|

|

市場調査レポート

商品コード

1784630

欧州の手術用抗菌縫合糸市場の予測 (2021~2031年):市場範囲・セグメント・動向・競合分析Europe Antimicrobial Surgical Suture Market Report 2021-2031 by Scope, Segmentation, Dynamics, and Competitive Analysis |

||||||

|

|||||||

|

|||||||

| 欧州の手術用抗菌縫合糸市場の予測 (2021~2031年):市場範囲・セグメント・動向・競合分析 |

|

出版日: 2025年07月10日

発行: The Insight Partners

ページ情報: 英文 126 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

欧州の手術用抗菌縫合糸の市場規模は、2023年の1億1,972万米ドルから2031年には2億5,211万米ドルに達すると予測されています。2024年から2031年にかけてのCAGRは9.8%を記録すると推定されます。

エグゼクティブサマリー - 欧州の手術用抗菌縫合糸市場の分析

欧州の手術用抗菌縫合糸市場は、ドイツ、フランス、英国、スペイン、イタリア、その他欧州に区分されます。欧州は世界の手術用抗菌縫合糸市場において第2位の地位を占めており、予測期間中に堅調な成長率を記録することが期待されています。心臓血管外科手術、一般外科手術、整形外科手術の増加により、手術用抗菌縫合糸の製造に注力する市場プレイヤーの増加が市場成長に繋がっています。

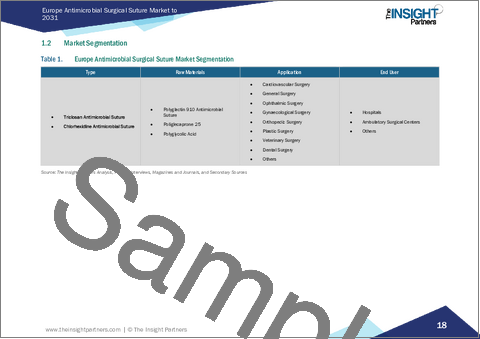

欧州の手術用抗菌縫合糸市場 - セグメンテーション分析:

手術用抗菌縫合糸市場の分析に貢献した主要セグメントは、種類、原材料、用途、エンドユーザーです。

種類別では、欧州の手術用抗菌縫合糸市場はトリクロサン抗菌縫合糸とクロルヘキシジン抗菌縫合糸に二分されます。2023年にはトリクロサン抗菌縫合糸が大きなシェアを占めています。

原料別では、欧州の手術用抗菌縫合糸市場はポリグラクチン910抗菌縫合糸、ポリグルカプロン25、ポリグリコール酸に区分されます。2023年にはポリグラクチン910抗菌縫合糸セグメントが最大シェアを占めています。

用途別では、欧州の手術用抗菌縫合糸市場は心臓血管外科、一般外科、眼科外科、婦人科外科、整形外科、形成外科、獣医外科、歯科外科、その他に区分されます。2023年には、心臓血管外科セグメントが市場で最大のシェアを占めています。

エンドユーザー別では、欧州の手術用抗菌縫合糸市場は病院、外来手術センター、その他に区分されます。2023年には病院セグメントが最大シェアを占めています。

欧州の手術用抗菌縫合糸市場の展望

鋭利な傷害以外にも、職場や職業における傷害の種類は世界的に増加しています。国際労働機関(ILO)によると、毎年230万人が労働災害を経験し、健康や生活の質に影響を及ぼしています。慢性創傷の負担が急増するにつれ、最終的には国の医療システムによる財政負担を大幅に軽減するための高度な創傷ケア管理方法に対する需要が高まっています。様々な国が傷害の治療や関連リスクの回避に多額の資金を費やしています。したがって、慢性創傷の発生率の増加に伴い、手術用抗菌縫合糸の需要も世界的に増加しています。

さらに、医療環境で行われる一般外科手術、心臓血管外科手術、整形外科手術、婦人科手術、がん手術の件数は、世界中で驚異的に増加しています。さらに、老人人口の増加は、主要な治療オプションとして手術を必要とする重篤な健康状態(例えば、ヘルニアや白内障)を助長しています。老年人口は、CVD、整形外科疾患、代謝疾患、神経疾患などにかかりやすいです。WHOによると、世界の高齢化人口は2019年の10億人から2050年には21億人に増加すると見られています。美容整形手術は、エンターテインメント業界で働く人々の間でも一般的になっています。これらの手術は、偶発的または先天的に奇形がある患者や、外見をより魅力的にしたいと望む患者に対して行われます。したがって、病院や同様の医療機関で行われる手術の急増が、手術用抗菌縫合糸の需要を押し上げています。

欧州の手術用抗菌縫合糸市場 - 国別分析

国別に見ると、欧州の手術用抗菌縫合糸市場は、ドイツ、フランス、英国、イタリア、スペイン、その他欧州で構成されます。2023年にはドイツが最大のシェアを占めています。

手術部位感染(SSI)や抗生物質耐性菌の発生率が上昇しているため、医療環境における感染予防・管理対策への需要が高まっていることが市場促進要因の主な要因です。アビディケアが調査記事で発表した最近の調査データによると、厳格な法律やガイドラインにもかかわらず、ドイツでは2008年から2016年にかけて手術部位感染(SSI)が減少していないです。400万人の患者から得た実際の病院の診療報酬データに基づくと、研究期間の総SSI有病率は4.9%でした。研究者らは、自主的なKrankenhaus-Infektions-Surveillance-Systemに基づくドイツの病院のSSI発生率の自己申告値1.08%に比べ、実際のSSI発生数は大幅に過小評価されていると結論づけています。

抗菌縫合糸がSSIを減少させ、患者の転帰を改善する利点について、医療専門家の間で認識が高まっていることが、抗菌縫合糸の採用に寄与しています。ドイツでは償還政策が優遇されており、医療費も高いため、病院やクリニックが高度な縫合技術を採用することができます。同国では医療システムが確立されており、毎年多くの外科手術が行われているため、抗菌縫合糸に対する需要が高いです。さらに、感染管理に関する厳しい規制の枠組みやガイドラインが、標準治療としての抗菌縫合糸の採用を後押ししています。国内の企業による継続的な研究開発活動は、革新的な抗菌縫合糸製品の導入につながっており、市場の成長をさらに促進しています。

欧州の手術用抗菌縫合糸市場 - 企業プロファイル

市場で事業を展開する主要企業には、TI Medical社、Healthium Medtech Limited社、Meril Life Sciences Pvt Ltd社、Unilene社、Johnson &Johnson社、Futura Surgicare Pvt Ltd社(Dolphin Sutures社)、Cencora社(AmerisourceBergen社)、Advanced MedTech Solutions Pvt Ltd社、Internacional Farmaceutica SA社などがあります。これらの企業は、消費者に革新的な製品を提供し、市場シェアを拡大するために、事業拡大、製品革新、M&Aなど様々な戦略を採用しています。

欧州の手術用抗菌縫合糸市場 - 調査手法:

本レポートで紹介するデータの収集と分析には、以下の調査手法を採用しています:

二次調査の調査プロセスは、各市場の質的・量的データを収集するために、社内外の情報源を活用した包括的な二次調査から始まります。一般的に参照される二次調査情報源は以下の通りですが、これらに限定されるものではない:

企業のウェブサイト、年次報告書、財務諸表、ブローカーの分析、投資家のプレゼンテーション。業界専門誌、その他関連出版物政府文書、統計データベース、市場レポートニュース記事、プレスリリース、ウェブキャスト。なお、企業プロファイルに含まれる財務データはすべて米ドルに統一されています。他の通貨で報告されている企業の数値は、該当年の関連為替レートを使用して米ドルに換算されています。

1次調査 - インサイト・パートナーズでは、データ分析を検証し、貴重な知見を得るために、毎年、業界利害関係者や専門家に相当数の1次インタビューを実施しています。これらの調査は、以下を目的としています:

2次調査の結果を検証し、改良します。分析チームの専門知識と市場理解を深めます。市場規模、動向、成長パターン、競合力学、将来の見通しに関する考察を得ます。1次調査は、様々な市場、カテゴリー、セグメント、サブセグメントを対象とし、Eメールでのやり取りや電話インタビューで実施します。参加者は通常以下の通りです:

業界利害関係者(副社長、事業開拓マネージャー、マーケット・インテリジェンス・マネージャー、国内営業マネージャー、外部専門家)、評価専門家(調査アナリスト、業界固有の専門知識を持つ主要オピニオンリーダー)

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要な洞察

第3章 調査手法

- 2次調査

- 1次調査

- 仮説の策定

- マクロ経済要因分析

- ファンデーション数値の開発

- データの三角測量

- 国レベルのデータ

第4章 欧州の手術用抗菌縫合糸市場:主要市場力学

- 市場促進要因

- 手術部位感染の急増

- 慢性創傷および手術例の増加

- 市場抑制要因

- 縫合糸に代わる非侵襲的な方法

- 市場機会

- 手術用抗菌縫合糸における戦略的取り組み

- 今後の動向

- スマート抗菌縫合糸

- 促進要因と抑制要因の影響

第5章 手術用抗菌縫合糸市場:欧州分析

- 欧州の手術用抗菌縫合糸市場の収益(2021~2031年)

- 欧州の手術用抗菌縫合糸市場の予測分析

第6章 欧州の手術用抗菌縫合糸市場分析:種類別

- トリクロサン抗菌縫合糸

- クロルヘキシジン抗菌縫合糸

第7章 欧州の手術用抗菌縫合糸の市場分析:原材料別

- ポリグラクチン910抗菌縫合糸

- ポリグルカプロン25

- ポリグリコール酸

第8章 欧州の手術用抗菌縫合糸の市場分析:用途別

- 心臓血管外科

- 一般外科

- 眼科手術

- 婦人科外科

- 整形外科

- 形成外科

- 獣医外科

- 歯科外科

- その他

第9章 欧州の手術用抗菌縫合糸市場分析:エンドユーザー別

- 病院

- 外来手術センター

- その他

第10章 欧州の手術用抗菌縫合糸市場:国別分析

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- その他欧州

第11章 業界情勢

- 成長戦略

- 企業シェア分析(%、2023年)

第12章 企業プロファイル

- TI Medical

- Healthium Medtech Limited

- Meril Life Sciences Pvt Ltd

- Unilene

- Johnson & Johnson

- Futura Surgicare Pvt Ltd(Dolphin Sutures)

- Cencora, Inc.(AmerisourceBergen Corporation)

- Advanced MedTech Solutions Pvt. Ltd.

- Internacional Farmaceutica SA

第13章 付録

List Of Tables

- Table 1. Europe Antimicrobial Surgical Suture Market Segmentation

- Table 2. Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Table 3. Germany: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Type

- Table 4. Germany: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Raw Materials

- Table 5. Germany: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Application

- Table 6. Germany: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by End User

- Table 7. France: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Type

- Table 8. France: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Raw Materials

- Table 9. France: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Application

- Table 10. France: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by End User

- Table 11. United Kingdom: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Type

- Table 12. United Kingdom: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Raw Materials

- Table 13. United Kingdom: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Application

- Table 14. United Kingdom: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by End User

- Table 15. Italy: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Type

- Table 16. Italy: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Raw Materials

- Table 17. Italy: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Application

- Table 18. Italy: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by End User

- Table 19. Spain: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Type

- Table 20. Spain: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Raw Materials

- Table 21. Spain: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Application

- Table 22. Spain: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by End User

- Table 23. Rest of Europe: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Type

- Table 24. Rest of Europe: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Raw Materials

- Table 25. Rest of Europe: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by Application

- Table 26. Rest of Europe: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million) - by End User

- Table 27. Recent Growth Strategies in Europe Antimicrobial Surgical Suture Market

- Table 28. Glossary of Terms, Antimicrobial Surgical Suture Market

List Of Figures

- Figure 1. Europe Antimicrobial Surgical Suture Market Segmentation, by Country

- Figure 2. Europe Antimicrobial Surgical Suture Market - Key Market Dynamics

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Europe Antimicrobial Surgical Suture Market Revenue (US$ Million), 2021-2031

- Figure 5. Europe Antimicrobial Surgical Suture Market Share (%) - by Type (2023 and 2031)

- Figure 6. Triclosan Antimicrobial Suture: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 7. Chlorhexidine Antimicrobial Suture: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 8. Europe Antimicrobial Surgical Suture Market Share (%) - by Raw Materials (2023 and 2031)

- Figure 9. Polyglactin 910 Antimicrobial Suture: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 10. Poliglecaprone 25: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 11. Polyglycolic Acid: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 12. Europe Antimicrobial Surgical Suture Market Share (%) - by Application (2023 and 2031)

- Figure 13. Cardiovascular Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 14. General Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 15. Ophthalmic Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 16. Gynaecological Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 17. Orthopedic Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 18. Plastic Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 19. Veterinary Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 20. Dental Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 21. Others: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 22. Europe Antimicrobial Surgical Suture Market Share (%) - by End User (2023 and 2031)

- Figure 23. Hospitals: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 24. Ambulatory Surgical Centers: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 25. Others: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- Figure 26. Europe: Europe Antimicrobial Surgical Suture Market Breakdown, by Key Countries - Revenue (2023) (US$ Million)

- Figure 27. Europe: Europe Antimicrobial Surgical Suture Market Breakdown, by Key Countries, 2023 and 2031 (%)

- Figure 28. Germany: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million)

- Figure 29. France: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million)

- Figure 30. United Kingdom: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million)

- Figure 31. Italy: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million)

- Figure 32. Spain: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million)

- Figure 33. Rest of Europe: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031(US$ Million)

The Europe antimicrobial surgical suture market size is expected to reach US$ 252.11 million by 2031 from US$ 119.72 million in 2023. The market is estimated to record a CAGR of 9.8% from 2024-2031.

Executive Summary and Europe Antimicrobial Surgical Suture Market Analysis:

The Europe antimicrobial surgical suture market is segmented into Germany, France, the UK, Spain, Italy, and the Rest of Europe. Europe occupies the second position in the global antimicrobial surgical suture market and is expected to register a robust growth rate over the forecast period. The increasing focus of market players on manufacturing antimicrobial surgical sutures due to the rise in cardiovascular surgeries, general surgeries, and orthopedic surgeries is leading to market growth.

Europe Antimicrobial Surgical Suture Market Segmentation Analysis:

Key segments that contributed to the derivation of the antimicrobial surgical suture market analysis are type, raw materials, application, and end user.

Based on type, the Europe antimicrobial surgical suture market is bifurcated into triclosan antimicrobial suture and chlorhexidine antimicrobial suture. The triclosan antimicrobial suture held a larger share of the market in 2023.

By raw materials, the Europe antimicrobial surgical suture market is segmented into polyglactin 910 antimicrobial suture, poliglecaprone 25, and polyglycolic acid. The polyglactin 910 antimicrobial suture segment held the largest share of the market in 2023.

By application, the Europe antimicrobial surgical suture market is segmented into cardiovascular surgery, general surgery, ophthalmic surgery, gynaecological surgery, orthopedic surgery, plastic surgery, veterinary surgery, dental surgery, and others. The cardiovascular surgery segment held the largest share of the market in 2023.

By end user, the Europe antimicrobial surgical suture market is segmented into hospitals, ambulatory surgical centers, and others. The hospitals segment held the largest share of the market in 2023.

Europe Antimicrobial Surgical Suture Market Outlook

Besides sharp injuries, the number of other types of workplace or occupational injuries is increasing worldwide. According to the International Labor Organization, ~2.3 million people experience work-related injuries every year, affecting their health and quality of life. The soaring burden of chronic wounds eventually propels the demand for advanced wound care management methods to substantially reduce the financial burden from national healthcare systems. Various countries spend significant amounts of money on treating injuries and avoiding associated risks. Therefore, with the increasing incidence of chronic wounds, the demand for antimicrobial surgical sutures is also increasing worldwide.

Further, the number of general, cardiovascular, orthopedic, gynecological, and cancer surgeries performed in healthcare settings is increasing tremendously across the world. Moreover, the growing geriatric population contributes to severe health conditions (e.g., hernia and cataracts) that require surgeries as a primary treatment option. The geriatric population is prone to CVDs, orthopedic disorders, metabolic disorders, and neurological disorders, among others. According to the WHO, the aging population across the world is likely to rise from ~1 billion in 2019 to ~2.1 billion by 2050. Aesthetic surgeries have also become common among people working in the entertainment industry. These surgeries are performed on patients who have accidental or inherent deformities and on those who wish to make their appearance more appealing. Therefore, the surging number of surgeries performed in hospitals or similar healthcare institutions is driving the demand for antimicrobial surgical sutures.

Europe Antimicrobial Surgical Suture Market Country Insights

Based on country, the Europe antimicrobial surgical suture market comprises Germany, France, the UK, Italy, Spain, and the Rest of Europe. Germany held the largest share in 2023.

The increasing demand for infection prevention and control measures in healthcare settings is a primary market driver, owing to the rising incidence of surgical site infections (SSIs) and antibiotic-resistant bacteria. Data from a recent study published in Research Article by Avidicare indicate that despite stringent laws and guidelines, surgical site infections (SSIs) in Germany did not decline between 2008 and 2016. Based on real hospital reimbursement data from 4 million patients, the study period's total SSI prevalence was 4.9%. The researchers conclude that the actual number of SSIs has been greatly underestimated compared to the self-reported 1.08% SSI rates for German hospitals based on the voluntary Krankenhaus-Infektions-Surveillance-System.

The growing awareness among healthcare professionals about the benefits of antimicrobial sutures in reducing SSIs and improving patient outcomes is contributing to the adoption of these sutures. Favorable reimbursement policies and high healthcare expenditure in Germany also enable hospitals and clinics to adopt advanced suturing technologies. The country's well-established healthcare system and many annual surgical procedures create a high demand for antimicrobial sutures. Furthermore, stringent regulatory frameworks and guidelines for infection control are driving the adoption of antimicrobial sutures as a standard of care. Ongoing research and development activities by companies in the country are leading to the introduction of innovative antimicrobial suture products, further fueling market growth.

Europe Antimicrobial Surgical Suture Market Company Profiles

Some of the key players operating in the market include TI Medical; Healthium Medtech Limited; Meril Life Sciences Pvt Ltd; Unilene; Johnson & Johnson; Futura Surgicare Pvt Ltd (Dolphin Sutures); Cencora, Inc. (AmerisourceBergen Corporation); Advanced MedTech Solutions Pvt. Ltd.; and Internacional Farmaceutica SA among others. These players are adopting various strategies such as expansion, product innovation, and mergers and acquisitions to provide innovative products to their consumers and increase their market share.

Europe Antimicrobial Surgical Suture Market Research Methodology :

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research The research process begins with comprehensive secondary research, utilizing both internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

Company websites , annual reports, financial statements, broker analyses, and investor presentations. Industry trade journals and other relevant publications. Government documents , statistical databases, and market reports. News articles , press releases, and webcasts specific to companies operating in the market. Note: All financial data included in the Company Profiles section has been standardized to USD. For companies reporting in other currencies, figures have been converted to USD using the relevant exchange rates for the corresponding year.

Primary Research The Insight Partners' conducts a significant number of primary interviews each year with industry stakeholders and experts to validate its data analysis, and gain valuable insights. These research interviews are designed to:

Validate and refine findings from secondary research. Enhance the expertise and market understanding of the analysis team. Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects. Primary research is conducted via email interactions and telephone interviews, encompassing various markets, categories, segments, and sub-segments across different regions. Participants typically include:

Industry stakeholders : Vice Presidents, business development managers, market intelligence managers, and national sales managers External experts : Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

3. Research Methodology

- 3.1 Secondary Research

- 3.2 Primary Research

- 3.2.1 Hypothesis formulation:

- 3.2.2 Macro-economic factor analysis:

- 3.2.3 Developing base number:

- 3.2.4 Data Triangulation:

- 3.2.5 Country level data:

4. Europe Antimicrobial Surgical Suture Market - Key Market Dynamics

- 4.1 Market Drivers:

- 4.1.1 Surging Prevalence of Surgical Site Infections

- 4.1.2 Increasing Cases of Chronic Wounds and Surgeries

- 4.2 Market Restraints

- 4.2.1 Non-invasive Alternatives to Stitches

- 4.3 Market Opportunities

- 4.3.1 Strategic Initiatives in Antimicrobial Surgical Suture

- 4.4 Future Trends

- 4.4.1 Smart Antimicrobial Sutures

- 4.5 Impact of Drivers and Restraints:

5. Antimicrobial Surgical Suture Market - Europe Analysis

- 5.1 Europe Antimicrobial Surgical Suture Market Revenue (US$ Million), 2021-2031

- 5.2 Europe Antimicrobial Surgical Suture Market Forecast Analysis

6. Europe Antimicrobial Surgical Suture Market Analysis - by Type

- 6.1 Triclosan Antimicrobial Suture

- 6.1.1 Overview

- 6.1.2 Triclosan Antimicrobial Suture: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 6.2 Chlorhexidine Antimicrobial Suture

- 6.2.1 Overview

- 6.2.2 Chlorhexidine Antimicrobial Suture: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

7. Europe Antimicrobial Surgical Suture Market Analysis - by Raw Materials

- 7.1 Polyglactin 910 Antimicrobial Suture

- 7.1.1 Overview

- 7.1.2 Polyglactin 910 Antimicrobial Suture: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 7.2 Poliglecaprone 25

- 7.2.1 Overview

- 7.2.2 Poliglecaprone 25: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 7.3 Polyglycolic Acid

- 7.3.1 Overview

- 7.3.2 Polyglycolic Acid: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

8. Europe Antimicrobial Surgical Suture Market Analysis - by Application

- 8.1 Cardiovascular Surgery

- 8.1.1 Overview

- 8.1.2 Cardiovascular Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 8.2 General Surgery

- 8.2.1 Overview

- 8.2.2 General Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 8.3 Ophthalmic Surgery

- 8.3.1 Overview

- 8.3.2 Ophthalmic Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 8.4 Gynaecological Surgery

- 8.4.1 Overview

- 8.4.2 Gynaecological Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 8.5 Orthopedic Surgery

- 8.5.1 Overview

- 8.5.2 Orthopedic Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 8.6 Plastic Surgery

- 8.6.1 Overview

- 8.6.2 Plastic Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 8.7 Veterinary Surgery

- 8.7.1 Overview

- 8.7.2 Veterinary Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 8.8 Dental Surgery

- 8.8.1 Overview

- 8.8.2 Dental Surgery: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 8.9 Others

- 8.9.1 Overview

- 8.9.2 Others: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

9. Europe Antimicrobial Surgical Suture Market Analysis - by End User

- 9.1 Hospitals

- 9.1.1 Overview

- 9.1.2 Hospitals: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 9.2 Ambulatory Surgical Centers

- 9.2.1 Overview

- 9.2.2 Ambulatory Surgical Centers: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 9.3 Others

- 9.3.1 Overview

- 9.3.2 Others: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

10. Europe Antimicrobial Surgical Suture Market - Country Analysis

- 10.1 Europe

- 10.1.1 Europe Antimicrobial Surgical Suture Market Overview

- 10.1.2 Europe Antimicrobial Surgical Suture Market - Breakdown, by Key Countries, 2023 and 2031 (%)

- 10.1.2.1 Germany: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 10.1.2.1.1 Germany: Europe Antimicrobial Surgical Suture Market Breakdown, by Type

- 10.1.2.1.2 Germany: Europe Antimicrobial Surgical Suture Market Breakdown, by Raw Materials

- 10.1.2.1.3 Germany: Europe Antimicrobial Surgical Suture Market Breakdown, by Application

- 10.1.2.1.4 Germany: Europe Antimicrobial Surgical Suture Market Breakdown, by End User

- 10.1.2.2 France: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 10.1.2.2.1 France: Europe Antimicrobial Surgical Suture Market Breakdown, by Type

- 10.1.2.2.2 France: Europe Antimicrobial Surgical Suture Market Breakdown, by Raw Materials

- 10.1.2.2.3 France: Europe Antimicrobial Surgical Suture Market Breakdown, by Application

- 10.1.2.2.4 France: Europe Antimicrobial Surgical Suture Market Breakdown, by End User

- 10.1.2.3 United Kingdom: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 10.1.2.3.1 United Kingdom: Europe Antimicrobial Surgical Suture Market Breakdown, by Type

- 10.1.2.3.2 United Kingdom: Europe Antimicrobial Surgical Suture Market Breakdown, by Raw Materials

- 10.1.2.3.3 United Kingdom: Europe Antimicrobial Surgical Suture Market Breakdown, by Application

- 10.1.2.3.4 United Kingdom: Europe Antimicrobial Surgical Suture Market Breakdown, by End User

- 10.1.2.4 Italy: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 10.1.2.4.1 Italy: Europe Antimicrobial Surgical Suture Market Breakdown, by Type

- 10.1.2.4.2 Italy: Europe Antimicrobial Surgical Suture Market Breakdown, by Raw Materials

- 10.1.2.4.3 Italy: Europe Antimicrobial Surgical Suture Market Breakdown, by Application

- 10.1.2.4.4 Italy: Europe Antimicrobial Surgical Suture Market Breakdown, by End User

- 10.1.2.5 Spain: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 10.1.2.5.1 Spain: Europe Antimicrobial Surgical Suture Market Breakdown, by Type

- 10.1.2.5.2 Spain: Europe Antimicrobial Surgical Suture Market Breakdown, by Raw Materials

- 10.1.2.5.3 Spain: Europe Antimicrobial Surgical Suture Market Breakdown, by Application

- 10.1.2.5.4 Spain: Europe Antimicrobial Surgical Suture Market Breakdown, by End User

- 10.1.2.6 Rest of Europe: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

- 10.1.2.6.1 Rest of Europe: Europe Antimicrobial Surgical Suture Market Breakdown, by Type

- 10.1.2.6.2 Rest of Europe: Europe Antimicrobial Surgical Suture Market Breakdown, by Raw Materials

- 10.1.2.6.3 Rest of Europe: Europe Antimicrobial Surgical Suture Market Breakdown, by Application

- 10.1.2.6.4 Rest of Europe: Europe Antimicrobial Surgical Suture Market Breakdown, by End User

- 10.1.2.1 Germany: Europe Antimicrobial Surgical Suture Market - Revenue and Forecast to 2031 (US$ Million)

11. Industry Landscape

- 11.1 Overview

- 11.2 Growth Strategies

- 11.2.1 Overview

- 11.3 Company Market Share Analysis (%), 2023

12. Company Profiles

- 12.1 TI Medical

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Healthium Medtech Limited

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Meril Life Sciences Pvt Ltd

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Unilene

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Johnson & Johnson

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 Futura Surgicare Pvt Ltd (Dolphin Sutures)

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Cencora, Inc. (AmerisourceBergen Corporation)

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 Advanced MedTech Solutions Pvt. Ltd.

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 Internacional Farmaceutica SA

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners

- 13.2 Glossary of Terms