|

|

市場調査レポート

商品コード

1533100

欧州の風力タービン用複合材料:2030年市場予測- 地域別分析- 繊維タイプ、樹脂タイプ、技術、用途別Europe Wind Turbine Composites Market Forecast to 2030 - Regional Analysis - by Fiber Type, Resin Type, Technology, and Application |

||||||

|

|||||||

|

|||||||

| 欧州の風力タービン用複合材料:2030年市場予測- 地域別分析- 繊維タイプ、樹脂タイプ、技術、用途別 |

|

出版日: 2024年06月04日

発行: The Insight Partners

ページ情報: 英文 114 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

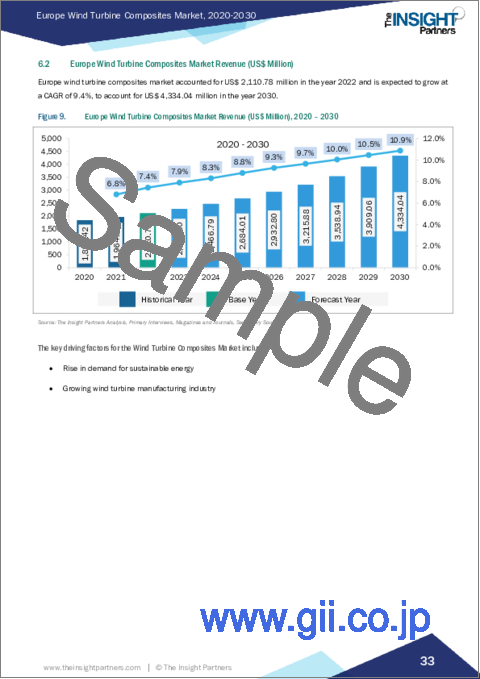

欧州の風力タービン用複合材料市場は、2022年に21億1,078万米ドルと評価され、2030年には43億3,404万米ドルに達すると予測され、2022年から2030年までのCAGRは9.4%で成長すると予測されています。

風力タービンの設置率増加が欧州の風力タービン用複合材料市場を牽引

風力発電は、燃料を燃やしたり大気を汚染したりすることなく電力を供給する、クリーンで再生可能なエネルギー源と考えられています。風力エネルギーは化石燃料への依存を減らすのに役立ちます。そのため、さまざまな国で風力エネルギーへの関心が高まっており、その結果、風力発電の設備容量が急速に増加しています。2020年、陸上風力発電所の新規設置量は86.9GWに達し、洋上風力発電所は6.1GWに達し、2020年は陸上と洋上の新規風力発電所設置量でそれぞれ史上最高と史上2番目に高い年となった。欧州では2022年に陸上風力発電の導入量が過去最高を記録し、この地域の新規風力発電容量増加のシェアを2021年の19%から2022年には25%に押し上げました。欧州では、2022年の新規風力発電設備は1,910万kW(陸上1,670万kW、洋上250万kW)に達しました。さらに、2022年の欧州の風力新設の87%は陸上風力でした。ドイツ、スウェーデン、フィンランドが陸上風力発電所の建設に大きく貢献しました。洋上設置の約半分は英国でした。また、フランスは初の大型洋上風力発電所を設置しました。風力タービンの複合材料は、ブレードやナセルなどの機器の製造に利用される材料です。これらの材料には、弾力性と高い引張強度をもたらす繊維とマトリックスが含まれます。ガラス繊維強化プラスチック(GRP)は、風力タービン産業で最も一般的に使用されている複合材料です。風力タービン用複合材料の需要が伸びているのは、再生可能エネルギーに対する政府の注目が高まっているため、洋上および陸上プロジェクトで新しい風力タービンが設置されているためです。風力発電所の容量が増加し、世界中で風力発電所プロジェクトが急増しているため、風力タービンのニーズが高まっており、風力タービン用複合材料の需要に拍車をかけています。

欧州の風力タービン用複合材料市場概要

欧州の風力タービン用複合材料市場は、ドイツ、フランス、イタリア、英国、ロシア、その他欧州(スウェーデン、フィンランドなど)に区分されます。この地域のさまざまな国が、持続可能性の目標を達成するために技術力を活用しています。以下の図に見られるように、2022年の欧州の新規風力発電設備は合計1,910万kW(陸上1,670万kW、洋上250万kW)で、2021年比で4%の増加を記録しました。2022年に最も多くの陸上風力プロジェクトを建設したのはドイツ、スウェーデン、フィンランドでした。英国は洋上設置のほぼ半分を占めました。さらに、スウェーデンは風力エネルギー部門に多額の投資を行っています。2022年12月に発表されたニュースによると、北欧投資銀行(NIB)とKolvallen Vind ABは、スウェーデンに277MWの風力発電所を建設するため、5,015万ユーロ(5,482万米ドル)の融資契約を締結しました。WindEuropeによると、欧州は2021年に新規風力発電所に410億ユーロ(450億7,000万米ドル)を投資し、これには25GWの新規容量への融資が含まれています。さらに、2022年の新規風力発電所への投資額は170億ユーロ(186億9,000万米ドル)と、2021年の4,847万米ドルから減少し、2009年以降で最低の投資額となった。欧州の風力産業は、投入コストの上昇とサプライチェーンの混乱に苦しんでいます。さらに、ロシア・ウクライナ戦争は、原材料コストの変動と国際輸送に関連する課題を増幅させました。その結果、欧州における風力タービンの生産コストは過去2年間で最大40%上昇しました。このため、風力エネルギー分野への投資は2022年に欧州全域で減少し、同地域の風力タービン用複合材料市場の足かせとなった。

欧州の風力タービン用複合材料市場の収益と2030年までの予測(金額)

欧州の風力タービン用複合材料市場のセグメンテーション

欧州の風力タービン用複合材料市場は、繊維タイプ、樹脂タイプ、技術、用途、国によって区分されます。

繊維タイプに基づき、欧州の風力タービン用複合材料市場は炭素繊維複合材料、ガラス繊維複合材料、その他に区分されます。2022年にはガラス繊維複合材料セグメントがより大きなシェアを占めています。

樹脂タイプでは、欧州の風力タービン用複合材料市場はポリエステル、エポキシ、ポリウレタン、ビニルエステル、その他に区分されます。2022年にはエポキシセグメントが最大のシェアを占めています。

技術別では、欧州の風力タービン用複合材料市場は、樹脂注入、プリプレグ、レイアップ、その他に区分されます。樹脂注入セグメントが2022年に最大のシェアを占めました。

用途別では、欧州の風力タービン用複合材料市場はブレードとナセルに二分されます。ブレードセグメントが2022年に大きなシェアを占めました。

国別では、欧州の風力タービン用複合材料市場はドイツ、フランス、イタリア、英国、ロシア、その他欧州に区分されます。その他欧州が2022年の欧州の風力タービン用複合材料市場を独占しました。

Avient Corp、Toray Industries Inc、SGL Carbon SE、Owens Corning、Gurit Holding AG、Covestro AG、Hexion Inc、EPSILON Composite SA、Exel Composites Oyj、Hexcel Corpは、欧州の風力タービン用複合材料市場で事業を展開している大手企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 欧州の風力タービン用複合材料市場情勢

- ポーターズ分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- エコシステム分析

- 原材料サプライヤー

- 風力タービン用複合材料メーカー

- ディストリビューター/サプライヤー

- エンドユーザーと相手先ブランドメーカー

- バリューチェーンのベンダー一覧

第5章 欧州の風力タービン用複合材料市場:主要市場力学

- 市場促進要因

- 風力タービン設置容量の増加

- 風力タービンブレードの長さ増加

- 市場抑制要因

- 風力エネルギー産業の政府補助金依存度の高さ

- 市場機会

- 風力エネルギー部門発展のための政府の取り組み

- 今後の動向

- 天然繊維強化ポリマー(NFRP)複合材料の採用

- 影響分析

第6章 風力タービン用複合材料の欧州市場分析

- 欧州の風力タービン用複合材料の市場規模

- 欧州の風力タービン用複合材料の市場収益

- 欧州の風力タービン用複合材料の市場予測と分析

第7章 欧州の風力タービン用複合材料市場分析:繊維タイプ

- 炭素繊維複合材料

- ガラス繊維複合材料

- その他

第8章 欧州の風力タービン用複合材料市場分析:樹脂タイプ

- ポリエステル

- エポキシ

- ポリウレタン

- ビニルエステル

- その他

第9章 欧州の風力タービン用複合材料の市場分析:技術

- 樹脂注入

- プリプレグ

- レイアップ

- その他

第10章 欧州の風力タービン用複合材料市場分析:用途

- ブレード

- ナセル

第11章 欧州の風力タービン用複合材料市場:国別分析

- 欧州

- ドイツ

- フランス

- イタリア

- 英国

- ロシア

- その他欧州

第12章 競合情勢

- 主要企業によるヒートマップ分析

第13章 業界情勢

- 合併と買収

- パートナーシップ

第14章 企業プロファイル

- Avient Corp

- Toray Industries Inc

- SGL Carbon SE

- Owens Corning

- Gurit Holding AG

- Covestro AG

- Hexion Inc

- EPSILON Composite SA

- Exel Composites Oyj

- Hexcel Corp

第15章 企業概要付録

List Of Tables

- Table 1. Europe Wind Turbine Composites Market Segmentation

- Table 2. List of Raw Material Suppliers

- Table 3. List of Manufacturers

- Table 4. Europe Wind Turbine Composites Market Volume and Forecasts To 2030 (Kilo Tons)

- Table 5. Europe Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million)

- Table 6. Europe Wind Turbine Composites Market Volume and Forecasts To 2030 (Kilo Tons) - Fiber Type

- Table 7. Europe Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - Fiber Type

- Table 8. Europe Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - Resin Type

- Table 9. Europe Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - Technology

- Table 10. Europe Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - Application

- Table 11. Germany Wind Turbine Composites Market Volume and Forecasts To 2030 (Kilo Tons) - By Fiber Type

- Table 12. Germany Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Fiber Type

- Table 13. Germany Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Resin Type

- Table 14. Germany Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Technology

- Table 15. Germany Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Application

- Table 16. France Wind Turbine Composites Market Volume and Forecasts To 2030 (Kilo Tons) - By Fiber Type

- Table 17. France Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Fiber Type

- Table 18. France Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Resin Type

- Table 19. France Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Technology

- Table 20. France Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Application

- Table 21. Italy Wind Turbine Composites Market Volume and Forecasts To 2030 (Kilo Tons) - By Fiber Type

- Table 22. Italy Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Fiber Type

- Table 23. Italy Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Resin Type

- Table 24. Italy Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Technology

- Table 25. Italy Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Application

- Table 26. UK Wind Turbine Composites Market Volume and Forecasts To 2030 (Kilo Tons) - By Fiber Type

- Table 27. UK Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Fiber Type

- Table 28. UK Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Resin Type

- Table 29. UK Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Technology

- Table 30. UK Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Application

- Table 31. Russia Wind Turbine Composites Market Revenue and Forecasts To 2030 (Kilo Tons) - By Fiber Type

- Table 32. Russia Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Fiber Type

- Table 33. Russia Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Resin Type

- Table 34. Russia Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Technology

- Table 35. Russia Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Application

- Table 36. Rest of Europe Wind Turbine Composites Market Volume and Forecasts To 2030 (Kilo Tons) - By Fiber Type

- Table 37. Rest of Europe Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Fiber Type

- Table 38. Rest of Europe Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Resin Type

- Table 39. Rest of Europe Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Technology

- Table 40. Rest of Europe Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million) - By Application

- Table 41. Company Positioning & Concentration

List Of Figures

- Figure 1. Europe Wind Turbine Composites Market Segmentation, By country

- Figure 2. Europe Wind Turbine Composites Market - Porter's Analysis

- Figure 3. Ecosystem: Europe Wind Turbine Composites Market

- Figure 4. Market Dynamics: Europe Wind Turbine Composites Market

- Figure 5. Historic Development of New Installations (GW)

- Figure 6. New Wind Power Capacity in 2022, by Region (%)

- Figure 7. Europe Wind Turbine Composites Market Impact Analysis of Drivers and Restraints

- Figure 8. Europe Wind Turbine Composites Market Volume (Kilo Tons), 2020 - 2030

- Figure 9. Europe Wind Turbine Composites Market Revenue (US$ Million), 2020 - 2030

- Figure 10. Europe Wind Turbine Composites Market Share (%) - Fiber Type, 2022 and 2030

- Figure 11. Carbon Fiber Composites Market Volume and Forecasts To 2030 (Kilo Tons)

- Figure 12. Carbon Fiber Composites Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 13. Glass Fiber Composites Market Volume and Forecasts To 2030 (Kilo Tons)

- Figure 14. Glass Fiber Composites Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 15. Others Market Volume and Forecasts To 2030 (Kilo Tons)

- Figure 16. Others Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 17. Europe Wind Turbine Composites Market Share (%) - Resin Type, 2022 and 2030

- Figure 18. Polyester Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 19. Epoxy Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 20. Polyurethane Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 21. Vinyl Ester Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 22. Others Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 23. Europe Wind Turbine Composites Market Share (%) - Technology, 2022 and 2030

- Figure 24. Resin Infusion Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 25. Prepreg Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 26. Lay Up Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 27. Others Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 28. Europe Wind Turbine Composites Market Share (%) - Application, 2022 and 2030

- Figure 29. Blades Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 30. Nacelles Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 31. Europe Wind Turbine Composites Market, by key Country - Revenue (2022) (US$ Million)

- Figure 32. Wind Turbine Composites Market Breakdown by Key Countries, 2022 and 2030 (%)

- Figure 33. Germany Wind Turbine Composites Market Volume and Forecasts To 2030 (Kilo Tons)

- Figure 34. Germany Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 35. France Wind Turbine Composites Market Volume and Forecasts To 2030 (Kilo Tons)

- Figure 36. France Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 37. Italy Wind Turbine Composites Market Volume and Forecasts To 2030 (Kilo Tons)

- Figure 38. Italy Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 39. UK Wind Turbine Composites Market Volume and Forecasts To 2030 (Kilo Tons)

- Figure 40. UK Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 41. Russia Wind Turbine Composites Market Volume and Forecasts To 2030 (Kilo Tons)

- Figure 42. Russia Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million)

- Figure 43. Rest of Europe Wind Turbine Composites Market Volume and Forecasts To 2030 (Kilo Tons)

- Figure 44. Rest of Europe Wind Turbine Composites Market Revenue and Forecasts To 2030 (US$ Million)

The Europe wind turbine composites market was valued at US$ 2,110.78 million in 2022 and is expected to reach US$ 4,334.04 million by 2030; it is estimated to grow at a CAGR of 9.4% from 2022 to 2030.

Increase in Installation Rate of Wind Turbine Capacity Drives Europe Wind Turbine Composites Market

Wind power is considered a clean and renewable energy source that provides electricity without burning fuel or polluting the air. Wind energy helps reduce reliance on fossil fuels. Hence, there is an increasing interest in wind energy among various countries, which has resulted in rapid growth in their installed wind capacity. In 2020, new installations in the onshore wind farms reached 86.9 GW, while the offshore wind farms reached 6.1 GW, making 2020 the highest and the second-highest year in history for new wind installations for onshore and offshore, respectively. Europe witnessed record onshore wind installations in 2022, which helped boost the region's share in new wind power capacity addition from 19% in 2021 to 25% in 2022. In Europe, in 2022, new wind installations amounted to 19.1 GW (16.7 GW onshore and 2.5 GW offshore). Furthermore, 87% of the new wind installations in Europe in 2022 were onshore wind. Germany, Sweden, and Finland were significant contributors to the construction of onshore wind farms. Approximately half the offshore installations were in the UK. Also, France installed its first large offshore wind farm. Wind turbine composites are the materials that are utilized in the production of equipment such as blades and nacelles. These materials include fiber and matrix, which provide resilience and high tensile strength. Glass fiber-reinforced plastics (GRP) have been the most commonly used composite material in the wind turbine industry. The growing demand for wind turbine composites can be attributed to the installation of new wind turbines in offshore and onshore projects due to increasing governmental focus on renewable energy forms. The increasing capacity of wind farms and a surge in the number of wind farm projects across the globe are boosting the need for wind turbines, fueling the demand for wind turbine composites.

Europe Wind Turbine Composites Market Overview

The Europe wind turbine composites market is segmented into Germany, France, Italy, the UK, Russia, and the Rest of Europe (Sweden, Finland, etc.). Various countries in the region are harnessing technological capabilities to achieve their sustainability goals. As seen in the following figure, in 2022, new wind installations in Europe totaled 19.1 GW (16.7 GW onshore and 2.5 GW offshore), recording an increase of 4% compared with 2021. Germany, Sweden, and Finland built the most onshore wind projects in 2022. The UK accounted for almost half the offshore installations. Further, Sweden is making significant investments in the wind energy sector. According to news released in December 2022, the Nordic Investment Bank (NIB) and Kolvallen Vind AB signed a EUR 50.15 million (US$ 54.82 million) loan agreement to construct a 277 MW wind farm in Sweden. According to WindEurope, Europe invested EUR 41 billion (US$ 45.07 billion) in new wind farms in 2021, which included the financing of 25 GW of new capacity. Moreover, the region invested EUR 17 billion (US$ 18.69 billion) in new wind farms in 2022, down from US$ 48.47 million in 2021 and the lowest investment figure since 2009. The European wind industry suffers from higher input costs and supply chain disruptions. Moreover, the Russia-Ukraine war amplified challenges associated with raw material cost volatility and international shipping. As a result, the cost of producing a wind turbine in Europe has increased by up to 40% in the last two years. Thus, investments in the wind energy sector dropped in 2022 across Europe, which hampered the wind turbine composites market in the region.

Europe Wind Turbine Composites Market Revenue and Forecast to 2030 (US$ Million)

Europe Wind Turbine Composites Market Segmentation

The Europe wind turbine composites market is segmented based on fiber type, resin type, technology, application, and country.

Based on fiber type, the Europe wind turbine composites market is segmented into carbon fiber composites, glass fiber composites, and others. The glass fiber composites segment held a larger share in 2022.

In terms of resin type, the Europe wind turbine composites market is segmented into polyester, epoxy, polyurethane, vinyl ester, and others. The epoxy segment held the largest share in 2022.

Based on technology, the Europe wind turbine composites market is segmented into resin infusion, prepreg, lay up, and others. The resin infusion segment held the largest share in 2022.

By application, the Europe wind turbine composites market is bifurcated into blades and nacelles. The blades segment held a larger share in 2022.

Based on country, the Europe wind turbine composites market is segmented into Germany, France, Italy, the UK, Russia, and the Rest of Europe. The Rest of Europe dominated the Europe wind turbine composites market in 2022.

Avient Corp, Toray Industries Inc, SGL Carbon SE, Owens Corning, Gurit Holding AG, Covestro AG, Hexion Inc, EPSILON Composite SA, Exel Composites Oyj, and Hexcel Corp are some of the leading companies operating in the Europe wind turbine composites market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

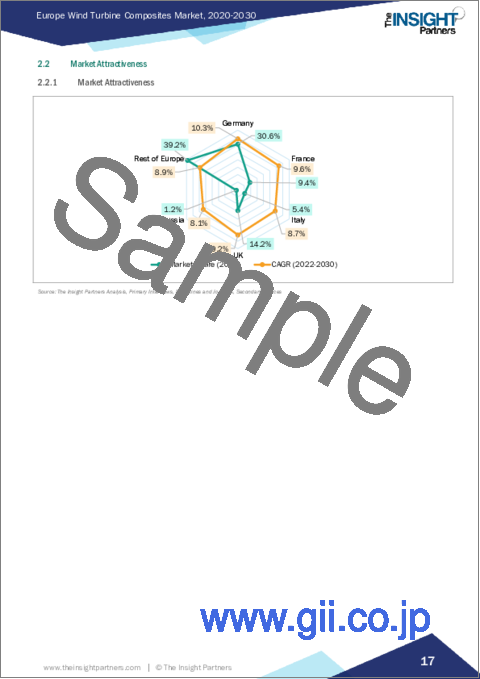

- 2.2 Market Attractiveness

- 2.2.1 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Europe Wind Turbine Composites Market Landscape

- 4.1 Overview

- 4.2 Porters Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Ecosystem Analysis

- 4.3.1 Raw Material Suppliers

- 4.3.2 Wind Turbine Composites Manufacturers

- 4.3.3 Distributors/Suppliers

- 4.3.4 End-Users and Original Equipment Manufacturers

- 4.3.5 List of Vendors in the Value Chain

5. Europe Wind Turbine Composites Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Increase in Installation Rate of Wind Turbine Capacity

- 5.1.2 Increasing Length of Wind Turbine Blades

- 5.2 Market Restraints

- 5.2.1 High Dependence of Wind Energy Industry on Government Subsidies

- 5.3 Market Opportunities

- 5.3.1 Government Initiatives for Development of Wind Energy Sector

- 5.4 Future Trends

- 5.4.1 Adoption of Natural Fiber Reinforced Polymer (NFRP) Composites

- 5.5 Impact Analysis

6. Wind Turbine Composites Market - Europe Market Analysis

- 6.1 Europe Wind Turbine Composites Market Volume (Kilo Tons)

- 6.2 Europe Wind Turbine Composites Market Revenue (US$ Million)

- 6.3 Europe Wind Turbine Composites Market Forecast and Analysis

7. Europe Wind Turbine Composites Market Analysis - Fiber Type

- 7.1 Carbon Fiber Composites

- 7.1.1 Overview

- 7.1.2 Carbon Fiber Composites Market Volume and Forecast to 2030 (Kilo Tons)

- 7.1.3 Carbon Fiber Composites Market Revenue and Forecast to 2030 (US$ Million)

- 7.2 Glass Fiber Composites

- 7.2.1 Overview

- 7.2.2 Glass Fiber Composites Market Volume and Forecast to 2030 (Kilo Tons)

- 7.2.3 Glass Fiber Composites Market Revenue and Forecast to 2030 (US$ Million)

- 7.3 Others

- 7.3.1 Overview

- 7.3.2 Others Market Volume and Forecast to 2030 (Kilo Tons)

- 7.3.1 Others Market Revenue and Forecast to 2030 (US$ Million)

8. Europe Wind Turbine Composites Market Analysis - Resin Type

- 8.1 Polyester

- 8.1.1 Overview

- 8.1.2 Polyester Market Revenue and Forecast to 2030 (US$ Million)

- 8.2 Epoxy

- 8.2.1 Overview

- 8.2.2 Epoxy Market Revenue and Forecast to 2030 (US$ Million)

- 8.3 Polyurethane

- 8.3.1 Overview

- 8.3.2 Polyurethane Market Revenue and Forecast to 2030 (US$ Million)

- 8.4 Vinyl Ester

- 8.4.1 Overview

- 8.4.2 Vinyl Ester Market Revenue and Forecast to 2030 (US$ Million)

- 8.5 Others

- 8.5.1 Overview

- 8.5.2 Others Market Revenue and Forecast to 2030 (US$ Million)

9. Europe Wind Turbine Composites Market Analysis - Technology

- 9.1 Resin Infusion

- 9.1.1 Overview

- 9.1.2 Resin Infusion Market Revenue and Forecast to 2030 (US$ Million)

- 9.2 Prepreg

- 9.2.1 Overview

- 9.2.2 Prepreg Market Revenue and Forecast to 2030 (US$ Million)

- 9.3 Lay Up

- 9.3.1 Overview

- 9.3.2 Lay Up Market Revenue and Forecast to 2030 (US$ Million)

- 9.4 Others

- 9.4.1 Overview

- 9.4.2 Others Market Revenue and Forecast to 2030 (US$ Million)

10. Europe Wind Turbine Composites Market Analysis - Application

- 10.1 Blades

- 10.1.1 Overview

- 10.1.2 Blades Market, Revenue, and Forecast to 2030 (US$ Million)

- 10.2 Nacelles

- 10.2.1 Overview

- 10.2.2 Nacelles Market Revenue, and Forecast to 2030 (US$ Million)

11. Europe Wind Turbine Composites Market - Country Analysis

- 11.1 Europe

- 11.1.1 Wind Turbine Composites Market Breakdown by Country

- 11.1.2 Germany Wind Turbine Composites Market Volume and Forecasts to 2030 (Kilo Tons)

- 11.1.3 Germany Wind Turbine Composites Market Revenue and Forecasts to 2030 (US$ Million)

- 11.1.3.1 Germany Wind Turbine Composites Market Breakdown by Fiber Type

- 11.1.3.2 Germany Wind Turbine Composites Market Breakdown by Resin Type

- 11.1.3.3 Germany Wind Turbine Composites Market Breakdown by Technology

- 11.1.3.4 Germany Wind Turbine Composites Market Breakdown by Application

- 11.1.4 France Wind Turbine Composites Market Volume and Forecasts to 2030 (Kilo Tons)

- 11.1.5 France Wind Turbine Composites Market Revenue and Forecasts to 2030 (US$ Million)

- 11.1.5.1 France Wind Turbine Composites Market Breakdown by Fiber Type

- 11.1.5.2 France Wind Turbine Composites Market Breakdown by Resin Type

- 11.1.5.3 France Wind Turbine Composites Market Breakdown by Technology

- 11.1.5.4 France Wind Turbine Composites Market Breakdown by Application

- 11.1.6 Italy Wind Turbine Composites Market Volume and Forecasts to 2030 (Kilo Tons)

- 11.1.7 Italy Wind Turbine Composites Market Revenue and Forecasts to 2030 (US$ Million)

- 11.1.7.1 Italy Wind Turbine Composites Market Breakdown by Fiber Type

- 11.1.7.2 Italy Wind Turbine Composites Market Breakdown by Resin Type

- 11.1.7.3 Italy Wind Turbine Composites Market Breakdown by Technology

- 11.1.7.4 Italy Wind Turbine Composites Market Breakdown by Application

- 11.1.8 UK Wind Turbine Composites Market Volume and Forecasts to 2030 (Kilo Tons)

- 11.1.9 UK Wind Turbine Composites Market Revenue and Forecasts to 2030 (US$ Million)

- 11.1.9.1 UK Wind Turbine Composites Market Breakdown by Fiber Type

- 11.1.9.2 UK Wind Turbine Composites Market Breakdown by Resin Type

- 11.1.9.3 UK Wind Turbine Composites Market Breakdown by Technology

- 11.1.9.4 UK Wind Turbine Composites Market Breakdown by Application

- 11.1.10 Russia Wind Turbine Composites Market Volume and Forecasts to 2030 (Kilo Tons)

- 11.1.11 Russia Wind Turbine Composites Market Revenue and Forecasts to 2030 (US$ Million)

- 11.1.11.1 Russia Wind Turbine Composites Market Breakdown by Fiber Type

- 11.1.11.2 Russia Wind Turbine Composites Market Breakdown by Resin Type

- 11.1.11.3 Russia Wind Turbine Composites Market Breakdown by Technology

- 11.1.11.4 Russia Wind Turbine Composites Market Breakdown by Application

- 11.1.12 Rest of Europe Wind Turbine Composites Market Volume and Forecasts to 2030 (Kilo Tons)

- 11.1.13 Rest of Europe Wind Turbine Composites Market Revenue and Forecasts to 2030 (US$ Million)

- 11.1.13.1 Rest of Europe Wind Turbine Composites Market Breakdown by Fiber Type

- 11.1.13.2 Rest of Europe Wind Turbine Composites Market Breakdown by Resin Type

- 11.1.13.3 Rest of Europe Wind Turbine Composites Market Breakdown by Technology

- 11.1.13.4 Rest of Europe Wind Turbine Composites Market Breakdown by Application

12. Competitive Landscape

- 12.1 Heat Map Analysis by Key Players

13. Industry Landscape

- 13.1 Overview

- 13.2 Merger and Acquisition

- 13.3 Partnerships

14. Company Profiles

- 14.1 Avient Corp

- 14.1.1 Key Facts

- 14.1.2 Business Description

- 14.1.3 Products and Services

- 14.1.4 Financial Overview

- 14.1.5 SWOT Analysis

- 14.1.6 Key Developments

- 14.2 Toray Industries Inc

- 14.2.1 Key Facts

- 14.2.2 Business Description

- 14.2.3 Products and Services

- 14.2.4 Financial Overview

- 14.2.5 SWOT Analysis

- 14.2.6 Key Developments

- 14.3 SGL Carbon SE

- 14.3.1 Key Facts

- 14.3.2 Business Description

- 14.3.3 Products and Services

- 14.3.4 Financial Overview

- 14.3.5 SWOT Analysis

- 14.3.6 Key Developments

- 14.4 Owens Corning

- 14.4.1 Key Facts

- 14.4.2 Business Description

- 14.4.3 Products and Services

- 14.4.4 Financial Overview

- 14.4.5 SWOT Analysis

- 14.4.6 Key Developments

- 14.5 Gurit Holding AG

- 14.5.1 Key Facts

- 14.5.2 Business Description

- 14.5.3 Products and Services

- 14.5.4 Financial Overview

- 14.5.5 SWOT Analysis

- 14.5.6 Key Developments

- 14.6 Covestro AG

- 14.6.1 Key Facts

- 14.6.2 Business Description

- 14.6.3 Products and Services

- 14.6.4 Financial Overview

- 14.6.5 SWOT Analysis

- 14.6.6 Key Developments

- 14.7 Hexion Inc

- 14.7.1 Key Facts

- 14.7.2 Business Description

- 14.7.3 Products and Services

- 14.7.4 Financial Overview

- 14.7.5 SWOT Analysis

- 14.7.6 Key Developments

- 14.8 EPSILON Composite SA

- 14.8.1 Key Facts

- 14.8.2 Business Description

- 14.8.3 Products and Services

- 14.8.4 SWOT Analysis

- 14.8.5 Key Developments

- 14.9 Exel Composites Oyj

- 14.9.1 Key Facts

- 14.9.2 Business Description

- 14.9.3 Products and Services

- 14.9.4 Financial Overview

- 14.9.5 SWOT Analysis

- 14.9.6 Key Developments

- 14.10 Hexcel Corp

- 14.10.1 Key Facts

- 14.10.2 Business Description

- 14.10.3 Products and Services

- 14.10.4 Financial Overview

- 14.10.5 SWOT Analysis