18 GLOBAL 1-13 AGE GROUP FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 19 GLOBAL 64 & ABOVE AGE GROUP FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 20 WALMART RETAIL OUTLETS BY COUNTRIES

- TABLE 21 GLOBAL HYPERMARKET FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 22 GLOBAL CONVENIENCE STORES FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 23 GLOBAL ONLINE FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 24 GLOBAL GROCERY STORES FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 25 GLOBAL SPECIALTY STORES FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 26 NUMBER OF HOSPITALS BY COUNTRY

- TABLE 27 GLOBAL INSTITUTIONAL SALES FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 28 FUNCTIONAL MILK MARKET IN APAC BY FORM 2023-2029 ($ BILLION)

- TABLE 29 FUNCTIONAL MILK MARKET IN APAC BY APPLICATIONS 2023-2029 ($ BILLION)

- TABLE 30 FUNCTIONAL MILK MARKET IN APAC BY AGE 2023-2029 ($ BILLION)

- TABLE 31 FUNCTIONAL MILK MARKET IN APAC BY DISTRIBUTION CHANNEL 2023-2029 ($ BILLION)

- TABLE 32 FUNCTIONAL MILK MARKET IN NORTH AMERICA BY FORM 2023-2029 ($ BILLION)

- TABLE 33 FUNCTIONAL MILK MARKET IN NORTH AMERICA BY APPLICATIONS 2023-2029 ($ BILLION)

- TABLE 34 FUNCTIONAL MILK MARKET IN NORTH AMERICA BY AGE 2023-2029 ($ BILLION)

- TABLE 35 FUNCTIONAL MILK MARKET IN NORTH AMERICA BY DISTRIBUTION CHANNEL 2023-2029 ($ BILLION)

- TABLE 36 FUNCTIONAL MILK MARKET IN EUROPE BY FORM 2023-2029 ($ BILLION)

- TABLE 37 FUNCTIONAL MILK MARKET IN EUROPE BY APPLICATIONS 2023-2029 ($ BILLION)

- TABLE 38 FUNCTIONAL MILK MARKET IN EUROPE BY AGE 2023-2029 ($ BILLION)

- TABLE 39 FUNCTIONAL MILK MARKET IN EUROPE BY DISTRIBUTION CHANNEL 2023-2029 ($ BILLION)

- TABLE 40 FUNCTIONAL MILK MARKET IN LATIN AMERICA BY FORM 2023-2029 ($ BILLION)

- TABLE 41 FUNCTIONAL MILK MARKET IN LATIN AMERICA BY APPLICATIONS 2023-2029 ($ BILLION)

- TABLE 42 FUNCTIONAL MILK MARKET IN LATIN AMERICA BY AGE 2023-2029 ($ BILLION)

- TABLE 43 FUNCTIONAL MILK MARKET IN LATIN AMERICA BY DISTRIBUTION CHANNEL 2023-2029 ($ BILLION)

- TABLE 44 FUNCTIONAL MILK MARKET IN THE MIDDLE EAST AND AFRICA BY FORM 2023-2029 ($ BILLION)

- TABLE 45 FUNCTIONAL MILK MARKET IN THE MIDDLE EAST AND AFRICA BY APPLICATIONS 2023-2029 ($ BILLION)

- TABLE 46 FUNCTIONAL MILK MARKET IN THE MIDDLE EAST AND AFRICA BY AGE 2023-2029 ($ BILLION)

- TABLE 47 FUNCTIONAL MILK MARKET IN THE MIDDLE EAST AND AFRICA BY DISTRIBUTION CHANNEL 2023-2029 ($ BILLION)

- TABLE 48 VENDORS RANKING IN FUNCTIONAL MILK MARKET - 2022

- TABLE 49 ABBOTT: MAJOR PRODUCT OFFERINGS

- TABLE 50 DANONE: MAJOR PRODUCT OFFERINGS

- TABLE 51 LACTALIS INTERNATIONAL: MAJOR PRODUCT OFFERINGS

- TABLE 52 NESTLE: MAJOR PRODUCT OFFERINGS

- TABLE 53 AROMA MILK PRODUCTS: MAJOR PRODUCT OFFERINGS

- TABLE 54 ARLA FOODS AMBA: MAJOR PRODUCT OFFERINGS

- TABLE 55 AGROPUR: MAJOR PRODUCT OFFERINGS

- TABLE 56 BEST WAY INGREDIENTS: MAJOR PRODUCT OFFERINGS

- TABLE 57 BEST HEALTH FOODS: MAJOR PRODUCT OFFERINGS

- TABLE 58 BRIGHT LIFECARE: MAJOR PRODUCT OFFERINGS

- TABLE 59 CAPSA: MAJOR PRODUCT OFFERINGS

- TABLE 60 CREDITON DAIRY: MAJOR PRODUCT OFFERINGS

- TABLE 61 CAYUGA MILK INGREDIENTS: MAJOR PRODUCT OFFERINGS

- TABLE 62 CLOVER SONOMA: MAJOR PRODUCT OFFERINGS

- TABLE 63 DAIRY FARMERS OF AMERICA: MAJOR PRODUCT OFFERINGS

- TABLE 64 DARIGOLD: MAJOR PRODUCT OFFERINGS

- TABLE 65 EHRMANN: MAJOR PRODUCT OFFERINGS

- TABLE 66 FONTERRA: MAJOR PRODUCT OFFERINGS

- TABLE 67 F&N DAIRIES: MAJOR PRODUCT OFFERINGS

- TABLE 68 FAIRLIFE: MAJOR PRODUCT OFFERINGS

- TABLE 69 FRIESLANDCAMPINA: MAJOR PRODUCT OFFERINGS

- TABLE 70 GLANBIA: MAJOR PRODUCT OFFERINGS

- TABLE 71 GCMMF: MAJOR PRODUCT OFFERINGS

- TABLE 72 GAY LEA FOODS: MAJOR PRODUCT OFFERINGS

- TABLE 73 HERITAGE FOODS: MAJOR PRODUCT OFFERINGS

- TABLE 74 HP HOOD: MAJOR PRODUCT OFFERINGS

- TABLE 75 INGREDIA: MAJOR PRODUCT OFFERINGS

- TABLE 76 LAND O' LAKES: MAJOR PRODUCT OFFERINGS

- TABLE 77 LYCOTEC: MAJOR PRODUCT OFFERINGS

- TABLE 78 MCNEIL NUTRITIONALS: MAJOR PRODUCT OFFERINGS

- TABLE 79 MEGMILK SNOW BRAND: MAJOR PRODUCT OFFERINGS

- TABLE 80 MILLIGANS FOOD GROUP: MAJOR PRODUCT OFFERINGS

- TABLE 81 MOTHER DAIRY FRUIT & VEGETABLE: MAJOR PRODUCT OFFERINGS

- TABLE 82 ORGANIC VALLEY: MAJOR PRODUCT OFFERINGS

- TABLE 83 PROCAL DAIRIES: MAJOR PRODUCT OFFERINGS

- TABLE 84 PARAG MILK FOODS: MAJOR PRODUCT OFFERINGS

- TABLE 85 SADAFCO: MAJOR PRODUCT OFFERINGS

- TABLE 86 SLEEPWELL: MAJOR PRODUCT OFFERINGS

- TABLE 87 STOLLE MILK BIOLOGICS: MAJOR PRODUCT OFFERINGS

- TABLE 88 SYNLAIT: MAJOR PRODUCT OFFERINGS

- TABLE 89 TIRLAN: MAJOR PRODUCT OFFERINGS

- TABLE 90 TESCO: MAJOR PRODUCT OFFERINGS

- TABLE 91 VINDIJA D. D.: MAJOR PRODUCT OFFERINGS

- TABLE 92 VALFOO: MAJOR PRODUCT OFFERINGS

- TABLE 93 VINAMILK: MAJOR PRODUCT OFFERINGS

- TABLE 94 GLOBAL FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 ($ BILLION)

- TABLE 95 GLOBAL FUNCTIONAL MILK MARKET BY GEOGRAPHY 2023-2029 (%)

- TABLE 96 GLOBAL FUNCTIONAL MILK MARKET BY FORM 2023-2029 ($ BILLION)

- TABLE 97 GLOBAL FUNCTIONAL MILK MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 98 GLOBAL FUNCTIONAL MILK MARKET BY AGE GROUP 2023-2029 ($ BILLION)

- TABLE 99 GLOBAL FUNCTIONAL MILK MARKET BY DISTRIBUTION CHANNEL 2023-2029 ($ BILLION)

- TABLE 100 APAC FUNCTIONAL MILK MARKET BY FORM 2023-2029 ($ BILLION)

- TABLE 101 APAC FUNCTIONAL MILK MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 102 APAC FUNCTIONAL MILK MARKET BY AGE GROUP 2023-2029 ($ BILLION)

- TABLE 103 APAC FUNCTIONAL MILK MARKET BY DISTRIBUTION CHANNEL 2023-2029 ($ BILLION)

- TABLE 104 NORTH AMERICA FUNCTIONAL MILK MARKET BY FORM 2023-2029 ($ BILLION)

- TABLE 105 NORTH AMERICA FUNCTIONAL MILK MARKET BY APPLICATIONS 2023-2029 ($ BILLION)

- TABLE 106 NORTH AMERICA FUNCTIONAL MILK MARKET BY AGE GROUP 2023-2029 ($ BILLION)

- TABLE 107 NORTH AMERICA FUNCTIONAL MILK MARKET BY DISTRIBUTION CHANNEL 2023-2029 ($ BILLION)

- TABLE 108 EUROPE FUNCTIONAL MILK MARKET BY FORM 2023-2029 ($ BILLION)

- TABLE 109 EUROPE FUNCTIONAL MILK MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 110 EUROPE FUNCTIONAL MILK MARKET BY AGE GROUP 2023-2029 ($ BILLION)

- TABLE 111 EUROPE FUNCTIONAL MILK MARKET BY DISTRIBUTION CHANNEL 2023-2029 ($ BILLION)

- TABLE 112 LATIN AMERICA FUNCTIONAL MILK MARKET BY FORM 2023-2029 ($ BILLION)

- TABLE 113 LATIN AMERICA FUNCTIONAL MILK MARKET BY APPLICATION 2023-2029 ($ BILLION)

- TABLE 114 LATIN AMERICA FUNCTIONAL MILK MARKET BY AGE GROUP 2023-2029 ($ BILLION)

- TABLE 115 LATIN AMERICA FUNCTIONAL MILK MARKET BY DISTRIBUTION CHANNEL 2023-2029 ($ BILLION)

- TABLE 116 MIDDLE EAST AND AFRICA FUNCTIONAL MILK MARKET BY FORM 2023-2029 ($ BILLION)

- TABLE 117 MIDDLE EAST AND AFRICA FUNCTIONAL MILK MARKET BY APPLICATIONS 2023-2029 ($ BILLION)

- TABLE 118 MIDDLE EAST AND AFRICA FUNCTIONAL MILK MARKET BY AGE GROUP 2023-2029 ($ BILLION)

- TABLE 119 MIDDLE EAST AND AFRICA FUNCTIONAL MILK MARKET BY DISTRIBUTION CHANNEL 2023-2029 ($ BILLION)

- TABLE 120 CURRENCY CONVERSION 2017-2023

The global functional milk market was valued at USD 27.00 billion in 2023 and is expected to grow at a CAGR of 7.53% from 2023-2029.

MARKET TRENDS & DRIVERS

Introduction of Clean Label Products in Functional Milk

The growing consumer preference for clean-label products has significantly increased the demand for functional milk. Clean-label products are characterized by simple and easily understandable ingredient lists, free from artificial additives and preservatives. As consumers become more health-conscious and seek transparency in their food choices, they are turning towards functional milk that provides essential nutrients and aligns with their clean eating preferences. Furthermore, functional milk, improved with vitamins, minerals, and other bioactive compounds, caters to consumers' health and wellness needs. These products often boast improved digestion, enhanced immune support, and better nutritional profiles. These functional milk products' clear and straightforward labeling resonates with consumers looking for wholesome, minimally processed options. For instance, Dairy Farmers of America focuses on developing clean label solutions such as no artificial color, no artificial flavor, and more, which increases the consumer base and demand for the products in the market.

Vendors Focus on Product Innovation

Product innovation is pivotal in shaping the functional milk market dynamics, significantly impacting consumer preferences and industry competition. The introduction of novel ingredients, formulations, and technologies has the potential to revolutionize the way consumers perceive and engage with functional milk products. Innovations such as fortification with vitamins, minerals, probiotics, or other health-enhancing components can address evolving consumer demands for wellness and nutritional benefits. These advancements cater to health-conscious consumers and provide opportunities for market differentiation among competitors. Moreover, product innovation can stimulate consumer interest, drive market growth, and establish a brand's reputation as an industry leader. As the functional milk market evolves, businesses that embrace and implement innovative strategies will likely gain a competitive edge, fostering sustainability and growth in an increasingly dynamic market landscape.

SEGMENTATION INSIGHTS

INSIGHTS BY FORM

The powder form segment dominated the global functional milk market in 2023 and is projected to continue the trend during the forecast period. This notable growth can be attributed to various factors. First, the appeal of powder lies in its extended shelf life, addressing concerns related to product longevity. In addition, the powdered form facilitates convenient transportation, making it an attractive option for both manufacturers and consumers. Moreover, the cost-effectiveness of powder production further contributed to its increased demand in the functional milk market. These factors fueled the demand for functional milk in powder form, highlighting its versatility and economic advantages in the evolving market landscape.

Segmentation by Form

- Powder

- Liquid

INSIGHTS BY APPLICATIONS

The global functional milk market by applications is segmented into immunity & disease management, weight management, and clinical nutrition. In 2023, immunity & disease management had the highest share in the application segment. This surge in demand can be attributed to the increasing prevalence of various health concerns, including heart disease, osteoporosis, autoimmune diseases, and other related conditions. As individuals become more conscious about their health, the emphasis on bolstering immunity and effectively managing diseases has become paramount. This trend reflects a broader societal shift towards proactive healthcare measures, driving innovation and investments in technologies and solutions that cater to immunity enhancement and disease management. Furthermore, weight management exhibits a remarkable compound annual growth rate during the forecast period. This surge is attributed to the rising demand for functional milk, fueled by concerns related to obesity, cardiovascular diseases, and other health factors. The increasing emphasis on weight management reflects a growing awareness of health issues, driving the demand for functional milk products that contribute to overall well-being.

Segmentation by Applications

- Immunity & Disease Management

- Weight Management

- Clinical Nutrition

- Others

INSIGHTS BY AGE

The 14-19 age segment accounted for the highest revenue share of the global functional milk market in 2023. With the demand for functional milk growing among the age group of 15-19 in the US, it is crucial to emphasize the potential health benefits associated with its consumption. The statistics on cancer diagnoses and deaths in this age range, marketing functional milk as a source of nutrients that may contribute to overall well-being and potentially aid in disease prevention could be effective. Highlighting ingredients known for their health properties, such as vitamins, minerals, and antioxidants, can be a key strategy. In addition, engaging in educational campaigns through various channels, including social media, to raise awareness about the importance of maintaining a healthy lifestyle, including dietary choices, may further boost the demand for functional milk among this demographic.

Segmentation by Age

- 14-19

- 20-64

- 1-13

- 64 & Above

INSIGHTS BY DISTRIBUTION CHANNEL

The global functional milk market by distribution channel is segmented into hypermarkets, convenience stores, online grocery stores, specialty stores, and institutional sales. In 2023, the hypermarket distribution channel emerged as the dominant segment, capturing the highest market share of over 19%. Hypermarkets strategically employed various marketing techniques, such as discount offers, innovative bundling offers, and engaging in-store demonstrations, to highlight the numerous benefits of functional milk. These initiatives attracted health-conscious consumers and elevated the overall shopping experience. The hypermarket's effective communication of the advantages of functional milk through these promotional strategies played a pivotal role in securing its leading position in the market. Furthermore, convenience stores hold a significant position in the industry, and their success can be attributed to their ability to offer a convenient solution for swift, on-the-go purchases. Convenience stores strategically cater to a target demographic characterized by busy lifestyles, positioning themselves as an accessible and time-efficient choice for consumers.

Segmentation by Distribution Channel

- Hypermarkets

- Convenience Stores

- Online

- Grocery Stores

- Specialty Stores

- Institutional Sales

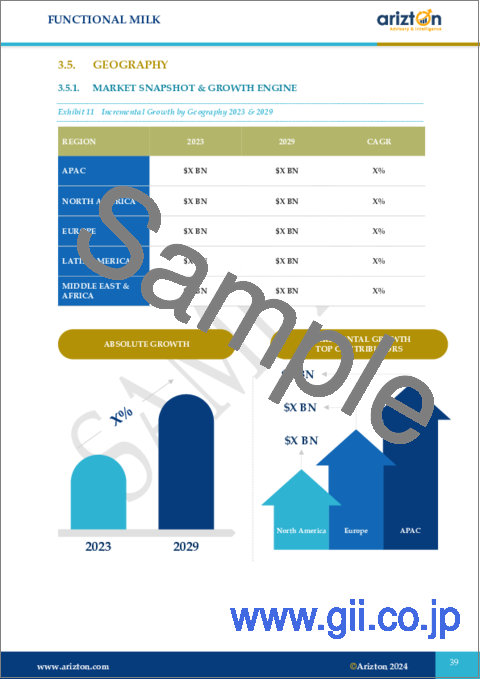

GEOGRAPHICAL ANALYSIS

APAC dominated the global functional milk market share, accounting for over 31% in 2023. In APAC, demand for functional milk has experienced robust growth, driven by factors such as awareness, consumer willingness to pay more, and a heightened focus on preventive healthcare. Furthermore, the rising prevalence of chronic diseases in the APAC has heightened health consciousness, leading consumers to seek functional milk products with potential health benefits. The increasing aging population in China, Japan, and other countries in the APAC is likely to boost the demand for functional milk, driven by a growing focus on health and nutrition among older adults. The rising overweight and obesity in children and adults in the APAC is fueling an increasing demand for functional milk products as consumers seek healthier alternatives to address dietary and nutritional needs.

Segmentation by Geography

- APAC

- China

- Japan

- South Korea

- Australia

- India

- Thailand

- Indonesia

- Philippines

- Malaysia

- Vietnam

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Spain

- Italy

- Russia

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East & Africa

- Turkey

- Saudi Africa

- Saudi Arabia

VENDOR LANDSCAPE

The global functional milk market is characterized by a high level of fragmentation, with several major international and regional players competing for industry share alongside smaller local companies. Despite this fragmentation, a few key players, including Nestle, Danone, Abbott, and Lactalis International, wield significant influence, holding substantial functional milk market shares. Complementing these dominant players are numerous regional and smaller companies that contribute to the overall diversity of the industry.

Key Developments in the Functional Milk Market

- In 2022, ABBOTT spent on research and development around USD 2,888 million to increase its consumer base and generate more revenue in the industry.

- By 2025, DANONE will launch ≥85% vol Kids dairy fortified with relevant vitamins & minerals.

- In 2022, NESTLE introduced an infant formula with HMO, which helps increase brain myelination, support gut health, and strengthen immunity.

Key Company Profiles

- ABBOTT

- Danone

- Lactalis International

- Nestle

Other Prominent Vendors

- Aroma Milk Products

- Arla Foods amba

- Best Way Ingredients

- Best Health Foods

- Bright LifeCare

- CAPSA

- Crediton Dairy

- Dairy Farmers of America

- Ehrmann

- Fonterra

- Glanbia

- GCMMF

- Heritage Foods

- INGREDIA

- Land O' Lakes

- Lycotec

- MEGMILK SNOW BRAND

- Milligans Food Group

- Mother Dairy Fruit & Vegetable

- Parag Milk Foods

- SADAFCO

- SLEEPWELL

- Stolle Milk Biologics

- Synlait

- Tirlan

- Tesco

- Vindija d.d.

- Valfoo

- Vinamilk

- F&N Dairies

- FrieslandCampina

- Organic Valley

- Clover Sonoma

- Darigold

- Fairlife

- McNeil Nutritionals

- Agropur

- Gay Lea Foods Co-operative Ltd.

- Cayuga Milk Ingredients

- Procal Dairies

- HP Hood

KEY QUESTIONS ANSWERED:

1. How big is the functional milk market?

2. What is the growth rate of the global functional milk market?

3. Which region dominates the global functional milk market share?

4. What are the significant trends in the functional milk market?

5. Who are the key players in the global functional milk market?

TABLE OF CONTENTS

1. SCOPE & COVERAGE

- 1.1. MARKET DEFINITION

- 1.1.1. INCLUSIONS

- 1.1.2. EXCLUSIONS

- 1.1.3. MARKET ESTIMATION CAVEATS

- 1.2. SEGMENTS COVERED & DEFINITIONS

- 1.2.1. MARKET BY FORM

- 1.2.2. MARKET BY AGE

- 1.2.3. MARKET BY APPLICATION

- 1.2.4. MARKET BY DISTRIBUTION CHANNEL

- 1.2.6. REGIONS & COUNTRIES COVERED

- 1.3. MARKET DERIVATION

- 1.3.1. BASE YEAR

2. PREMIUM INSIGHTS

- 2.1. OPPORTUNITY POCKETS

- 2.2. MARKET DEFINITION

- 2.3. REPORT OVERVIEW

- 2.4. OPPORTUNITIES & CHALLENGE ANALYSIS

- 2.5. SEGMENT ANALYSIS

- 2.6. REGIONAL ANALYSIS

- 2.7. COMPETITIVE LANDSCAPE

3. MARKET AT A GLANCE

4. INTRODUCTION

- 4.1. OVERVIEW

- 4.1.1. REQUIREMENTS OF MILK IN LIFE STAGES

- 4.1.2. BONE HEALTH

- 4.1.3. SWOT ANALYSIS

- 4.2. RISING DEMAND FOR FUNCTIONAL FOOD

- 4.2.1. COVID-19 IMPACT ON FUNCTIONAL FOOD

- 4.3. VALUE CHAIN ANALYSIS

- 4.3.1. PRODUCTION

- 4.3.2. PROCESSING

- 4.3.3. PACKAGING

- 4.3.4. DISTRIBUTORS

- 4.3.5. RETAIL AND B2B

- 4.3.6. CUSTOMERS AND CONSUMERS

5. MARKET OPPORTUNITIES & TRENDS

- 5.1. INTRODUCTION OF CLEAN LABEL PRODUCTS IN FUNCTIONAL MILK

- 5.2. INCREASED DEMAND FOR LACTOSE-FREE MILK

- 5.3. PROBIOTICS AND DIGESTIVE HEALTH

6. MARKET GROWTH ENABLERS

- 6.1. RISE IN THE PREVALENCE OF OBESITY

- 6.2. GROWING DEMAND FOR FUNCTIONAL MILK ENHANCING MOBILITY

- 6.3. VENDORS FOCUS ON PRODUCT INNOVATION

7. MARKET RESTRAINTS

- 7.1. INCREASING ALTERNATIVES FOR FUNCTIONAL MILK

- 7.2. HIGH PRODUCTION COST OF FUNCTIONAL MILK

- 7.3. STRINGENT GOVERNMENT REGULATIONS

8. MARKET LANDSCAPE

- 8.1. MARKET OVERVIEW

- 8.2. MARKET SIZE & FORECAST

- 8.3. VENDOR ANALYSIS

- 8.4. DEMAND INSIGHTS

- 8.5. FIVE FORCES ANALYSIS

- 8.5.1. THREAT OF NEW ENTRANTS

- 8.5.2. BARGAINING POWER OF SUPPLIERS

- 8.5.3. BARGAINING POWER OF BUYERS

- 8.5.4. THREAT OF SUBSTITUTES

- 8.5.5. COMPETITIVE RIVALRY

9. FORM

- 9.1. MARKET SNAPSHOT & GROWTH ENGINE

- 9.2. MARKET OVERVIEW

- 9.3. POWDER

- 9.3.1. MARKET OVERVIEW

- 9.3.2. MARKET SIZE & FORECAST

- 9.3.3. MARKET BY GEOGRAPHY

- 9.4. LIQUID

- 9.4.1. MARKET OVERVIEW

- 9.4.2. MARKET SIZE & FORECAST

- 9.4.3. MARKET BY GEOGRAPHY

10. APPLICATIONS

- 10.1. MARKET SNAPSHOT & GROWTH ENGINE

- 10.2. MARKET OVERVIEW

- 10.1. IMMUNITY & DISEASE MANAGEMENT

- 10.1.1. MARKET OVERVIEW

- 10.1.2. MARKET SIZE & FORECAST

- 10.1.3. MARKET BY GEOGRAPHY

- 10.2. WEIGHT MANAGEMENT

- 10.2.1. MARKET OVERVIEW

- 10.2.2. MARKET SIZE & FORECAST

- 10.2.3. MARKET BY GEOGRAPHY

- 10.3. CLINICAL NUTRITION

- 10.3.1. MARKET OVERVIEW

- 10.3.2. MARKET SIZE & FORECAST

- 10.3.3. MARKET BY GEOGRAPHY

- 10.4. OTHERS

- 10.4.1. MARKET OVERVIEW

- 10.4.2. MARKET SIZE & FORECAST

- 10.4.3. MARKET BY GEOGRAPHY

11. AGE

- 11.1. MARKET SNAPSHOT & GROWTH ENGINE

- 11.2. MARKET OVERVIEW

- 11.3. 14-19 AGE GROUP

- 11.3.1. MARKET OVERVIEW

- 11.3.2. MARKET SIZE & FORECAST

- 11.3.3. MARKET BY GEOGRAPHY

- 11.4. 20-64 AGE GROUP

- 11.4.1. MARKET OVERVIEW

- 11.4.2. MARKET SIZE & FORECAST

- 11.4.3. MARKET BY GEOGRAPHY

- 11.5. 1-13 AGE GROUP

- 11.5.1. MARKET OVERVIEW

- 11.5.2. MARKET SIZE & FORECAST

- 11.5.3. MARKET BY GEOGRAPHY

- 11.6. 64 & ABOVE

- 11.6.1. MARKET OVERVIEW

- 11.6.2. MARKET SIZE & FORECAST

- 11.6.3. MARKET BY GEOGRAPHY

12. DISTRIBUTION CHANNEL

- 12.1. MARKET SNAPSHOT & GROWTH ENGINE

- 12.2. MARKET OVERVIEW

- 12.3. HYPERMARKETS

- 12.3.1. MARKET OVERVIEW

- 12.3.2. MARKET SIZE & FORECAST

- 12.3.3. MARKET BY GEOGRAPHY

- 12.4. CONVENIENCE STORES

- 12.4.1. MARKET OVERVIEW

- 12.4.2. MARKET SIZE & FORECAST

- 12.4.3. MARKET BY GEOGRAPHY

- 12.5. ONLINE

- 12.5.1. MARKET OVERVIEW

- 12.5.2. MARKET SIZE & FORECAST

- 12.5.3. MARKET BY GEOGRAPHY

- 12.6. GROCERY STORES

- 12.6.1. MARKET OVERVIEW

- 12.6.2. MARKET SIZE & FORECAST

- 12.6.3. MARKET BY GEOGRAPHY

- 12.7. SPECIALTY STORES

- 12.7.1. MARKET OVERVIEW

- 12.7.2. MARKET SIZE & FORECAST

- 12.7.3. MARKET BY GEOGRAPHY

- 12.8. INSTITUTIONAL SALES

- 12.8.1. MARKET OVERVIEW

- 12.8.2. MARKET SIZE & FORECAST

- 12.8.3. MARKET BY GEOGRAPHY

13. GEOGRAPHY

- 13.1. MARKET SNAPSHOT & GROWTH ENGINE

- 13.2. GEOGRAPHIC OVERVIEW

14. APAC

- 14.1. MARKET OVERVIEW

- 14.2. MARKET SIZE & FORECAST

- 14.3. FORM

- 14.3.1. MARKET SIZE & FORECAST

- 14.4. APPLICATIONS

- 14.4.1. MARKET SIZE & FORECAST

- 14.5. AGE

- 14.5.1. MARKET SIZE & FORECAST

- 14.6. DISTRIBUTION CHANNEL

- 14.6.1. MARKET SIZE & FORECAST

- 14.7. KEY COUNTRIES

- 14.8. CHINA: MARKET SIZE & FORECAST

- 14.9. JAPAN: MARKET SIZE & FORECAST

- 14.10. SOUTH KOREA: MARKET SIZE & FORECAST

- 14.11. AUSTRALIA: MARKET SIZE & FORECAST

- 14.12. INDIA: MARKET SIZE & FORECAST

- 14.13. THAILAND: MARKET SIZE & FORECAST

- 14.14. INDONESIA: MARKET SIZE & FORECAST

- 14.15. PHILIPPINES: MARKET SIZE & FORECAST

- 14.16. MALAYSIA: MARKET SIZE & FORECAST

- 14.17. VIETNAM: MARKET SIZE & FORECAST

15. NORTH AMERICA

- 15.1. MARKET OVERVIEW

- 15.2. MARKET SIZE & FORECAST

- 15.3. FORM

- 15.3.1. MARKET SIZE & FORECAST

- 15.4. APPLICATIONS

- 15.4.1. MARKET SIZE & FORECAST

- 15.5. AGE

- 15.5.1. MARKET SIZE & FORECAST

- 15.6. DISTRIBUTION CHANNEL

- 15.6.1. MARKET SIZE & FORECAST

- 15.7. KEY COUNTRIES

- 15.8. US: MARKET SIZE & FORECAST

- 15.9. CANADA: MARKET SIZE & FORECAST

16. EUROPE

- 16.1. MARKET OVERVIEW

- 16.2. MARKET SIZE & FORECAST

- 16.3. FORM

- 16.3.1. MARKET SIZE & FORECAST

- 16.4. APPLICATIONS

- 16.4.1. MARKET SIZE & FORECAST

- 16.5. AGE

- 16.5.1. MARKET SIZE & FORECAST

- 16.6. DISTRIBUTION CHANNEL

- 16.6.1. MARKET SIZE & FORECAST

- 16.7. KEY COUNTRIES

- 16.8. GERMANY: MARKET SIZE & FORECAST

- 16.9. FRANCE: MARKET SIZE & FORECAST

- 16.10. UK: MARKET SIZE & FORECAST

- 16.11. SPAIN: MARKET SIZE & FORECAST

- 16.12. ITALY: MARKET SIZE & FORECAST

- 16.13. RUSSIA: MARKET SIZE & FORECAST

17. LATIN AMERICA

- 17.1. MARKET OVERVIEW

- 17.2. MARKET SIZE & FORECAST

- 17.3. FORM

- 17.3.1. MARKET SIZE & FORECAST

- 17.4. APPLICATIONS

- 17.4.1. MARKET SIZE & FORECAST

- 17.5. AGE

- 17.5.1. MARKET SIZE & FORECAST

- 17.6. DISTRIBUTION CHANNEL

- 17.6.1. MARKET SIZE & FORECAST

- 17.7. KEY COUNTRIES

- 17.8. BRAZIL: MARKET SIZE & FORECAST

- 17.9. MEXICO: MARKET SIZE & FORECAST

- 17.10. ARGENTINA: MARKET SIZE & FORECAST

18. MIDDLE EAST AND AFRICA

- 18.1. MARKET OVERVIEW

- 18.2. MARKET SIZE & FORECAST

- 18.3. FORM

- 18.3.1. MARKET SIZE & FORECAST

- 18.4. APPLICATIONS

- 18.4.1. MARKET SIZE & FORECAST

- 18.5. AGE

- 18.5.1. MARKET SIZE & FORECAST

- 18.6. DISTRIBUTION CHANNEL

- 18.6.1. MARKET SIZE & FORECAST

- 18.7. KEY COUNTRIES

- 18.8. TURKEY: MARKET SIZE & FORECAST

- 18.9. SOUTH AFRICA: MARKET SIZE & FORECAST

- 18.10. SAUDI ARABIA: MARKET SIZE & FORECAST

19. COMPETITIVE LANDSCAPE

- 19.1. COMPETITION OVERVIEW

20. KEY COMPANY PROFILES

- 20.1. ABBOTT

- 20.1.1. BUSINESS OVERVIEW

- 20.1.2. PRODUCT OFFERINGS

- 20.1.3. KEY STRATEGIES

- 20.1.4. KEY STRENGTHS

- 20.1.5. KEY OPPORTUNITIES

- 20.2. DANONE

- 20.2.1. BUSINESS OVERVIEW

- 20.2.2. PRODUCT OFFERINGS

- 20.2.3. KEY STRATEGIES

- 20.2.4. KEY STRENGTHS

- 20.2.5. KEY OPPORTUNITIES

- 20.3. LACTALIS INTERNATIONAL

- 20.3.1. BUSINESS OVERVIEW

- 20.3.2. PRODUCT OFFERINGS

- 20.3.3. KEY STRATEGIES

- 20.3.4. KEY STRENGTHS

- 20.3.5. KEY OPPORTUNITIES

- 20.4. NESTLE

- 20.4.1. BUSINESS OVERVIEW

- 20.4.2. PRODUCT OFFERINGS

- 20.4.3. KEY STRATEGIES

- 20.4.4. KEY STRENGTHS

- 20.4.5. KEY OPPORTUNITIES

21. OTHER PROMINENT VENDORS

- 21.1. AROMA MILK PRODUCTS

- 21.1.1. BUSINESS OVERVIEW

- 21.1.2. PRODUCT OFFERINGS

- 21.2. ARLA FOODS AMBA

- 21.2.1. BUSINESS OVERVIEW

- 21.2.2. PRODUCT OFFERINGS

- 21.3. AGROPUR

- 21.3.1. BUSINESS OVERVIEW

- 21.3.2. PRODUCT OFFERINGS

- 21.4. BEST WAY INGREDIENTS

- 21.4.1. BUSINESS OVERVIEW

- 21.4.2. PRODUCT OFFERINGS

- 21.5. BEST HEALTH FOODS

- 21.5.1. BUSINESS OVERVIEW

- 21.5.2. PRODUCT OFFERINGS

- 21.6. BRIGHT LIFECARE

- 21.6.1. BUSINESS OVERVIEW

- 21.6.2. PRODUCT OFFERINGS

- 21.7. CAPSA

- 21.7.1. BUSINESS OVERVIEW

- 21.7.2. PRODUCT OFFERINGS

- 21.8. CREDITON DAIRY

- 21.8.1. BUSINESS OVERVIEW

- 21.8.2. PRODUCT OFFERINGS

- 21.9. CAYUGA MILK INGREDIENTS

- 21.9.1. BUSINESS OVERVIEW

- 21.9.2. PRODUCT OFFERINGS

- 21.10. CLOVER SONOMA

- 21.10.1. BUSINESS OVERVIEW

- 21.10.2. PRODUCT OFFERINGS

- 21.11. DAIRY FARMERS OF AMERICA

- 21.11.1. BUSINESS OVERVIEW

- 21.11.2. PRODUCT OFFERINGS

- 21.12. DARIGOLD

- 21.12.1. BUSINESS OVERVIEW

- 21.12.2. PRODUCT OFFERINGS

- 21.13. EHRMANN

- 21.13.1. BUSINESS OVERVIEW

- 21.13.2. PRODUCT OFFERINGS

- 21.14. FONTERRA

- 21.14.1. BUSINESS OVERVIEW

- 21.14.2. PRODUCT OFFERINGS

- 21.15. F&N DAIRIES

- 21.15.1. BUSINESS OVERVIEW

- 21.15.2. PRODUCT OFFERINGS

- 21.16. FAIRLIFE

- 21.16.1. BUSINESS OVERVIEW

- 21.16.2. PRODUCT OFFERINGS

- 21.17. FRIESLANDCAMPINA

- 21.17.1. BUSINESS OVERVIEW

- 21.17.2. PRODUCT OFFERINGS

- 21.18. GLANBIA

- 21.18.1. BUSINESS OVERVIEW

- 21.18.2. PRODUCT OFFERINGS

- 21.19. GCMMF

- 21.19.1. BUSINESS OVERVIEW

- 21.19.2. PRODUCT OFFERINGS

- 21.20. GAY LEA FOODS

- 21.20.1. BUSINESS OVERVIEW

- 21.20.2. PRODUCT OFFERINGS

- 21.21. HERITAGE FOODS

- 21.21.1. BUSINESS OVERVIEW

- 21.21.2. PRODUCT OFFERINGS

- 21.22. HP HOOD

- 21.22.1. BUSINESS OVERVIEW

- 21.22.2. PRODUCT OFFERINGS

- 21.23. INGREDIA

- 21.23.1. BUSINESS OVERVIEW

- 21.23.2. PRODUCT OFFERINGS

- 21.24. LAND O' LAKES

- 21.24.1. BUSINESS OVERVIEW

- 21.24.2. PRODUCT OFFERINGS

- 21.25. LYCOTEC

- 21.25.1. BUSINESS OVERVIEW

- 21.25.2. PRODUCT OFFERINGS

- 21.26. MCNELL NUTRITIONALS

- 21.26.1. BUSINESS OVERVIEW

- 21.26.2. PRODUCT OFFERINGS

- 21.27. MEGMILK SNOW BRAND

- 21.27.1. BUSINESS OVERVIEW

- 21.27.2. PRODUCT OFFERINGS

- 21.28. MILLIGANS FOOD GROUP

- 21.28.1. BUSINESS OVERVIEW

- 21.28.2. PRODUCT OFFERINGS

- 21.29. MOTHER DAIRY FRUIT & VEGETABLE

- 21.29.1. BUSINESS OVERVIEW

- 21.29.2. PRODUCT OFFERINGS

- 21.30. ORGANIC VALLEY

- 21.30.1. BUSINESS OVERVIEW

- 21.30.2. PRODUCT OFFERINGS

- 21.31. PROCAL DAIRIES

- 21.31.1. BUSINESS OVERVIEW

- 21.31.2. PRODUCT OFFERINGS

- 21.32. PARAG MILK FOODS

- 21.32.1. BUSINESS OVERVIEW

- 21.32.2. PRODUCT OFFERINGS

- 21.33. SADAFCO

- 21.33.1. BUSINESS OVERVIEW

- 21.33.2. PRODUCT OFFERINGS

- 21.34. SLEEPWELL

- 21.34.1. BUSINESS OVERVIEW

- 21.34.2. PRODUCT OFFERINGS

- 21.35. STOLLE MILK BIOLOGICS

- 21.35.1. BUSINESS OVERVIEW

- 21.35.2. PRODUCT OFFERINGS

- 21.36. SYNLAIT

- 21.36.1. BUSINESS OVERVIEW

- 21.36.2. PRODUCT OFFERINGS

- 21.37. TIRLAN

- 21.37.1. BUSINESS OVERVIEW

- 21.37.2. PRODUCT OFFERINGS

- 21.38. TESCO

- 21.38.1. BUSINESS OVERVIEW

- 21.38.2. PRODUCT OFFERINGS

- 21.39. VINDIJA D. D.

- 21.39.1. BUSINESS OVERVIEW

- 21.39.2. PRODUCT OFFERINGS

- 21.40. VALFOO

- 21.40.1. BUSINESS OVERVIEW

- 21.40.2. PRODUCT OFFERINGS

- 21.41. VINAMILK

- 21.41.1. BUSINESS OVERVIEW

- 21.41.2. PRODUCT OFFERINGS

22. REPORT SUMMARY

- 22.1. KEY TAKEAWAYS

- 22.2. STRATEGIC RECOMMENDATIONS

23. QUANTITATIVE SUMMARY

- 23.1. MARKET BY GEOGRAPHY

- 23.2. MARKET BY FORM

- 23.3. MARKET BY APPLICATION

- 23.4. MARKET BY AGE

- 23.5. MARKET BY DISTRIBUTION CHANNEL

- 23.6. APAC

- 23.6.1. FORM: MARKET SIZE & FORECAST

- 23.6.2. APPLICATIONS: MARKET SIZE & FORECAST

- 23.6.3. AGE: MARKET SIZE & FORECAST

- 23.6.4. DISTRIBUTION CHANNEL: MARKET SIZE & FORECAST

- 23.7. NORTH AMERICA

- 23.7.1. FORM: MARKET SIZE & FORECAST

- 23.7.2. APPLICATION: MARKET SIZE & FORECAST

- 23.7.3. AGE: MARKET SIZE & FORECAST

- 23.7.4. DISTRIBUTION CHANNEL: MARKET SIZE & FORECAST

- 23.8. EUROPE

- 23.8.1. FORM: MARKET SIZE & FORECAST

- 23.8.2. APPLICATION: MARKET SIZE & FORECAST

- 23.8.3. AGE: MARKET SIZE & FORECAST

- 23.8.4. DISTRIBUTION CHANNEL: MARKET SIZE & FORECAST

- 23.9. LATIN AMERICA

- 23.9.1. FORM: MARKET SIZE & FORECAST

- 23.9.2. APPLICATION: MARKET SIZE & FORECAST

- 23.9.3. AGE: MARKET SIZE & FORECAST

- 23.9.4. DISTRIBUTION CHANNEL: MARKET SIZE & FORECAST

- 23.10. MIDDLE EAST AND AFRICA

- 23.10.1. FORM: MARKET SIZE & FORECAST

- 23.10.2. APPLICATION: MARKET SIZE & FORECAST

- 23.10.3. AGE: MARKET SIZE & FORECAST

- 23.10.4. DISTRIBUTION CHANNEL: MARKET SIZE & FORECAST

24. APPENDIX

- 24.1. RESEARCH METHODOLOGY

- 24.2. RESEARCH PROCESS

- 24.3. REPORT ASSUMPTIONS & CAVEATS

- 24.3.1. KEY CAVEATS

- 24.3.2. CURRENCY CONVERSION

- 24.4. ABBREVIATIONS