ペロブスカイトの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Perovskite Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750311

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

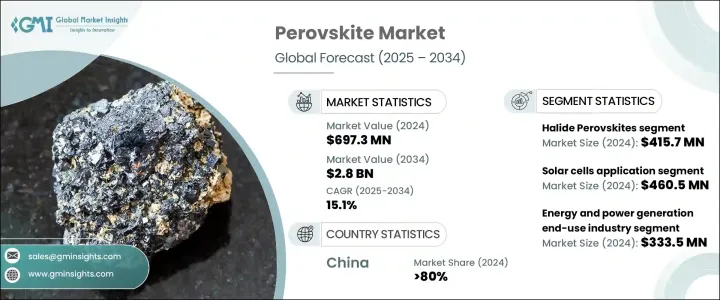

世界のペロブスカイト市場は、2024年に6億9,730万米ドルと評価され、2034年にはCAGR 15.1%で成長して28億米ドルに達すると推定されています。

エネルギーインフラが再生可能な統合をサポートするよう適応する中、ペロブスカイトはその汎用性、軽量特性、先進的エネルギーシステムとの互換性により支持を集めています。これらの材料は、軟質で効率的な薄膜構成における強力な性能により、太陽光発電、センサ、民生用電子機器製品における新たな可能性を引き出しています。

特に米国では、政府が支持する持続可能性の目標が、フォトニクスや半導体の技術革新への投資と一致しています。シリコンとペロブスカイトを組み合わせたタンデム型太陽電池への関心が高まっており、従来型太陽光発電の効率レベルを上回る可能性があります。また、その適応性は、携帯型や装着型のソーラーデバイスへの応用をサポートし、住宅と商業市場の需要に対応します。薄膜エレクトロニクスの急速な技術革新は、独創的なデバイス設計を可能にし、将来を見据えた技術におけるペロブスカイトの関連性をさらに高めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 6億9,730万米ドル |

| 予測金額 | 28億米ドル |

| CAGR | 15.1% |

2024年、ハロゲン化物ペロブスカイトは4億1,570万米ドルを生み出し、2034年までCAGR 16.7%で成長すると予想されます。これらの材料は、その卓越した光吸収能力により、太陽電池やオプトエレクトロニクスの用途で特に有効であることが証明されています。タンデムソーラー構成で優れた性能を発揮するその能力は、研究者や商業開発者から注目され続けています。新興の太陽電池材料に対する資金が着実に増加していることは、これらの技術に対する世界の信頼が確固たるものであることを示しています。ハロゲン化物ペロブスカイトを含む技術革新は、高効率太陽電池とフォトニクスソリューションの進歩を加速すると予想されます。

太陽電池セグメントは、2024年に4億6,050万米ドルの市場規模を占め、66.1%のシェアを占め、2034年まで18%のCAGRで成長すると予測されています。ペロブスカイト太陽電池のエネルギー変換効率の向上、特にタンデム構成が、世界の太陽電池産業での利用を促進しています。この技術は、製造コストの削減とスケーラブルな製造方法によって、住宅用と公益事業用の両方のプロジェクトで使用されるソーラーパネルにますます組み込まれるようになっています。この動向は、再生可能エネルギーへの世界の移行と一致しており、ソーラーが将来のクリーンエネルギー投資をリードすると予測されています。

ペロブスカイトウェハー、セル、モジュールといった重要部品の製造能力が世界的に集中する中国市場は、2024年に80%のシェアを占めます。この広範な管理は、太陽電池技術の主要輸出国としての地位を強化するだけでなく、ペロブスカイトを含む新興太陽電池セグメントの価格設定、拡大性、技術革新ペースに対する戦略的影響力を強化しています。中国は、研究開発への積極的な投資、国からの補助金、垂直統合された製造エコシステムにより、次世代技術の商業化を可能にしています。

この市場の主要企業には、Frontier Materials、Swift Solar、Oxford PV、Saule Technologies、Microquanta Semiconductorなどがあります。主要企業はその地位を確保するため、生産能力の拡大、材料技術革新による効率の向上、エネルギー供給会社や研究機関との戦略的提携に注力しています。多くの企業は、大規模展開の実行可能性をテストするためにパイロット生産ラインに投資する一方、競争優位性を維持するために特許を通じて知的財産を保護しています。こうした戦略は、世界の需要に応え、長期的な市場での存在感を高めるためのものです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 産業への影響

- 供給側の影響(原料)

- 主要原料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原料)

- 影響を受ける主要企業

- 戦略的な産業対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 施策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)注:上記の貿易統計は主要国についてのみ提供されます

- 主要輸出国

- 主要輸入国

- 利益率分析

- 主要ニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 世界のエネルギー需要の増加が次世代太陽光発電の導入を促進

- クリーンで分散型のエネルギーシステムに対する政府の有利なインセンティブ

- ペロブスカイトベースの太陽光発電技術の優れた効率性とコスト優位性

- 発展途上地域と遠隔地におけるオフグリッド電化プロジェクトの増加

- 産業の潜在的リスク・課題

- 過酷な環境におけるペロブスカイト材料の安定性と耐久性に関する懸念

- 確立された大規模な製造と商業化インフラの欠如

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 競合情勢

- 製品ポートフォリオと仕様

- SWOT分析

- 企業の市場シェア分析

- 企業による世界の市場シェア

- 地域市場シェア分析

- 製品ポートフォリオシェア分析

- 戦略的取り組み

- 合併と買収

- パートナーシップとコラボレーション

- 製品の発売と革新

- 拡大計画と投資

- 企業ベンチマーク

- 製品イノベーションのベンチマーク

- 価格戦略の比較

- 配電網の比較

- 顧客サービスとサポートの比較

第5章 市場推定・予測:材料別、2021~2034年

- 主要動向

- ハロゲン化物ペロブスカイト

- 有機無機ハイブリッドハライドペロブスカイト

- 全無機ハロゲン化物ペロブスカイト

- 鉛系ハロゲン化物ペロブスカイト

- 鉛フリーハロゲン化物ペロブスカイト

- 酸化物ペロブスカイト

- チタン酸塩系酸化物ペロブスカイト

- 強誘電体酸化物ペロブスカイト

- その他の酸化物ペロブスカイト

- その他のペロブスカイト資料

- 二重ペロブスカイト

- 層状ペロブスカイト

- ペロブスカイトに着想を得た材料

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 太陽電池

- 単接合型ペロブスカイト太陽電池

- タンデムペロブスカイトシリコン太陽電池

- 軟質ペロブスカイト太陽電池

- 建物一体型太陽光発電(BIPV)

- 宇宙用途

- 発光ダイオード(LED)

- ディスプレイ技術

- 照明用途

- 光検出器とセンサ

- X線検出器

- 光検出器

- ガスセンサ

- 圧力センサ

- レーザーと光学用途

- エネルギー貯蔵装置

- 量子コンピューティングの用途

- その他

- 触媒

- 熱電デバイス

- ニューロモルフィックコンピューティング

第7章 市場推定・予測:最終用途産業別、2021~2034年

- 主要動向

- エネルギーと発電

- エレクトロニクスとオプトエレクトロニクス

- 建設資材

- 自動車と輸送

- 航空宇宙と防衛

- ヘルスケアと医療機器

- 通信

- その他

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第9章 企業プロファイル

- Oxford PV

- Saule Technologies

- Microquanta Semiconductor

- Swift Solar

- Frontier Materials

- Toshiba

- Panasonic

- Sekisui Chemical

- Hanwha Vision

- GCL Suzhou Nanotechnology

- EneCoat Technologies

- Kaneka Corporation

- Aisin Corporation

- UtmoLight

- Wonder Solar

- Other Notable Players

目次

The Global Perovskite Market was valued at USD 697.3 million in 2024 and is estimated to grow at a CAGR of 15.1% to reach USD 2.8 billion by 2034, driven by the rising global attention toward sustainable energy and material innovation in the spotlight, especially in clean energy applications. As energy infrastructures adapt to support renewable integration, perovskites are gaining traction due to their versatility, lightweight properties, and compatibility with advanced energy systems. These materials are unlocking new possibilities in solar power, sensors, and consumer electronics thanks to their strong performance in flexible and efficient thin-film configurations.

Ongoing R&D is driven by public and private initiatives focused on accelerating energy transformation, particularly in the United States, where government-backed sustainability targets align with investments in photonics and semiconductor innovation. Interest is growing in combining silicon with perovskite for tandem solar cell use, offering potential to exceed the efficiency levels of traditional photovoltaics. Their adaptability also supports applications in portable and wearable solar devices, addressing demand from residential and commercial markets. Rapid innovation in thin-film electronics enables creative device designs, further increasing the relevance of perovskites in future-facing technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $697.3 Million |

| Forecast Value | $2.8 Billion |

| CAGR | 15.1% |

In 2024, halide perovskites generated USD 415.7 million and are expected to grow at a CAGR of 16.7% through 2034. These materials are proving especially effective in solar and optoelectronic applications because of their exceptional light absorption capabilities. Their ability to perform well in tandem solar configurations continues to draw attention from researchers and commercial developers. A steady increase in funding for emerging solar materials indicates robust global confidence in these technologies. Innovations involving halide perovskites are expected to accelerate progress in high-efficiency solar and photonics solutions.

The solar cell segment dominated the market with USD 460.5 million in 2024, holding a 66.1% share and anticipated to grow at 18% CAGR through 2034. The improved energy conversion efficiency of perovskite solar cells, especially in tandem configurations, propels their use in the global solar industry. Technology is increasingly being integrated into solar panels used in both residential and utility-scale projects due to reduced manufacturing costs and scalable fabrication methods. This trend aligns with the global transition toward renewable energy, with solar projected to lead future clean energy investments.

China Perovskite Market held 80% share in 2024, driven by the world's manufacturing capacity for critical components, such as wafers, cells, and modules, concentrated within its borders. This extensive control not only strengthens its position as the primary exporter of solar technologies but also reinforces its strategic influence over the pricing, scalability, and innovation pace across emerging solar segments, including perovskites. China's aggressive investments in R&D, state-backed subsidies, and vertically integrated manufacturing ecosystems enable it to commercialize next-generation technologies.

Top companies in this market include Frontier Materials, Swift Solar, Oxford PV, Saule Technologies, and Microquanta Semiconductor. To secure their positions, leading companies focus on scaling production capabilities, enhancing efficiency through material innovation, and forming strategic partnerships with energy providers and research institutions. Many invest in pilot production lines to test large-scale deployment viability while protecting their IP through patents to maintain a competitive advantage. These strategies are designed to meet global demand and reinforce long-term market presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code) Note: the above trade statistics will be provided for key countries only.

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising global energy demand driving next-generation photovoltaic adoption

- 3.7.1.2 Favorable government incentives for clean and decentralized energy systems

- 3.7.1.3 Superior efficiency and cost advantages of perovskite-based solar technologies

- 3.7.1.4 Increasing off-grid electrification projects in developing and remote regions

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Stability and durability concerns of perovskite materials in harsh environments

- 3.7.2.2 Lack of established large-scale manufacturing and commercialization infrastructure

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Competitive landscape

- 4.1.1 Company overview

- 4.1.2 Product portfolio and specifications

- 4.1.3 Swot analysis

- 4.2 Company market share analysis, 2024

- 4.2.1 Global market share by company

- 4.2.2 Regional market share analysis

- 4.2.3 Product portfolio share analysis

- 4.3 Strategic initiative

- 4.3.1 Mergers and acquisitions

- 4.3.2 Partnerships and collaborations

- 4.3.3 Product launches and innovations

- 4.3.4 Expansion plans and investments

- 4.4 Company benchmarking

- 4.4.1 Product innovation benchmarking

- 4.4.2 Pricing strategy comparison

- 4.4.3 Distribution network comparison

- 4.4.4 Customer service and support comparison

Chapter 5 Market Estimates & Forecast, By Material Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Halide perovskites

- 5.2.1 Organic-inorganic hybrid halide perovskites

- 5.2.2 All-inorganic halide perovskites

- 5.2.3 Lead-based halide perovskites

- 5.2.4 Lead-free halide perovskites

- 5.3 Oxide perovskites

- 5.3.1 Titanate-based oxide perovskites

- 5.3.2 Ferroelectric oxide perovskites

- 5.3.3 Other oxide perovskites

- 5.4 Other perovskite materials

- 5.4.1 Double perovskites

- 5.4.2 Layered perovskites

- 5.4.3 Perovskite-inspired materials

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solar cells

- 6.2.1 Single-junction perovskite solar cells

- 6.2.2 Tandem perovskite-silicon solar cells

- 6.2.3 Flexible perovskite solar cells

- 6.2.4 Building-integrated photovoltaics (bipv)

- 6.2.5 Space applications

- 6.3 Light-emitting diodes (leds)

- 6.3.1 Display technologies

- 6.3.2 Lighting applications

- 6.4 Photodetectors and sensors

- 6.4.1 X-ray detectors

- 6.4.2 Photodetectors

- 6.4.3 Gas sensors

- 6.4.4 Pressure sensors

- 6.5 Lasers and optical applications

- 6.6 Energy storage devices

- 6.7 Quantum computing applications

- 6.8 Other applications

- 6.8.1 Catalysis

- 6.8.2 Thermoelectric devices

- 6.8.3 Neuromorphic computing

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Energy and power generation

- 7.3 Electronics and optoelectronics

- 7.4 Construction and building materials

- 7.5 Automotive and transportation

- 7.6 Aerospace and defense

- 7.7 Healthcare and medical devices

- 7.8 Telecommunications

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Oxford PV

- 9.2 Saule Technologies

- 9.3 Microquanta Semiconductor

- 9.4 Swift Solar

- 9.5 Frontier Materials

- 9.6 Toshiba

- 9.7 Panasonic

- 9.8 Sekisui Chemical

- 9.9 Hanwha Vision

- 9.10 GCL Suzhou Nanotechnology

- 9.11 EneCoat Technologies

- 9.12 Kaneka Corporation

- 9.13 Aisin Corporation

- 9.14 UtmoLight

- 9.15 Wonder Solar

- 9.16 Other Notable Players

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日