|

|

市場調査レポート

商品コード

1562316

アジア太平洋のアセット健全性管理:2030年までの市場予測 - 地域分析 - 地域別分析- サービスタイプ別、エンドユーザー別Asia Pacific Asset Integrity Management Market Forecast to 2030 - Regional Analysis - by Service Type and End User |

||||||

|

|||||||

|

|||||||

| アジア太平洋のアセット健全性管理:2030年までの市場予測 - 地域分析 - 地域別分析- サービスタイプ別、エンドユーザー別 |

|

出版日: 2024年07月04日

発行: The Insight Partners

ページ情報: 英文 102 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

アジア太平洋のアセット健全性管理市場は、2022年には7億4,613万米ドルと評価され、2030年には17億5,277万米ドルに達すると予測され、2022年から2030年までのCAGRは11.3%を記録すると予測されています。

石油・ガス産業の拡大がアジア太平洋のアセット健全性管理市場を押し上げる

幅広い産業でデジタルトランスフォーメーションが進む中、石油・ガス産業はこの産業革命と世界の経済成長において重要な役割を果たしています。この産業の進化を促す主な要因は、急速に増加する人口に対する電気、電力、自動車、航空機の需要の高さです。さらに、石油・ガス産業は、世界の消費エネルギー資源の中で最大のシェアを占めています。使用量の観点から、天然ガスは今後数年間で、最も急速に枯渇する化石燃料になると推定されます。世界的には、既存の石油埋蔵量の枯渇に起因するエネルギー需要の増加に対応するため、石油供給が急増すると予想されています。国際エネルギー機関(IEA)によると、2023年6月現在、世界の石油需要は2022年から2028年の間に6%増加し、石油化学産業と航空産業からの莫大な需要により、1億570万バレル/日に達すると予想されています。したがって、石油化学と航空セクターにおける石油・ガス需要の増加も、石油・ガス産業の成長を後押ししています。石油・ガス事業には、パイプや掘削装置など、手作業による保守を困難にする極めて過酷な環境にさらされる、多様で複雑な資産が関わっています。そのため、石油・ガス会社がすべての資産を効率的に管理することは課題であり、資産には厳しい規制があり、コストもかかります。そのため、カスタム・フィットの戦略と計画を提供し、故障の時期を推定・予測し、機器のライフサイクルを予測する資産管理サービスを選択する必要性が生じています。さらに、石油・ガス会社は、世界のエネルギー需要の増加に対応するため、より高い効率を達成する新技術を導入しています。同時に、多くの企業では、エンジニアリング部門やメンテナンス部門に、高い生産レベルを維持しながら、操業コスト、予算、労働力を削減することを強いています。したがって、石油・ガス会社にとっては、石油・ガスプラントからの有害汚染物質の排出に関する包括的な方針を確立し、安全保障とリスク違反をコスト効率よく管理するための実践が必要です。このように、石油・ガス産業の拡大と石油化学産業や航空産業からの石油・ガス需要の増加は、予測期間中に市場プレーヤーに大きな成長機会を提供すると期待されています。

アジア太平洋のアセット健全性管理市場概要

アジア太平洋は、インド、中国、韓国、日本を含む先進国で構成されています。国際通貨基金(IMF)によると、中国は世界中で急速に新興経済諸国となっています。同国は、航空宇宙、石油・ガス、エレクトロニクスなど数多くの産業の製造拠点でもあり、その生産活動には膨大なエネルギーと電力が必要とされます。これらの資産の生産性と寿命を維持するため、この地域の規制機関や機関は、市場全体の成長に大きく貢献している数多くのイニシアチブを取っています。例えば、2012年6月に設立された中国資産管理協会(AMAC)は、イノベーション、コミュニケーション、競合、専門性を活用して主要産業にサービスを提供することを主な目的としています。また、産業界と政府とのコミュニケーション・プラットフォームを提供することも目的としています。2022年12月、中国資産運用協会は、私募投資ファンドの登録・記録に関する措置とそれに付随するガイドラインの公開草案を発表しました。これらの草案の公表は、AMACの自主規制ルールシステムを改善し、将来的に後続の補完的ルールを策定するための基礎を築くことを目的としています。他の経済発展国の中で、インドは中国に次ぐ世界第3位のエネルギー消費国として認識されています。インドでは国内生産量が相対的に少なく、輸入量が多いため、原油を最適な方法で精製することが非常に重要になっています。さらに、この地域に存在する製油所の絶え間ない操業と、これらの製油所における多数の斬新なシステムや設備の導入により、環境持続可能性と操業施設の全体的なセキュリティを確保するため、アセット健全性管理サービスに対する需要が高まると予想されます。さらに、APACでは製造業のデジタル化が進んでおり、環境関連の規制を遵守するためのアセット健全性管理ソフトウェアに対する需要が生じています。アジア太平洋のさまざまな事業体が、施設のデジタル化を採用しています。オーストラリアでは、さまざまな市場プレーヤーが新しいソリューションの開拓に余念がないです。例えば、2021年7月、オーストラリアのApplus+はNext Advanced Solutionsと提携し、資産・施設完全性管理ソリューションの顧客に付加価値を与えることでポートフォリオを拡大しました。同社のアセット健全性は、非破壊検査(NII)ソフトウェアであるNIIPROによってサポートされています。NIIPROは、3D環境におけるNII要件の設定と管理に一貫したアプローチを提供します。さらに、Atteris Pty Ltd.やApplus+など、複数の大手企業が存在することも、アセット健全性管理ソフトウェア市場の成長を後押ししています。

アジア太平洋のアセット健全性管理市場の収益と2030年までの予測(金額)

アジア太平洋のアセット健全性管理市場のセグメンテーション

アジア太平洋のアセット健全性管理市場は、サービスタイプ、エンドユーザー、国別に区分されます。

サービスタイプ別に見ると、アジア太平洋のアセット健全性管理市場は、非破壊検査、腐食管理、パイプラインインテグリティ管理、構造インテグリティ管理、リスクベース検査、その他に分類されます。2022年には、非破壊検査セグメントが最大の市場シェアを占めました。

エンドユーザー別では、アジア太平洋のアセット健全性管理市場は石油・ガス、電力、海洋、鉱業、航空宇宙、その他に分類されます。石油・ガスセグメントが2022年に最大の市場シェアを占めました。

国別では、アジア太平洋のアセット健全性管理市場は、中国、日本、韓国、インド、オーストラリア、その他アジア太平洋に区分されます。2022年のアジア太平洋のアセット健全性管理市場シェアは中国が独占しました。

SGS SA、Intertek Group Plc、Aker Solutions SA、Bureau Veritas SA、Fluor Corp、DNV Group AS、John Wood Group Plc、Rosen Group、TechnipFMC Plc、Oceaneering International Incは、アジア太平洋のアセット健全性管理市場で事業を展開する主要企業の一部です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 アジア太平洋のアセット健全性管理市場情勢

- エコシステム分析

- バリューチェーンのベンダー一覧

第5章 アジア太平洋のアセット健全性管理市場:主要市場力学

- 市場促進要因

- リスクベース産業における老朽資産の運用安全性へのニーズの高まり

- 政府の厳しい安全規制

- 市場プレイヤーによる成長戦略の採用増加

- 市場抑制要因

- 付加価値のないメンテナンスと不適切な操作に伴うコスト

- 市場機会

- 石油・ガス産業の拡大

- 原子力産業の成長

- 今後の動向

- デジタルツインとIIoTとアセット健全性管理ソフトウェアの統合

- 促進要因と抑制要因の影響

第6章 アセット健全性管理市場:アジア太平洋市場分析

- アセット健全性管理市場の収益、2020年~2030年

- アセット健全性管理市場の予測分析

第7章 アジア太平洋のアセット健全性管理市場分析:サービスタイプ別

- 非破壊検査(NDT)検査

- 腐食管理

- パイプラインの完全性管理

- 構造物の完全性管理

- リスクベース検査(RBI)

- その他

第8章 アジア太平洋のアセット健全性管理市場分析:エンドユーザー別

- 石油・ガス

- 電力

- 海洋

- 鉱業

- 航空宇宙

- その他

第9章 アジア太平洋のアセット健全性管理市場:国別分析

- アジア太平洋市場の概要

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- その他アジア太平洋

- アジア太平洋

第10章 競合情勢

- 主要プレーヤーによるヒートマップ分析

第11章 業界情勢

- 市場イニシアティブ

第12章 企業プロファイル

- SGS SA

- Intertek Group Plc

- Aker Solutions ASA

- Bureau Veritas SA

- Fluor Corp

- DNV Group AS

- John Wood Group Plc

- ROSEN Group

- TechnipFMC plc

- Oceaneering International Inc

第13章 付録

List Of Tables

- Table 1. Asset Integrity Management Market Segmentation

- Table 2. List of Vendors

- Table 3. Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Table 4. Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million) - by Service Type

- Table 5. Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million) - by End User

- Table 6. Asia Pacific: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Country

- Table 7. China: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 8. China: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 9. Japan: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 10. Japan: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 11. South Korea: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 12. South Korea: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 13. India: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 14. India: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 15. Australia: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 16. Australia: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 17. Rest of Asia Pacific: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 18. Rest of Asia Pacific: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 19. Heat Map Analysis by Key Players

- Table 20. List of Abbreviation

List Of Figures

- Figure 1. Asset Integrity Management Market Segmentation, by Country

- Figure 2. Ecosystem: Asset Integrity Management Market

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Asset Integrity Management Market Revenue (US$ Million), 2020-2030

- Figure 5. Asset Integrity Management Market Share (%) - by Service Type (2022 and 2030)

- Figure 6. Non-Destructive Testing (NDT) Inspection: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 7. Corrosion Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 8. Pipeline Integrity Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 9. Structural Integrity Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 10. Risk-Based Inspection (RBI): Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 11. Others: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 12. Asset Integrity Management Market Share (%) - by End User (2022 and 2030)

- Figure 13. Oil & Gas: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 14. Power: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 15. Marine: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 16. Mining: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 17. Aerospace: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 18. Others: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 19. Asia Pacific Asset Integrity Management Market, by Country - Revenue (2022) (US$ Million)

- Figure 20. Asia Pacific: Asset Integrity Management Market Breakdown, by Key Countries, 2022 and 2030 (%)

- Figure 21. China: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

- Figure 22. Japan: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

- Figure 23. South Korea: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

- Figure 24. India: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

- Figure 25. Australia: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

- Figure 26. Rest of Asia Pacific: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

The Asia Pacific asset integrity management market was valued at US$ 746.13 million in 2022 and is expected to reach US$ 1,752.77 million by 2030; it is estimated to record a CAGR of 11.3% from 2022 to 2030.

Expansion of Oil & Gas Industry Boosts Asia Pacific Asset Integrity Management Market

With the rise in digital transformation in a wide range of industries, the oil & gas industry plays a key role in this industrial revolution and the economic growth of the world. The major factor driving the evolution of this industry is the high demand for electricity, power, automobiles, and aircraft to the rapidly growing population. Moreover, the oil & gas industry accounted for the largest share of global consumed energy resources. In terms of usage, natural gas is estimated to become the fastest-depleting fossil fuel in the coming years. Globally, oil supply is expected to increase rapidly in order to meet the rise in energy demand owing to the depletion of existing oil reserves. According to the International Energy Agency (IEA), as of June 2023, worldwide oil demand is anticipated to increase by 6% between 2022 and 2028 and reach 105.7 million barrels per day (mb/d) due to tremendous demand from the petrochemical and aviation industries. Hence, an increased demand for oil and gas in the petrochemicals and aviation sectors is also propelling the growth of the oil & gas industry. Oil & gas operations involve a diverse set of complex assets, such as pipes and drilling equipment, which are exposed to extremely harsh environments that make manual maintenance difficult. Hence, it is challenging for oil & gas companies to manage every asset efficiently, where assets are heavily regulated and expensive. Thus, it creates a need for companies to opt for asset management services that provide custom-fit strategies and plans, estimate the time of failure, and forecast equipment lifecycles. Moreover, oil and gas companies are deploying new technologies to attain greater efficiency to meet the world's increasing demand for energy. Simultaneously, many companies are forcing engineering and maintenance divisions to reduce operating costs, budget, and labor while maintaining high production levels. Hence, it is necessary for oil and gas companies to establish inclusive policies regarding discharge of harmful pollutant from oil & gas plant and practices to manage security and risk violations cost-effectively. Thus, the expansion of the oil & gas industry with an increase in demand for oil & gas from petrochemical and aviation industries is expected to provide substantial growth opportunities to the market players during the forecast period.

Asia Pacific Asset Integrity Management Market Overview

Asia Pacific consists of developed countries, including India, China, South Korea, and Japan. As per the International Monetary Fund (IMF), China is among the rapidly developing economies across the globe. The country is also a manufacturing center for numerous industries, such as aerospace, oil & gas, and electronics, whose production activities demand extensive energy and power. In order to maintain the productivity and lifespan of these assets, the local regulatory bodies and agencies across the region are taking numerous initiatives that have significantly contributed to the growth of the overall market. For instance, the Asset Management Association of China (AMAC), which was established in June 2012, has the principal objective of providing services to major industries by leveraging innovation, communication, competitiveness, and professionalism. The agency also aims to provide a communication platform between industries and the government. In December 2022, the Asset Management Association of China issued an exposure draft of the measures for the registration and record of private investment funds and their accompanying guidelines. The release of these drafts aims to improve the AMAC's self-regulatory rules system and lay a foundation for the formulation of subsequent complementary rules in the future. Among the other economically evolving economies, India is recognized as the third-largest energy consumer worldwide after China. As the domestic production in India is relatively lower and imports are higher, refining the crude oil commodities in the most optimum way becomes extremely important. Furthermore, the constant operations of the refineries present across the region and the incorporation of numerous novel systems and equipment in these refineries are expected to increase the demand for asset integrity management services in order to ensure environmental sustainability and overall security of the premises they operate in. Moreover, there is an increase in digitalization in manufacturing in APAC, which is creating a demand for asset integrity management software to comply with regulations related to the environment. Various entities across Asia Pacific are adopting digitalization at their facilities. Various market players in Australia are indulging in the development of new solutions. For example, in July 2021, Applus+ in Australia partnered with Next Advanced Solutions to expand portfolio by adding value to clients for asset and facility integrity management solutions. The company's asset integrity is supported by its non-intrusive inspection (NII) software, NIIPRO. NIIPRO offers a consistent approach to setting up and managing NII requirements in a 3D environment. Moreover, the presence of several major players, including Atteris Pty Ltd. and Applus+, propels the growth of the asset integrity management software market.

Asia Pacific Asset Integrity Management Market Revenue and Forecast to 2030 (US$ Million)

Asia Pacific Asset Integrity Management Market Segmentation

The Asia Pacific asset integrity management market is segmented into service type, end user, and country.

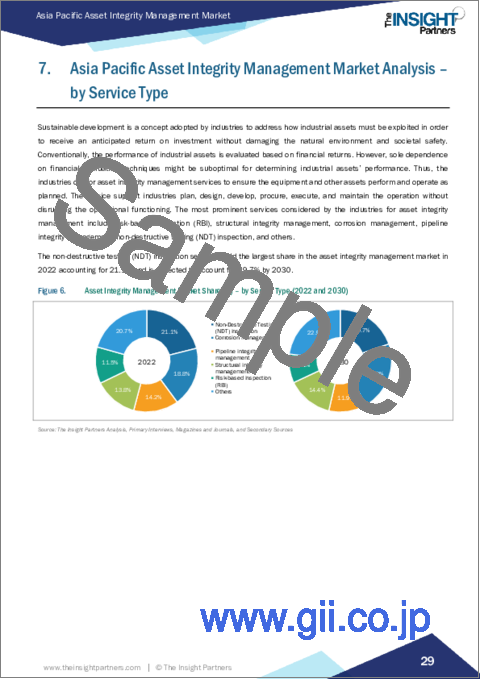

Based on service type, the Asia Pacific asset integrity management market is categorized into non-destructive testing inspection, corrosion management, pipeline integrity management, structural integrity management, risk-based inspection, and others. The non-destructive testing inspection segment held the largest market share in 2022.

In terms of end user, the Asia Pacific asset integrity management market is categorized into oil & gas, power, marine, mining, aerospace, and others. The oil & gas segment held the largest market share in 2022.

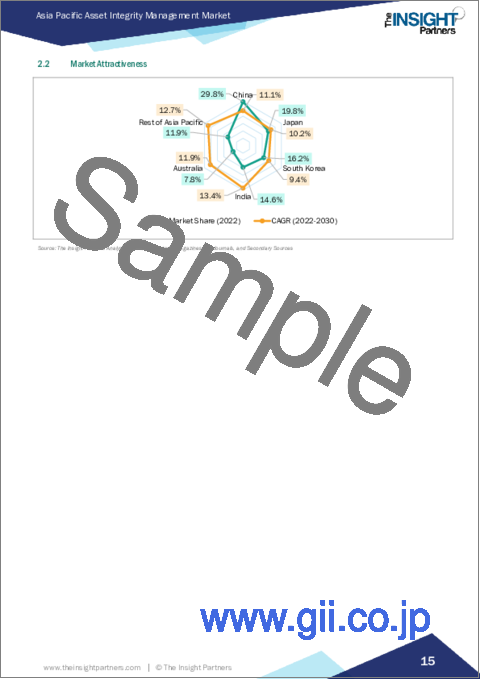

By country, the Asia Pacific asset integrity management market is segmented into China, Japan, South Korea, India, Australia, and the Rest of Asia Pacific. China dominated the Asia Pacific asset integrity management market share in 2022.

SGS SA, Intertek Group Plc, Aker Solutions SA, Bureau Veritas SA, Fluor Corp, DNV Group AS, John Wood Group Plc, Rosen Group, TechnipFMC Plc, and Oceaneering International Inc are some of the leading companies operating in the Asia Pacific asset integrity management market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Asia Pacific Asset Integrity Management Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

- 4.2.1 List of Vendors in the Value Chain

5. Asia Pacific Asset Integrity Management Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Increase in Need for Operational Safety of Aging Assets in Risk-Based Industries

- 5.1.2 Stringent Government Safety Regulations

- 5.1.3 Rising Adoption of Growth Strategies by Market Players

- 5.2 Market Restraints

- 5.2.1 Cost Involved in Non-Value-Added Maintenance and Improper Operation

- 5.3 Market Opportunities

- 5.3.1 Expansion of Oil & Gas Industry

- 5.3.2 Growth in Nuclear Power Industry

- 5.4 Future Trend

- 5.4.1 Integration of Digital Twin and IIoT with Asset Integrity Management Software

- 5.5 Impact of Drivers and Restraints:

6. Asset Integrity Management Market - Asia Pacific Market Analysis

- 6.1 Asset Integrity Management Market Revenue (US$ Million), 2020-2030

- 6.2 Asset Integrity Management Market Forecast Analysis

7. Asia Pacific Asset Integrity Management Market Analysis - by Service Type

- 7.1 Non-Destructive Testing (NDT) Inspection

- 7.1.1 Overview

- 7.1.2 Non-Destructive Testing (NDT) Inspection: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2 Corrosion Management

- 7.2.1 Overview

- 7.2.2 Corrosion Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.3 Pipeline Integrity Management

- 7.3.1 Overview

- 7.3.2 Pipeline Integrity Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.4 Structural Integrity Management

- 7.4.1 Overview

- 7.4.2 Structural Integrity Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.5 Risk-Based Inspection (RBI)

- 7.5.1 Overview

- 7.5.2 Risk-Based Inspection (RBI): Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.6 Others

- 7.6.1 Overview

- 7.6.2 Others: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

8. Asia Pacific Asset Integrity Management Market Analysis - by End User

- 8.1 Oil & Gas

- 8.1.1 Overview

- 8.1.2 Oil & Gas: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2 Power

- 8.2.1 Overview

- 8.2.2 Power: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.3 Marine

- 8.3.1 Overview

- 8.3.2 Marine: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.4 Mining

- 8.4.1 Overview

- 8.4.2 Mining: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.5 Aerospace

- 8.5.1 Overview

- 8.5.2 Aerospace: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.6 Others

- 8.6.1 Overview

- 8.6.2 Others: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

9. Asia Pacific Asset Integrity Management Market - Country Analysis

- 9.1 Asia Pacific Market Overview

- 9.1.1 Asia Pacific: Asset Integrity Management Market - Revenue and Forecast Analysis - by Country

- 9.1.1.1 Asia Pacific: Asset Integrity Management Market - Revenue and Forecast Analysis - by Country

- 9.1.1.2 China: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.2.1 China: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.2.2 China: Asset Integrity Management Market Breakdown, by End User

- 9.1.1.3 Japan: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.3.1 Japan: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.3.2 Japan: Asset Integrity Management Market Breakdown, by End User

- 9.1.1.4 South Korea: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.4.1 South Korea: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.4.2 South Korea: Asset Integrity Management Market Breakdown, by End User

- 9.1.1.5 India: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.5.1 India: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.5.2 India: Asset Integrity Management Market Breakdown, by End User

- 9.1.1.6 Australia: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.6.1 Australia: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.6.2 Australia: Asset Integrity Management Market Breakdown, by End User

- 9.1.1.7 Rest of Asia Pacific: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.7.1 Rest of Asia Pacific: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.7.2 Rest of Asia Pacific: Asset Integrity Management Market Breakdown, by End User

- 9.1.1 Asia Pacific: Asset Integrity Management Market - Revenue and Forecast Analysis - by Country

10. Competitive Landscape

- 10.1 Heat Map Analysis by Key Players

11. Industry Landscape

- 11.1 Overview

- 11.2 Market Initiative

12. Company Profiles

- 12.1 SGS SA

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Intertek Group Plc

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Aker Solutions ASA

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Bureau Veritas SA

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Fluor Corp

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 DNV Group AS

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 John Wood Group Plc

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 ROSEN Group

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 TechnipFMC plc

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 Oceaneering International Inc

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 SWOT Analysis

- 12.10.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners

- 13.2 Word Index