|

|

市場調査レポート

商品コード

1461363

ペロブスカイト太陽電池市場:現状分析と予測(2023-2030年)Perovskite Solar Cells Market: Current Analysis and Forecast (2023-2030) |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ペロブスカイト太陽電池市場:現状分析と予測(2023-2030年) |

|

出版日: 2024年03月01日

発行: UnivDatos Market Insights Pvt Ltd

ページ情報: 英文 138 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 目次

ペロブスカイト太陽電池市場は、気候変動とエネルギー安全保障に対する懸念の高まりにより、太陽光発電のような再生可能エネルギー源に対する需要が急速に増加しているため、予測期間中に48.56 %の強力なCAGRで成長する見込みです。ペロブスカイト太陽電池は、従来のシリコン太陽電池に代わる有望な代替品であり、高効率と低コストが期待できます。さらに、ペロブスカイト太陽電池の製造コストは、技術が成熟し、規模の経済が達成されるにつれて、今後数年間で大幅に低下すると予想されます。これにより、ペロブスカイト太陽電池は従来のシリコン太陽電池との競争力を高めることになります。

構造に基づき、市場はプレーナー型ペロブスカイト太陽電池とメソポーラス型ペロブスカイト太陽電池に区分されます。このうち、ペロブスカイト太陽電池市場で圧倒的なシェアを占めているのはプレーナー型です。プレーナー型太陽電池は、メソポーラス型太陽電池に比べて必要な層数が少なく、プロセスも単純であるため、製造コスト効率が高いです。さらに、最近のブレークスルーにより、プレーナー型太陽電池の電力変換効率は大幅に改善され、他の太陽電池技術との競争力が高まっています。

製品によって、市場は硬質なペロブスカイト太陽電池と柔軟なペロブスカイト太陽電池に区分されます。なかでも柔軟なペロブスカイト太陽電池は軽量で曲げられるため、ペロブスカイト太陽電池市場で大きく成長しています。これらの特性により、従来の硬質太陽電池パネルが理想的でないさまざまな用途に適しています。さらに、建物のファサードや屋根にシームレスに組み込むことができ、衣服やその他のウェアラブル機器にも快適に組み込むことができます。

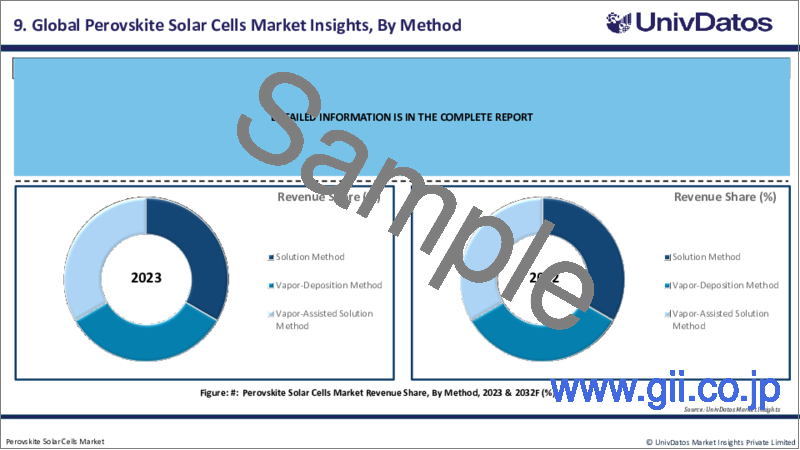

製法別に見ると、市場は溶液製法、蒸着製法、蒸気アシスト溶液製法に区分されます。このうち、蒸着法セグメントはペロブスカイト太陽電池市場で大きなシェアを占めています。蒸着ペロブスカイト膜は、スピンコーティングやインクジェット印刷などの他の溶液法で製造されたものよりも効率率が高いことが示されているからです。これは、蒸着プロセスによって製造されるペロブスカイト材料の結晶性と形態が改善されるためです。さらに、蒸着法は、他の溶液法で製造されたものよりも過酷な環境条件に耐えることができる、より安定したペロブスカイト膜をもたらします。

用途別に見ると、市場はスマートガラス、ソーラーパネル、ペロブスカイト型タンデム太陽電池、携帯機器、公益事業、BIPV(建物一体型太陽光発電)に区分されます。中でもソーラーパネル分野は、ペロブスカイト太陽電池市場において大きな成長を遂げています。これは、ソーラーパネルがペロブスカイト太陽電池にとって最も成熟したアプリケーションであり、商業化に向けて研究開発が進められているためです。さらに、高効率化の可能性もある:ペロブスカイト太陽電池は、従来のシリコン太陽電池に比べて高い効率を達成する可能性があり、単位面積当たりの発電量の増加につながります。

市場は最終用途に基づき、製造、エネルギー、産業オートメーション、航空宇宙、家電に区分されます。なかでもエネルギー分野は、ペロブスカイト太陽電池が従来のシリコン系太陽電池に比べて製造コストの低減、高効率化、柔軟な設計オプションなど、いくつかの利点を備えていることから、ペロブスカイト太陽電池市場の成長が著しいです。さらに、ペロブスカイト太陽電池は、製造コストが低く、必要な材料が少ないため、従来のシリコン系太陽電池よりもカーボンフットプリントが大幅に低いです。

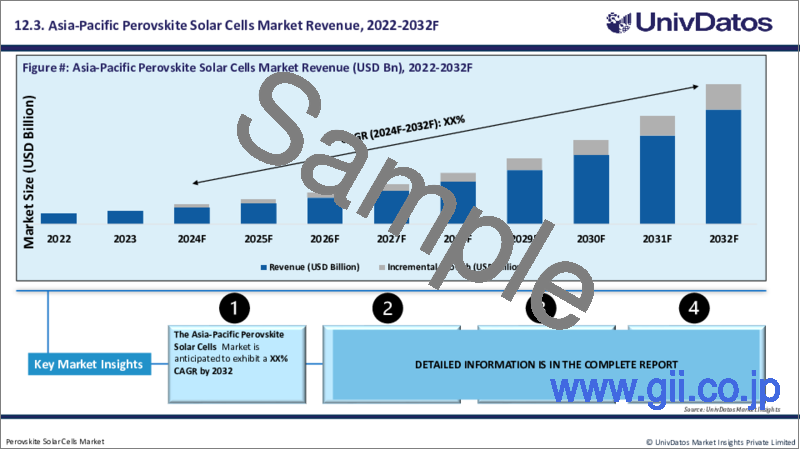

市場導入の理解を深めるため、市場は北米(米国、カナダ、その他北米地域)、欧州(ドイツ、英国、オランダ、フランス、イタリア、スペイン、その他欧州地域)、アジア太平洋地域(中国、日本、インド、その他アジア太平洋地域)、その他世界の国々における世界の存在に基づいて分析されています。アジア太平洋地域がペロブスカイト太陽電池市場で優位を占めているのは、同地域の急速な都市化と経済成長がエネルギー需要の増加につながるためです。さらに、気候変動やエネルギー安全保障への懸念が、太陽光発電のような再生可能エネルギー源への強い推進力となっています。中国、日本、韓国のような国々は、再生可能エネルギー技術の開発と展開を奨励する支援的な政策と政策を実施しています。これらの政策には、ペロブスカイト太陽電池の研究開発および商業化のための財政的インセンティブや補助金が含まれていることが多いです。さらに、この地域は、ソーラーパネルを含むさまざまな電子機器の製造インフラが確立されています。この既存のインフラは、ペロブスカイト太陽電池の技術が商業的に成熟すれば、容易に生産に適応させることができます。最後に、パイロット製造施設を持つマイクロクアンタ・セミコンダクター(中国)のような主要市場企業の存在が、アジア太平洋の優位性をさらに強めています。

同市場で事業を展開する主要企業には、Dyenamo AB、Energy Materials Corp、Fraunhofer ISE、Panasonic Holdings Corporation、Frontier Energy Solution、FrontMaterials Co.Ltd.、富士フイルム和光純薬株式会社、株式会社東芝、G24 Power Ltd.、Tandem PV, Inc.などです。

目次

第1章 市場イントロダクション

- 市場の定義

- 主な目標

- ステークホルダー

- 制限事項

第2章 調査手法または前提条件

- 調査プロセス

- 調査手法

- 回答者プロファイル

第3章 市場要約

第4章 エグゼクティブサマリー

第5章 世界のペロブスカイト太陽電池市場COVID-19の影響

第6章 世界のペロブスカイト太陽電池市場収益、2020-2030年

第7章 構造別の市場分析

- 平面ペロブスカイト太陽電池

- メソポーラスペロブスカイト太陽電池

第8章 製品別市場分析

- 硬質なペロブスカイト太陽電池

- 柔軟なペロブスカイト太陽電池

第9章 方法別の市場分析

- 溶液製法

- 蒸着法

- 蒸気アシスト溶液製法

第10章 用途別の市場分析

- スマートグラス

- ソーラーパネル

- タンデム太陽電池のペロブスカイト

- 携帯機器

- 公益事業

- BIPV(建物一体型太陽光発電)

第11章 最終用途別の市場分析

- 製造業

- エネルギー

- 産業自動化

- 航空宇宙

- 家電

第12章 地域別市場分析

- 北米

- 米国

- カナダ

- その他北米地域

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋

- 中国

- 日本

- インド

- アジア太平洋のその他諸国

- 世界のその他の地域

第13章 ペロブスカイト太陽電池市場力学

- 市場促進要因

- 市場の課題

- 影響分析

第14章 ペロブスカイト太陽電池市場機会

第15章 ペロブスカイト太陽電池市場動向

第16章 需要と供給の分析

- 需要側分析

- 供給側分析

第17章 バリューチェーン分析

第18章 価格分析

第19章 競争シナリオ

- ポーターのファイブフォース分析

- 競合情勢

第20章 会社概要

- Dyenamo AB

- Energy Materials Corp

- Fraunhofer ISE

- Panasonic Holdings Corporation

- Frontier Energy Solution,

- FrontMaterials Co. Ltd.,

- FUJIFILM Wako Pure Chemical Corporation

- Toshiba Corporation

- G24 Power Ltd

- Tandem PV, Inc.

第21免責事項

Perovskite solar cells are a type of photovoltaic material that has shown great potential as an alternative to traditional silicon-based solar cells. These solar cells are named after the mineral perovskite, which is a calcium titanium oxide. They are relatively lightweight, flexible, and cheap to produce, making them ideal for use in a variety of applications, such as rooftops or buildings. Nowadays, Consumers are increasingly using their smartphones and tablets to access various applications and content on the go. This trend has created a significant opportunity for the automotive industry to integrate these devices into vehicles to provide seamless connectivity and entertainment options.

The Perovskite Solar Cells Market is expected to grow at a strong CAGR of 48.56 % during the forecast period owing to increasing concerns about climate change and energy security, the demand for renewable energy sources like solar power is increasing rapidly. Perovskite solar cells offer a promising alternative to traditional silicon solar cells, with the potential for higher efficiency and lower costs. Additionally, the cost of manufacturing perovskite solar cells is expected to decline significantly in the coming years, as the technology matures and economies of scale are achieved. This will make perovskite solar cells more competitive with traditional silicon solar cells.

Based on structure, the market is segmented into planar perovskite solar cells and mesoporous perovskite solar cells. Amongst these, the segment with the dominating share in the perovskite solar cell market is planar perovskite solar cells because of simpler device design and fabrication techniques. Planar cells require fewer layers and simpler processes compared to mesoporous cells, making them more cost-effective to manufacture. Additionally, recent breakthroughs have significantly improved the power conversion efficiency of planar cells, making them more competitive with other solar cell technologies.

Based on product, the market is segmented into rigid perovskite solar cells and flexible perovskite solar cells. Amongst these, the flexible perovskite solar cells segment has significant growth in the perovskite solar cell market because they are lightweight and bendable. These properties make them suitable for various applications where traditional rigid solar panels are not ideal. Additionally, they can be seamlessly integrated into building facades or roofs and can be comfortably incorporated into clothing or other wearable devices.

Based on method, the market is segmented into solution method, vapor-deposition method, and vapor-assisted solution method. Amongst these, the vapor-deposition method segment has significant share in the perovskite solar cell market because vapor-deposited perovskite films have been shown to have higher efficiency rates than those produced by other solution methods such as spin coating or inkjet printing. This is due to the improved crystallinity and morphology of the perovskite material produced by the vapor-deposition process. Additionally, the vapor-deposition method also results in more stable perovskite films that can withstand harsh environmental conditions better than those made using other solution methods.

Based on application, the market is segmented into smart glass, solar panel, perovskite in tandem solar cells, portable devices, utilities, and BIPV (building-integrated photovoltaics). Amongst these, the solar panel segment has significant growth in the perovskite solar cell market because solar panels are the most mature application for perovskite solar cells, with ongoing research and development efforts towards commercialization. Additionally, potential for higher efficiency: Perovskite solar cells have the potential to achieve higher efficiencies compared to traditional silicon solar cells, leading to increased power generation per unit area.

Based on end use, the market is segmented into manufacturing, energy, industrial automation, aerospace, and consumer electronics. Amongst these, the energy segment has a significant growth in the perovskite solar cell market because it offers several advantages over traditional silicon-based solar cells, including lower manufacturing costs, higher efficiency rates, and flexible design options. Additionally, Perovskite solar cells have a significantly lower carbon footprint than traditional silicon-based solar cells due to their lower manufacturing costs and reduced material requirements.

For a better understanding of the market adoption, the market is analyzed based on its worldwide presence in countries such as North America (U.S., Canada, and the Rest of North America), Europe (Germany, UK, Netherlands, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India and Rest of Asia-Pacific), Rest of World. Asia-Pacific region's dominance in the perovskite solar cell market due to rapid urbanization and growing economies in the region lead to increasing energy demand. Additionally, concerns about climate change and energy security drive a strong push towards renewable energy sources like solar power. Countries like China, Japan, and South Korea have implemented supportive policies and regulations encouraging the development and deployment of renewable energy technologies. These policies often include financial incentives and subsidies for research, development, and commercialization of perovskite solar cells. Furthermore, the region boasts a well-established manufacturing infrastructure for various electronics, including solar panels. This existing infrastructure can be readily adapted to produce perovskite solar cells once the technology matures commercially. Finally, The presence of major market players in the region, like Microquanta Semiconductor (China) with its pilot manufacturing facility, further strengthens the Asia-Pacific dominance.

Some major players operating in the market include Dyenamo AB, Energy Materials Corp, Fraunhofer ISE, Panasonic Holdings Corporation, Frontier Energy Solution, FrontMaterials Co. Ltd., FUJIFILM Wako Pure Chemical Corporation, Toshiba Corporation, G24 Power Ltd, and Tandem PV, Inc.

TABLE OF CONTENTS

1.MARKET INTRODUCTION

- 1.1.Market Definitions

- 1.2.Main Objective

- 1.3.Stakeholders

- 1.4.Limitation

2.RESEARCH METHODOLOGY OR ASSUMPTION

- 2.1.Research Process of the Perovskite Solar Cells Market

- 2.2.Research Methodology of the Perovskite Solar Cells Market

- 2.3.Respondent Profile

3.MARKET SYNOPSIS

4.EXECUTIVE SUMMARY

5.GLOBAL PEROVSKITE SOLAR CELLS MARKET COVID-19 IMPACT

6.GLOBAL PEROVSKITE SOLAR CELLS MARKET REVENUE, 2020-2030F

7.MARKET INSIGHTS BY STRUCTURE

- 7.1.Planar Perovskite Solar Cells

- 7.2.Mesoporous Perovskite Solar Cells

8.MARKET INSIGHTS BY PRODUCT

- 8.1.Rigid Perovskite Solar Cells

- 8.2.Flexible Perovskite Solar Cells

9.MARKET INSIGHTS BY METHOD

- 9.1.Solution Method

- 9.2.Vapor-Deposition Method

- 9.3.Vapor-Assisted Solution Method

10.MARKET INSIGHTS BY APPLICATION

- 10.1.Smart Glass

- 10.2.Solar Panel

- 10.3.Perovskite in Tandem Solar Cells

- 10.4.Portable Devices

- 10.5.Utilities

- 10.6.BIPV (Building-Integrated Photovoltaics)

11.MARKET INSIGHTS BY END USE

- 11.1.Manufacturing

- 11.2.Energy

- 11.3.Industrial Automation

- 11.4.Aerospace

- 11.5.Consumer Electronics

12.MARKET INSIGHTS BY REGION

- 12.1.North America

- 12.1.1.U.S.

- 12.1.2.Canada

- 12.1.3.Rest of North America

- 12.2.Europe

- 12.2.1.Germany

- 12.2.2.France

- 12.2.3.UK

- 12.2.4.Italy

- 12.2.5.Spain

- 12.2.6.Rest of Europe

- 12.3.Asia-Pacific

- 12.3.1.China

- 12.3.2.Japan

- 12.3.3.India

- 12.3.4.Rest of APAC

- 12.4.Rest of the World

13.PEROVSKITE SOLAR CELLS MARKET DYNAMICS

- 13.1.Market Drivers

- 13.2.Market Challenges

- 13.3.Impact Analysis

14.PEROVSKITE SOLAR CELLS MARKET OPPORTUNITIES

15.PEROVSKITE SOLAR CELLS MARKET TRENDS

16.DEMAND AND SUPPLY-SIDE ANALYSIS

- 16.1.Demand Side Analysis

- 16.2.Supply Side Analysis

17.VALUE CHAIN ANALYSIS

18.PRICING ANALYSIS

19.COMPETITIVE SCENARIO

- 19.1.Porter's Five Forces Analysis

- 19.2.Competitive Landscape

20.COMPANY PROFILED

- 20.1.Dyenamo AB

- 20.2.Energy Materials Corp

- 20.3.Fraunhofer ISE

- 20.4.Panasonic Holdings Corporation

- 20.5.Frontier Energy Solution,

- 20.6.FrontMaterials Co. Ltd.,

- 20.7.FUJIFILM Wako Pure Chemical Corporation

- 20.8.Toshiba Corporation

- 20.9.G24 Power Ltd

- 20.10.Tandem PV, Inc.