|

|

市場調査レポート

商品コード

1562328

欧州のアセット健全性管理:2030年までの市場予測 - 地域分析 - サービスタイプ別、エンドユーザー別Europe Asset Integrity Management Market Forecast to 2030 - Regional Analysis - by Service Type and End User |

||||||

|

|||||||

|

|||||||

| 欧州のアセット健全性管理:2030年までの市場予測 - 地域分析 - サービスタイプ別、エンドユーザー別 |

|

出版日: 2024年07月04日

発行: The Insight Partners

ページ情報: 英文 103 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

欧州のアセット健全性管理市場は、2022年に8億8,615万米ドルと評価され、2030年には18億3,414万米ドルに達すると予測され、2022年から2030年までのCAGRは9.5%を記録すると予測されています。

厳しい政府の安全規制が欧州のアセット健全性管理市場を牽引

アセット健全性管理市場で事業を展開する複数の企業が、政府の規制要件に準拠したサービスを提供しています。現在、工業化の進展に伴い、さまざまな企業が業務全体の効率を向上させるための高度なソリューションを求めて活動しています。石油・ガス、電力、化学、鉱業などの業界では、アセット健全性管理・サービスが、製造作業中のリスクを最小限に抑える上で重要な役割を果たしています。これらの業界には、政府主導の環境規制がいくつか存在します。石油・ガス産業における規制は、環境保護、天然資源の保護、労働者と公衆の健康と安全の保護を主な目的として採用されています。石油・ガス産業は、排出ガスを発生させる様々な機器や作業に関与しています。また、装置オペレータは、排出制御装置のメンテナンスの難しさに直面しています。資産保全・信頼性管理ソフトウェアは、状態ベースのモニタリング、リスクベースの検査分析、安全保全管理、アセット健全性指標化から根本原因分析に至るまで、幅広いサービスを提供します。これらのサービスにより、製造オペレーションにリスクをもたらす可能性のある資産の故障を予測・特定することができます。また、生産的で効率的な操業に不可欠な、プロアクティブな検査とメンテナンスにもつながります。その結果、企業は設備の故障を回避するため、設備の保守・点検にアセット健全性管理・サービスを採用する傾向が強まっています。

このように、政府主導の厳格な環境規制は、複数の業界にわたってアセット健全性管理サービスの導入を後押ししており、これがアセット健全性管理市場を牽引しています。

欧州のアセット健全性管理市場の概要

欧州のアセット健全性管理ソフトウェア市場には、フランス、ドイツ、ロシア、イタリア、英国、その他欧州といった国々が含まれます。欧州の石油・ガスパイプラインは、この地域の50カ国に広がる高度に多様化したネットワークです。パイプラインには、国境を越えたライン、欧州を起点または終点とする国際パイプライン、石油・ガスやその他様々な物質の供給に使用される国内パイプラインが含まれます。石油・天然ガスは、これらのパイプラインを通じて欧州諸国に供給されます。ロシア連邦はEUに対する化石燃料の最大の供給国です。EUがさまざまな目的で消費する石油・天然ガスの約40%はロシア連邦から輸入されています。欧州における石油・ガスのサプライチェーンはまったく異なります。EUのサード・パーティ・アクセスは天然ガスのトランスミッションを規制しており、天然ガスは固定パイプラインで流通しています。そのため、アセット健全性管理の利用は、天然ガスパイプラインの所有者やオペレーターが中心となっています。さらに、この地域のいくつかの化学メーカーが、リスクベースの検査用アセット健全性・ソフトウェアを使用する契約を結んでいます。2021年6月現在、INEOSは、Anteaのリスクベース検査アセット健全性・ソフトウェアを使用する契約を締結しています。INEOSは、API 581準拠の認定RBIと包括的なIDMSモジュールを備えたAnteaプラットフォームが、同社の要件を満たす堅牢で信頼性の高いソリューションであると判断しました。アセット健全性管理ソフトウェアに対する需要の高まりが、市場の成長を後押ししています。さらに、欧州では複数の企業が合併・買収に乗り出しています。例えば、2024年1月、アセット健全性・ソフトウェアを提供するCenoscoは、Shellの健全性管理・システム(IMS)ソフトウェアを買収し、石油・ガスや化学セクターでより広範に利用できるようになった。このように、この地域におけるこのような買収は、アセット健全性管理ソフトウェア市場の成長を促進しました。この地域の企業は、インフラストラクチャーの耐久性とアップグレードを保証するために、正しく永続的な保護を保証する最も効果的な方法で使用されると予想される重要な投資を行っています。老朽化したインフラを適切に処理するためには、従来とは異なる管理アプローチが必要です。このことは、欧州の新しいインフラにかかるコストが既存のネットワークを維持するよりも高いという事実と相まって、欧州では主に既存のネットワークの寿命を維持・延長することで、健全で利用可能、かつ使い勝手の良い輸送インフラ網を持つことができるという点を浮き彫りにしています。

欧州のアセット健全性管理市場の収益と2030年までの予測(金額)

欧州のアセット健全性管理市場のセグメンテーション

欧州のアセット健全性管理市場は、サービスタイプ、エンドユーザー、国に区分されます。

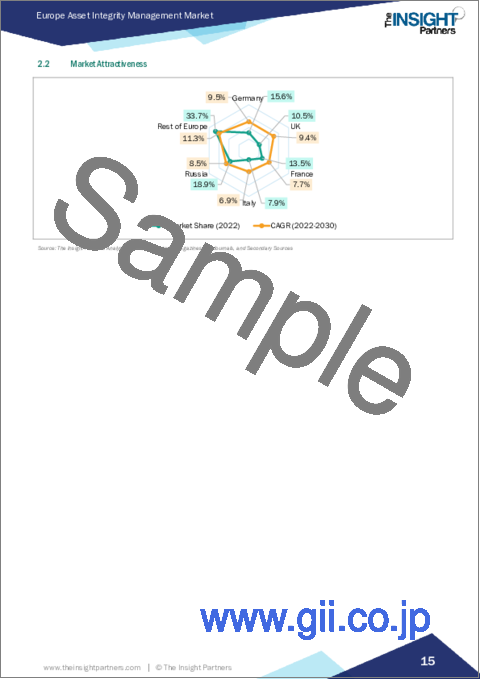

サービスタイプに基づき、欧州のアセット健全性管理市場は、非破壊検査、腐食管理、パイプラインインテグリティ管理、構造インテグリティ管理、リスクベース検査、その他に分類されます。2022年には、その他セグメントが最大の市場シェアを占めました。

エンドユーザー別では、欧州のアセット健全性管理市場は石油・ガス、電力、海洋、鉱業、航空宇宙、その他に分類されます。石油・ガスセグメントが2022年に最大の市場シェアを占めました。

国別では、欧州アセット健全性管理市場はドイツ、英国、フランス、イタリア、ロシア、その他欧州に区分されます。その他欧州が2022年の欧州アセット健全性管理市場シェアを独占しました。

SGS SA、Intertek Group Plc、Aker Solutions SA、Bureau Veritas SA、Fluor Corp、DNV Group AS、John Wood Group Plc、Rosen Group、TechnipFMC Plc、Oceaneering International Incは、欧州のアセット健全性管理市場で事業を展開している主要企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 欧州のアセット健全性管理市場情勢

- エコシステム分析

- バリューチェーンのベンダー一覧

第5章 欧州アセット健全性管理市場:主要市場力学

- 市場促進要因

- リスクベース産業における老朽資産の運用安全性へのニーズの高まり

- 政府の厳しい安全規制

- 市場プレイヤーによる成長戦略の採用増加

- 市場抑制要因

- 付加価値のないメンテナンスと不適切な操作に伴うコスト

- 市場機会

- 石油・ガス産業の拡大

- 原子力産業の成長

- 今後の動向

- デジタルツインとIIoTとアセット健全性管理ソフトウェアの統合

- 促進要因と抑制要因の影響

第6章 アセット健全性管理市場:欧州市場分析

- アセット健全性管理市場の収益、2020年~2030年

- アセット健全性管理市場の予測分析

第7章 欧州のアセット健全性管理市場分析:サービスタイプ別

- 非破壊検査(NDT)検査

- 腐食管理

- パイプラインの完全性管理

- 構造物の完全性管理

- リスクベース検査(RBI)

- その他

第8章 欧州のアセット健全性管理市場分析:エンドユーザー別

- 石油・ガス

- 電力

- 海洋

- 鉱業

- 航空宇宙

- その他

第9章 欧州のアセット健全性管理市場:国別分析

- 欧州市場概要

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア連邦

- その他欧州

- 欧州

第10章 競合情勢

- 主要プレーヤーによるヒートマップ分析

第11章 業界情勢

- 市場イニシアティブ

第12章 企業プロファイル

- SGS SA

- Intertek Group Plc

- Aker Solutions ASA

- Bureau Veritas SA

- Fluor Corp

- DNV Group AS

- John Wood Group Plc

- ROSEN Group

- TechnipFMC plc

- Oceaneering International Inc

第13章 付録

List Of Tables

- Table 1. Asset Integrity Management Market Segmentation

- Table 2. List of Vendors

- Table 3. Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Table 4. Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million) - by Service Type

- Table 5. Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million) - by End User

- Table 6. Europe: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Country

- Table 7. Germany: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 8. Germany: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 9. United Kingdom: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 10. United Kingdom: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 11. France: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 12. France: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 13. Italy: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 14. Italy: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 15. Russian Federation: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 16. Russian Federation: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 17. Rest of Europe: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 18. Rest of Europe: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 19. Heat Map Analysis by Key Players

- Table 20. List of Abbreviation

List Of Figures

- Figure 1. Asset Integrity Management Market Segmentation, by Country

- Figure 2. Ecosystem: Asset Integrity Management Market

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Asset Integrity Management Market Revenue (US$ Million), 2020-2030

- Figure 5. Asset Integrity Management Market Share (%) - by Service Type (2022 and 2030)

- Figure 6. Non-Destructive Testing (NDT) Inspection: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 7. Corrosion Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 8. Pipeline Integrity Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 9. Structural Integrity Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 10. Risk-Based Inspection (RBI): Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 11. Others: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 12. Asset Integrity Management Market Share (%) - by End User (2022 and 2030)

- Figure 13. Oil & Gas: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 14. Power: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 15. Marine: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 16. Mining: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 17. Aerospace: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 18. Others: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 19. Europe Asset Integrity Management Market, by Country - Revenue (2022) (US$ Million)

- Figure 20. Europe: Asset Integrity Management Market Breakdown, by Key Countries, 2022 and 2030 (%)

- Figure 21. Germany: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

- Figure 22. United Kingdom: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

- Figure 23. France: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

- Figure 24. Italy: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

- Figure 25. Russian Federation: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

- Figure 26. Rest of Europe: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

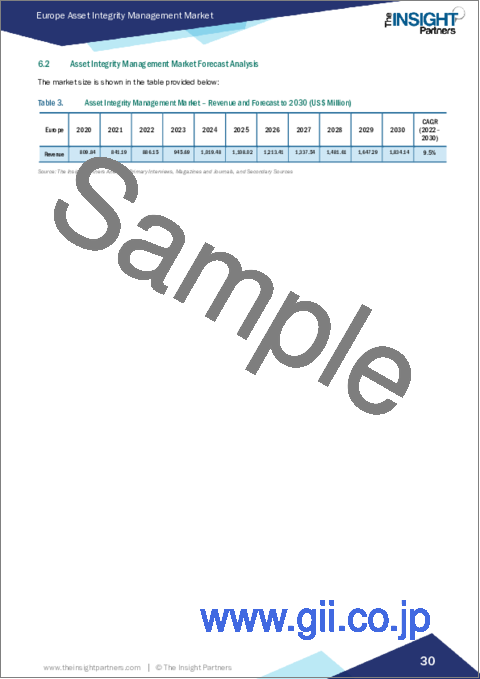

The Europe asset integrity management market was valued at US$ 886.15 million in 2022 and is expected to reach US$ 1,834.14 million by 2030; it is estimated to record a CAGR of 9.5% from 2022 to 2030.

Stringent Government Safety Regulations Drive Europe Asset Integrity Management Market

Several companies operating in the asset integrity management market offer services that comply with government regulatory requirements. Currently, with the increase in industrialization, a wide range of companies are operating for advanced solutions to improve the overall efficiency of operations. In industries such as oil & gas, power, chemical, mining, etc., asset integrity management services play a vital role in minimizing risk during manufacturing operations. These industries are associated with several government-led environmental regulations. The regulations in the oil & gas industry are employed for the major objectives of protecting the environment, conserving natural resources, and protecting workers & public health and safety. The oil & gas industry comprises the involvement of a wide range of equipment and operations that causes emissions. Also, equipment operators face difficulty in the maintenance of the emission control equipment. Asset integrity and reliability management software offers a wide variety of services ranging from condition-based monitoring, risk-based inspection analysis, safety integrity management, and asset health indexing to root cause analysis. These services enable the prediction and identification of the failure of assets that can pose a risk to the manufacturing operation. It also leads to proactive inspection and maintenance, which is crucial for productive and efficient operation. As a result, companies are more inclined toward the adoption of asset integrity management services for equipment maintenance and inspection to avoid equipment failure.

Thus, stringent government-led environmental regulations boost the implementation of asset integrity management services across several industries, which drives the asset integrity management market.

Europe Asset Integrity Management Market Overview

The Europe asset integrity management software market includes countries such as France, Germany, Russia, Italy, the UK, and the Rest of Europe. Oil and gas pipelines in Europe are a highly diversified network spread across 50 countries in this region. Pipelines include cross-border lines, international pipelines that originate or end in Europe, and domestic pipelines used for the supply of oil, gas, and various other materials. Oil and natural gas are distributed to the European nations through these pipelines. Russian Federation is the largest supplier of fossil fuels to the European Union. Approximately 40% of the oil and natural gas consumed by the European Union for various purposes is imported from the Russian Federation. The supply chain for oil and gas in Europe is quite different. Third-party access in the EU regulates the transmission of natural gas, and it is distributed on fixed pipelines. Therefore, the use of asset integrity management is majorly by the natural gas pipeline owners and operators. Moreover, several chemical manufacturers in the region are signing agreements to use risk-based inspection asset integrity software. As of June 2021, INEOS signed an agreement to use Antea's risk-based inspection asset integrity software. INEOS determined the Antea Platform, with its certified API 581-compliant RBI and comprehensive IDMS module, to be a robust, reliable solution that adheres to their requirements. The growing demand for asset integrity management software is propelling the growth of the market. Further, several players across Europe are indulging in mergers and acquisitions. For instance, in January 2024, Cenosco, which provides asset integrity software, acquired Shell's integrity management system (IMS) software, making the software available on a broader scale in oil & gas and chemical sectors. Thus, such acquisitions in the region propelled the growth of the asset integrity management software market. Companies across region is making significant investments that are anticipated to be used in the most effective way to guarantee correct and lasting protection to assure the endurance and upgrade of the infrastructure. In order to properly handle the aging infrastructures, a different management approach is needed; this, combined with the fact that the costs of new European infrastructures are more than maintaining the existing network, brings to the point that Europe can have a healthy, available, and usable transport infrastructure network, mainly by preserving and prolonging the lifetime of the existing network.

Europe Asset Integrity Management Market Revenue and Forecast to 2030 (US$ Million)

Europe Asset Integrity Management Market Segmentation

The Europe asset integrity management market is segmented into service type, end user, and country.

Based on service type, the Europe asset integrity management market is categorized into non-destructive testing inspection, corrosion management, pipeline integrity management, structural integrity management, risk-based inspection, and others. The others segment held the largest market share in 2022.

In terms of end user, the Europe asset integrity management market is categorized into oil & gas, power, marine, mining, aerospace, and others. The oil & gas segment held the largest market share in 2022.

By country, the Europe asset integrity management market is segmented into Germany, the UK, France, Italy, Russia, and the Rest of Europe. The Rest of Europe dominated the Europe asset integrity management market share in 2022.

SGS SA, Intertek Group Plc, Aker Solutions SA, Bureau Veritas SA, Fluor Corp, DNV Group AS, John Wood Group Plc, Rosen Group, TechnipFMC Plc, and Oceaneering International Inc are some of the leading companies operating in the Europe asset integrity management market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Europe Asset Integrity Management Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

- 4.2.1 List of Vendors in the Value Chain

5. Europe Asset Integrity Management Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Increase in Need for Operational Safety of Aging Assets in Risk-Based Industries

- 5.1.2 Stringent Government Safety Regulations

- 5.1.3 Rising Adoption of Growth Strategies by Market Players

- 5.2 Market Restraints

- 5.2.1 Cost Involved in Non-Value-Added Maintenance and Improper Operation

- 5.3 Market Opportunities

- 5.3.1 Expansion of Oil & Gas Industry

- 5.3.2 Growth in Nuclear Power Industry

- 5.4 Future Trend

- 5.4.1 Integration of Digital Twin and IIoT with Asset Integrity Management Software

- 5.5 Impact of Drivers and Restraints:

6. Asset Integrity Management Market - Europe Market Analysis

- 6.1 Asset Integrity Management Market Revenue (US$ Million), 2020-2030

- 6.2 Asset Integrity Management Market Forecast Analysis

7. Europe Asset Integrity Management Market Analysis - by Service Type

- 7.1 Non-Destructive Testing (NDT) Inspection

- 7.1.1 Overview

- 7.1.2 Non-Destructive Testing (NDT) Inspection: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2 Corrosion Management

- 7.2.1 Overview

- 7.2.2 Corrosion Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.3 Pipeline Integrity Management

- 7.3.1 Overview

- 7.3.2 Pipeline Integrity Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.4 Structural Integrity Management

- 7.4.1 Overview

- 7.4.2 Structural Integrity Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.5 Risk-Based Inspection (RBI)

- 7.5.1 Overview

- 7.5.2 Risk-Based Inspection (RBI): Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.6 Others

- 7.6.1 Overview

- 7.6.2 Others: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

8. Europe Asset Integrity Management Market Analysis - by End User

- 8.1 Oil & Gas

- 8.1.1 Overview

- 8.1.2 Oil & Gas: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2 Power

- 8.2.1 Overview

- 8.2.2 Power: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.3 Marine

- 8.3.1 Overview

- 8.3.2 Marine: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.4 Mining

- 8.4.1 Overview

- 8.4.2 Mining: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.5 Aerospace

- 8.5.1 Overview

- 8.5.2 Aerospace: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.6 Others

- 8.6.1 Overview

- 8.6.2 Others: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

9. Europe Asset Integrity Management Market - Country Analysis

- 9.1 Europe Market Overview

- 9.1.1 Europe: Asset Integrity Management Market - Revenue and Forecast Analysis - by Country

- 9.1.1.1 Europe: Asset Integrity Management Market - Revenue and Forecast Analysis - by Country

- 9.1.1.2 Germany: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.2.1 Germany: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.2.2 Germany: Asset Integrity Management Market Breakdown, by End User

- 9.1.1.3 United Kingdom: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.3.1 United Kingdom: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.3.2 United Kingdom: Asset Integrity Management Market Breakdown, by End User

- 9.1.1.4 France: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.4.1 France: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.4.2 France: Asset Integrity Management Market Breakdown, by End User

- 9.1.1.5 Italy: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.5.1 Italy: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.5.2 Italy: Asset Integrity Management Market Breakdown, by End User

- 9.1.1.6 Russian Federation: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.6.1 Russian Federation: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.6.2 Russian Federation: Asset Integrity Management Market Breakdown, by End User

- 9.1.1.7 Rest of Europe: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.7.1 Rest of Europe: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.7.2 Rest of Europe: Asset Integrity Management Market Breakdown, by End User

- 9.1.1 Europe: Asset Integrity Management Market - Revenue and Forecast Analysis - by Country

10. Competitive Landscape

- 10.1 Heat Map Analysis by Key Players

11. Industry Landscape

- 11.1 Overview

- 11.2 Market Initiative

12. Company Profiles

- 12.1 SGS SA

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Intertek Group Plc

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Aker Solutions ASA

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Bureau Veritas SA

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Fluor Corp

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 DNV Group AS

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 John Wood Group Plc

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 ROSEN Group

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 TechnipFMC plc

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 Oceaneering International Inc

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 SWOT Analysis

- 12.10.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners

- 13.2 Word Index