|

|

市場調査レポート

商品コード

1533040

アジア太平洋地域のフィルフィニッシュ製造:2030年市場予測- 地域別分析- 製品、モダリティ、エンドユーザー別Asia Pacific Fill Finish Manufacturing Market Forecast to 2030 - Regional Analysis - by Product, Modality, and End User |

||||||

|

|||||||

|

|||||||

| アジア太平洋地域のフィルフィニッシュ製造:2030年市場予測- 地域別分析- 製品、モダリティ、エンドユーザー別 |

|

出版日: 2024年06月05日

発行: The Insight Partners

ページ情報: 英文 106 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

アジア太平洋地域のフィルフィニッシュ製造市場は、2022年に18億6,735万米ドルと評価され、2030年には42億236万米ドルに達すると予測され、2022年から2030年までのCAGRは10.7%で成長すると予測されています。

新興国における低ビジネスコストがアジア太平洋地域のフィルフィニッシュ製造市場を押し上げる

多くのアジア諸国は、世界中の様々なバイオ医薬品メーカーにとって魅力的なアウトソーシング先として台頭してきています。中国、インド、その他のアジア諸国における製造コストや事業コストの低さが、受託製造を後押しする主な要因となっています。さらに、中国とインドにおける最近のバイオ医薬品産業の動向は、同市場の大きな可能性を示しています。生物製剤とバイオシミラーのパイプラインの成長は、アジア太平洋地域の受託製造業者に新たな道をさらに開いています。受託製造は、運営コストの低減により、初期段階の医薬品メーカーに利益をもたらすことがほとんどです。増大する需要に対応するため、多くのCMOが製造能力を拡大しています。例えば、2020年1月、WuXi AppTec傘下のSTA Pharmaceutical Co., Ltd.は、中国に大規模なオリゴヌクレオチド原薬(API)製造施設を新設しました。

アジア太平洋地域のフィルフィニッシュ製造市場の概要

アジア太平洋地域では、中国がフィルフィニッシュ剤製造の最大市場です。同市場の成長は主に、中国におけるフィルフィニッシュ製造プロセスの技術的進歩の高まり、市場参入企業による開拓の増加、バイオ医薬品産業の拡大、慢性疾患の蔓延の増加に起因しています。中国には500社以上の生物学的製剤/バイオ医薬品企業があります。研究開発に携わっている企業のほとんどは、海外からの帰国者や欧米の合弁企業によって設立されました。見積もりには幅があるが、アナリストによれば、中国政府は資金援助イニシアティブを通じて、年間6億米ドル以上をバイオテクノロジー研究開発に費やしています。中国の国や地方政府も、IT企業に投資する準ベンチャー・キャピタル企業に投資しています。

市場企業は、有機的・無機的成長戦略を通じて事業を拡大しています。例えば、WuXi Biologicsは2022年6月に中国の無錫に医薬品工場を開設し、プレフィルドシリンジ(PFS)の生産能力を年間1,700万ユニットに増やしました。

受託開発製造機関(CDMO)であるウーシー・バイオが運営する最近のD.P.施設はDP5と呼ばれ、信頼性の高い連続充填サービスのための高度なアイソレーター充填ラインを備えています。同社によると、これによりPFSは、1.25mL、3mL、1mL、1mLを含む様々な容量供給オプションを提供できます。

アジア太平洋地域のフィルフィニッシュ製造市場の収益と2030年までの予測(金額)

アジア太平洋地域のフィルフィニッシュ製造市場のセグメンテーション

アジア太平洋地域のフィルフィニッシュ製造市場は、製品、モダリティ、エンドユーザー、国によって区分されます。製品別では、アジア太平洋地域のフィルフィニッシュ製造市場は消耗品と器具に二分されます。消耗品セグメントは2022年に大きな市場シェアを占めました。さらに、消耗品はプレフィルドシリンジ、ガラスバイアル/プラスチックバイアル、カートリッジ、その他に細分化されます。

モダリティの観点から、アジア太平洋地域のフィルフィニッシュ製造市場は、組み換えタンパク質、モノクローナル抗体、ワクチン、細胞療法および生物学的療法、遺伝子療法、その他にセグメント化されます。2022年にはワクチン分野が最大の市場シェアを占めています。

エンドユーザー別では、アジア太平洋地域のフィルフィニッシュ製造市場は、受託製造機関、バイオ医薬品会社、その他に分類されます。受託製造機関セグメントが2022年に最大の市場シェアを占めました。

国別に見ると、アジア太平洋地域のフィルフィニッシュ製造市場は中国、日本、インド、オーストラリア、韓国、その他アジア太平洋地域に分類されます。中国は2022年にアジア太平洋地域のフィルフィニッシュ製造市場シェアを独占しました。

Becton Dickinson and Co、Gerresheimer AG、IMA Industria Macchine Automatiche SpA、Maquinaria Industrial Dara SL、Nipro Medical Asia Pacific NV、NNE AS、Optima Packaging Group Gmbh、Schott AG、SGD SA、Stevanato Group SpA、Syntegon Technology GmbH、West Pharmaceutical Services Incは、アジア太平洋地域のフィルフィニッシュ製造市場で事業を展開している大手企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要な洞察

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 アジア太平洋地域のフィルフィニッシュ製造市場情勢

- 概観

- PEST分析

第5章 アジア太平洋地域のフィルフィニッシュ製造市場-主要産業力学

- フィルフィニッシュ製造市場:主要産業力学

- 主な市場促進要因

- 非経口投与用プレフィルドシリンジの採用拡大

- 生物製剤に対する需要の高まり

- 主な市場抑制要因

- 生物製剤製造の複雑さ

- 主な市場機会

- 新興市場における低いビジネスコスト

- 主な将来動向

- 無菌フィルフィニッシュ用シングルユースシステム

- 促進要因と抑制要因の影響

第6章 フィルフィニッシュ製造市場-アジア太平洋市場分析

第7章 アジア太平洋地域のフィルフィニッシュ製造市場の分析-製品別

- 消耗品

- 消耗品市場、収益と2030年までの予測

- 消耗品

- インストルメンツ市場:収益と2030年までの予測

第8章 アジア太平洋地域のフィルフィニッシュ製造市場の分析:モダリティ別

- 組換えタンパク質

- 組換えタンパク質市場、収益と2030年までの予測

- モノクローナル抗体

- モノクローナル抗体市場、収益と2030年までの予測

- ワクチン

- ワクチン市場、収益と2030年までの予測

- 細胞治療と生物学的治療

- 細胞療法と生物学的療法の市場、収益と2030年までの予測

- 遺伝子治療

- 遺伝子治療市場、収益と2030年までの予測

- その他

- その他の概要

- その他市場、収益と2030年までの予測

第9章 アジア太平洋地域のフィルフィニッシュ製造市場の分析:エンドユーザー別

- 製造受託機関

- 受託製造機関市場、収益と2030年までの予測

- バイオ医薬品企業

- バイオ医薬品企業市場:収益と2030年までの予測

- その他

- その他の概要

- その他の市場、収益と2030年までの予測

第10章 アジア太平洋地域のフィルフィニッシュ製造市場:国別分析

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

第11章 業界情勢

- フィルフィニッシュ製造市場における成長戦略、2020~2023年

- 無機的成長戦略

- 有機的成長戦略

第12章 企業プロファイル

- IMA Industria Macchine Automatiche SpA

- Nipro Medical Europe NV

- Maquinaria Industrial Dara SL

- SGD SA

- Optima Packaging Group Gmbh

- NNE AS

- Stevanato Group SpA

- Syntegon Technology GmbH

- West Pharmaceutical Services Inc

- Gerresheimer AG

- Schott AG

- Becton Dickinson and Co

第13章 付録

List Of Tables

- Table 1. Fill Finish Manufacturing Market Segmentation

- Table 2. Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Million) - Product

- Table 3. Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Million) - Consumables

- Table 4. Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Million) - Modality

- Table 5. Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Million) - End User

- Table 6. China Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Product

- Table 7. China Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Consumables

- Table 8. China Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Modality

- Table 9. China Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 10. Japan Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Product

- Table 11. Japan Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Consumables

- Table 12. Japan Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Modality

- Table 13. Japan Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 14. India Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Product

- Table 15. India Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Consumables

- Table 16. India Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Modality

- Table 17. India Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 18. Australia Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Product

- Table 19. Australia Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Consumables

- Table 20. Australia Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Modality

- Table 21. Australia Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 22. South Korea Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Product

- Table 23. South Korea Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Consumables

- Table 24. South Korea Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Modality

- Table 25. South Korea Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 26. Rest of Asia Pacific Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Product

- Table 27. Rest of Asia Pacific Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Consumables

- Table 28. Rest of Asia Pacific Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By Modality

- Table 29. Rest of Asia Pacific Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn) - By End User

- Table 30. Recent Inorganic Growth Strategies in the Fill Finish Manufacturing Market

- Table 31. Recent Organic Growth Strategies in the Fill Finish Manufacturing Market

- Table 32. Glossary of Terms, Fill Finish Manufacturing Market

List Of Figures

- Figure 1. Fill Finish Manufacturing Market Segmentation, By Country

- Figure 2. PEST Analysis

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Fill Finish Manufacturing Market Revenue (US$ Million), 2022 - 2030

- Figure 5. Fill Finish Manufacturing Market Share (%) - Product, 2022 and 2030

- Figure 6. Consumables Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 7. Instruments Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 8. Fill Finish Manufacturing Market Share (%) - Modality, 2022 and 2030

- Figure 9. Recombinant Proteins Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 10. Monoclonal Antibodies Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 11. Vaccines Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 12. Cell Therapies and Biological Therapies Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 13. Gene Therapies Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 14. Others Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 15. Fill Finish Manufacturing Market Share (%) - End User, 2022 and 2030

- Figure 16. Contract Manufacturing Organizations Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 17. Biopharmaceutical Companies Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 18. Others Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 19. Asia Pacific Fill Finish Manufacturing Market, by Key Countries - Revenue (2022) (US$ Million)

- Figure 20. Asia Pacific Fill Finish Manufacturing Market Breakdown by Key Countries, 2022 and 2030 (%)

- Figure 21. China Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 22. Japan Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 23. India Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 24. Australia Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 25. South Korea Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 26. Rest of Asia Pacific Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 27. Growth Strategies in the Fill Finish Manufacturing Market, 2020-2023

The Asia Pacific fill finish manufacturing market was valued at US$ 1,867.35 million in 2022 and is expected to reach US$ 4,202.36 million by 2030; it is estimated to grow at a CAGR of 10.7% from 2022 to 2030.

Low Business Costs in Emerging Markets Boosts Asia Pacific Fill Finish Manufacturing Market

Many Asian countries are emerging as attractive outsourcing locations for various biopharmaceutical manufacturers across the globe. Low manufacturing and operating costs in China, India, and other countries in Asia are the key factors boosting contract manufacturing. Moreover, recent developments in the biopharmaceutical industry in China and India indicate significant potential for the market. The growing pipelines of biologics and biosimilars are further opening new avenues for the contract manufacturers in APAC. Contract manufacturing mostly benefits early-stage drug innovators owing to lower operational costs. To meet the growing demand, many CMOs are expanding their manufacturing capabilities. For instance, in January 2020, STA Pharmaceutical Co., Ltd-a WuXi AppTec company-opened a new large-scale oligonucleotide active pharmaceutical ingredient (API) manufacturing facility in China.

Asia Pacific Fill Finish Manufacturing Market Overview

In Asia Pacific, China is the largest market for fill finish manufacturing. The growth of the market is primarily attributed to the rising technological advancements in fill finish manufacturing processes in China, increasing developments by the market players, the biopharmaceutical industry's expansion, and the growing prevalence of chronic diseases. There are more than 500 biological product/biopharmaceutical companies in China. Most of those involved in R&D were established by returnees from abroad or by Western/joint venture companies. Although estimates vary widely, analysts believe that the Chinese government spends more than US$ 600 million annually on biotech R&D through its funding initiatives. China's national and local governments also invest in quasi-venture capital companies that invest in IT enterprises.

The market players are expanding their business through organic and inorganic growth strategies. For instance, WuXi Biologics increased the capacity of prefilled syringes (PFS) to 17 million units yearly in June 2022 by opening its drug product factory in Wuxi, China.

The most recent D.P. facility operated by WuXi Bio, a contract development manufacturing organization (CDMO), is called DP5, and it has an advanced isolator filling line for reliable, continuous filling services. According to the company, this provides PFS with a variety of volume delivery options, including 1.25 mL, 3 mL, 1 mL, and 1 mL.

Asia Pacific Fill Finish Manufacturing Market Revenue and Forecast to 2030 (US$ Million)

Asia Pacific Fill Finish Manufacturing Market Segmentation

The Asia Pacific fill finish manufacturing market is segmented based on product, modality, end user, and country. Based on product, the Asia Pacific fill finish manufacturing market is bifurcated into consumables and instruments. The consumables segment held a larger market share in 2022. Furthermore, the consumables is sub segmented into prefilled syringes, glass vial/plastic vials, cartridges, and others.

In terms of modality, the Asia Pacific fill finish manufacturing market is segmented into recombinant proteins, monoclonal antibodies, vaccines, cell therapies and biological therapies, gene therapies, and others. The vaccines segment held the largest market share in 2022.

By end user, the Asia Pacific fill finish manufacturing market is categorized into contract manufacturing organizations, biopharmaceutical companies, and others. The contract manufacturing organizations segment held the largest market share in 2022.

Based on country, the Asia Pacific fill finish manufacturing market is segmented into China, Japan, India, Australia, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific fill finish manufacturing market share in 2022.

Becton Dickinson and Co, Gerresheimer AG, IMA Industria Macchine Automatiche SpA, Maquinaria Industrial Dara SL, Nipro Medical Asia Pacific NV, NNE AS, Optima Packaging Group Gmbh, Schott AG, SGD SA, Stevanato Group SpA, Syntegon Technology GmbH, and West Pharmaceutical Services Inc are some of the leading players operating in the Asia Pacific fill finish manufacturing market.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Asia Pacific Fill Finish Manufacturing Market Landscape

- 4.1 Overview

- 4.2 PEST Analysis

5. Asia Pacific Fill Finish Manufacturing Market - Key Industry Dynamics

- 5.1 Fill Finish Manufacturing Market - Key Industry Dynamics

- 5.2 Key Market Drivers

- 5.2.1 Growing Adoption of Prefilled Syringes for Parenteral Administration

- 5.2.2 Elevating Demand for Biologics

- 5.3 Key Market Restraints

- 5.3.1 Complexity in Biologics Manufacturing

- 5.4 Key Market Opportunities

- 5.4.1 Low Business Costs in Emerging Markets

- 5.5 Key Future Trends

- 5.5.1 Single-Use Systems for Aseptic Fill Finish

- 5.6 Impact of Drivers and Restraints:

6. Fill Finish Manufacturing Market - Asia Pacific Market Analysis

7. Asia Pacific Fill Finish Manufacturing Market Analysis - Product

- 7.1 Consumables

- 7.1.1 Overview

- 7.1.2 Consumables Market, Revenue and Forecast to 2030 (US$ Million)

- 7.2 Instruments

- 7.2.1 Overview

- 7.2.2 Instruments Market, Revenue and Forecast to 2030 (US$ Million)

8. Asia Pacific Fill Finish Manufacturing Market Analysis - Modality

- 8.1 Recombinant Proteins

- 8.1.1 Overview

- 8.1.2 Recombinant Proteins Market, Revenue and Forecast to 2030 (US$ Million)

- 8.2 Monoclonal Antibodies

- 8.2.1 Overview

- 8.2.2 Monoclonal Antibodies Market, Revenue and Forecast to 2030 (US$ Million)

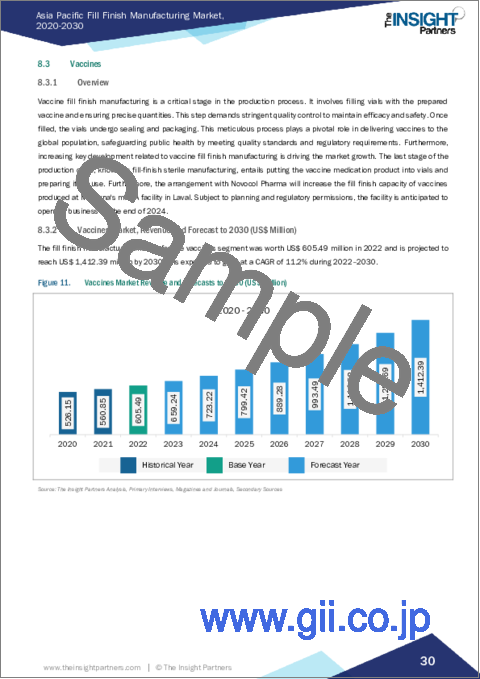

- 8.3 Vaccines

- 8.3.1 Overview

- 8.3.2 Vaccines Market, Revenue and Forecast to 2030 (US$ Million)

- 8.4 Cell Therapies and Biological Therapies

- 8.4.1 Overview

- 8.4.2 Cell Therapies and Biological Therapies Market, Revenue and Forecast to 2030 (US$ Million)

- 8.5 Gene Therapies

- 8.5.1 Overview

- 8.5.2 Gene Therapies Market, Revenue and Forecast to 2030 (US$ Million)

- 8.6 Others

- 8.6.1 Overview

- 8.6.2 Others Market, Revenue and Forecast to 2030 (US$ Million)

9. Asia Pacific Fill Finish Manufacturing Market Analysis - End User

- 9.1 Contract Manufacturing Organizations

- 9.1.1 Overview

- 9.1.2 Contract Manufacturing Organizations Market, Revenue and Forecast to 2030 (US$ Million)

- 9.2 Biopharmaceutical Companies

- 9.2.1 Overview

- 9.2.2 Biopharmaceutical Companies Market, Revenue and Forecast to 2030 (US$ Million)

- 9.3 Others

- 9.3.1 Overview

- 9.3.2 Others Market, Revenue and Forecast to 2030 (US$ Million)

10. Asia Pacific Fill Finish Manufacturing Market - Country Analysis

- 10.1 Asia Pacific Fill Finish Manufacturing Market Breakdown, by Country

- 10.1.1 China

- 10.1.2 China Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- 10.1.2.1 China Fill Finish Manufacturing Market Breakdown by Product

- 10.1.2.1.1 China Fill Finish Manufacturing Market Breakdown by Consumables

- 10.1.2.2 China Fill Finish Manufacturing Market Breakdown by Modality

- 10.1.2.3 China Fill Finish Manufacturing Market Breakdown by End User

- 10.1.2.1 China Fill Finish Manufacturing Market Breakdown by Product

- 10.1.3 Japan

- 10.1.3.1 Japan Fill Finish Manufacturing Market Breakdown by Product

- 10.1.3.1.1 Japan Fill Finish Manufacturing Market Breakdown by Consumables

- 10.1.3.2 Japan Fill Finish Manufacturing Market Breakdown by Modality

- 10.1.3.3 Japan Fill Finish Manufacturing Market Breakdown by End User

- 10.1.3.1 Japan Fill Finish Manufacturing Market Breakdown by Product

- 10.1.4 India

- 10.1.5 India Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- 10.1.5.1 India Fill Finish Manufacturing Market Breakdown by Product

- 10.1.5.1.1 India Fill Finish Manufacturing Market Breakdown by Consumables

- 10.1.5.2 India Fill Finish Manufacturing Market Breakdown by Modality

- 10.1.5.3 India Fill Finish Manufacturing Market Breakdown by End User

- 10.1.5.1 India Fill Finish Manufacturing Market Breakdown by Product

- 10.1.6 Australia

- 10.1.7 Australia Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- 10.1.7.1 Australia Fill Finish Manufacturing Market Breakdown by Product

- 10.1.7.1.1 Australia Fill Finish Manufacturing Market Breakdown by Consumables

- 10.1.7.2 Australia Fill Finish Manufacturing Market Breakdown by Modality

- 10.1.7.3 Australia Fill Finish Manufacturing Market Breakdown by End User

- 10.1.7.1 Australia Fill Finish Manufacturing Market Breakdown by Product

- 10.1.8 South Korea

- 10.1.9 South Korea Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- 10.1.9.1 South Korea Fill Finish Manufacturing Market Breakdown by Product

- 10.1.9.1.1 South Korea Fill Finish Manufacturing Market Breakdown by Consumables

- 10.1.9.2 South Korea Fill Finish Manufacturing Market Breakdown by Modality

- 10.1.9.3 South Korea Fill Finish Manufacturing Market Breakdown by End User

- 10.1.9.1 South Korea Fill Finish Manufacturing Market Breakdown by Product

- 10.1.10 Rest of Asia Pacific

- 10.1.11 Rest of Asia Pacific Fill Finish Manufacturing Market Revenue and Forecasts to 2030 (US$ Mn)

- 10.1.11.1 Rest of Asia Pacific Fill Finish Manufacturing Market Breakdown by Product

- 10.1.11.1.1 Rest of Asia Pacific Fill Finish Manufacturing Market Breakdown by Consumables

- 10.1.11.2 Rest of Asia Pacific Fill Finish Manufacturing Market Breakdown by Modality

- 10.1.11.3 Rest of Asia Pacific Fill Finish Manufacturing Market Breakdown by End User

- 10.1.11.1 Rest of Asia Pacific Fill Finish Manufacturing Market Breakdown by Product

11. Industry Landscape

- 11.1 Overview

- 11.2 Growth Strategies in the Fill Finish Manufacturing Market, 2020-2023

- 11.3 Inorganic Growth Strategies

- 11.3.1 Overview

- 11.4 Organic Growth Strategies

- 11.4.1 Overview

12. Company Profiles

- 12.1 IMA Industria Macchine Automatiche SpA

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Nipro Medical Europe NV

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Maquinaria Industrial Dara SL

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 SGD SA

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Optima Packaging Group Gmbh

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 NNE AS

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Product & Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Stevanato Group SpA

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 Syntegon Technology GmbH

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 West Pharmaceutical Services Inc

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 Gerresheimer AG

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 SWOT Analysis

- 12.10.6 Key Developments

- 12.11 Schott AG

- 12.11.1 Key Facts

- 12.11.2 Business Description

- 12.11.3 Products and Services

- 12.11.4 Financial Overview

- 12.11.5 SWOT Analysis

- 12.11.6 Key Developments

- 12.12 Becton Dickinson and Co

- 12.12.1 Key Facts

- 12.12.2 Business Description

- 12.12.3 Products and Services

- 12.12.4 Financial Overview

- 12.12.5 SWOT Analysis

- 12.12.6 Key Developments

13. Appendix

- 13.1 About Us

- 13.2 Glossary of Terms