|

|

市場調査レポート

商品コード

1784670

アジア太平洋の水産飼料市場の分析(2021~2031年):市場範囲・区分・動向・競合分析Asia Pacific Aquafeed Market Report 2021-2031 by Scope, Segmentation, Dynamics, and Competitive Analysis |

||||||

|

|||||||

|

|||||||

| アジア太平洋の水産飼料市場の分析(2021~2031年):市場範囲・区分・動向・競合分析 |

|

出版日: 2025年07月10日

発行: The Insight Partners

ページ情報: 英文 214 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

アジア太平洋の水産飼料の市場規模は、2024年の406億5,328万米ドルから2031年には631億4,721万米ドルに達すると予測されています。2024年から2031年までのCAGRは6.5%を記録すると推定されます。

エグゼクティブサマリー - アジア太平洋の水産飼料市場の分析

アジア太平洋は世界最大の水産物の生産・消費地であり、水産飼料にとって重要な市場です。この地域は人口が多く、成長しているため、水産物を含むタンパク質が豊富な食品に対する需要が高いです。所得が上昇し食生活が多様化するにつれて、水産物の消費はさらに増加し、養殖生産を支える水産飼料へのニーズが高まることが予想されます。水産養殖はアジア太平洋の主要産業であり、世界の水産物生産に大きく貢献しています。国連食糧農業機関(FAO)によると、2022年にはアジアが養殖総生産量の91.4%を占めています。増大する需要に対応するために集約的な水産養殖がますます重視されるようになっており、養殖水産動物の最適な成長と健康を確保するために高品質の水産飼料を安定供給する必要があります。さらに、この地域では、水産加工品や特殊種などの付加価値の高い養殖製品へのシフトが見られます。これらの製品は、特定の栄養ニーズを満たすために特殊な飼料や配合飼料を必要とすることが多く、水産飼料の需要をさらに押し上げています。さらに、水産飼料技術の進歩と、より持続可能で効率的な飼料配合の開発が、アジア太平洋の水産飼料市場の成長に寄与しています。

アジア太平洋の水産飼料市場 - セグメント別分析:

水産飼料市場の分析に寄与した主要セグメントは、原料の種類、魚種、ライフサイクルです。

原料の種類別では、水産飼料市場は大豆、トウモロコシ、魚粉・魚油、その他に区分されます。2024年にはその他が最大シェアを占めています。

魚種別では、水産飼料市場は魚類、甲殻類、軟体動物、その他に区分されます。2024年には魚類が最大のシェアを占めています。

ライフサイクル別では、水産飼料市場はスターター飼料、グロワー飼料、フィニッシャー飼料、ブローダー飼料に区分されます。2024年にはスターター飼料が最大シェアを占める。

アジア太平洋の水産飼料市場 - 展望

飼料生産における技術の進歩は、効率性、持続可能性、カスタマイズ性を高めることによって水産飼料産業の将来を形成しています。精密栄養学や高度な配合技術などの革新により、メーカーはさまざまな水生種の特定の食事要件に合わせた飼料を作ることができます。これにより、養殖種の最適な成長率、より良い飼料転換率、免疫力の向上が保証され、高品質な魚介類に対する需要の高まりに対応することができます。マイクロカプセル化やナノテクノロジーなどの技術は、必須栄養素、ビタミン、ミネラルの効率的な送達を可能にし、栄養損失を減らし、様々な養殖条件下での飼料の安定性を高める。

昆虫ミール、藻類、単細胞タンパク質などの代替タンパク質源の統合も、加工・配合技術の進歩によって実現可能になりました。こうした持続可能な原料は魚粉や魚油への依存を減らし、環境問題や原料コストの変動に対処します。さらに、データ分析、機械学習、モノのインターネット(IoT)を活用したスマート給餌システムが飼料管理に革命をもたらしています。これらのシステムは、魚の行動、水質、環境パラメーターをリアルタイムで監視し、給餌スケジュールを最適化し、無駄を削減します。さらに、酵素技術とプロバイオティクスの進歩により、栄養消化率と腸内環境が改善され、全体的な飼料性能が向上しています。

アジア太平洋の水産飼料市場 - 国別考察

国別に見ると、アジア太平洋の水産飼料市場は、中国、日本、インド、オーストラリア、韓国、その他アジア太平洋で構成されます。2024年には中国が最大のシェアを占めています。

中国の水産飼料市場は、養殖生産の世界的リーダーとしての中国の地位によって、世界最大かつ最もダイナミックな市場の一つです。中国は世界の養殖水産物生産量の大部分を占めており、コイ、ティラピア、エビ、ナマズなどの魚種が養殖の主役となっています。FAOによれば、中国はアジアの養殖業増加の55.4%(330万トン)を占め、引き続き主要な貢献国です。水産物の主要生産国であることに加え、中国は2002年以来、水産物の主要輸出国でもあります。FAOによれば、2022年の水産動物製品の世界輸出に占める中国の寄与率は12%で、商品貿易全体に占める中国のシェア14%にわずかに及ばないもの、それに匹敵します。この膨大な生産規模は、養殖される水生種の栄養ニーズと成長をサポートするために、養殖に対する高く安定した需要を生み出しています。市場の成長は、人口の増加、所得の上昇、より健康的でタンパク質の豊富な食生活へのシフトに牽引された、中国国内の水産物消費の増加によって支えられています。水産飼料が中国人の食生活に欠かせないものとなるにつれて、水産養殖産業は需要を満たすために規模を拡大し、高品質で栄養バランスのとれた水産飼料の必要性を高めています。

アジア太平洋の水産飼料市場 - 企業プロファイル

市場で事業を展開する主要企業には、 Cargill, Incorporated、World Feeds Limited、Kemin Industries Inc、Archer-Daniels-Midland Co、Alltech Inc、BioMar Group AS、Purina Animal Nutrition LLC、Godrej Agrovet Ltd、Aller Aqua AS、Raanan Fish Feed West Africa Limited、Arabian Agricultural Services Company、Bern Aqua NV、Avanti Feeds Limited、Skretting、Ridley Corporation Limited、Growel Feeds Pvt Ltd、Quality Feeds Limited、Grand Fish Feed、Dibaq Diproteg SA、Marubeni Nisshin Feed Co Ltd, などがあります。これらの企業は、消費者に革新的な製品を提供し、市場シェアを拡大するために、事業拡大、製品革新、M&Aなど様々な戦略を採用しています。

アジア太平洋の水産飼料市場 - 分析手法:

当レポートで紹介するデータの収集と分析には、以下の調査手法を採用しています:

二次調査の調査プロセスは、各市場の質的・量的データを収集するために、社内外の情報源を活用した包括的な二次調査から始まります。一般的に参照される二次調査情報源は以下の通りですが、これらに限定されるものではありません:

企業のウェブサイト、年次報告書、財務諸表、ブローカーの分析、投資家のプレゼンテーション。業界専門誌、その他関連、出版物、政府文書、統計データベース、市場レポートニュース記事、プレスリリース、ウェブキャスト。ただし、企業プロファイルに含まれる財務データはすべて米ドルに統一されています。他の通貨で報告されている企業の数値は、該当年の関連為替レートを使用して米ドルに換算されています。

一次調査:インサイト・パートナーズでは、データ分析を検証し、貴重な知見を得るために、毎年、業界利害関係者や専門家に相当数の1次インタビューを実施しています。これらの調査は、以下を目的としています:

二次調査の結果を検証し、改良します。分析チームの専門知識と市場理解を深めます。市場規模、動向、成長パターン、競合力学、将来の見通しに関する考察を得ます。1次調査は、様々な市場、カテゴリー、セグメント、サブセグメントを対象とし、Eメールでのやり取りや電話インタビューで実施します。参加者は通常以下の通りです:

業界の利害関係者(副社長、事業開発マネージャー、マーケット・インテリジェンス・マネージャー、国内営業マネージャー)、業界固有の専門知識を持つ外部専門家(評価専門家、リサーチアナリスト、国内営業マネージャー、主要オピニオンリーダー)

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 分析手法

- 二次調査

- 一次調査

- 仮説の策定

- マクロ経済要因分析

- 基礎数値の動向

- データの三角測量

- 国レベルのデータ

第4章 アジア太平洋の水産飼料市場情勢

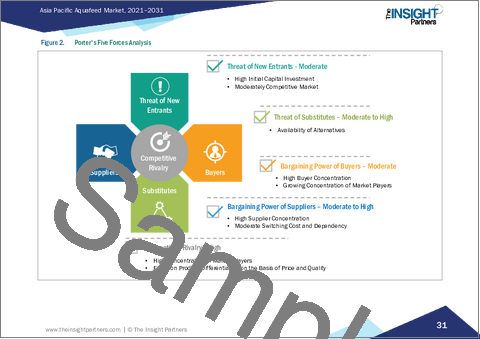

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- エコシステム分析

- 原材料サプライヤー

- メーカー

- ディストリビューター/サプライヤー

- エンドユーザー

- 生産能力:メーカー別(キロトン、2023年)

第5章 アジア太平洋の水産飼料市場:主要市場力学

- アジア太平洋の水産飼料市場:主要市場力学

- 市場促進要因

- 水産養殖産業の成長

- 高品質飼料へのシフトの増加

- 市場抑制要因

- 原材料の高コスト

- 市場機会

- 機能性・薬用飼料への需要の高まり

- 今後の動向

- 飼料生産における技術の進歩

- 促進要因と抑制要因の影響

第6章 水産飼料市場:アジア太平洋市場の分析

- アジア太平洋の水産飼料市場の規模 (数量ベース、2021~2031年)

- アジア太平洋の水産飼料市場の予測・分析 (数量ベース)

- アジア太平洋の水産飼料市場の収益 (2021~2031年)

- アジア太平洋の水産飼料市場の予測・分析

第7章 アジア太平洋の水産飼料市場規模・収益分析:原料の種類別

- 大豆

- トウモロコシ

- 魚粉・魚油

- その他

第8章 アジア太平洋の水産飼料市場の数量と収益分析:魚種別

- 魚類

- 甲殻類

- 軟体動物

- その他

第9章 アジア太平洋の水産飼料市場規模・収益分析-ライフサイクル別

- スターター飼料

- グロワー飼料

- フィニッシャー飼料

- ブローダー飼料

第10章 アジア太平洋の水産飼料市場:国別分析

- アジア太平洋

- オーストラリア

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

第11章 競合情勢

- 競合ベンチマーキング

- 競合ベンチマーキング:アジア太平洋

- 市場集中度

第12章 業界情勢

- 製品発表

- 企業ニュース

- 事業拡大

- 合弁事業

第13章 企業プロファイル

- Cargill, Incorporated

- World Feeds Limited

- Kemin Industries Inc

- Archer-Daniels-Midland Co

- Alltech Inc

- BioMar Group AS

- Purina Animal Nutrition LLC

- Godrej Agrovet Ltd

- Aller Aqua AS

- Raanan Fish Feed West Africa Limited

- Arabian Agricultural Services Company

- Bern Aqua NV

- Avanti Feeds Limited

- Skretting

- Ridley Corporation Limited

- Growel Feeds Pvt Ltd

- Quality Feeds Limited

- Grand Fish Feed

- Dibaq Diproteg SA

- Marubeni Nisshin Feed Co Ltd

第14章 付録

List Of Tables

- Table 1. Asia Pacific Aquafeed Market Segmentation

- Table 2. List of Raw Material Suppliers, GCC and Iraq

- Table 3. List of Potential Customers, GCC and Iraq

- Table 4. Production Capacity by Manufacturers, 2023 (Kilo Tons)

- Table 5. Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- Table 6. Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Table 7. Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Ingredient Type

- Table 8. Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Ingredient Type

- Table 9. Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Species

- Table 10. Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Species

- Table 11. Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Lifecycle

- Table 12. Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Lifecycle

- Table 13. Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Country

- Table 14. Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Country

- Table 15. Australia: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Ingredient Type

- Table 16. Australia: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Ingredient Type

- Table 17. Australia: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Species

- Table 18. Australia: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Species

- Table 19. Australia: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Lifecycle

- Table 20. Australia: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Lifecycle

- Table 21. China: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Ingredient Type

- Table 22. China: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Ingredient Type

- Table 23. China: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Species

- Table 24. China: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Species

- Table 25. China: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Lifecycle

- Table 26. China: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Lifecycle

- Table 27. India: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Ingredient Type

- Table 28. India: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Ingredient Type

- Table 29. India: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Species

- Table 30. India: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Species

- Table 31. India: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Lifecycle

- Table 32. India: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Lifecycle

- Table 33. Japan: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Ingredient Type

- Table 34. Japan: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Ingredient Type

- Table 35. Japan: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Species

- Table 36. Japan: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Species

- Table 37. Japan: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Lifecycle

- Table 38. Japan: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Lifecycle

- Table 39. South Korea: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Ingredient Type

- Table 40. South Korea: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Ingredient Type

- Table 41. South Korea: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Species

- Table 42. South Korea: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Species

- Table 43. South Korea: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Lifecycle

- Table 44. South Korea: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Lifecycle

- Table 45. Rest of APAC: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Ingredient Type

- Table 46. Rest of APAC: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Ingredient Type

- Table 47. Rest of APAC: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Species

- Table 48. Rest of APAC: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Species

- Table 49. Rest of APAC: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons) - by Lifecycle

- Table 50. Rest of APAC: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Lifecycle

List Of Figures

- Figure 1. Asia Pacific Aquafeed Market Segmentation - Country

- Figure 2. Porter's Five Forces Analysis

- Figure 3. Ecosystem: Aquafeed Market

- Figure 4. World Aquaculture Production, 1990-2022

- Figure 5. Future Price Development of Fish Oil (A) and Fishmeal (B) in USD/ton Under the Four Climate Change and European Aquatic Resources (CERES) Scenarios

- Figure 6. Impact Analysis of Drivers and Restraints

- Figure 7. Asia Pacific Aquafeed Market Volume (Kilo Tons), 2021-2031

- Figure 8. Asia Pacific Aquafeed Market Revenue (US$ Million), 2024-2031

- Figure 9. Asia Pacific Aquafeed Market Share (%) - Ingredient Type, 2024 and 2031

- Figure 10. Soybean: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- Figure 11. Soybean: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 12. Corn: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- Figure 13. Corn: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 14. Fishmeal and Fish Oil: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- Figure 15. Fishmeal and Fish Oil: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 16. Others: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- Figure 17. Others: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 18. Asia Pacific Aquafeed Market Share (%) - Species, 2024 and 2031

- Figure 19. Fish: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- Figure 20. Fish: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 21. Crustaceans: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- Figure 22. Crustaceans: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 23. Mollusks: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- Figure 24. Mollusks: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 25. Others: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- Figure 26. Others: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 27. Asia Pacific Aquafeed Market Share (%) - Lifecycle, 2024 and 2031

- Figure 28. Starter Feed: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- Figure 29. Starter Feed: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 30. Grower Feed: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- Figure 31. Grower Feed: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 32. Finisher Feed: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- Figure 33. Finisher Feed: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 34. Brooder Feed: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- Figure 35. Brooder Feed: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 36. Asia Pacific Aquafeed Market Breakdown by Key Countries, 2024 and 2031 (%)

- Figure 37. Australia: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 38. China: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 39. India: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 40. Japan: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 41. South Korea: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 42. Rest of APAC: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 43. Market Concentration

The Asia Pacific aquafeed market size is expected to reach US$ 63,147.21 million by 2031 from US$ 40,653.28 million in 2024. The market is estimated to record a CAGR of 6.5% from 2024 to 2031.

Executive Summary and Asia Pacific Aquafeed Market Analysis:

Asia Pacific is the world's largest producer and consumer of seafood, making it a significant market for aquafeed. The region's large and growing population has a high demand for protein-rich foods, including seafood. As income rises and diets diversify, seafood consumption is expected to increase further, driving the need for more aquafeed to support aquaculture production. Aquaculture is a major industry in Asia Pacific, contributing significantly to global seafood production. According to the Food and Agriculture Organization of the United Nations (FAO), in 2022, Asia contributed 91.4% of total aquaculture production. The increasing focus on intensive aquaculture practices to meet growing demand requires a steady supply of high-quality aquafeed to ensure optimal growth and the health of farmed aquatic animals. Furthermore, the region is witnessing a shift toward value-added aquaculture products, such as processed seafood and specialty species. These products often require specialized diets and formulated feeds to meet specific nutritional needs, further boosting the demand for aquafeed. Further, advancements in aquafeed technology and the development of more sustainable and efficient feed formulations are contributing to the growth of the aquafeed market in Asia Pacific.

Asia Pacific Aquafeed Market Segmentation Analysis:

Key segments that contributed to the derivation of the Aquafeed Market analysis are ingredient type, species, and lifecycle.

By ingredient type, the aquafeed market is segmented into soybean, corn, fishmeal, fish oil, and others. The others held the largest share of the market in 2024.

By species, the aquafeed market is segmented into fish, crustaceans, mollusks, and others. The fish held the largest share of the market in 2024.

By lifecycle, the aquafeed market is segmented into starter feed, grower feed, finisher feed, and brooder feed. The starter feed held the largest share of the market in 2024.

Asia Pacific Aquafeed Market Outlook

Technological advancements in feed production are shaping the future of the aquafeed industry by enhancing efficiency, sustainability, and customization. Innovations such as precision nutrition and advanced formulation techniques allow manufacturers to create feeds tailored to the specific dietary requirements of different aquatic species. This ensures optimal growth rates, better feed conversion ratios, and improved immunity in farmed species, addressing the growing demand for high-quality seafood. Technologies such as microencapsulation and nanotechnology enable the efficient delivery of essential nutrients, vitamins, and minerals, reducing nutrient loss and enhancing feed stability under varying aquaculture conditions.

The integration of alternative protein sources, such as insect meal, algae, and single-cell proteins, has also been made feasible through advancements in processing and formulation technologies. These sustainable ingredients reduce dependency on fishmeal and fish oil, addressing environmental concerns and raw material cost fluctuations. Additionally, smart feeding systems powered by data analytics, machine learning, and the Internet of Things (IoT) are revolutionizing feed management. These systems monitor fish behavior, water quality, and environmental parameters in real-time to optimize feeding schedules and reduce wastage. Furthermore, advancements in enzyme technology and probiotics are improving nutrient digestibility and gut health, enhancing overall feed performance.

Asia Pacific Aquafeed Market Country Insights

Based on country, the Asia Pacific aquafeed market comprises China, Japan, India, Australia, South Korea, and the Rest of Asia Pacific. China held the largest share in 2024.

The aquafeed market in China is one of the largest and most dynamic in the world, driven by the country's position as a global leader in aquaculture production. China accounts for a significant portion of global farmed seafood output, with species such as carp, tilapia, shrimp, and catfish dominating its aquaculture landscape. According to the FAO, China continues to be the main contributor, accounting for 55.4% (3.3 million tonnes) of the growth in Asian aquaculture. In addition to being by far the major producer of aquatic products, China has also been the leading exporter of aquatic products since 2002. According to the FAO, in 2022, China's contribution to world exports of aquatic animal products stood at 12%, comparable to-although slightly less than-the country's 14% share in total merchandise trade. This vast scale of production generates a high and consistent demand for aquaculture to support the nutritional needs and growth of these farmed aquatic species. The market's growth is underpinned by China's increasing domestic seafood consumption, driven by a growing population, rising incomes, and a shift toward healthier protein-rich diets. As seafood becomes an integral part of the Chinese diet, the aquaculture industry is scaling up to meet the demand, boosting the need for high-quality, nutritionally balanced aquafeed.

Asia Pacific Aquafeed Market Company Profiles

Some of the key players operating in the market include Cargill, Incorporated; World Feeds Limited; Kemin Industries Inc; Archer-Daniels-Midland Co; Alltech Inc; BioMar Group AS; Purina Animal Nutrition LLC; Godrej Agrovet Ltd; Aller Aqua AS; Raanan Fish Feed West Africa Limited; Arabian Agricultural Services Company; Bern Aqua NV; Avanti Feeds Limited; Skretting; Ridley Corporation Limited; Growel Feeds Pvt Ltd; Quality Feeds Limited; Grand Fish Feed; Dibaq Diproteg SA; and Marubeni Nisshin Feed Co Ltd, among others. These players are adopting various strategies such as expansion, product innovation, and mergers and acquisitions to provide innovative products to their consumers and increase their market share.

Asia Pacific Aquafeed Market Research Methodology :

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research The research process begins with comprehensive secondary research, utilizing both internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

Company websites , annual reports, financial statements, broker analyses, and investor presentations. Industry trade journals and other relevant publications. Government documents , statistical databases, and market reports. News articles , press releases, and webcasts specific to companies operating in the market. Note: All financial data included in the Company Profiles section has been standardized to USD. For companies reporting in other currencies, figures have been converted to USD using the relevant exchange rates for the corresponding year.

Primary Research The Insight Partners' conducts a significant number of primary interviews each year with industry stakeholders and experts to validate its data analysis, and gain valuable insights. These research interviews are designed to:

Validate and refine findings from secondary research. Enhance the expertise and market understanding of the analysis team. Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects. Primary research is conducted via email interactions and telephone interviews, encompassing various markets, categories, segments, and sub-segments across different regions. Participants typically include:

Industry stakeholders : Vice Presidents, business development managers, market intelligence managers, and national sales managers External experts : Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

Table Of Contents

1. Introduction

- 1.1 Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Secondary Research

- 3.2 Primary Research

- 3.2.1 Hypothesis formulation:

- 3.2.2 Macroeconomic factor analysis:

- 3.2.3 Developing base number:

- 3.2.4 Data Triangulation:

- 3.2.5 Country-level data:

4. Asia Pacific Aquafeed Market Landscape

- 4.1 Porter's Five Forces Analysis

- 4.1.1 Bargaining Power of Suppliers

- 4.1.2 Bargaining Power of Buyers

- 4.1.3 Threat of New Entrants

- 4.1.4 Competitive Rivalry

- 4.1.5 Threat of Substitutes

- 4.2 Ecosystem Analysis

- 4.2.1 Raw Material Suppliers:

- 4.2.2 Manufacturers:

- 4.2.3 Distributors/Suppliers:

- 4.2.4 End Users:

- 4.3 Production Capacity by Manufacturers, 2023 (Kilo Tons)

5. Asia Pacific Aquafeed Market - Key Market Dynamics

- 5.1 Asia Pacific Aquafeed Market - Key Market Dynamics

- 5.2 Market Drivers

- 5.2.1 Growing Aquaculture Industry

- 5.2.2 Increasing Shift Toward High-Quality Feed

- 5.3 Market Restraints

- 5.3.1 High Cost of Raw Materials

- 5.4 Market Opportunities

- 5.4.1 Rising Demand for Functional and Medicated Feed

- 5.5 Future Trends

- 5.5.1 Technological Advancements in Feed Production

- 5.6 Impact of Drivers and Restraints:

6. Aquafeed Market - Asia Pacific Market Analysis

- 6.1 Asia Pacific Aquafeed Market Volume (Kilo Tons), 2021-2031

- 6.2 Asia Pacific Aquafeed Market Volume Forecast and Analysis (Kilo Tons)

- 6.3 Asia Pacific Aquafeed Market Revenue (US$ Million), 2024-2031

- 6.4 Asia Pacific Aquafeed Market Forecast and Analysis

7. Asia Pacific Aquafeed Market Volume and Revenue Analysis - by Ingredient Type

- 7.1 Soybean

- 7.1.1 Overview

- 7.1.2 Soybean: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- 7.1.3 Soybean: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 7.2 Corn

- 7.2.1 Overview

- 7.2.2 Corn: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- 7.2.3 Corn: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 7.3 Fishmeal and Fish Oil

- 7.3.1 Overview

- 7.3.2 Fishmeal and Fish Oil: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- 7.3.3 Fishmeal and Fish Oil: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 7.4 Others

- 7.4.1 Overview

- 7.4.2 Others: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- 7.4.3 Others: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

8. Asia Pacific Aquafeed Market Volume and Revenue Analysis - by Species

- 8.1 Fish

- 8.1.1 Overview

- 8.1.2 Fish: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- 8.1.3 Fish: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 8.2 Crustaceans

- 8.2.1 Overview

- 8.2.2 Crustaceans: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- 8.2.3 Crustaceans: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 8.3 Mollusks

- 8.3.1 Overview

- 8.3.2 Mollusks: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- 8.3.3 Mollusks: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 8.4 Others

- 8.4.1 Overview

- 8.4.2 Others: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- 8.4.3 Others: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

9. Asia Pacific Aquafeed Market Volume and Revenue Analysis - by Lifecycle

- 9.1 Starter Feed

- 9.1.1 Overview

- 9.1.2 Starter Feed: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- 9.1.3 Starter Feed: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 9.2 Grower Feed

- 9.2.1 Overview

- 9.2.2 Grower Feed: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- 9.2.3 Grower Feed: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 9.3 Finisher Feed

- 9.3.1 Overview

- 9.3.2 Finisher Feed: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- 9.3.3 Finisher Feed: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 9.4 Brooder Feed

- 9.4.1 Overview

- 9.4.2 Brooder Feed: Asia Pacific Aquafeed Market - Volume and Forecast, 2021-2031 (Kilo Tons)

- 9.4.3 Brooder Feed: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

10. Asia Pacific Aquafeed Market - Country Analysis

- 10.1 Asia Pacific

- 10.1.1 Asia Pacific Aquafeed Market Revenue and Forecast and Analysis - by Country

- 10.1.1.1 Asia Pacific Aquafeed Market Volume and Forecast and Analysis - by Country

- 10.1.1.2 Asia Pacific Aquafeed Market Revenue and Forecast and Analysis - by Country

- 10.1.1.3 Australia: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 10.1.1.3.1 Australia: Asia Pacific Aquafeed Market Share - by Ingredient Type

- 10.1.1.3.2 Australia: Asia Pacific Aquafeed Market Share - by Species

- 10.1.1.3.3 Australia: Asia Pacific Aquafeed Market Share - by Lifecycle

- 10.1.1.4 China: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 10.1.1.4.1 China: Asia Pacific Aquafeed Market Share - by Ingredient Type

- 10.1.1.4.2 China: Asia Pacific Aquafeed Market Share - by Species

- 10.1.1.4.3 China: Asia Pacific Aquafeed Market Share - by Lifecycle

- 10.1.1.5 India: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 10.1.1.5.1 India: Asia Pacific Aquafeed Market Share - by Ingredient Type

- 10.1.1.5.2 India: Asia Pacific Aquafeed Market Share - by Species

- 10.1.1.5.3 India: Asia Pacific Aquafeed Market Share - by Lifecycle

- 10.1.1.6 Japan: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 10.1.1.6.1 Japan: Asia Pacific Aquafeed Market Share - by Ingredient Type

- 10.1.1.6.2 Japan: Asia Pacific Aquafeed Market Share - by Species

- 10.1.1.6.3 Japan: Asia Pacific Aquafeed Market Share - by Lifecycle

- 10.1.1.7 South Korea: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 10.1.1.7.1 South Korea: Asia Pacific Aquafeed Market Share - by Ingredient Type

- 10.1.1.7.2 South Korea: Asia Pacific Aquafeed Market Share - by Species

- 10.1.1.7.3 South Korea: Asia Pacific Aquafeed Market Share - by Lifecycle

- 10.1.1.8 Rest of APAC: Asia Pacific Aquafeed Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 10.1.1.8.1 Rest of APAC: Asia Pacific Aquafeed Market Share - by Ingredient Type

- 10.1.1.8.2 Rest of APAC: Asia Pacific Aquafeed Market Share - by Species

- 10.1.1.8.3 Rest of APAC: Asia Pacific Aquafeed Market Share - by Lifecycle

- 10.1.1 Asia Pacific Aquafeed Market Revenue and Forecast and Analysis - by Country

11. Competitive Landscape

- 11.1 Competitive Benchmarking

- 11.1.1 Competitive Benchmarking - Asia Pacific

- 11.2 Market Concentration

12. Industry Landscape

- 12.1 Overview

- 12.2 Product Launch

- 12.3 Company News

- 12.4 Expansion

- 12.5 Joint Venture

13. Company Profiles

- 13.1 Cargill, Incorporated

- 13.1.1 Key Facts

- 13.1.2 Business Description

- 13.1.3 Products and Services

- 13.1.4 Financial Overview

- 13.1.5 SWOT Analysis

- 13.1.6 Key Developments

- 13.2 World Feeds Limited

- 13.2.1 Key Facts

- 13.2.2 Business Description

- 13.2.3 Products and Services

- 13.2.4 Financial Overview

- 13.2.5 SWOT Analysis

- 13.2.6 Key Developments

- 13.3 Kemin Industries Inc

- 13.3.1 Key Facts

- 13.3.2 Business Description

- 13.3.3 Products and Services

- 13.3.4 Financial Overview

- 13.3.5 SWOT Analysis

- 13.3.6 Key Developments

- 13.4 Archer-Daniels-Midland Co

- 13.4.1 Key Facts

- 13.4.2 Business Description

- 13.4.3 Products and Services

- 13.4.4 Financial Overview

- 13.4.5 SWOT Analysis

- 13.4.6 Key Developments

- 13.5 Alltech Inc

- 13.5.1 Key Facts

- 13.5.2 Business Description

- 13.5.3 Products and Services

- 13.5.4 Financial Overview

- 13.5.5 SWOT Analysis

- 13.5.6 Key Developments

- 13.6 BioMar Group AS

- 13.6.1 Key Facts

- 13.6.2 Business Description

- 13.6.3 Products and Services

- 13.6.4 Financial Overview

- 13.6.5 SWOT Analysis

- 13.6.6 Key Developments

- 13.7 Purina Animal Nutrition LLC

- 13.7.1 Key Facts

- 13.7.2 Business Description

- 13.7.3 Products and Services

- 13.7.4 Financial Overview

- 13.7.5 SWOT Analysis

- 13.7.6 Key Developments

- 13.8 Godrej Agrovet Ltd

- 13.8.1 Key Facts

- 13.8.2 Business Description

- 13.8.3 Products and Services

- 13.8.4 Financial Overview

- 13.8.5 SWOT Analysis

- 13.8.6 Key Developments

- 13.9 Aller Aqua AS

- 13.9.1 Key Facts

- 13.9.2 Business Description

- 13.9.3 Products and Services

- 13.9.4 Financial Overview

- 13.9.5 SWOT Analysis

- 13.9.6 Key Developments

- 13.10 Raanan Fish Feed West Africa Limited

- 13.10.1 Key Facts

- 13.10.2 Business Description

- 13.10.3 Products and Services

- 13.10.4 Financial Overview

- 13.10.5 SWOT Analysis

- 13.10.6 Key Developments

- 13.11 Arabian Agricultural Services Company

- 13.11.1 Key Facts

- 13.11.2 Business Description

- 13.11.3 Products and Services

- 13.11.4 Financial Overview

- 13.11.5 SWOT Analysis

- 13.11.6 Key Developments

- 13.12 Bern Aqua NV

- 13.12.1 Key Facts

- 13.12.2 Business Description

- 13.12.3 Products and Services

- 13.12.4 Financial Overview

- 13.12.5 SWOT Analysis

- 13.12.6 Key Developments

- 13.13 Avanti Feeds Limited

- 13.13.1 Key Facts

- 13.13.2 Business Description

- 13.13.3 Products and Services

- 13.13.4 Financial Overview

- 13.13.5 SWOT Analysis

- 13.13.6 Key Developments

- 13.14 Skretting

- 13.14.1 Key Facts

- 13.14.2 Business Description

- 13.14.3 Products and Services

- 13.14.4 Financial Overview

- 13.14.5 SWOT Analysis

- 13.14.6 Key Developments

- 13.15 Ridley Corporation Limited

- 13.15.1 Key Facts

- 13.15.2 Business Description

- 13.15.3 Products and Services

- 13.15.4 Financial Overview

- 13.15.5 SWOT Analysis

- 13.15.6 Key Developments

- 13.16 Growel Feeds Pvt Ltd

- 13.16.1 Key Facts

- 13.16.2 Business Description

- 13.16.3 Products and Services

- 13.16.4 Financial Overview

- 13.16.5 SWOT Analysis

- 13.16.6 Key Developments

- 13.17 Quality Feeds Limited

- 13.17.1 Key Facts

- 13.17.2 Business Description

- 13.17.3 Products and Services

- 13.17.4 Financial Overview

- 13.17.5 SWOT Analysis

- 13.17.6 Key Developments

- 13.18 Grand Fish Feed

- 13.18.1 Key Facts

- 13.18.2 Business Description

- 13.18.3 Products and Services

- 13.18.4 Financial Overview

- 13.18.5 SWOT Analysis

- 13.18.6 Key Developments

- 13.19 Dibaq Diproteg SA

- 13.19.1 Key Facts

- 13.19.2 Business Description

- 13.19.3 Products and Services

- 13.19.4 Financial Overview

- 13.19.5 SWOT Analysis

- 13.19.6 Key Developments

- 13.20 Marubeni Nisshin Feed Co Ltd

- 13.20.1 Key Facts

- 13.20.2 Business Description

- 13.20.3 Products and Services

- 13.20.4 Financial Overview

- 13.20.5 SWOT Analysis

- 13.20.6 Key Developments

14. Appendix

- 14.1 About The Insight Partners