|

|

市場調査レポート

商品コード

1489538

IoTサイバーセキュリティの業界分析 (2024~2030年)IoT Cybersecurity Industry Analysis 2024-2030 |

||||||

|

|||||||

| IoTサイバーセキュリティの業界分析 (2024~2030年) |

|

出版日: 2024年06月01日

発行: Westlands Advisory Ltd

ページ情報: 英文

納期: 即日から翌営業日

|

全表示

- 概要

- 目次

概要

一部の業界では他の業界よりも進んでいるにもかかわらず、IoTサイバーセキュリティの成熟度は、相対的に低いままです。IoTサイバーセキュリティの成熟度は、IoT導入の急速な成長に遅れをとっており、セキュリティ対策の必要性が高まっていることを浮き彫りにしています。IoT導入の複雑さ・規模・範囲が拡大し、デバイスの数が増加するにつれて、攻撃対象が拡大するため、セキュリティはますます重要になります。2023年のIoTセキュリティ支出は73億米ドルで、世界のサイバーセキュリティ支出の3.7%以上に達すると推定されています。2030年までには、IoTは支出の5%を占めるようになると思われます。

投資の原動力となっているのは、規制、脆弱なデバイスセキュリティ、デバイスの急増、IoTデバイスへの警戒感の増大です。特に、重要な国家インフラ (ユーティリティ、運輸、金融セクター) や生命に関わる領域 (航空宇宙、自動車医療) への投資が活発です。重要インフラのサイバーセキュリティに対する関心の高まりと、これらの分野でのIoTデバイスの急速な導入は、規制の厳しい業界において大きな成長を促すと思われます。したがって、これらは最大の市場セグメントであり、投資は2030年まで急速に増加し続けると思われます。

5G技術の展開は、より高速で信頼性の高い接続性を提供することにより、より広範な「大規模」かつ「重要な」IoT展開を促進し、IoTの急速な成長を促しています。データの本質的な価値がますます認識されるようになり、意思決定や業務効率の改善のためにリアルタイムの知見を活用しようとする組織のIoT導入がさらに進んでいます。組織が意思決定と業務効率の改善のためにリアルタイムの洞察を活用しようとしているため、データの本質的価値がますます認識されるようになり、IoTの導入がさらに促進されています。IoTの導入が進むにつれて、接続されるデバイスの数は増加すると予想され、この拡大を効果的に処理するために包括的なデバイス資産管理が必要となります。そのため、セキュア・バイ・デザインや組み込みデバイス保護への注目が高まっており、特にIoT製品のセキュリティ強化を目的とした法的イニシアティブや国家認証制度によって加速しています。

2030年までに、IoTサイバーセキュリティの成熟度は自動車産業と航空宇宙産業で著しく向上し、運輸とユーティリティがそれに続く、と予想されています。IoTデバイスが業務やインフラにますます不可欠になるにつれて、多くの組織がIoTセキュリティをサイバーセキュリティ戦略全体に組み込むようになると思われます。また、規制によってセキュア・バイ・デザインの実践への投資が促進されるため、ネイティブ・デバイスのセキュリティもはるかに強化されると考えられています。IoTの導入規模や範囲、サイバーセキュリティの成熟度は、業界や地域によって大きく異なるもの、IoTセキュリティに対する認識と導入が高まる傾向は、今後も続くと予想されます。

定義

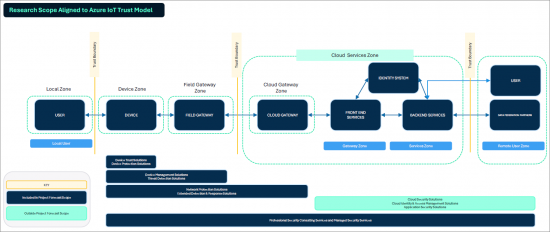

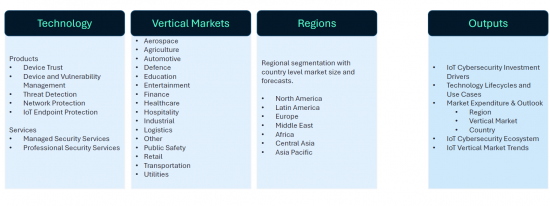

このプロジェクトでは、デバイス、エッジ、ネットワークの各レベルで信頼とセキュリティを確立するために使用されるサイバーセキュリティ技術とソリューションを対象として取り上げます。これには、仮想プライベートクラウド、クラウドに存在するIoTデータ、IoTアプリケーションのセキュリティは含まれないです。Azure IoT Trust Modelを使用して、デバイス、ゲートウェイ、ネットワーク、およびフィールドゲートウェイとクラウドゲートウェイ間のトランジットにおけるデータの保護に重点を置いています。プロフェッショナルおよびマネージド・セキュリティ・サービスのセグメントには、クラウド・サービスを含むIoTデバイスやネットワークのアドバイス、実装、監視に関するサービスが含まれます。

市場区分

調査概要

目次

- 1. 定義とセグメンテーション

エグゼクティブサマリー

- 1. エグゼクティブサマリー

- 2. 全体的な市場規模:産業セグメント別

- 3. 市場予測:業界セグメント別

- 4. 市場シェアと成長率:産業セグメント別

- 5. 市場規模:国別

- 6. 市場規模:地域別・産業別

- 7. 市場支出・成長率:技術・サービス別

サイバーセキュリティ投資の促進要因

- 1. 投資促進要因:概要

- 2. 経済の概要

- 3. 技術の概要

- 4. 規制の概要

- 5. 主要な規制動向の概要

- 6. 規制が産業に与える影響

- 7. リスクの概要

- 8. IoTの脅威・脆弱性の概要

- 9. 脅威の動向

- 10. 脆弱性の動向

- 11. リスクの動向

IoTのアーキテクチャ

- 1. 高レベルIoTプラットフォーム・アーキテクチャ

- 2. 高レベルIoTプラットフォーム・アーキテクチャとプロジェクトの範囲

- 3. IoTのシナリオ

- 4. AWSのアーキテクチャ

- 5. Azureのアーキテクチャ

- 6. Rockwell Automation・PTC・Azureのアーキテクチャ

- 7. IoTの接続要件

- 8. IoTの接続技術

- 9. 脅威・セキュリティ対策に対応したIoTスタック

技術のライフサイクルと利用事例

- 1. IoTデバイスの信頼の定義

- 2. IoTデバイスの信頼の動向

- 3. デバイス信頼ソリューション

- 4. IoTデバイス・セキュリティ管理の定義

- 5. IoTデバイス・セキュリティ管理の動向

- 6. IoTデバイス・セキュリティ管理ソリューション

- 7. IoT脅威検出の定義

- 8. IoT脅威検出の動向

- 9. IoT脅威検出ソリューション

- 10. ネットワーク保護の定義

- 11. ネットワーク保護の動向

- 12. ネットワーク保護ソリューション

- 13. IoTエンドポイント保護の定義

- 14. IoTエンドポイント保護の動向

- 15. IoTエンドポイント保護ソリューション

- 16. プロフェッショナルセキュリティサービスの定義

- 17. プロフェッショナルセキュリティサービスの動向

- 18. マネージドセキュリティサービスの定義

- 19. マネージドセキュリティサービスの動向

- 20. IoTセキュリティ技術・サービスの予測 (2023~2030年)

市場支出と見通し

- 1. 要約

- 2. 市場予測:産業区分別 (2023~2030年)

- 3. 支出額・成長率:産業区分別

- 4. 北米市場の予測:産業区分別 (2023~2030年)

- 5. 北米の支出額とCAGR:産業区分別 (2023年)

- 6. 北米市場の予測:国別 (2023~2030年)

- 7. アジア太平洋市場の予測:産業区分別 (2023~2030年)

- 8. アジア太平洋の支出額とCAGR:産業区分別 (2023年)

- 9. アジア太平洋市場の予測:国別 (2023~2030年)

- 10. 欧州市場の予測:産業区分別 (2023~2030年)

- 11. 欧州の支出額とCAGR:産業区分別 (2023年)

- 12. 欧州市場の予測:国別 (2023~2030年)

- 13. アフリカ市場の予測:産業区分別 (2023~2030年)

- 14. アフリカの支出額とCAGR:産業区分別 (2023年)

- 15. アフリカ市場の予測:国別 (2023~2030年)

- 16. 中東市場の予測:産業区分別 (2023~2030年)

- 17. 中東の支出額とCAGR:産業区分別 (2023年)

- 18. 中東市場の予測:国別 (2023~2030年)

- 19. ラテンアメリカ市場の予測:産業区分別 (2023~2030年)

- 20. ラテンアメリカの支出額とCAGR:産業区分別 (2023年)

- 21. ラテンアメリカ市場の予測:国別 (2023~2030年)

- 22. 中央アジア市場の予測:産業区分別 (2023~2030年)

- 23. 中央アジアの支出額とCAGR:産業区分別 (2023年)

- 24. 中央アジア市場の予測:国別 (2023~2030年)

IoTサイバーセキュリティのエコシステム

- 1. 要約

- 2. エコシステム

- 3. ベンダー別製品マップ

- 4. IoTプラットフォームとセキュリティサービス

産業別の市場予測

- 1. 航空宇宙の動向

- 2. 航空宇宙市場の支出額 (2023~2030年) と地域別動向

- 3. 農業の動向

- 4. 農業市場の支出額 (2023~2030年) と地域別動向

- 5. 自動車の動向

- 6. 自動車市場の支出額 (2023~2030年) と地域別動向

- 7. 教育の動向

- 8. 教育市場の支出額 (2023~2030年) と地域別動向

- 9. 医療の動向

- 10. 医療市場の支出額 (2023~2030年) と地域別動向

- 11. ホスピタリティ・エンタテインメントの動向

- 12. ホスピタリティ・エンタテインメント市場の支出額 (2023~2030年) と地域別動向

- 13. 工業の動向

- 14. 工業市場の支出額 (2023~2030年) と地域別動向

- 15. 物流の動向

- 16. 物流市場の支出額 (2023~2030年) と地域別動向

- 17. 運輸の動向

- 18. 運輸市場の支出額 (2023~2030年) と地域別動向

- 19. ユーティリティの動向

- 20. ユーティリティ市場の支出額 (2023~2030年) と地域別動向

- 21. 小売の動向

- 22. 小売市場の支出額 (2023~2030年) と地域別動向

- 23. 防衛の動向

- 24. 防衛市場の支出額 (2023~2030年) と地域別動向

- 25. 金融の動向

- 26. 金融市場の支出額 (2023~2030年) と地域別動向

- 27. 公共安全の動向

- 28. 公共安全市場の支出額 (2023~2030年) と地域別動向

付録:調査手法

Overview

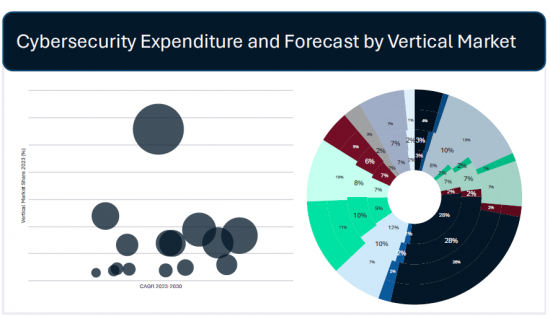

Across all industries, IoT cybersecurity maturity remains relatively low despite some industries being further along than others. The maturity of IoT cybersecurity lags behind the rapid growth in IoT deployments, highlighting the escalating necessity for security measures. As the complexity, scale and scope of IoT deployments evolve, and the growing number of devices expands attack surfaces, security will become increasingly critical. Westlands advisory estimates that expenditure on IoT security in 2023 was $7.3B or 3.7% of the global spend on cybersecurity. By 2030 IoT will make up 5% of expenditure.

Investment is being driven by regulation, weak native device security, device proliferation and growing adversarial interest in IoT devices. Investment is particularly strong in critical national infrastructure (utilities, transportation, and financial sectors) and life critical applications (aerospace, automotive, and healthcare) . A growing focus on critical infrastructure cybersecurity and the rapid adoption of IoT devices in these fields will drive significant growth in highly regulated industries. Accordingly, these are the largest market segments and investment will continue to increase rapidly to 2030.

The rollout of 5G technology is catalysing rapid IoT growth by providing fast, more reliable connectivity thereby facilitating more widespread 'Massive' and 'Critical' IoT deployments. The increasing recognition of data's intrinsic value is further driving IoT adoption as organisations seek to leverage real time insights for improved decision making and operational efficiency. As IoT adoption increases, the number of connected devices is expected to grow, necessitating comprehensive Device Asset Management to effectively handle this expansion. Poor native device security has made these devices particularly weak links in the security of digital deployments. As such there is a growing focus on secure by design and embedded device protection, particularly accelerated by legislative initiatives and national certification schemes aimed at enhancing IoT product security.

By 2030 WA expects IoT cybersecurity maturity to have advanced significantly within the automotive and aerospace industries with transportation and utilities following closely behind. Many organisations will integrate IoT security into their overall cybersecurity strategy as these devices become increasingly integral to their operations and infrastructure. WA also expects far greater native device security as regulation drives investment in secure-by-design practices. Although the scale and scope of IoT adoption and cyber security maturity will vary greatly across industries and geographies, the trend towards greater IoT security awareness and implementation is expected to continue its upward trajectory.

Definition

The project focuses on cybersecurity technologies and solutions used to establish trust and security at the device, edge and network level. This does not include security of Virtual Private Clouds, the IoT data residing in the cloud, or IoT applications. Using the Azure IoT Trust Model, the focus of the work includes protection of devices, gateways, networks, and data in transit between the field gateway and the cloud gateway. The professional and managed security services segment includes services related to advising, implementing and monitoring IoT devices and networks which may include the cloud services.

Segmentation

Deliverables

Table of Contents

- 1. Definitions & Segmentation

Executive Summary

- 1. Executive Summary

- 2. Total Available Market by Industry Segment

- 3. Market Forecast by Industry Segment

- 4. Market Share and Growth Rates by Industry Segment

- 5. Market Size by Country

- 6. Market Size by Region and Industry Segment

- 7. Market Expenditure and Growth Rate by Technology and Service

Cybersecurity Investment Drivers

- 1. Summary of Investment Drivers

- 2. Economics Summary

- 3. Technology Summary

- 4. Regulatory Summary

- 5. Summary of Major Regulatory Developments

- 6. Regulatory Impact on Industries

- 7. Risk Summary

- 8. Summary of IoT Threats and Vulnerabilities

- 9. Threat Trends

- 10. Vulnerability Trends

- 11. Risk Trends

IoT Architectures

- 1. High Level IoT Platform Architecture

- 2. High Level IoT Platform Architecture and Project Scope

- 3. IoT Scenarios

- 4. AWS Architecture

- 5. Azure Architecture

- 6. Rockwell Automation, PTC & Azure Architecture

- 7. IoT Connectivity Requirements

- 8. IoT Connectivity Technologies

- 9. IoT Stack Mapped to Threats and Security Measures

Technology Lifecycle & Use Cases

- 1. IoT Device Trust Definition

- 2. IoT Device Trust Trends

- 3. Device Trust Solutions

- 4. IoT Device Security Management Definition

- 5. IoT Device Security Management Trends

- 6. IoT Device Security Management Solutions

- 7. IoT Threat Detection Definition

- 8. IoT Threat Detection Trends

- 9. IoT Threat Detection Solutions

- 10. Network Protection Definition

- 11. Network Protection Trends

- 12. Network Protection Solutions

- 13. IoT Endpoint Protection Definition

- 14. IoT Endpoint Protection Trends

- 15. IoT Endpoint Protection Solutions

- 16. Professional Security Services Definition

- 17. Professional Security Services Trends

- 18. Managed Security Services Definition

- 19. Managed Security Services Trends

- 20. IoT Security Technology and Services Forecast 2023-2030

Market Expenditure & Outlook

- 1. Summary

- 2. Market Forecast by Industry Segment 2023-2030

- 3. Industry Segment by Expenditure & Growth Rate

- 4. North America Market Forecast by Industry Segment 2023-2030

- 5. North America Expenditure 2030 and CAGR by Industry Segment

- 6. North America Market Forecast by Country 2023-2030

- 7. Asia-Pacific Market Forecast by Industry Segment 2023-2030

- 8. Asia-Pacific Expenditure 2030 and CAGR by Industry Segment

- 9. Asia-Pacific Market Forecast by Country 2023-2030

- 10. Europe Market Forecast by Industry Segment 2023-2030

- 11. Europe Expenditure 2030 and CAGR by Industry Segment

- 12. Europe Market Forecast by Country 2023-2030

- 13. Africa Market Forecast by Industry Segment 2023-2030

- 14. Africa Expenditure 2030 and CAGR by Industry Segment

- 15. Africa Market Forecast by Country 2023-2030

- 16. Middle East Market Forecast by Industry Segment 2023-2030

- 17. Middle East Expenditure 2030 and CAGR by Industry Segment

- 18. Middle East Market Forecast by Country 2023-2030

- 19. Latin America Market Forecast by Industry Segment 2023-2030

- 20. Latin America Expenditure 2030 and CAGR by Industry Segment

- 21. Latin America Market Forecast by Country 2023-2030

- 22. Central Asia Market Forecast by Industry Segment 2023-2030

- 23. Central Asia Expenditure 2030 and CAGR by Industry Segment

- 24. Central Asia Market Forecast by Country 2023-2030

IoT Cybersecurity Ecosystem

- 1. Summary

- 2. Ecosystem

- 3. Product Map by Vendor

- 4. IoT Platforms and Security Services

Vertical Market Forecast

- 1. Aerospace Trends

- 2. Aerospace Market Expenditure 2023-2030 and by Region

- 3. Agriculture Trends

- 4. Agriculture Market Expenditure 2023-2030 and by Region

- 5. Automotive Trends

- 6. Automotive Market Expenditure 2023-2030 and by Region

- 7. Education Trends

- 8. Education Market Expenditure 2023-2030 and by Region

- 9. Healthcare Trends

- 10. Healthcare Market Expenditure 2023-2030 and by Region

- 11. Hospitality and Entertainment Trends

- 12. Hospitality and Entertainment Market Expenditure 2023-2030 and by Region

- 13. Industrial Trends

- 14. Industrial Market Expenditure 2023-2030 and by Region

- 15. Logistics Trends

- 16. Logistics Market Expenditure 2023-2030 and by Region

- 17. Transportation Trends

- 18. Transportation Market Expenditure 2023-2030 and by Region

- 19. Utilities Trends

- 20. Utilities Market Expenditure 2023-2030 and by Region

- 21. Retail Trends

- 22. Retail Market Expenditure 2023-2030 and by Region

- 23. Defence Trends

- 24. Defence Market Expenditure 2023-2030 and by Region

- 25. Finance Trends

- 26. Finance Market Expenditure 2023-2030 and by Region

- 27. Public Safety Trends

- 28. Public Safety Market Expenditure 2023-2030 and by Region