|

|

市場調査レポート

商品コード

1372555

ヘルスエコノミクス&アウトカムリサーチサービスの中東・西アフリカ市場規模および予測、地域シェア、動向、成長機会分析対象:サービス別、サービスプロバイダー別、エンドユーザー別、地域別MEWA Health Economics & Outcomes Research Services Market Size and Forecast, Regional Share, Trends, and Growth Opportunity Analysis Coverage: By Service, Service Provider, End User, and Region |

||||||

|

|

|||||||

|

|||||||

| ヘルスエコノミクス&アウトカムリサーチサービスの中東・西アフリカ市場規模および予測、地域シェア、動向、成長機会分析対象:サービス別、サービスプロバイダー別、エンドユーザー別、地域別 |

|

出版日: 2023年09月26日

発行: The Insight Partners

ページ情報: 英文 88 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

中東・西アフリカの医療経済&アウトカム調査(HEOR)サービス市場は、2022年の3,447万米ドルから2030年には5,790万米ドルに達すると予測され、2022年から2030年までのCAGRは6.7%で成長する見込みです。バイオテクノロジー・製薬企業や研究開発、ヘルスケア支出の増加などの要因が、中東・西アフリカの医療経済・アウトカム調査(HEOR)サービス市場の成長を促進すると予想されます。さらに、精密医療の出現も、予測期間中の中東・西アフリカの医療経済&アウトカム調査(HEOR)サービス市場の成長を促進すると予想されます。しかし、実世界データ(RWD)へのアクセス制限が中東・西アフリカの医療経済&アウトカム調査(HEOR)サービス市場の成長を阻害する可能性があります。

ヘルスケアのデジタル化が今後の中東・西アフリカの医療経済&アウトカム調査(HEOR)サービス市場を押し上げる

ヘルスケア産業は、情報技術(IT)、人工知能(AI)、デジタル技術の統合によって大きく発展してきました。ヘルスケア業界では、デジタル化がポジティブな影響を与えています。ヘルスケアのデジタル化の成果には、電子カルテ、遠隔医療、ビッグデータなどがあります。政府、NGO、非公開会社、ソフトウェア会社が関与するいくつかのe-ヘルスシステムは、すべての利害関係者間の調整を必要とし、これらのシステムを非冗長かつ効果的なものにしています。関係者が同期したアプローチをとることで、時間の節約と生産性の向上が期待できます。

中東では、予防措置や診断から介入やセルフケア管理まで、ヘルスケアの提供方法に革命をもたらした技術の進歩により、デジタル・ヘルス・システムの導入が増加しています。デジタルヘルス技術はCOVID-19パンデミック以前から台頭していたが、パンデミック時にその開発、応用、普及が加速しました。デジタルヘルス・ソリューションは、ケアの継続性を確保するための重要なツールとなっています。デジタルヘルスは、ヘルスケアへのアクセス、ケアの質、労働力の生産性を向上させることができるため、政府にとって魅力的な提案です。Innovation Origins誌に掲載された「デジタルヘルスが中東のヘルスケア提供に革命を起こす」と題する記事によると、同地域のデジタルヘルス市場は2028年までに100億米ドル規模になると推定されています。デジタルヘルスは、サウジアラビア王国(KSA)とアラブ首長国連邦(UAE)における患者のケアと福祉の向上に役立っています。このように、ヘルスケアにおけるデジタル化は、既存プレーヤーや新規市場参入者に成長機会を提供しています。

アフリカでは、不十分で不足した医療インフラ、医療・救急医療資源の地域格差、患者情報の不足により、非伝染性疾患や感染症の負担が増大しています。バイエル、メルク、サノフィ、ピエール・ファーブルは、アフリカのeヘルス新興企業に指導と資金援助を提供している多国籍製薬会社の例です。ケニアの新興企業KEHEALAは、患者の行動介入と疾病管理を可能にするモバイル・ヘルスケア・プラットフォームを開発しました。ナイジェリアのWellNewMeは、アルゴリズム・アプローチを使って個人の健康リスクを評価するオンライン・プラットフォームを開発しました。

このように、このような事例はヘルスケア業界を変革し、HEORサービスプロバイダーが意思決定者に最適なテクノロジーを選択する際の指針となることが期待されます。また、ヘルスケアプロバイダーがコスト効率よく健康結果を改善するのに役立ち、市場成長を押し上げると思われます。

中東・西アフリカの医療経済&アウトカム調査(HEOR)サービス市場は、サービス、サービスプロバイダー、エンドユーザー、地域によって区分されます。サービスに基づいて、中東・西アフリカの医療経済&アウトカム調査(HEOR)サービス市場は、臨床アウトカム、経済モデリング/評価、市場アクセスソリューションと償還、実データ分析と情報システムに区分されます。臨床アウトカム分野が2022年に最大の市場シェアを占めました。実世界データ分析・情報システム分野は、2022~2030年のCAGRが7.5%と最も高くなると予測されています。中東・西アフリカの医療経済&アウトカム調査(HEOR)サービス市場は、サービスプロバイダー別に見ると、委託研究機関とコンサルタント会社に二分されます。2022年の市場シェアは受託研究機関が大きく、2022-2030年のCAGRは受託研究機関が上回ると予測されます。中東・西アフリカの医療経済&アウトカム調査(HEOR)サービス市場は、エンドユーザー別に、バイオテクノロジー/製薬会社、ヘルスケア支払者、政府機関、ヘルスケアプロバイダーに区分されます。バイオテクノロジー/製薬企業セグメントは2022年に最大の市場シェアを占め、2022年から2030年にかけて最も高いCAGRを記録すると予測されています。

国際医療経済学アウトカム調査学会(ISPOR)、臨床経済審査機構(ICER)、食品医薬品局(FDA)、国立がん研究所(NCI)、保健予防省(MoHAP)、国家変革プログラム(NTP)などは、中東・西アフリカの医療経済学&アウトカム調査(HEOR)サービス市場に関するレポート作成時に参照した一次情報と二次情報の一部です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要な洞察

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 中東・西アフリカの医療経済&アウトカムリサーチ(HEOR)市場- 市場情勢

- 中東・西アフリカのPEST分析

第5章 中東・西アフリカの医療経済&アウトカムリサーチ(HEOR)市場:国別分析

- 主要市場促進要因

- 成長するバイオテクノロジー・製薬企業と医薬品開発

- ヘルスケア支出の増加

- 市場抑制要因

- 実世界データ(RWD)へのアクセス制限

- 市場機会

- プレシジョン・メディシンの出現

- 今後の動向

- ヘルスケアにおけるデジタル化

- 影響分析

第6章 中東・西アフリカの医療経済・アウトカムリサーチ(HEOR)市場:国別分析

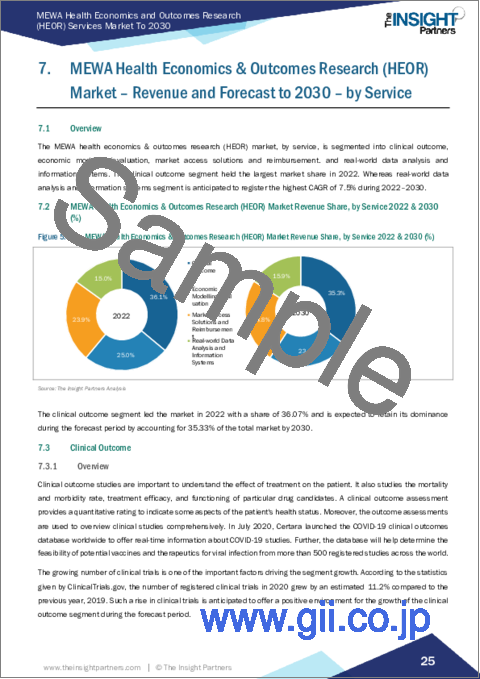

第7章 中東・西アフリカの医療経済&アウトカムリサーチ(HEOR)市場-2030年までの収益と予測-サービス別

- 中東・西アフリカの医療経済&アウトカムリサーチ(HEOR)市場:2022年・2030年サービス別収益シェア(%)

- 臨床アウトカム

- 経済モデリング/評価

- 市場参入ソリューションと償還

- 実世界データ分析と情報システム

第8章 中東・西アフリカの医療経済&アウトカムリサーチ(HEOR)市場:収益と2030年までの予測:サービスプロバイダー別

- 中東・西アフリカのヘルスエコノミクス&アウトカムリサーチ(HEOR)市場収益シェア、サービスプロバイダー別2022年&2030年(%)

- 調査受託機関

- コンサルタント会社

第9章 中東・西アフリカの医療経済&アウトカムリサーチ(HEOR)市場-2030年までの収益と予測-エンドユーザー別

- 中東・西アフリカのヘルスエコノミクス&アウトカムリサーチ(HEOR)市場エンドユーザー別2022年・2030年収益シェア(%)

- バイオテクノロジー/製薬会社

- ヘルスケアペイヤー

- 政府機関

- ヘルスケアプロバイダー

第10章 中東・西アフリカの医療経済&アウトカムリサーチ(HEOR)市場:収益と2030年までの予測:国別分析

- 中東・西アフリカ

第11章 中東・西アフリカの医療経済&アウトカム調査(HEOR)市場-業界情勢

- 有機的展開

- 無機的展開

第12章 企業プロファイル

- PharmaLex GmbH

- ICON Plc

- IQVIA Holdings Inc

- Syneos Health Inc

- Optum Inc

- Value In Research

- ExlService Holdings, Inc.

- Clarivate Plc

- CCHO

第13章 付録

List Of Tables

- Table 1. MEWA Health economics & outcomes research (HEOR) Market Segmentation

- Table 2. MEWA: Health Economics & Outcomes Research (HEOR) Market, by Service - Revenue and Forecast to 2030 (USD Million)

- Table 3. MEWA: Health Economics & Outcomes Research (HEOR) Market, by Service Provider - Revenue and Forecast to 2030 (USD Million)

- Table 4. MEWA: Health Economics & Outcomes Research (HEOR) Market, by End User - Revenue and Forecast to 2030 (USD Million)

- Table 5. Saudi Arabia Health Economics & Outcomes Research (HEOR) Market, by Service - Revenue and Forecast to 2030 (US$ Million)

- Table 6. Saudi Arabia: Health Economics & Outcomes Research (HEOR) Market, by Service Provider - Revenue and Forecast to 2030 (USD Million)

- Table 7. Saudi Arabia Health Economics & Outcomes Research (HEOR) Market, by End User - Revenue and Forecast to 2030 (US$ Million)

- Table 8. UAE Health Economics & Outcomes Research (HEOR) Market, by Service - Revenue and Forecast to 2030 (US$ Million)

- Table 9. UAE: Health Economics & Outcomes Research (HEOR) Market, by Service Provider - Revenue and Forecast to 2030 (USD Million)

- Table 10. UAE Health Economics & Outcomes Research (HEOR) Market, by End User - Revenue and Forecast to 2030 (US$ Million)

- Table 11. Qatar Health Economics & Outcomes Research (HEOR) Market, by Service - Revenue and Forecast to 2030 (US$ Million)

- Table 12. Qatar: Health Economics & Outcomes Research (HEOR) Market, by Service Provider - Revenue and Forecast to 2030 (USD Million)

- Table 13. Qatar Health Economics & Outcomes Research (HEOR) Market, by End User - Revenue and Forecast to 2030 (US$ Million)

- Table 14. Kuwait Health Economics & Outcomes Research (HEOR) Market, by Service - Revenue and Forecast to 2030 (US$ Million)

- Table 15. Kuwait: Health Economics & Outcomes Research (HEOR) Market, by Service Provider - Revenue and Forecast to 2030 (USD Million)

- Table 16. Kuwait Health Economics & Outcomes Research (HEOR) Market, by End User - Revenue and Forecast to 2030 (US$ Million)

- Table 17. Rest of MEWA Health Economics & Outcomes Research (HEOR) Market, by Service - Revenue and Forecast to 2030 (US$ Million)

- Table 18. Rest of MEWA: Health Economics & Outcomes Research (HEOR) Market, by Service Provider - Revenue and Forecast to 2030 (USD Million)

- Table 19. Rest of MEWA Health Economics & Outcomes Research (HEOR) Market, by End User - Revenue and Forecast to 2030 (US$ Million)

- Table 20. Organic Developments Done by Companies

- Table 21. Inorganic Developments Done by Companies

- Table 22. Glossary of Terms

List Of Figures

- Figure 1. MEWA: PEST Analysis

- Figure 2. MEWA Health Economics & Outcomes Research (HEOR) Market - Key Industry Dynamics

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue Forecast and Analysis - 2020-2030

- Figure 5. MEWA Health Economics & Outcomes Research (HEOR) Market Revenue Share, by Service 2022 & 2030 (%)

- Figure 6. Clinical Outcome: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 7. Economic Modelling/Evaluation: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 8. Market Access Solutions and Reimbursement: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 9. Real-World Data Analysis and Information Systems: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 10. MEWA Health Economics & Outcomes Research (HEOR) Market Revenue Share, By Service Provider 2022 & 2030 (%)

- Figure 11. Contract Research Organizations: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 12. Consultancy: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 13. MEWA Health Economics & Outcomes Research (HEOR) Market Revenue Share, By End User 2022 & 2030 (%)

- Figure 14. Biotech/Pharma Companies: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 15. Healthcare Payers: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 16. Government Organizations: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 17. Healthcare Providers: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 18. MEWA: Health Economics & Outcomes Research (HEOR) Market, by Key Country - Revenue (2022) (US$ Million)

- Figure 19. MEWA: Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (USD Million)

- Figure 20. MEWA: Health Economics & Outcomes Research (HEOR) Market, by Country, 2022 & 2030 (%)

- Figure 21. Saudi Arabia: Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 22. UAE: Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 23. Qatar: Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 24. Kuwait: Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 25. Rest of MEWA: Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

The MEWA health economics & outcomes research (HEOR) services market is projected to reach US$ 57.90 million by 2030 from US$ 34.47 million in 2022; it is expected to grow at a CAGR of 6.7% from 2022 to 2030. The factors such as growing biotechnology & pharmaceutical companies and drug developments and increasing healthcare spending are expected to drive the MEWA health economics & outcomes research (HEOR) services market growth. Moreover, emergence of precision medicines is also expected to foster the MEWA health economics & outcomes research (HEOR) services market growth during the forecast period. However, the restrictions on access to real-world data (RWD) may hinder the MEWA health economics & outcomes research (HEOR) services market growth.

Digitalization in Healthcare to Boost the MEWA Health Economics & Outcomes Research (HEOR) Services Market in Future

The healthcare industry has significantly evolved owing to the integration of information technology (IT), artificial intelligence (AI), and digital technology. There have been positive impacts of digitalization in the healthcare industry. Some healthcare digitalization results include electronic medical records, telemedicine, and big data. Several e-health systems involving governments, NGOs, private investors, and software companies need coordination between all their stakeholders, making these systems nonredundant and effective. A synchronized approach by the parties involved would save time and increase productivity.

In the Middle East, the adoption of digital health systems has increased due to technological advancements that have revolutionized how healthcare is delivered-from preventive measures and diagnosis to interventions and self-care management. Digital health technologies were already on the rise before the COVID-19 pandemic, but their development, application, and distribution accelerated during the pandemic. Digital health solutions have become an important tool to ensure continuity of care. Digital health is an attractive proposition for governments because it can improve access to healthcare, quality of care, and workforce productivity. According to an article titled "Digital Health Revolutionizes Healthcare Delivery in the Middle East," published in Innovation Origins, the digital health market is estimated to be worth US$ 10 billion by 2028 in the region. Digital health has helped improve patient care and well-being in the Kingdom of Saudi Arabia (KSA) and the UAE. Thus, digitalization in healthcare has offered growth opportunities for existing players and new market entrants.

Africa faces a growing burden of noncommunicable and infectious diseases due to inadequate and deficient health infrastructure, regional disparities in medical and paramedical resources, and a lack of patient information. eHealth companies are already a reality on the continent, offering diverse services and contributing to better healthcare access and patient well-being. Bayer, Merck, Sanofi, and Pierre Fabre are examples of multinational pharmaceutical companies providing mentoring and financial support to African e-health start-ups. Kenyan start-up KEHEALA has developed a mobile healthcare platform that enables behavioral interventions and disease management for patients. WellNewMe in Nigeria has developed an online platform to assess the health risks of individuals using an algorithmic approach.

Thus, such instances are expected to transform the healthcare industry and help the HEOR service providers guide decision-makers in choosing the best technologies. It would also help healthcare providers improve health results cost-effectively, thereby boosting market growth.

The MEWA health economics & outcomes research (HEOR) services market is segmented on the basis of service, service provider, end user, and region. Based on service, the MEWA health economics & outcome research (HEOR) services market is segmented into clinical outcome, economic modelling/evaluation, market access solutions and reimbursement, and real-world data analysis and information systems. The clinical outcome segment held the largest market share in 2022. The real-world data analysis and information systems segment is predicted to register the highest CAGR of 7.5% during 2022-2030. The MEWA health economics & outcome research (HEOR) services market, by service provider, is bifurcated into contract research organizations and consultancy. The contract research organizations segment held a larger market share in 2022 and is anticipated to register a higher CAGR during 2022-2030. The MEWA health economics & outcome research (HEOR) services market, by end user, is segmented into biotech/pharma companies, healthcare payers, government organizations, and healthcare providers. The biotech/pharma companies segment held the largest market share in 2022 and is anticipated to register the highest CAGR during 2022-2030.

The International Society For Pharmacoeconomics And Outcomes Research (ISPOR), Institute For Clinical And Economic Review (ICER), Food and Drug Administration (FDA), National Cancer Institute (NCI), Ministry Of Health And Prevention (MoHAP), and National Transformation Program (NTP) are among some of the primary and secondary sources referred to while preparing the report on the MEWA health economics & outcomes research (HEOR) services market.

Reasons to Buy:

- Save and reduce time carrying out entry-level research by identifying the growth, size, leading players, and segments in the MEWA health economics & outcomes research (HEOR) services market.

- Highlights key business priorities in order to assist companies to realign their business strategies.

- The key findings and recommendations highlight crucial progressive industry trends in the MEWA health economics & outcomes research (HEOR) services market, thereby allowing players across the value chain to develop effective long-term strategies.

- Develop/modify business expansion plans by using substantial growth offering developed and emerging markets.

- Scrutinize in-depth global market trends and outlook coupled with the factors driving the MEWA health economics & outcomes research (HEOR) services market, as well as those hindering it.

- Enhance the decision-making process by understanding the strategies that underpin security interest with respect to client products, segmentation, pricing, and distribution.

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. MEWA Health Economics & Outcomes Research (HEOR) Market - Market Landscape

- 4.1 Overview

- 4.1.1 MEWA PEST Analysis

5. MEWA Health Economics & Outcomes Research (HEOR) Market - Country Analysis

- 5.1 Key Market Drivers:

- 5.1.1 Growing Biotechnology & Pharmaceutical Companies and Drug Development

- 5.1.2 Increasing Healthcare Spending

- 5.2 Market Restraints

- 5.2.1 Restrictions on Access to Real-World Data (RWD)

- 5.3 Market Opportunities

- 5.3.1 Emergence of Precision Medicines

- 5.4 Future Trends

- 5.4.1 Digitalization in Healthcare

- 5.5 Impact Analysis:

6. MEWA Health Economics & Outcomes Research (HEOR) Market - Country Analysis

- 6.1 MEWA Health Economics & Outcomes Research (HEOR) Market Revenue Forecast and Analysis

7. MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 - by Service

- 7.1 Overview

- 7.2 MEWA Health Economics & Outcomes Research (HEOR) Market Revenue Share, by Service 2022 & 2030 (%)

- 7.3 Clinical Outcome

- 7.3.1 Overview

- 7.3.2 Clinical Outcome: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- 7.4 Economic Modelling/Evaluation

- 7.4.1 Overview

- 7.4.2 Economic Modelling/Evaluation: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- 7.5 Market Access Solutions and Reimbursement

- 7.5.1 Overview

- 7.5.2 Market Access Solutions and Reimbursement: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- 7.6 Real-World Data Analysis and Information Systems

- 7.6.1 Overview

- 7.6.2 Real-World Data Analysis and Information Systems: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

8. MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 - By Service Provider

- 8.1 Overview

- 8.2 MEWA Health Economics & Outcomes Research (HEOR) Market Revenue Share, By Service Provider 2022 & 2030 (%)

- 8.3 Contract Research Organizations

- 8.3.1 Overview

- 8.3.2 Contract Research Organizations: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- 8.4 Consultancy

- 8.4.1 Overview

- 8.4.2 Consultancy: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

9. MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 - By End User

- 9.1 Overview

- 9.2 MEWA Health Economics & Outcomes Research (HEOR) Market Revenue Share, By End User 2022 & 2030 (%)

- 9.3 Biotech/Pharma Companies

- 9.3.1 Overview

- 9.3.2 Biotech/Pharma Companies: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- 9.4 Healthcare Payers

- 9.4.1 Overview

- 9.4.2 Healthcare Payers: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- 9.5 Government Organizations

- 9.5.1 Overview

- 9.5.2 Government Organizations: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- 9.6 Healthcare Providers

- 9.6.1 Overview

- 9.6.2 Healthcare Providers: MEWA Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

10. MEWA Health economics & outcomes research (HEOR) Market - Revenue and Forecast to 2030 - Country Analysis

- 10.1 MEWA: Health Economics & Outcomes Research (HEOR) Market Revenue and Forecast to 2030

- 10.1.1 Overview

- 10.1.1.1 MEWA: Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (USD Million)

- 10.1.2 MEWA: Health Economics & Outcomes Research (HEOR) Market, by Service, 2030 (USD Million)

- 10.1.3 MEWA: Health Economics & Outcomes Research (HEOR) Market, by Service Provider, 2030 (USD Million)

- 10.1.4 MEWA: Health Economics & Outcomes Research (HEOR) Market, by End User, 2030 (USD Million)

- 10.1.5 MEWA: Health Economics & Outcomes Research (HEOR) Market, by Country, 2022 & 2030 (%)

- 10.1.5.1 Saudi Arabia

- 10.1.5.1.1 Overview

- 10.1.5.1.2 Saudi Arabia: Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.5.1.3 Saudi Arabia: Health Economics & Outcomes Research (HEOR) Market, by Service, 2020-2030 (US$ Million)

- 10.1.5.1.4 Saudi Arabia: Health Economics & Outcomes Research (HEOR) Market, by Service Provider, 2030 (USD Million)

- 10.1.5.1.5 Saudi Arabia: Health Economics & Outcomes Research (HEOR) Market, by End User, 2020-2030 (US$ Million)

- 10.1.5.2 UAE

- 10.1.5.2.1 Overview

- 10.1.5.2.2 UAE: Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.5.2.3 UAE: Health Economics & Outcomes Research (HEOR) Market, by Service, 2020-2030 (US$ Million)

- 10.1.5.2.4 UAE: Health Economics & Outcomes Research (HEOR) Market, by Service Provider, 2030 (USD Million)

- 10.1.5.2.5 UAE: Health Economics & Outcomes Research (HEOR) Market, by End User, 2020-2030 (US$ Million)

- 10.1.5.3 Qatar

- 10.1.5.3.1 Overview

- 10.1.5.3.2 Qatar: Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.5.3.3 Qatar: Health Economics & Outcomes Research (HEOR) Market, by Service, 2020-2030 (US$ Million)

- 10.1.5.3.4 Qatar: Health Economics & Outcomes Research (HEOR) Market, by Service Provider, 2030 (USD Million)

- 10.1.5.3.5 Qatar: Health Economics & Outcomes Research (HEOR) Market, by End User, 2020-2030 (US$ Million)

- 10.1.5.4 Kuwait

- 10.1.5.4.1 Overview

- 10.1.5.4.2 Kuwait: Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.5.4.3 Kuwait: Health Economics & Outcomes Research (HEOR) Market, by Service, 2020-2030 (US$ Million)

- 10.1.5.4.4 Kuwait: Health Economics & Outcomes Research (HEOR) Market, by Service Provider, 2030 (USD Million)

- 10.1.5.4.5 Kuwait: Health Economics & Outcomes Research (HEOR) Market, by End User, 2020-2030 (US$ Million)

- 10.1.5.5 Rest of MEWA

- 10.1.5.5.1 Overview

- 10.1.5.5.2 Rest of MEWA: Health Economics & Outcomes Research (HEOR) Market - Revenue and Forecast to 2030 (US$ Million)

- 10.1.5.5.3 Rest of MEWA: Health Economics & Outcomes Research (HEOR) Market, by Service, 2020-2030 (US$ Million)

- 10.1.5.5.4 Rest of MEWA: Health Economics & Outcomes Research (HEOR) Market, by Service Provider, 2030 (USD Million)

- 10.1.5.5.5 Rest of MEWA: Health Economics & Outcomes Research (HEOR) Market, by End User, 2020-2030 (US$ Million)

- 10.1.5.1 Saudi Arabia

- 10.1.1 Overview

11. MEWA Health Economics & Outcomes Research (HEOR) Market - Industry Landscape

- 11.1 Overview

- 11.1 Organic Developments

- 11.1.1 Overview

- 11.2 Inorganic Developments

- 11.2.1 Overview

12. Company Profiles

- 12.1 PharmaLex GmbH

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 ICON Plc

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 IQVIA Holdings Inc

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Syneos Health Inc

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Optum Inc

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 Value In Research

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 ExlService Holdings, Inc.

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 Clarivate Plc

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 CCHO

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners

- 13.2 Glossary of Terms