|

|

市場調査レポート

商品コード

1389687

鎌状赤血球症治療薬の世界市場:市場規模・予測、世界・地域シェア、動向、成長機会分析:治療薬別・投与経路別・流通チャネル別Sickle Cell Disease Treatment Market Size and Forecasts, Global and Regional Share, Trends, and Growth Opportunity Analysis By Treatment, Route of Administration, and Distribution Channel |

||||||

|

|

|||||||

|

|||||||

| 鎌状赤血球症治療薬の世界市場:市場規模・予測、世界・地域シェア、動向、成長機会分析:治療薬別・投与経路別・流通チャネル別 |

|

出版日: 2023年11月07日

発行: The Insight Partners

ページ情報: 英文 245 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

世界の鎌状赤血球症治療薬市場は、2022年の11億6,000万米ドルから2030年には46億9,100万米ドルに成長すると予測され、2022年から2030年までのCAGRは19.1%と推定されます。鎌状赤血球症治療薬市場は、鎌状赤血球症の有病率の増加や、鎌状赤血球症に対する認識を高めるための政府・民間セクターの取り組みにより拡大しています。また、先進的な診断ツールの発売が増加していることや、効果的な治療薬を提供するための調査活動が活発化していることも、市場の成長をさらに後押ししています。しかし、鎌状赤血球症の治療オプションの不足などの要因が市場の成長を抑制しています。

鎌状赤血球症 (SCD) の治療計画は、健康維持と合併症治療の2つに分けられます。鎌状赤血球貧血には、ヘモグロビン遺伝子のユニークな変異に基づく遺伝子型と表現型の変異があります。鎌状赤血球貧血の有病率は高く、その重症度も世界中で上昇しています。WHOによると、世界人口の約5%が鎌状赤血球貧血やサラセミアなどのヘモグロビン疾患を阻害する遺伝子を持っています。National Library of Medicineに掲載された鎌状赤血球症に関する研究によると、毎年30万人以上の新生児が重度のヘモグロビン異常を持って生まれており、また2050年までに40万人の新生児が鎌状赤血球症になると予想されています。また、米国血液学会が2023年に発表した報告書によると、米国におけるSCDの推定患者数は約7万~10万人です。このように、世界中のさまざまな地域でマラリアと鎌状赤血球症の有病率が上昇していることが、マラリアと鎌状赤血球症治療薬市場の成長を後押ししています。

長年にわたり、小児科専用プログラムや研究イニシアティブによって、患者のケアや余命が大幅に改善されてきました。以下は、米国および世界でSCD治療に取り組むために資金を集めた財団の一部です。

米国血液学会財団では、以下のような具体的なプログラムを開発するために、50万米ドルの寄付を募集しています:

SCDに対する認識の改善と行動の促進

SCD患者を治療する血液専門医やその他の医療提供者の訓練と教育

SCDプログラムへの資金援助

SCD患者の治療基準・研究プログラム・臨床試験へのアクセスの改善

すべての段階 (早期診断から小児期、成人期まで) においてSCD患者を最適に治療するための、血液専門医やその他の医療従事者の支援

Doris Duke Foundationでは、ヘモグロビンの機能を回復させるための遺伝子組み換えや薬物療法を含む、SCDの先進的な治療法を支援しています。プロジェクトを支援するための年間直接経費は150,000~300,000米ドルに達し、さらに3年ごとに10%の間接経費がかかります。この援助は、以下のような臨床研究を支援することを目的としています:

臨床における鎌状赤血球症向け高度遺伝子治療 (遺伝子添加やゲノム編集など)

赤血球機能を回復させるためのグロビン制御メカニズムの構築

死滅を最小限に抑え、予後を改善するための骨髄移植手技の高度化

2021年8月、部族問題省はICMRと共同で、スクリーニングを含む鎌状赤血球貧血に取り組むための助成金を求める州に720万米ドルをリリースしました。部族問題省 (MoTA) の部族研究所 (TRI) 部門は、サー・ガンガ・ラーム病院で鎌状赤血球症に関する調査研究プログラムを認可しました。また、「鎌状赤血球貧血およびサラセミア患者に対する診断、IECおよび栄養サポート」と呼ばれるプロジェクトも実施されました。

2021年2月、NovartisとBill & Melinda Gates Foundationは、鎌状赤血球症に対する利用可能な生体内遺伝子治療を決定・開発するために協力しました。728万米ドルが提供されたこのパートナーシップは、鎌状赤血球症の有病率が高い低資源地域、特に世界の罹患者の約80%がいるサハラ以南のアフリカで使用できるような、手頃な価格でシンプルな治療法を開発することを目的としています。この共同研究は、SCDを治療するための現在の遺伝子治療アプローチに含まれる生体内ステップのいくつかを回避できる、既製の治療法を生み出すことを期待しています。

2022年3月、国際的な研究者チームは、ガーナの鎌状赤血球症の子どもたちの全遺伝子コードの配列を決定するため、米国国立衛生研究所 (NIH) から300万米ドルの助成金を受け取っています。ガーナの鎌状赤血球症の子ども500人のDNA全塩基配列を解析することにより、研究チームは、患者の管理とケアの改善に役立つ、この病気の潜在的な遺伝的修飾因子を特定することを期待しています。これらの子供たちは、アフリカ鎌状赤血球症ゲノミクス・ネットワーク (SickleGenAfrica) の参加者です。Ofori-Acquahが率いる米国NIHの資金による540万米ドルの国際プロジェクトも、遺伝がアフリカ人のSCDの進行にどのように影響するかを理解することに重点を置いています。

治療薬別の洞察

鎌状赤血球症治療薬市場は治療薬に基づき、ジェネリック医薬品とオリジネーターに区分されます。2022年の市場シェアはオリジネーターが最大でした。鎌状赤血球症は、ヘモグロビンの欠陥を特徴とする遺伝性の血液疾患です。赤血球中のヘモグロビンが酸素を運搬する能力が阻害されます。

投与経路別の洞察

投与経路別では、マラリア治療薬市場は経口薬と非経口薬・静脈注射薬に二分されます。2022年の市場シェアは経口剤が最大でしたが、予測期間中は非経口剤が最も高いCAGRを記録すると予想されます。経口薬剤送達は、高い患者コンプライアンス、非侵襲性、最小限の無菌性制約、費用対効果、剤形設計の柔軟性、製造プロセスの容易さを提供するため、最も好まれ、適切な薬剤投与経路です。投与の容易さや長期的なコスト効率といった利点は、経口薬の採用を促進する主な要因です。

流通チャネル別の洞察

流通チャネル別では、マラリア治療薬市場は直接入札、病院薬局、小売薬局、オンライン薬局、その他に区分されます。2022年の市場シェアは直接入札セグメントが最大でしたが、予測期間中はオンライン薬局セグメントが最も高いCAGRを記録すると予想されます。

マラリア治療市場に関するレポート作成時に参照した主な一次情報および二次情報には、世界保健機関 (WHO)、米国国勢調査局、CDCなどがあります。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 鎌状赤血球症治療薬市場の情勢

- PEST分析:鎌状赤血球症治療薬

第5章 鎌状赤血球症治療薬市場:主な産業力学

- 主な市場促進要因

- 市場抑制要因

- 鎌状赤血球症の治療オプションの欠如

- 市場機会

- 今後の動向

- 影響度の分析

第6章 鎌状赤血球症治療薬市場:世界市場の分析

- 鎌状赤血球症治療薬市場の収益 (2022年~2030年)

- 市場収益の分析:地域別 (2022年~2030年)

- 鎌状赤血球症

- 鎌状赤血球症 (SCD) 向け資金提供

- 鎌状赤血球症向け医療費償還シナリオ

第7章 鎌状赤血球症治療薬市場の収益と予測:治療薬別 (2030年まで)

- 鎌状赤血球症治療薬市場:収益シェア、治療薬別 (%、2022年、2030年)

- オリジネーター (創薬企業)

- ジェネリック医薬品

第8章 鎌状赤血球症治療薬市場の収益と予測:投与経路別 (2030年まで)

- 鎌状赤血球症治療薬市場:収益シェア、投与経路別 (%、2022年、2030年)

- 経口薬

- 非経口薬

第9章 鎌状赤血球症治療薬市場の収益と予測:流通チャネル別 (2030年まで)

- 鎌状赤血球症治療薬市場:収益シェア、r流通チャネル別 (%、2022年、2030年)

- 直接入札

- 病院薬局

- 小売薬局

- オンライン薬局

- その他

第10章 鎌状赤血球症治療薬市場:地域別分析

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- 中南米

第11章 鎌状赤血球症治療薬市場:産業情勢

- 鎌状赤血球症治療薬市場における成長戦略

- 無機的成長戦略

- 有機的成長戦略

第12章 企業プロファイル

- Cipla Ltd

- Sun Pharmaceutical Industries Ltd

- Sanofi SA

- GSK Plc

- Novartis AG

- Pfizer Inc

- Emmaus Life Sciences Inc

- AdvaCare Pharma USA LLC

- VLP Therapeutics LLC

- Lupin Ltd

- Teva Pharmaceutical Industries Ltd

第13章 付録

List Of Tables

List Of Figures

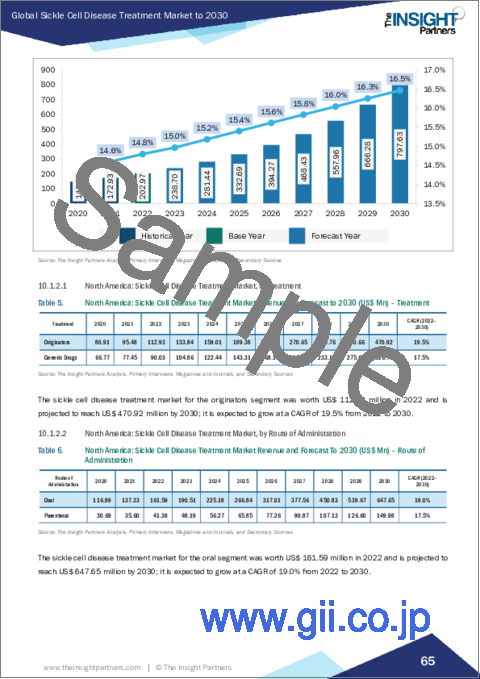

The sickle cell disease treatment market is expected to grow from US$ 1.160 billion in 2022 to US$ 4.691 billion by 2030; it is estimated to grow at a CAGR of 19.1% from 2022 to 2030. The market for sickle cell disease treatment is growing due to the increasing prevalence of sickle cell disease and the government and private sector's initiatives to raise awareness about sickle cell disease. Also, the increasing number of launches of advanced diagnostic tools and rising research activities to provide effective therapeutics are further driving the growth of the market. However, factors such as lack of sickle cell disease treatment options are restraining the market growth.

The treatment plan for sickle cell disease (SCD) can be divided into two categories: maintaining health and treating complications. Sickle cell anemia has genotypic and phenotypic variants that are based on unique mutations in hemoglobin genes. There is a high prevalence of the disease as well as a rise in its severity across the globe. According to the WHO, approximately 5% of the world's population has genes inhibiting hemoglobin diseases such as sickle cell anemia and thalassemia. According to a study on sickle cell disease published in the National Library of Medicine, more than 300,000 babies are born with severe hemoglobin disorders each year; also, 400,000 newborns are expected to have sickle cell disease by 2050. In addition, according to a published report in 2023 by the American Society of Hematology, the estimated number of people suffering from SCD in the US is approximately 70,000-100,000. Thus, the rising prevalence of malaria and sickle cell disease in different regions across the globe boosts the malaria and sickle cell disease treatment market growth.

Over the years, dedicated pediatric programs and research initiatives have significantly improved patient care and life expectancy. Following are a few foundations that have raised funds to address SCD treatment in the US and around the world.

American Society of Hematology Foundation seeks to raise US$ 500,000 in private charitable care to develop specific programs that focus on:

Raising awareness and encouraging action against SCD

Training and educating hematologists and other healthcare providers who treat SCD patients

Alleviating funding of SCD programs

Improving standards of care, research programs, and access to clinical trials for SCD people

Supporting workforce of hematologists and other health care professionals to optimally treat SCD patients throughout all stages-i.e., early diagnosis through childhood and into adulthood

Doris Duke Foundation grant awards to support advanced healing methods for SCD, including gene modification and drug therapies to restore hemoglobin function. The annual direct costs to support projects range from US$ 150,000-300,000 plus 10% indirect costs for each of three years. This award aims to support clinical research that will support:

Advanced gene therapies such as gene addition and genome editing for sickle cell disease in clinics

Build on globin regulatory mechanisms to restore red blood cell function

Advance bone marrow transplant procedures to minimize deadliness and improve outcomes

In August 2021, the Ministry of Tribal Affairs, in collaboration with ICMR, released US$ 7.2 million to the states seeking grants to tackle sickle cell anemia, including screening. The Tribal Research Institute (TRI) Division of the Ministry of Tribal Affairs (MoTA) sanctioned a research study program at Sir Ganga Ram Hospital on sickle cell disease. Also, a project called "'Diagnosis, IEC and Nutri support for sickle cell anemia and Thalassemia affected patients" was undertaken.

In February 2021, Novartis and the Bill & Melinda Gates Foundation collaborated to determine and develop an accessible in vivo gene therapy for sickle cell disease. The partnership, funded with US$ 7.28 million, aims to develop a treatment that is affordable and simple enough to be used in low-resource areas with a high prevalence of SCD, particularly sub-Saharan Africa, where about 80% of affected people worldwide are located. The collaboration hopes to create an off-the-shelf treatment that can bypass some of the in vivo steps involved in current gene therapy approaches to treat SCD, which are costly, complex, and crafted for individual patients.

In March 2022, a team of international researchers received a grant of US$ 3 million from the National Institutes of Health (NIH) to sequence the whole genetic code of children with sickle cell disease in Ghana. By analyzing the whole DNA sequence of 500 Ghanaian children with SCD, the researchers hope to identify potential genetic modifiers of the disease that will help improve the management and care of patients. These children are the participants in the Sickle Cell Disease Genomics Network of Africa (SickleGenAfrica). A US$ 5.4-million, NIH-funded international project led by Ofori-Acquah also focused on understanding how genetics influence SCD progression in Africans.

Treatment-Based Insights

The sickle cell disease treatment market is segmented based on treatment into generic drugs and originators. Originators segment held the largest market share in 2022. Sickle cell disease is an inherited blood disorder marked by defective hemoglobin. It inhibits the capability of hemoglobin in red blood cells to carry oxygen.

Route of Administration-Based Insights

Based on route of administration, the malaria treatment market is bifurcated into oral and parenteral & intravenous. The oral segment accounted for the largest share of the market in 2022; however, the parenteral segment is expected to register the highest CAGR during the forecast period. Oral drug delivery is the most preferred and suitable route of drug administration as it offers high patient compliance, non-invasiveness, least sterility constraints, cost-effectiveness, flexibility in the design of dosage form and ease in the manufacturing process. Benefits such as ease of administration and long-term cost efficiency are major factors fueling the adoption of oral drugs.

Distribution Channel-Based Insights

Based on distribution channels, the malaria treatment market is segmented into direct tender, hospital pharmacies, retail pharmacies, online pharmacies, and others. The direct tender segment accounted for the largest share of the market in 2022; however, the online pharmacies segment is expected to register the highest CAGR during the forecast period.

A few of the major primary and secondary sources referred to while preparing the report on the malaria treatment market are the World Health Organization (WHO), the US Census Bureau, and CDC, among others.

Reasons to Buy:

- Save and reduce time carrying out entry-level research by identifying the growth, size, leading players, and segments in the malaria treatment market.

- Highlights key business priorities in order to assist companies to realign their business strategies.

- The key findings and recommendations highlight crucial progressive industry trends in the global malaria treatment market, thereby allowing players across the value chain to develop effective long-term strategies.

- Develop/modify business expansion plans by using substantial growth offering developed and emerging markets.

- Scrutinize in-depth global market trends and outlook coupled with the factors driving the market, as well as those hindering it.

- Enhance the decision-making process by understanding the strategies that underpin security interest with respect to client products, segmentation, pricing and distribution.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights - Malaria

- 2.2 Key Insights – Sickle Cell Disease

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Sickle Cell Disease Treatment Market Landscape

- 4.1 Overview

- 4.2 PEST Analysis – Sickle Cell Disease Treatment

5. Sickle Cell Disease Treatment Market - Key Industry Dynamics

- 5.1 Key Market Drivers:

- 5.2 Market Restraints

- 5.2.1 Lack of Sickle Cell Disease Treatment Options

- 5.3 Market Opportunities

- 5.4 Future Trends

- 5.5 Impact Analysis 44

6. Sickle Cell Disease Treatment Market - Global Market Analysis

- 6.1 Sickle Cell Disease Treatment Market Revenue (US$ million), 2022 – 2030

- 6.2 Geography Analysis Market Revenue (US$ million), 2022 – 2030

- 6.3 Sickle Cell Disease

- 6.4 Fundings for Sickle Cell Disease (SCD)

- 6.5 Reimbursement Scenario for Sickle Cell Disease

7. Sickle Cell Disease Treatment Market – Revenue and Forecast to 2030 – by Treatment

- 7.1 Overview

- 7.2 Sickle Cell Disease Treatment Market Revenue Share, by Treatment 2022 & 2030 (%)

- 7.3 Originators

- 7.4 Generic Drugs

8. Sickle Cell Disease Treatment Market – Revenue and Forecast to 2030 – by Route of Administration

- 8.1 Overview

- 8.2 Sickle Cell Disease Treatment Market Revenue Share, by Route of Administration 2022 & 2030 (%)

- 8.3 Oral .

- 8.4 Parenteral

9. Sickle Cell Disease Treatment Market – Revenue and Forecast to 2030 – by Distribution Channel

- 9.1 Overview

- 9.2 Sickle Cell Disease Treatment Market Revenue Share, by Distribution Channel 2022 & 2030 (%)

- 9.3 Direct Tender

- 9.4 Hospital Pharmacies

- 9.5 Retail Pharmacies

- 9.6 Online Pharmacies

- 9.7 Others

10. Sickle Cell Disease Treatment Market - Geographical Analysis

- 10.1 North America Sickle Cell Disease Treatment Market, Revenue and Forecast To 2030

- 10.2 Europe Sickle Cell Disease Treatment Market, Revenue and Forecast To 2030

- 10.3 Asia Pacific Sickle Cell Disease Treatment Market, Revenue and Forecast To 2030

- 10.4 Middle East & Africa Sickle Cell Disease Treatment Market, Revenue and Forecast To 2030

- 10.5 South & Central America Sickle Cell Disease Treatment Market, Revenue and Forecast To 2030

11. Sickle Cell Disease Treatment Market Industry Landscape

- 11.1 Overview

- 11.2 Growth Strategies in the Sickle Cell Disease Treatment Market

- 11.3 Inorganic Growth Strategies

- 11.4 Organic Growth Strategies

12. Company Profiles

- 12.1 Cipla Ltd

- 12.2 Sun Pharmaceutical Industries Ltd

- 12.3 Sanofi SA

- 12.4 GSK Plc

- 12.5 Novartis AG

- 12.6 Pfizer Inc

- 12.7 Emmaus Life Sciences Inc

- 12.8 AdvaCare Pharma USA LLC

- 12.9 VLP Therapeutics LLC

- 12.10 Lupin Ltd

- 12.11 Teva Pharmaceutical Industries Ltd