|

|

市場調査レポート

商品コード

1533050

北米の自動試験装置:2030年市場予測- 地域別分析- タイプ別、コンポーネント別、エンドユーザー別North America Automated Test Equipment Market Forecast to 2030 - Regional Analysis - by Type, Component, and End User |

||||||

|

|||||||

|

|||||||

| 北米の自動試験装置:2030年市場予測- 地域別分析- タイプ別、コンポーネント別、エンドユーザー別 |

|

出版日: 2024年06月04日

発行: The Insight Partners

ページ情報: 英文 97 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

北米の自動試験装置市場は、2022年に15億6,755万米ドルと評価され、2030年には26億7,951万米ドルに達すると予測され、2022年から2030年までのCAGRは6.9%と推定されます。

製造業における自動化の進展が北米の自動試験装置市場を活性化

電子・半導体技術の進化は、製造部門の自動化への道を開いています。近年、オートメーションは、製造業の雇用、工場現場のオペレーション、製造業全体のダイナミクスを変革するために、製造業で非常に採用されています。人工知能、ロボット工学、機械学習など、いくつかの先進技術の採用が進むにつれて、製造業のさまざまなレベルで必要とされる認知活動などの製造活動において、機械が人間と同等か、人間を上回ることができるようになった。製造工程における自動化は、生産性を最大40%以上向上させ、無駄のない組立ラインに統合されながら、反復作業の45%を除去します。さらに、インダストリー4.0の進化も製造業を牽引する動向のひとつです。GSM協会によると、インダストリー4.0の動向は2023年から2025年にかけて46%の成長が見込まれており、先端技術の急速な展開が市場を牽引しています。自動搬送車や協働ロボットの力を活用するインダストリー4.0やモノのインターネット(IIoT)の進化は、製造部門の生産性をさらに押し上げています。

半導体製造は、世界中の製造部門で自動化の採用を増やしています。顧客の間でインターネットの利用が拡大しており、ソフトウェアからサービス、半導体デバイスに至るまで、バリューチェーン全体を変革し、自動化しています。世界中でのIoTの出現は、半導体産業での採用を増加させています。この業界は北米自動テスト装置市場の牽引役として重要な役割を果たすと期待されています。

IoTに接続された製品、デバイス、アプリケーションは、超小型チップ、ワイヤレス接続オプション、低消費電力を必要とします。スマートグラス、スマートフォン、スマートウォッチなど、多数のIoTセンサベースの製品の採用が拡大しているため、低技術ノードで電力優位性を持つMEMS/NEMSセンサプラットフォームの需要が高まっています。これらのプラットフォームは、単一の小さなフォームファクタのダイで機能を向上させる。

製造業では、RPA(ロボティック・プロセス・オートメーション)によりミスのない合理的な手順が実現しつつあります。製造企業は、製品の組み立て、品質チェック、梱包を行うために、生産ユニットを人力から産業用ロボットに置き換えています。部品表の作成、データ移行、管理、レポート、ERP自動化、物流データ自動化、カスタマーサポート、サービスデスク、Web統合型RPAなどの自動化活動のためのRPAの製造部門への統合は、自動試験装置市場の成長を促進しています。製造施設はより高いレベルの自動化を取り入れており、そのため新技術への需要が急速に高まっています。家電、自動車、ヘルスケア、防衛産業は、業務を合理化するために製造組立ラインに自動化を組み込むことで生産性を向上させている最も顕著な産業分野です。これらの産業は、自動化に使用される半導体デバイスの検査をより少なく迅速に行うことができるため、自動試験装置の需要を促進すると予想されます。

北米の自動試験装置市場概要

製造業は北米経済の成長に重要な役割を果たしています。米国、カナダ、メキシコがこの地域の主要国です。先進諸国(米国とカナダ)には効率的なインフラが整っているため、製造企業は科学、技術、商業の限界を探ることができます。全米製造業者協会(NAM)によると、米国は世界第2位の製造業を擁し、2023年9月時点で2兆9,000億米ドルを計上しています。Spex Precision Machine Technologies Inc.の調査によると、製造業は2023年時点で米国経済の11%を占めています。さらに、この産業は、最新技術の利用可能性とガス価格の低下による生産性の向上により、今後数年間で急成長が見込まれています。新興市場における人件費の上昇や知的財産の保護強化も、米国の製造業に利益をもたらす重要な要因です。北米、特に米国の製造業の動向は、ここ数年、世界的に最も影響力のある動向となっています。北米の主な製造業には、航空宇宙、自動車、通信、エレクトロニクスなどがあります。このように、確立された製造業は、この地域で自動試験装置に対する高い需要を生み出しています。

カナダの製造業は、消費者の間で石炭、金属、石油製品への需要が高まり、収益性が高まっています。同国では、ドルの価値が下がり、安価な電力が利用できるようになり、製造業に利益をもたらしています。メキシコでは、外国直接投資(FDI)を誘致するための政府の努力により、製造業が著しい成長を遂げています。さらに、同国は米国に近く、NAFTAによってコスト競争力を獲得できることも、この産業に利益をもたらしています。メキシコの自動車産業はパラダイムシフトを経験しており、多くの巨大自動車会社が国内に工場を建設しています。最近メキシコに工場を開設した企業には、起亜自動車、メルセデス・ベンツ、日産、アウディ、ゼネラル・モーターズなどがあります。また、Axium Packaging Inc.とFordも同国に新工場を建設し、2026年までに操業を開始する予定です。

北米の自動試験装置市場の収益と2030年までの予測(金額)

北米の自動試験装置市場のセグメンテーション

北米の自動試験装置市場は、タイプ別、コンポーネント別、エンドユーザー別、国に分類されます。

タイプ別では、北米の自動試験装置市場は、集積回路(IC)テスト、プリント基板(PCB)テスト、ハードディスクドライブ(HDD)テスト、その他に分類されます。集積回路(IC)テストセグメントが2022年に最大の市場シェアを占めました。

コンポーネント別では、北米の自動試験装置市場は産業用PC、マスインターコネクト、ハンドラ/プローバに区分されます。産業用PCセグメントが2022年に最大の市場シェアを占めました。

エンドユーザー別では、北米の自動試験装置市場は家庭用電子機器、自動車、医療、航空宇宙・防衛、IT・通信、その他の産業に分類されます。2022年には家庭用電子機器セグメントが最大の市場シェアを占めました。

国別では、北米の自動試験装置市場は米国、カナダ、メキシコに区分されます。2022年の北米の自動試験装置市場シェアは米国が独占しました。

Advantest Corp;Anritsu Corp;Astronics Corporation;Averna Technologies Inc;Chroma ATE Inc;National Instruments Corp;SPEA S.p.A;Teradyne Inc;Test Research, Inc.などが北米の自動試験装置市場で事業を展開している大手企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 北米の自動試験装置市場情勢

- エコシステム分析

- バリューチェーンのベンダー一覧

第5章 北米の自動試験装置市場:主要産業力学

- 促進要因

- 製造業における自動化の増加

- 堅牢な試験方法に対する需要の高まり

- 高速テスト機能に対するニーズの高まり

- 市場抑制要因

- テストにかかる膨大なコストとO&Mの複雑さ

- 市場機会

- IoTとコネクテッドデバイスの進化

- 自動車産業におけるコンシューマー・エレクトロニクスの統合

- 今後の動向

- 自律走行車向けセンサーのテスト

- 促進要因と抑制要因の影響

第6章 自動試験装置市場:北米市場分析

- 北米の自動試験装置市場概要

- 北米の自動試験装置市場収益、2022年~2030年

- 北米の自動試験装置市場の予測と分析

第7章 北米の自動試験装置市場分析-タイプ別

- 集積回路(IC)テスト

- 集積回路(IC)テスト市場の収益と2030年までの予測

- プリント基板(PCB)試験

- プリント基板(PCB)検査市場の収益と2030年までの予測

- ハードディスクドライブ(HDD)試験

- ハードディスクドライブ(HDDs)検査市場の収益と2030年までの予測

- その他

- その他の概要

- その他市場の収益と2030年までの予測

第8章 北米の自動試験装置市場の分析:コンポーネント別

- 産業用PC

- 産業用PC市場の収益と2030年までの予測

- マスインターコネクト

- マスインターコネクト市場の収益と2030年までの予測

- ハンドラー/プローバ

- ハンドラ/プローバ市場の収益と2030年までの予測

第9章 北米の自動試験装置市場の分析:エンドユーザー別

- コンシューマーエレクトロニクス

- コンシューマーエレクトロニクス市場の収益と2030年までの予測

- 自動車

- 自動車市場の収益と2030年までの予測

- 医療

- 医療市場の収益と2030年までの予測

- 航空宇宙・防衛

- 航空宇宙・防衛市場の収益と2030年までの予測

- IT・通信

- IT・通信市場の収益と2030年までの予測

- その他

- その他の概要

- その他市場の収益と2030年までの予測

第10章 北米の自動試験装置市場:国別分析

- 北米

- 米国

- カナダ

- メキシコ

第11章 業界情勢

- 市場イニシアティブ

- 製品開発

- 合併と買収

第12章 企業プロファイル

- Anritsu Corp

- Advantest Corp

- Astronics Corporation

- Averna Technologies Inc

- Chroma ATE Inc.

- National Instruments Corp

- SPEA S.p.A.

- Teradyne Inc

- Test Research, Inc.

第13章 付録

List Of Tables

- Table 1. North America Automated Test Equipment Market Segmentation

- Table 2. North America Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Million)

- Table 3. North America Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Million) - Type

- Table 4. North America Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Million) - Component

- Table 5. North America Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Million) - End User

- Table 6. North America Automated Test Equipment Market, by Country - Revenue and Forecast to 2030 (USD Million)

- Table 7. US Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn) - By Type

- Table 8. US Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn) - By Component

- Table 9. US Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 10. Canada Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn) - By Type

- Table 11. Canada Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn) - By Component

- Table 12. Canada Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 13. Mexico Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn) - By Type

- Table 14. Mexico Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn) - By Component

- Table 15. Mexico Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 16. List of Abbreviation

List Of Figures

- Figure 1. North America Automated Test Equipment Market Segmentation, By Country

- Figure 2. Ecosystem: Automated Test Equipment Market

- Figure 3. North America Automated Test Equipment Market - Key Industry Dynamics

- Figure 4. Impact Analysis of Drivers and Restraints

- Figure 5. North America Automated Test Equipment Market Revenue (US$ Million), 2022 - 2030

- Figure 6. North America Automated Test Equipment Market Share (%) - Type, 2022 and 2030

- Figure 7. Integrated Circuits (ICs) Testing Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 8. Printed Circuit Boards (PCBs) Testing Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 9. Hard Disk Drives (HDDs) Testing Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 10. Others Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 11. North America Automated Test Equipment Market Share (%) - Component, 2022 and 2030

- Figure 12. Industrial PCs Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 13. Mass Interconnect Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 14. Handler/Prober Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 15. North America Automated Test Equipment Market Share (%) - End User, 2022 and 2030

- Figure 16. Consumer Electronics Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 17. Automotive Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 18. Medical Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 19. Aerospace & Defense Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 20. IT & Telecommunication Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 21. Others Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 22. North America Automated Test Equipment Market, By Key Country - Revenue (2022) (US$ Million)

- Figure 23. Automated Test Equipment Market Breakdown by Key Countries, 2022 and 2030 (%)

- Figure 24. US Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 25. Canada Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 26. Mexico Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn)

The North America automated test equipment market was valued at US$ 1,567.55 million in 2022 and is expected to reach US$ 2,679.51 million by 2030; it is estimated to register a CAGR of 6.9% from 2022 to 2030.

Increasing Automation in Manufacturing Sector Fuels North America Automated Test Equipment Market

The evolution of electronic and semiconductor technologies is paving the way for automation in the manufacturing sector. In recent years, automation has been highly adopted in the manufacturing sector for transforming manufacturing employment, factory floor operations, and the overall dynamics of the manufacturing sector. The growing adoption of several advanced technologies, such as artificial intelligence, robotics, and machine learning, allows machines to match or outpace humans in manufacturing activities, such as the cognitive activities that are required at various levels of manufacturing. Automation in the manufacturing processes increases productivity by up to more than 40% and removes 45% of repetitive work while integrated on the lean assembly line. Further, the evolution of Industry 4.0 is another trend driving the manufacturing sector. According to the GSM Association, the industry 4.0 trend is expected to grow at 46% during 2023-2025, associated with the rapid deployment of advanced technologies, which is driving the market. The evolution of Industry 4.0 or the Industrial Internet of Things (IIoT) that would utilize automated guided vehicles and the powers of collaborative robots is further boosting productivity in the manufacturing sector.

Semiconductor fabrications are increasing the adoption of automation in the manufacturing sector worldwide. The growing use of the Internet among customers is transforming and automating the entire value chain, from software to service to semiconductor devices. The emergence of IoT across the globe increases its adoption in the semiconductor industry. The industry is expected to play a crucial role in driving the North America automated test equipment market.

IoT-connected products, devices, and applications need ultra-small chips, wireless connectivity options, and low power consumption. The growing adoption of numerous IoT sensor-based products such as smart glasses, smartphones, and smartwatches is creating demand for MEMS/NEMS sensor platforms that have power advantages with lower technology nodes. These platforms increase functionality on a single small form-factor die.

The manufacturing sector is witnessing error-free and streamlined procedures using Robotic Process Automation (RPA). Manufacturing companies are replacing the production units from human sources with industry robots for the products to assemble, quality checks, and packaging to be done. The integration of RPA into the manufacturing sector for automatic activities such as preparing bills of materials, data migration, administration and reporting, ERP automation, logistics data automation, customer support, and service desk, and Web-integrated RPA is fueling the automated test equipment market growth. Manufacturing facilities have been incorporating greater levels of automation, owing to which the demand for new technologies is growing rapidly. Consumer electronics, automobiles, healthcare, and defense industries are the most prominent industry verticals that have become productive by integrating automation into the manufacturing assembly lines to streamline operations. These industries are anticipated to drive the demand for automatic test equipment as it results in lesser and quicker inspection of the semiconductor devices used for automation.

North America Automated Test Equipment Market Overview

The manufacturing industry plays a vital role in the growth of the North American economy. The US, Canada, and Mexico are the prime countries in the region. The availability of efficient infrastructure in developed countries (the US and Canada) enables manufacturing companies to explore the limits of science, technology, and commerce. According to the National Association of Manufacturers (NAM), the US has the second-largest manufacturing industry in the world, which accounted for ~US$ 2.9 trillion as of September 2023. As per a survey by Spex Precision Machine Technologies Inc., the manufacturing industry accounts for 11% of the US economy as of 2023. Moreover, this industry is expected to grow rapidly in the coming years owing to increased productivity due to the availability of modern technologies and decreasing gas prices. Rising labor costs in emerging markets and better protection available for intellectual properties are other important factors benefiting the manufacturing businesses in the US. The manufacturing industry dynamics in North America, specifically in the US, have been the most influential trends globally over the past few years. A few of the major manufacturing industries in North America include aerospace, automotive, telecommunications, and electronics. Thus, the well-established manufacturing industry generates a high demand for automated test equipment in the region.

The manufacturing industry in Canada is becoming more profitable with the rising demand for coal, metal, and oil products among consumers. The country is experiencing a declining dollar value and availability of cheaper power, which benefits manufacturing businesses. In Mexico, the manufacturing industry is noticing significant growth due to efforts made by governments to attract foreign direct investments (FDIs). Furthermore, the country's proximity to the US and ability to achieve cost-competitiveness due to NAFTA benefit this industry. The automotive industry in Mexico is experiencing a paradigm shift, with many huge automobile companies constructing their plants in the country. A few of the companies that recently opened their plants in the country include Kia Motors, Mercedes-Benz, Nissan, Audi, General Motors, and others. Axium Packaging Inc. and Ford are also planning to construct their new plants in the country and start operations by 2026.

North America Automated Test Equipment Market Revenue and Forecast to 2030 (US$ Million)

North America Automated Test Equipment Market Segmentation

The North America automated test equipment market is categorized into type, component, end user, and country.

Based on type, the North America automated test equipment market is categorized into integrated circuits (ICs) testing, printed circuit boards (PCBs) testing, hard disk drives (HDDs) testing, and others. The integrated circuits (ICs) testing segment held the largest market share in 2022.

In terms of component, the North America automated test equipment market is segmented into industrial PCs, mass interconnect, and handler/prober. The industrial PCs segment held the largest market share in 2022.

By end user, the North America automated test equipment market is categorized into consumer electronics, automotive, medical, aerospace & defense, IT & telecommunication, and other industries. The consumer electronics segment held the largest market share in 2022.

By country, the North America automated test equipment market is segmented into the US, Canada, and Mexico. The US dominated the North America automated test equipment market share in 2022.

Advantest Corp; Anritsu Corp; Astronics Corporation; Averna Technologies Inc; Chroma ATE Inc.; National Instruments Corp; SPEA S.p.A; Teradyne Inc; and Test Research, Inc. are among the leading companies operating in the North America automated test equipment market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. North America Automated Test Equipment Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

- 4.2.1 List of Vendors in the Value Chain:

5. North America Automated Test Equipment Market - Key Industry Dynamics

- 5.1 Drivers

- 5.1.1 Increasing Automation in Manufacturing Sector

- 5.1.2 Rising Demand for Robust Testing Method

- 5.1.3 Growing Need for High-Speed Testing Capabilities

- 5.2 Market Restraints

- 5.2.1 Huge Costs Incurred in Testing and O&M Complexities

- 5.3 Market Opportunities

- 5.3.1 Evolution of IoT and Connected Devices

- 5.3.2 Integrations of Consumer Electronics in Automotive Industry

- 5.4 Future Trends

- 5.4.1 Testing of Sensors for Autonomous Vehicles

- 5.5 Impact of Drivers and Restraints:

6. Automated Test Equipment Market - North America Market Analysis

- 6.1 North America Automated Test Equipment Market Overview

- 6.2 North America Automated Test Equipment Market Revenue (US$ Million), 2022 - 2030

- 6.3 North America Automated Test Equipment Market Forecast and Analysis

7. North America Automated Test Equipment Market Analysis - Type

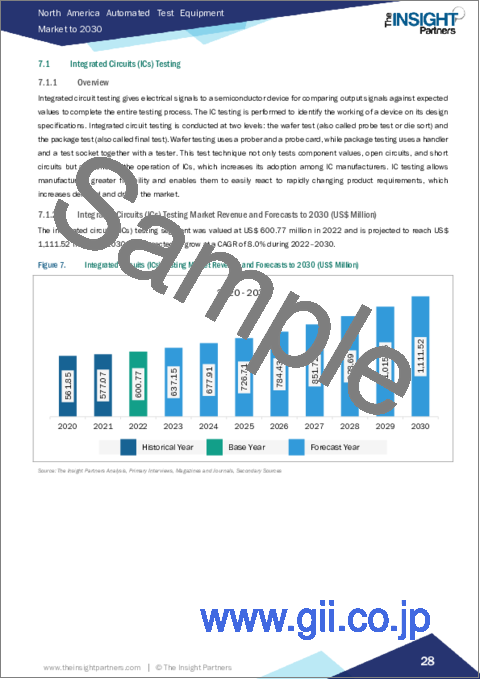

- 7.1 Integrated Circuits (ICs) Testing

- 7.1.1 Overview

- 7.1.2 Integrated Circuits (ICs) Testing Market Revenue and Forecasts to 2030 (US$ Million)

- 7.2 Printed Circuit Boards (PCBs) Testing

- 7.2.1 Overview

- 7.2.2 Printed Circuit Boards (PCBs) Testing Market Revenue and Forecasts to 2030 (US$ Million)

- 7.3 Hard Disk Drives (HDDs) Testing

- 7.3.1 Overview

- 7.3.2 Hard Disk Drives (HDDs) Testing Market Revenue and Forecasts to 2030 (US$ Million)

- 7.4 Others

- 7.4.1 Overview

- 7.4.2 Others Market Revenue and Forecasts to 2030 (US$ Million)

8. North America Automated Test Equipment Market Analysis - Component

- 8.1 Industrial PCs

- 8.1.1 Overview

- 8.1.2 Industrial PCs Market Revenue and Forecasts to 2030 (US$ Million)

- 8.2 Mass Interconnect

- 8.2.1 Overview

- 8.2.2 Mass Interconnect Market Revenue and Forecasts to 2030 (US$ Million)

- 8.3 Handler/Prober

- 8.3.1 Overview

- 8.3.2 Handler/Prober Market Revenue and Forecasts to 2030 (US$ Million)

9. North America Automated Test Equipment Market Analysis - End User

- 9.1 Consumer Electronics

- 9.1.1 Overview

- 9.1.2 Consumer Electronics Market Revenue and Forecasts to 2030 (US$ Million)

- 9.2 Automotive

- 9.2.1 Overview

- 9.2.2 Automotive Market Revenue and Forecasts to 2030 (US$ Million)

- 9.3 Medical

- 9.3.1 Overview

- 9.3.2 Medical Market Revenue and Forecasts to 2030 (US$ Million)

- 9.4 Aerospace & Defense

- 9.4.1 Overview

- 9.4.2 Aerospace & Defense Market Revenue and Forecasts to 2030 (US$ Million)

- 9.5 IT & Telecommunication

- 9.5.1 Overview

- 9.5.2 IT & Telecommunication Market Revenue and Forecasts to 2030 (US$ Million)

- 9.6 Others

- 9.6.1 Overview

- 9.6.2 Others Market Revenue and Forecasts to 2030 (US$ Million)

10. North America Automated Test Equipment Market - Country Analysis

- 10.1 North America

- 10.1.1 North America Automated Test Equipment Market Overview

- 10.1.2 North America Automated Test Equipment Market Revenue and Forecasts and Analysis - By Countries

- 10.1.2.1 US Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn)

- 10.1.2.1.1 US Automated Test Equipment Market Breakdown by Type

- 10.1.2.1.2 US Automated Test Equipment Market Breakdown by Component

- 10.1.2.1.3 US Automated Test Equipment Market Breakdown by End User

- 10.1.2.2 Canada Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn)

- 10.1.2.2.1 Canada Automated Test Equipment Market Breakdown by Type

- 10.1.2.2.2 Canada Automated Test Equipment Market Breakdown by Component

- 10.1.2.2.3 Canada Automated Test Equipment Market Breakdown by End User

- 10.1.2.3 Mexico Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn)

- 10.1.2.3.1 Mexico Automated Test Equipment Market Breakdown by Type

- 10.1.2.3.2 Mexico Automated Test Equipment Market Breakdown by Component

- 10.1.2.3.3 Mexico Automated Test Equipment Market Breakdown by End User

- 10.1.2.1 US Automated Test Equipment Market Revenue and Forecasts to 2030 (US$ Mn)

11. Industry Landscape

- 11.1 Overview

- 11.2 Market Initiative

- 11.3 Product Development

- 11.4 Mergers & Acquisitions

12. Company Profiles

- 12.1 Anritsu Corp

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Advantest Corp

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Astronics Corporation

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Averna Technologies Inc

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Chroma ATE Inc.

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 National Instruments Corp

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 SPEA S.p.A.

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 Teradyne Inc

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 Test Research, Inc.

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

13. Appendix

- 13.1 Word Index