|

|

市場調査レポート

商品コード

1562315

北米のアセット健全性管理:2030年までの市場予測 - 地域分析 - サービスタイプ別、エンドユーザー別North America Asset Integrity Management Market Forecast to 2030 - Regional Analysis - by Service Type and End User |

||||||

|

|||||||

|

|||||||

| 北米のアセット健全性管理:2030年までの市場予測 - 地域分析 - サービスタイプ別、エンドユーザー別 |

|

出版日: 2024年07月04日

発行: The Insight Partners

ページ情報: 英文 96 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

北米のアセット健全性管理市場は、2022年に11億2,852万米ドルと評価され、2030年には19億9,541万米ドルに達すると予測され、2022年から2030年までのCAGRは7.4%を記録すると予測されています。

リスクベース産業における老朽資産の運用安全性へのニーズの高まりが北米のアセット健全性管理市場を後押し

アセット健全性管理・ソフトウェアは、アセットがその機能を効果的に発揮できるよう保護するとともに、収益性を高めるために企業の資産を管理します。アセット健全性管理・ソフトウェアは、設計、検査、メンテナンス、運用など、インフラや設備のインテグリティに大きな影響を与えるさまざまなサービスを提供します。また、監査、検査、全体的な品質プロセス、資産の効率的な完全性管理のためのその他のツールも提供します。石油化学、石油・ガス、再生可能エネルギー、電力、インフラストラクチャーなどの業界は、環境と安全への懸念を満たしつつ生産性の向上を達成するために、これらのサービスを選択しています。これらの産業は、リスクベースかつ資産ベースであるため、資産の保守・点検は不可欠です。石油・ガス産業では、バリュー・チェーン全体を通じて、海底機器、プラットフォームのトップサイド、構造物、ガス処理プラント、パイプライン、精製所、コンプレッサー、ガス配給ネットワークなどの資産の完全性によって、パフォーマンスとオペレーショナル・リスク・レベルが左右されます。石油・ガス、鉱業、電力産業では、資産の運用効率が非常に重要であるため、生産性を最大化するためには、これらの資産を定期的にメンテナンスすることが重要です。

化学薬品や石油・ガス製品は腐食性や引火性があるため、全体的な運用効率と安全のために、設備の継続的な点検とメンテナンスが必要です。アセット健全性管理・サービスは、機器の信頼性、生産性、安全性を向上させ、持続可能な方法で質の高いパフォーマンスを実現します。また、このシステムは、プラントの信頼性を向上させることで、設備全体の修理コストを削減します。これは、企業の資産を維持するための費用対効果が高く信頼性の高いソリューションであり、老朽化した資産の寿命を確実に延ばし、操業の安全性を向上させるのに役立ちます。パフォーマンスとオペレーショナル・リスクを管理するために、世界中の様々な市場プレーヤーがアセット健全性管理・ソフトウェアを提供しています。例えば、DNV Group ASは、Synergi資産完全性ソフトウェアスイートを提供しており、石油・ガスのようなリスクベースの産業において、効果的なリスクベースの完全性管理をサポートするコアプラットフォームを提供しています。このように、リスクベース産業における老朽化した資産の運転上の安全性の必要性が、アセット健全性管理市場を牽引しています。

北米のアセット健全性管理市場の概要

北米には米国、カナダ、メキシコなどが含まれます。この地域の3カ国はいずれも、ここ数年の間にアセット健全性管理サービスの採用が増加しています。石油・ガス、化学、電力、天然資源産業は、独自のインフラに依存して事業を運営しているが、このインフラは急速に老朽化しており、故障のリスクが高まっています。この分野の企業はインフラ危機に直面しており、故障のリスクを生む10年前の構造で作業しています。さらに北米は、非在来型陸上石油の新規生産能力を提供する最大の地域であることに変わりはないと予想されます。石油・ガス業界では、成熟油田の大半のインフラが老朽化しており、これが腐食、スケーリング、坑井設備の故障につながり、その他の坑井の健全性問題を引き起こしています。こうした問題は、企業や公益事業の操業リスクを増大させ、インフラのアップグレードプロジェクトにより多くの資本を必要とします。北米の石油・ガス産業は、環境を保護し、文化資源を保護し、労働者の健康と安全を守るために、いくつかの政府の政策と政策に従う必要があります。この地域の上流・中流インフラは膨大です。米国は石油・天然ガスの最大の生産国で、大量の石油の探鉱、精製、輸送を行っています。また、米国の石油掘削業者は新たな石油リグを増設し、米国の石油リグ総数は862基となった。米国の石油・ガスパイプラインの総延長は250万キロメートル以上であるのに対し、カナダのパイプラインの総延長は80万キロメートル程度です。大規模で老朽化したインフラの結果、北米が石油・ガス資産の完全性管理市場を独占する可能性が高いです。さらに、米国には世界で最も古い発電システムがいくつかあります。米国は世界有数のエネルギー生産国であり、水圧破砕と水平掘削は、同国のエネルギー生産増加に貢献した技術です。このように、厳しい政府規制と巨大なガスパイプラインネットワークの存在は、予測期間中、アセット健全性管理ソフトウェア市場のプレーヤーに多大な成長機会をもたらすと期待されています。

北米のアセット健全性管理市場の収益と2030年までの予測(金額)

北米のアセット健全性管理市場のセグメンテーション

北米のアセット健全性管理市場は、サービスタイプ、エンドユーザー、国別に区分されます。

サービスタイプ別に見ると、北米のアセット健全性管理市場は、非破壊検査、腐食管理、パイプラインインテグリティ管理、構造インテグリティ管理、リスクベース検査、その他に分類されます。2022年には、非破壊検査セグメントが最大の市場シェアを占めています。

エンドユーザー別では、北米のアセット健全性管理市場は石油・ガス、電力、海洋、鉱業、航空宇宙、その他に分類されます。石油・ガスセグメントが2022年に最大の市場シェアを占めました。

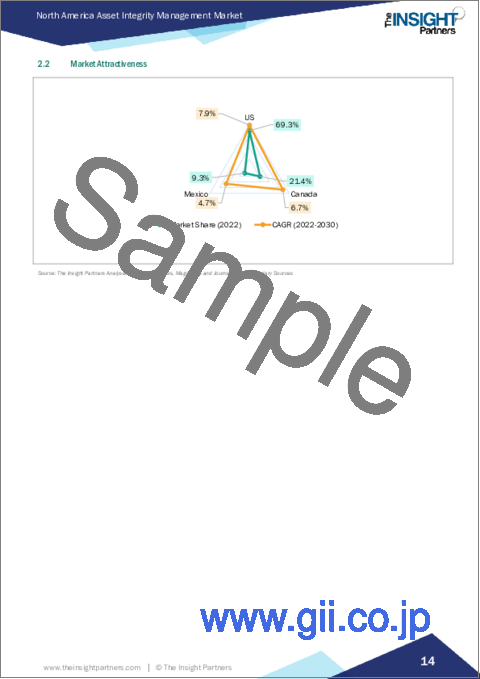

国別では、北米のアセット健全性管理市場は米国、カナダ、メキシコに区分されます。2022年の北米アセット健全性管理市場シェアは米国が独占。

SGS SA、Intertek Group Plc、Aker Solutions SA、Bureau Veritas SA、Fluor Corp、DNV Group AS、John Wood Group Plc、Rosen Group、TechnipFMC Plc、Oceaneering International Incは、北米のアセット健全性管理市場で事業を展開している主要企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 北米のアセット健全性管理市場情勢

- エコシステム分析

- バリューチェーンのベンダー一覧

第5章 北米のアセット健全性管理市場:主要市場力学

- 市場促進要因

- リスクベース産業における老朽資産の運用安全性へのニーズの高まり

- 政府の厳しい安全規制

- 市場プレイヤーによる成長戦略の採用増加

- 市場抑制要因

- 付加価値のないメンテナンスと不適切な操作に伴うコスト

- 市場機会

- 石油・ガス産業の拡大

- 原子力産業の成長

- 今後の動向

- デジタルツインとIIoTとソフトウェアの統合

- 促進要因と抑制要因の影響

第6章 アセット健全性管理市場:北米市場分析

- アセット健全性管理市場の収益、2020年~2030年

- アセット健全性管理市場の予測分析

第7章 北米のアセット健全性管理市場分析:サービスタイプ別

- 非破壊検査(NDT)検査

- 腐食管理

- パイプラインの完全性管理

- 構造物の完全性管理

- リスクベース検査(RBI)

- その他

第8章 北米のアセット健全性管理市場分析:エンドユーザー別

- 石油・ガス

- 電力

- 海洋

- 鉱業

- 航空宇宙

- その他

第9章 北米のアセット健全性管理市場:国別分析

- 北米市場概要

- 北米

- 米国

- カナダ

- メキシコ

- 北米

第10章 競合情勢

- 主要プレーヤーによるヒートマップ分析

第11章 業界情勢

- 市場イニシアティブ

第12章 企業プロファイル

- SGS SA

- Intertek Group Plc

- Aker Solutions ASA

- Bureau Veritas SA

- Fluor Corp

- DNV Group AS

- John Wood Group Plc

- ROSEN Group

- TechnipFMC plc

- Oceaneering International Inc

第13章 付録

List Of Tables

- Table 1. Asset Integrity Management Market Segmentation

- Table 2. List of Vendors

- Table 3. Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Table 4. Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million) - by Service Type

- Table 5. Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million) - by End User

- Table 6. North America: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Country

- Table 7. United States: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 8. United States: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 9. Canada: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 10. Canada: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 11. Mexico: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by Service Type

- Table 12. Mexico: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million) - by End User

- Table 13. Heat Map Analysis by Key Players

- Table 14. List of Abbreviation

List Of Figures

- Figure 1. Asset Integrity Management Market Segmentation, by Country

- Figure 2. Ecosystem: Asset Integrity Management Market

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Asset Integrity Management Market Revenue (US$ Million), 2020-2030

- Figure 5. Asset Integrity Management Market Share (%) - by Service Type (2022 and 2030)

- Figure 6. Non-Destructive Testing (NDT) Inspection: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 7. Corrosion Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 8. Pipeline Integrity Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 9. Structural Integrity Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 10. Risk-Based Inspection (RBI): Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 11. Others: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 12. Asset Integrity Management Market Share (%) - by End User (2022 and 2030)

- Figure 13. Oil & Gas: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 14. Power: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 15. Marine: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 16. Mining: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 17. Aerospace: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 18. Others: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 19. North America Asset Integrity Management Market, by Country - Revenue (2022) (US$ Million)

- Figure 20. North America: Asset Integrity Management Market Breakdown, by Key Countries, 2022 and 2030 (%)

- Figure 21. United States: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

- Figure 22. Canada: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

- Figure 23. Mexico: Asset Integrity Management Market - Revenue and Forecast to 2030(US$ Million)

The North America asset integrity management market was valued at US$ 1,128.52 million in 2022 and is expected to reach US$ 1,995.41 million by 2030; it is estimated to record a CAGR of 7.4% from 2022 to 2030.

Increase in Need for Operational Safety of Aging Assets in Risk-Based Industries Fuel North America Asset Integrity Management Market

Asset integrity management software protects the capability of an asset to perform its functions effectively, as well as manages corporate assets in order to gain profitability. Asset integrity management software offers various services, including design, inspection, maintenance, and operations, which highly impact the integrity of infrastructure and equipment. It also provides auditing, inspections, overall quality processes, and other tools for the effective integrity management of assets. Industries such as petrochemicals, oil & gas, renewable energy, power, and infrastructure opt for these services in order to achieve increased productivity while meeting environmental and safety concerns. These industries are risk-based and highly asset-based; hence, maintenance and inspection of such assets are essential. In oil & gas industry, performance and operational risk levels are dependent upon the integrity of the assets, such as subsea equipment, platform topsides, structures, gas processing plants, pipelines, refineries, compressors, and gas distribution networks, throughout the value chain. Operational efficiency for assets is highly necessary in oil & gas, mining, and power industries; thus, regular maintenance of these assets is important to gain maximum productivity.

Chemicals and oil & gas products are corrosive and flammable in nature and require continuous inspection and maintenance of the equipment for overall operational efficiency and safety. The asset integrity management services ensure improved reliability, productivity, and safety of the equipment to achieve quality performance in a sustainable manner. Also, this system reduces the overall repair cost of the equipment with increased plant reliability. It is a cost-effective and reliable solution to maintain the company's assets, which helps extend the lifetime of aging assets reliably and improve operational safety. Various market players across the globe are providing asset integrity management software in order to manage performance and operational risk. For example, DNV Group AS provides the Synergi asset integrity software suite, which offers a core platform to support effective risk-based integrity management in risk-based industries such as oil & gas. Thus, the need for operational safety of aging assets in risk-based industries drives the asset integrity management market.

North America Asset Integrity Management Market Overview

North America includes countries such as the US, Canada, and Mexico. All three countries in the area are witnessing increased adoption of asset integrity management services during the last few years. Oil & gas, chemical, power, and natural resource industries rely on proprietary infrastructure to run their operation, and this infrastructure is rapidly aging, which increases the risk of failure. Companies in this sector are facing an infrastructure crisis and working in decade-old structures that create a risk of breakdown. Further, North America is expected to remain the largest regional provider of new unconventional onshore oil production capacity. In the oil & gas industry, the infrastructure of the majority of mature oil fields is old, which leads to corrosion, scaling, and failed well equipment and causes other well-integrity problems. These issues increase the operational risk for companies and utilities, requiring more capital in infrastructure upgrade projects. The oil & gas industry in North America needs to follow several government policies and regulations to protect the environment, preserve cultural resources, and protect workers' health and safety. The region's upstream and midstream infrastructure is enormous. The US is the largest producer of oil and natural gas, which involves the exploration, refining, and transportation of a large quantity of oil. Also, US drillers added new oil rigs, which brought the total number of oil rigs in the US to 862. The US has over 2.5 million kilometers of oil and gas pipelines, whereas Canada has ~800,000 kilometers of pipeline. As a result of its massive and aging infrastructure, North America is likely to dominate the oil and gas asset integrity management market. Further, the US has a few of the oldest power generation systems in the world. The US is the world's leading energy producer, and hydraulic fracturing and horizontal drilling are technologies that helped increase energy production in this country. Thus, strict government regulations and the presence of a huge gas pipeline network are expected to generate a tremendous growth opportunity for asset integrity management software market players during the forecast period.

North America Asset Integrity Management Market Revenue and Forecast to 2030 (US$ Million)

North America Asset Integrity Management Market Segmentation

The North America asset integrity management market is segmented into service type, end user, and country.

Based on service type, the North America asset integrity management market is categorized into non-destructive testing inspection, corrosion management, pipeline integrity management, structural integrity management, risk-based inspection, and others. The non-destructive testing inspection segment held the largest market share in 2022.

In terms of end user, the North America asset integrity management market is categorized into oil & gas, power, marine, mining, aerospace, and others. The oil & gas segment held the largest market share in 2022.

By country, the North America asset integrity management market is segmented into the US, Canada, and Mexico. The US dominated the North America asset integrity management market share in 2022.

SGS SA, Intertek Group Plc, Aker Solutions SA, Bureau Veritas SA, Fluor Corp, DNV Group AS, John Wood Group Plc, Rosen Group, TechnipFMC Plc, and Oceaneering International Inc are some of the leading companies operating in the North America asset integrity management market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. North America Asset Integrity Management Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

- 4.2.1 List of Vendors in the Value Chain

5. North America Asset Integrity Management Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Increase in Need for Operational Safety of Aging Assets in Risk-Based Industries

- 5.1.2 Stringent Government Safety Regulations

- 5.1.3 Rising Adoption of Growth Strategies by Market Players

- 5.2 Market Restraints

- 5.2.1 Cost Involved in Non-Value-Added Maintenance and Improper Operation

- 5.3 Market Opportunities

- 5.3.1 Expansion of Oil & Gas Industry

- 5.3.2 Growth in Nuclear Power Industry

- 5.4 Future Trend

- 5.4.1 Integration of Digital Twin and IIoT with Asset Integrity Management Software

- 5.5 Impact of Drivers and Restraints:

6. Asset Integrity Management Market - North America Market Analysis

- 6.1 Asset Integrity Management Market Revenue (US$ Million), 2020-2030

- 6.2 Asset Integrity Management Market Forecast Analysis

7. North America Asset Integrity Management Market Analysis - by Service Type

- 7.1 Non-Destructive Testing (NDT) Inspection

- 7.1.1 Overview

- 7.1.2 Non-Destructive Testing (NDT) Inspection: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.2 Corrosion Management

- 7.2.1 Overview

- 7.2.2 Corrosion Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.3 Pipeline Integrity Management

- 7.3.1 Overview

- 7.3.2 Pipeline Integrity Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.4 Structural Integrity Management

- 7.4.1 Overview

- 7.4.2 Structural Integrity Management: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.5 Risk-Based Inspection (RBI)

- 7.5.1 Overview

- 7.5.2 Risk-Based Inspection (RBI): Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 7.6 Others

- 7.6.1 Overview

- 7.6.2 Others: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

8. North America Asset Integrity Management Market Analysis - by End User

- 8.1 Oil & Gas

- 8.1.1 Overview

- 8.1.2 Oil & Gas: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.2 Power

- 8.2.1 Overview

- 8.2.2 Power: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.3 Marine

- 8.3.1 Overview

- 8.3.2 Marine: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.4 Mining

- 8.4.1 Overview

- 8.4.2 Mining: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.5 Aerospace

- 8.5.1 Overview

- 8.5.2 Aerospace: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 8.6 Others

- 8.6.1 Overview

- 8.6.2 Others: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

9. North America Asset Integrity Management Market - Country Analysis

- 9.1 North America Market Overview

- 9.1.1 North America: Asset Integrity Management Market - Revenue and Forecast Analysis - by Country

- 9.1.1.1 North America: Asset Integrity Management Market - Revenue and Forecast Analysis - by Country

- 9.1.1.2 United States: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.2.1 United States: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.2.2 United States: Asset Integrity Management Market Breakdown, by End User

- 9.1.1.3 Canada: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.3.1 Canada: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.3.2 Canada: Asset Integrity Management Market Breakdown, by End User

- 9.1.1.4 Mexico: Asset Integrity Management Market - Revenue and Forecast to 2030 (US$ Million)

- 9.1.1.4.1 Mexico: Asset Integrity Management Market Breakdown, by Service Type

- 9.1.1.4.2 Mexico: Asset Integrity Management Market Breakdown, by End User

- 9.1.1 North America: Asset Integrity Management Market - Revenue and Forecast Analysis - by Country

10. Competitive Landscape

- 10.1 Heat Map Analysis by Key Players

11. Industry Landscape

- 11.1 Overview

- 11.2 Market Initiative

12. Company Profiles

- 12.1 SGS SA

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Intertek Group Plc

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Aker Solutions ASA

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Bureau Veritas SA

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Fluor Corp

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 DNV Group AS

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 John Wood Group Plc

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 ROSEN Group

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 TechnipFMC plc

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 Oceaneering International Inc

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 SWOT Analysis

- 12.10.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners

- 13.2 Word Index