|

|

市場調査レポート

商品コード

1362395

分子診断薬市場規模および予測、世界および地域シェア、動向、成長機会分析レポート対象範囲:疾患領域別、技術別、製品・サービス別、エンドユーザー別、地域別Molecular Diagnostics Market Size and Forecasts, Global and Regional Share, Trends, and Growth Opportunity Analysis Report Coverage: By Disease Area, Technology, Product & Services, End User, and Geography |

||||||

|

|

|||||||

|

|||||||

| 分子診断薬市場規模および予測、世界および地域シェア、動向、成長機会分析レポート対象範囲:疾患領域別、技術別、製品・サービス別、エンドユーザー別、地域別 |

|

出版日: 2023年09月08日

発行: The Insight Partners

ページ情報: 英文 272 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

分子診断薬市場規模は2022年の181億7,387万米ドルから2030年には458億7,565万米ドルに達すると予測され、2022年から2030年までのCAGRは12.3%と予測されます。当レポートでは、市場の動向と分子診断薬市場の成長を促進・阻害する要因について明らかにしています。市場の成長は、新製品の市場開拓、ポイントオブケア検査需要の増加、関連疾患の急増に起因します。しかし、分子検査に伴う限界が市場成長の妨げとなっています。

個別化医療における分子診断薬市場の今後の成長

ハイスループット技術の進歩により、ゲノム研究はより便利でコスト効率の高いものとなっています。分子診断学は、場合によっては実験室条件下で微生物を培養する必要があった従来の検査とは対照的に、これらのキットや検査は迅速な検出結果を提供するため、臨床検査室ではますます不可欠なものとなっています。プレシジョン・メディシン(精密医療)とは、患者一人一人の遺伝的体質や生活習慣、環境などに基づいて、その患者に合った治療や介入を行うことです。分子診断学はこのアプローチにおいて重要な役割を果たしています。なぜなら、患者の治療に関する意思決定に影響を与える特定のバイオマーカー、遺伝子変異、遺伝子発現パターンの同定を可能にするからです。医薬品開発は分子診断学にますます依存するようになっています。スクリーニング、検出、診断、治療、異質性の評価、進行計画の立案、分子特性の検討、患者の転帰のモニタリングなどに、幅広い分子イメージング技術が用いられています。加えて、分子イメージングは微小な腫瘍の検出やその活動の評価に役立ち、腫瘍学における個別化医療、研究、臨床試験、診療の発展と拡大に大きく貢献します。ハイスループットのジェノタイピング・プラットフォームを用いれば、臨床サンプル中の遺伝子異常を検出することができ、次世代シーケンサーを用いれば、がんを引き起こすあらゆる種類の変化を同定することができます。これらの技術を臨床にイントロダクションすることで、各患者の分子標的を同定することが可能になり、疾患の分子的進行の追跡も容易になります。こうしたアプローチにより、がん患者は個別化医療を受けることができるようになります。このように、テクノロジーの進化に伴い、分子診断薬市場には明るい未来があると思われます。

分子検査に伴う限界が市場成長を妨げる

分子検査の結果は、サンプリングや検査プロセス、技術者のスキルセットなどに依存するため、検査結果にばらつきが生じる可能性があります。さらに、検査手順によっては結果が出るまでに時間がかかるものもあります。検査キットが偽陽性または偽陰性を示すこともあります。このように、分子検査に関連する不確実性は、特に生命を脅かす疾患の診断や治療において、その普及を妨げています。特に新興諸国や低開発諸国では、ポイント・オブ・ケア検査に対する認識が限られていることも、市場の成長を妨げています。さらに、がんやウイルス感染などの適応症に対する分子検査のコストや供給不足も、分子診断薬市場の妨げとなっています。

分子診断市場、疾患領域別インサイト

分子診断市場は疾患領域別に、がん、感染症、遺伝子検査、心疾患、免疫系疾患、その他に区分されます。

感染症分野は2022年に最大の市場シェアを占めました。しかし、がん分野は予測期間中に12.6%と最も高いCAGRを記録すると予測されています。腫瘍分子診断薬は、遺伝物質、タンパク質、関連分子を暴露し、腫瘍学的情報を提供するDNA、RNA、タンパク質に基づく代謝機能、薬物代謝、疾患誘発を評価する検査です。世界保健機関(WHO)の発表によると、2020年のがんによる死亡者数はおよそ1,000万人です。さらに、アメリカがん協会による2021年の統計によると、2040年までに、がんの世界の負担は、2,750万人の新規患者と1,630万人のがん死亡者に増加すると予想されています。このような高い数値は、がんの発生頻度の高まりが、原始的な診断と予防的治療への加速度的な要求に影響を与えていることを示しています。がんを診断する方法はPCR、INAAT、NGSなど数多くあります。中でもPCR(ポリメラーゼ連鎖反応)の着想は、臨床DNA検査に大きな進歩をもたらしました。PCRに基づく方法論は、簡便な装置とインフラを必要とし、微量の生物学的物質を利用するだけで、臨床ルーチンに広く調和します。

PCRのコストは高いが、最も正確なリアルタイムPCR法(99%以上の精度)は、韓国を含む多くの先進国で実際に使用されています。他の選択肢は高価であるため、低開発国では一般的にRapid PCR(60~70%の精度)が使用されています。腫瘍分子診断の分野では、NGSも最も高い成長率を誇る技術です。数多くの企業がこの技術を経済的に利用するために熱心に取り組んでいます。例えば、2021年4月、Illumina Inc.は、NGSベースのTP53コンパニオン診断を共同開発するためにKartos Therapeuticsとの提携を発表しました。

分子診断市場、技術ベースの洞察

技術別では、分子診断市場はポリメラーゼ連鎖反応、等温核酸増幅技術、DNAシーケンシング&次世代シーケンシング、DNAマイクロアレイ、in-situハイブリダイゼーション、その他に区分されます。PCRはさらにRT-PCR、qPCR、マルチプレックスPCR、その他に細分化されます。PCR分野は2022年に市場で最大のシェアを占め、予測期間中、同分野は市場で最高のCAGR 12.7%を記録すると予測されています。PCRは主に、核酸鎖をコピーすることでDNAを作ったり増幅したりするために使用されます。サーマルサイクラーは、酵素、ヌクレオチド、新規DNAを構築するための緩衝液などの試薬とともに、増幅中にDNA鎖を変性およびアニールするために使用されます。この技術は、遺伝子の機能解析、遺伝性の診断、DNAクローニング、父子鑑定、感染症の検出、法医学など様々な応用に広く使われています。ポリメラーゼ連鎖反応は従来のPCR、リアルタイムPCR、デジタルPCRに分類されます。しかしながら、現在進行中の技術の進歩とパンデミックの中での需要の急増は、インドだけでなく他のアジア太平洋諸国でもPCR検査の必要性を煽り続けると思われます。結核、肝炎、インフルエンザ、重篤な感染症などの疾病の一貫した流行は、PoC分子診断業界の動向を促進すると思われます。現在、新型のCOVID-19パンデミックの発生は、このアプローチが病気の徴候を示さない個人のウイルスを検出するために非常に重要であるため、市場に有利な成長局面を作り出すと思われます。PCRの絶妙な感度、相対的な簡便さ、費用対効果により、PCRは他の核酸増幅技術とは一線を画し、分子研究所の主力技術として確固たる地位を築いています。PCRは、PCR技術の継続的な研究開発により、様々な臨床や診断のアプリケーションや検査に不可欠なツールとなっています。したがって、PCRは様々な感染症に対する迅速なポイントオブケア診断に多くの機会を提供しています。例えば、F. Hoffmann-La Roche LtdはDigital PCR(dPCR)技術の進歩に継続的に取り組んでいます。dPCRは臨床分野への応用を拡大し、重要な臨床ツールとして出現しました。パンデミック発生時、Mylab PathoDetect COVID-19 Qualitative PCRキットは、昨年中央医薬品標準管理機関(CDSCO)から国内で最初に商業承認を受けた。承認後、マイラボはバイオテクノロジー大手のSerum Institute of India社および地元企業のAP Globale社と提携しました。PCRはさらにRT-PCR、qPCR、マルチプレックスPCR、その他に細分化されます。分子診断市場、購入モード別インサイト。

分子診断市場は、製品・サービス別にアッセイ&キット、機器、サービス&ソフトウェアに区分されます。アッセイ&キット市場は2022年に最大シェアを占め、予測期間中に最も高いCAGRを記録すると予測されています。分子診断アッセイは、広く使用されている分析手法の一つです。迅速分子アッセイ、逆転写ポリメラーゼ連鎖反応(RT-PCR)、抗原などの様々なタイプのアッセイが、インフルエンザCOVID-19、結核などの様々な疾患の同定と分析に使用されています。製品革新や事業戦略の一環として、市場プレーヤーはさまざまな検査キット用の診断キットを提供しています。地域プレーヤーは、このセグメントに関連する事業開発に積極的に関与しています。例えば、2021年9月、Mylab Discovery Solutionsは、約70の検査をポイントで実行できるプラットフォームSwayam a point of care testing systemの開発者であるSanskritechの株式の過半数を取得しました。さらに、COVID19パンデミックでは、様々な世界市場プレーヤーが地域事業部を通じてキットを提供しています。以上の要因から、同分野は予測期間中に顕著な貢献が期待されます。

エンドユーザーに基づき、分子診断市場は病院&クリニック、診断ラボ、研究&学術機関、その他に区分されます。2022年には、診断ラボ部門が市場で最大のシェアを占めました。さらに、このセグメントは、2022年から2030年にかけて、最も速いCAGR 12.7%で需要が伸びると予測されています。診断ラボは、分子診断製品とサービスの主要な用途です。同施設は、規制要件に従って確立された施設を有しています。検査室では可能な限りの分子診断製品とサービスを使用しています。患者から採取されたサンプルは、さまざまな機器、試薬、方法、技術を用いて分析・研究されます。検査室は病院、診療所、在宅医療などにサービスを提供しています。慢性疾患や感染症の増加、個々の研究者による分子診断活動のアウトソーシングは、予測期間中の同分野の成長を支える要因の一つです。

分子診断市場競合情勢と主な発展

Abbott Laboratories、Agilent Technologies Inc.、Thermo Fisher Scientific Inc.、F. Hoffman-La Roche Ltd.、Qiagen NV、bioMerieux SA、Illumnia Inc.、Danaher、Siemens Healthineers AG、Novartis AG、TBG Diagnostics Limitedなどが分子診断薬市場で事業を展開する大手企業です。

市場プレーヤーは新製品を市場に投入しています。以下はその一例である:

2023年1月、アジレントはクエスト・ダイアグノスティックスと提携し、Agilent Resolution ctDx FIRSTリキッドバイオプシー検査へのアクセスを拡大します。クエストとアジレントの合意により、ワシントンのResolution Bioscience CLIAラボで実施されるシングルサイト市販前承認(ssPMA)検査であるctDx FIRSTが広く採用されることになります。

2023年7月、サーモフィッシャーは分子診断ラボ向けの新しいソフトウェアを発表しました。このソフトウエアはルーチン診断検査の標準化と迅速な結果を得るための合理化に役立ちます。このソフトウェアは、ワークフローのステップを単一のインターフェイス内で接続することにより、急速に変化する検査環境に動的に対応するラボの可能性を高めることができます。

2021年10月、アジレント・テクノロジー・インクは、Ki-67 IHC MIB-1 pharmDx(Dako Omnis)が、内分泌療法にベルゼニオ(アベマシクリブ)を併用する術後補助療法の対象となる、疾患再発リスクの高い早期乳がん(EBC)患者を同定する補助薬としてFDAに承認されたと発表しました。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要な洞察

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 分子診断市場情勢

- PEST分析

- 北米PEST分析

- 欧州PEST分析

- アジア太平洋PEST分析

- 中南米PEST分析

- 中東・アフリカPEST分析

第5章 分子診断市場力学:主要産業力学

- 主な市場促進要因

- 新製品の開発とポイントオブケア検査需要の増加

- 関連疾患の急増

- 市場抑制要因

- 分子検査に伴う限界

- 市場機会

- 分子診断技術の進歩

- 今後の動向

- 個別化医療における分子診断法

- インパクト分析

第6章 分子診断薬市場-世界市場分析

- 分子診断薬市場の収益、2022年~2030年

第7章 分子診断薬の世界市場-2030年までの収益と予測-疾患領域別

- 2022年および2030年における分子診断薬市場の疾患領域別収益シェア(%)

- がん領域

- 感染症

- 遺伝子検査

- 心臓疾患

- 免疫系疾患

- その他

第8章 分子診断薬の世界市場-2030年までの収益と予測-技術別

- 2022年および2030年における分子診断薬市場の技術別売上高シェア(%)

- ポリメラーゼ連鎖反応

- 等温核酸増幅技術(INAAT)

- DNAシーケンシングおよび次世代シーケンシング(NGS)

- DNAマイクロアレイ

- インサイチュハイブリダイゼーション(ISH)

- その他

第9章 分子診断の世界市場-2030年までの収益と予測-製品・サービス別

- 2022年および2030年における分子診断薬市場の製品・サービス別売上高シェア(%)

- アッセイとキット

- 機器

- サービスおよびソフトウェア

第10章 分子診断薬の世界市場:エンドユーザー別収益と2030年までの予測

- 2022年および2030年における分子診断薬市場のエンドユーザー別収益シェア(%)

- 病院および診療所

- 診断研究所

- 研究・学術機関

- その他

第11章 分子診断市場- 地域別分析

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- シンガポール

- マレーシア

- フィリピン

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- 中南米

- ブラジル

- アルゼンチン

- その他中南米

第12章 COVID-19前後の影響

- COVID-19前後の影響

第13章 分子診断市場の業界情勢

- 市場参入企業の成長戦略(%)

- 有機的展開

- 無機的展開

第14章 分子診断薬市場、主要企業プロファイル

- Abbott Laboratories

- Agilent Technologies Inc

- Thermo Fisher Scientific Inc

- F. Hoffmann-La Roche Ltd

- Qiagen NV

- bioMerieux SA

- Illumina Inc

- Danaher

- Siemens Healthineers AG

- Novartis AG

- TBG Diagnostics Limited

第15章 付録

List Of Tables

- Table 1. Molecular Diagnostics Market Segmentation

- Table 2. North America Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 3. North America Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 4. North America Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 5. North America Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 6. North America Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - End User

- Table 7. US Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 8. US Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 9. US Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 10. US Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 11. US Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 12. Canada Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 13. Canada Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 14. Canada Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 15. Canada Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 16. Canada Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 17. Mexico Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 18. Mexico Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 19. Mexico Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 20. Mexico Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 21. Mexico Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 22. Europe Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 23. Europe Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 24. Europe Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 25. Europe Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 26. Europe Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - End User

- Table 27. Germany Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Disease Area

- Table 28. Germany Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 29. Germany Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 30. Germany Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 31. Germany Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 32. UK Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 33. UK Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 34. UK Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 35. UK Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 36. UK Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 37. France Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 38. France Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 39. France Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 40. France Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 41. France Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 42. Italy Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 43. Italy Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 44. Italy Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 45. Italy Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 46. Italy Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 47. Spain Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 48. Spain Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 49. Spain Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 50. Spain Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 51. Spain Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 52. Rest of Europe Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 53. Rest of Europe Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 54. Rest of Europe Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 55. Rest of Europe Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 56. Rest of Europe Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 57. Asia Pacific Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 58. Asia Pacific Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 59. Asia Pacific Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 60. Asia PAcific Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 61. Asia Pacific Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - End User

- Table 62. China Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 63. China Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 64. China Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 65. North America Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 66. China Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 67. Japan Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 68. Japan Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 69. Japan Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 70. Japan Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 71. Japan Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 72. India Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 73. India Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 74. India Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 75. India Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 76. India Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 77. Australia Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 78. Australia Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 79. Australia Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 80. Australia Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 81. Australia Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 82. South Korea Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 83. South Korea Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 84. South Korea Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 85. South Korea Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 86. South Korea Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 87. Singapore Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 88. Singapore Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 89. Singapore Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 90. Singapore Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 91. Singapore Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - End User

- Table 92. Malaysia Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 93. Malaysia Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 94. Malaysia Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 95. Malaysia Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 96. Malaysia Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 97. Philippines Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 98. Philippines Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 99. Philippines Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 100. Philippines Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 101. Philippines Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 102. Thailand Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 103. Thailand Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 104. Thailand Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 105. Thailand Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 106. Thailand Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 107. Indonesia Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 108. Indonesia Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 109. Indonesia Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 110. Indonesia Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 111. Indonesia Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 112. Vietnam Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 113. Vietnam Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 114. Vietnam Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 115. Vietnam Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 116. Vietnam Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 117. Rest of Asia Pacific Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 118. Rest of Asia Pacific Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 119. Rest of Asia Pacific Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 120. Rest of Asia Pacific Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 121. Rest of Asia Pacific Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 122. Middle East & Africa Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 123. Middle East & Africa Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 124. Middle East & Africa Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 125. Middle East & Africa Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 126. Middle East & Africa Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - End User

- Table 127. UAE Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 128. UAE Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 129. UAE Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 130. UAE Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 131. UAE Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 132. Saudi Arabia Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 133. Saudi Arabia Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 134. Saudi Arabia Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 135. Saudi Arabia Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 136. Saudi Arabia Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 137. South Africa Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 138. South Africa Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 139. South Africa Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 140. South Africa Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 141. South Africa Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 142. Rest of Middle East & Africa Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 143. Rest of Middle East & Africa Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 144. Rest of Middle East & Africa Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 145. Rest of Middle East & Africa Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 146. Rest of Middle East & Africa Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 147. South & Central America Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 148. South & Central America Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 149. South & Central America Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 150. South & Central America Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 151. South & Central America Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - End User

- Table 152. Brazil Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 153. Brazil Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 154. Brazil Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 155. Brazil Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 156. Brazil Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 157. Argentina Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - Disease Area

- Table 158. Argentina Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Technology

- Table 159. Argentina Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 160. Argentina Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 161. Argentina Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 162. Rest of South & Central America Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn) - Disease Area

- Table 163. Rest of South & Central America Molecular Diagnostics Market Revenue and Forecast To 2028 (US$ Mn) - Technology

- Table 164. Rest of South & Central America Molecular Diagnostics Market Revenue and Forecast To 2028 (US$ Mn) - Polymerase Chain Reaction (PCR)

- Table 165. Rest of South & Central America Molecular Diagnostics Market Revenue And Forecast To 2028 (US$ Mn) - Product and Services

- Table 166. Rest of South & Central America Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn) - End User

- Table 167. Organic Developments Done By Companies

- Table 168. Inorganic Developments Done By Companies

- Table 169. Glossary of Terms, Molecular Diagnostics Market

List Of Figures

- Figure 1. North America - PEST Analysis

- Figure 2. Europe - PEST Analysis

- Figure 3. Asia Pacific - PEST Analysis

- Figure 4. South & Central America - PEST Analysis

- Figure 5. Middle East & Africa - PEST Analysis

- Figure 6. Molecular Diagnostics Market - Key Industry Dynamics

- Figure 7. Impact Analysis of Drivers and Restraints

- Figure 8. Molecular Diagnostics Market Revenue (US$ Mn), 2022 - 2030

- Figure 9. Molecular Diagnostics Market Revenue Share, by Disease Area 2022 & 2030 (%)

- Figure 10. Oncology: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 11. Infectious Disease: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 12. Infectious Disease: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 13. Cardiac Diseases: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 14. Immune System Disorders: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 15. Others: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 16. Molecular Diagnostics Market Revenue Share, by Technology 2022 & 2030 (%)

- Figure 17. PCR: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 18. RT-PCR: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 19. qPCR: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 20. Multiplex PCR: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 21. Others: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 22. Isothermal Nucleic Acid Amplification Technology (INAAT): Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 23. DNA Sequencing and Next-Generation Sequencing (NGS): Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 24. DNA microarrays: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 25. In-Situ Hybridization (ISH): Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 26. Others: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 27. Molecular Diagnostics Market Revenue Share, by Product and Services 2022 & 2030 (%)

- Figure 28. Assays and Kits: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 29. Instruments: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 30. Services and Software: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 31. Molecular Diagnostics Market Revenue Share, by End User 2022 & 2030 (%)

- Figure 32. Hospitals and Clinics: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 33. Ambulatory Surgical Centers: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 34. Research and Academic Institutes: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 35. Others: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- Figure 36. Molecular Diagnostics Market, 2022 ($Mn)

- Figure 37. North America Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

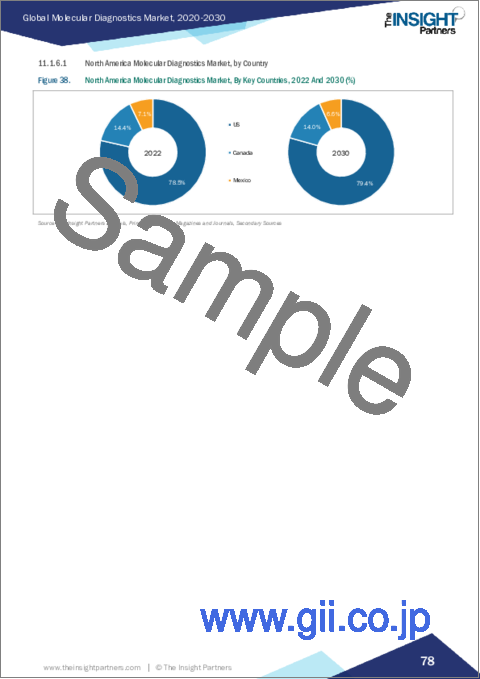

- Figure 38. North America Molecular Diagnostics Market, By Key Countries, 2022 And 2030 (%)

- Figure 39. US Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 40. Canada Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 41. Mexico Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 42. Europe Molecular Diagnostics Market, By Geography, 2022 ($Mn)

- Figure 43. Europe Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 44. Europe Molecular Diagnostics Market, By Key Countries, 2022 And 2030 (%)

- Figure 45. Germany Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 46. UK Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 47. France Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 48. Italy Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 49. Spain Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 50. Rest of Europe Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 51. Molecular Diagnostics Market, By Geography, 2022 ($Mn)

- Figure 52. Asia Pacific Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 53. Asia Pacific Molecular Diagnostics Market, By Key Countries, 2022 And 2030 (%)

- Figure 54. China Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 55. Japan Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 56. India Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 57. Australia Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 58. South Korea Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 59. Singapore Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 60. Malaysia Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 61. Philippines Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 62. Thailand Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 63. Indonesia Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 64. Vietnam Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 65. Rest of Asia Pacific Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 66. Molecular Diagnostics Market, By Geography, 2022 And 2030 ($Mn)

- Figure 67. Middle East & Africa Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 68. Middle East & Africa Molecular Diagnostics Market, By Key Countries, 2022 And 2030 (%)

- Figure 69. UAE Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 70. Saudi Arabia Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 71. South Africa Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 72. Rest of Middle East & Africa Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- Figure 73. Molecular Diagnostics Market, By Geography, 2022 ($Mn)

- Figure 74. South & Central America Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 75. South & Central America Molecular Diagnostics Market, By Key Countries, 2022 And 2030 (%)

- Figure 76. Brazil Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 77. Argentina Molecular Diagnostics Market Revenue And Forecast to 2030 (US$ Mn)

- Figure 78. Rest of South & Central America Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- Figure 79. Pre & Post Covid-19 Impact

- Figure 80. Growth Strategies Done by the Companies in the Market (%)

The molecular diagnostics market size is expected to reach US$ 45,875.65 million by 2030 from US$ 18,173.87 million in 2022; it is estimated to register a CAGR of 12.3% from 2022 to 2030. The report highlights trends prevailing in the market and the factors driving and hindering the molecular diagnostics market growth. The growth of the market is attributed to the development of new products and increase in demand for point-of-care testing and surging prevalence of associated diseases. However, limitations associated with molecular testing hinders the market growth.

Molecular Diagnostics in Personalized Medicine for Molecular Diagnostics Market Growth in the Upcoming Years

With progress in high-throughput techniques, genome research has become more convenient and cost effective. Molecular diagnostics is becoming increasingly indispensable in clinical laboratories as these kits and tests provide rapid detection results as opposed to the conventional tests, which also involved culturing microbes in laboratory conditions in some cases. Using precision medicine, medical treatments and interventions are tailored to each patient based on their unique genetic makeup, lifestyle, and environment. Molecular diagnostics plays an important role in this approach, as it enables the identification of specific biomarkers, genetic mutations, and gene expression patterns that impact decision-making related to the treatment of patients. Drug development has become increasingly dependent on molecular diagnostics. A wide range of molecular imaging techniques are used in screening, detecting, diagnosing, treating, and assessing heterogeneity; making progression plans; examining molecular characteristics; and monitoring patient outcomes. In addition, molecular imaging can aid in the detection of tiny tumors and assessment of their activities, contributing significantly to the development and expansion of personalized medicine, research, clinical trials, and medical practice in oncology. A high-throughput genotyping platform can be used to detect genetic aberrations in clinical samples, and next-generation sequencing can be used to identify all types of cancer-causing changes. The introduction of these techniques into clinical practice would enable the identification of molecular targets in each patient, along with facilitating the tracking of the molecular progression of diseases. With these approaches, cancer patients will be able to receive personalized medicine. Thus, with technology ever evolving, the market for molecular diagnostics seems to have a bright future.

Limitations Associated with Molecular Testing Hampers the Market Growth

The outcomes of molecular testing depend on sampling and testing processes, technicians' skill sets, etc., which may lead to variations in test results. Further, some test procedures take longer for producing results. Several times, test kits may show false positive or negative results. Thus, uncertainties associated with molecular tests hamper their adoption, especially in diagnostics and treatment of life-threatening diseases. The limited awareness of point-of-care tests, particularly in developing and underdeveloped countries, also hinders the market growth. In addition, the cost of molecular testing for indications such as cancer and viral infections, and the shortage of supplies are hampering the molecular diagnostics market.

Molecular Diagnostics Market, By Disease Area Insights

Based on disease area, the molecular diagnostics market is segmented into oncology, infectious disease, genetic testing, cardiac diseases, immune system disorders, and others.

The infectious disease segment held the largest market share in 2022. However, oncology segment is anticipated to register the highest CAGR of 12.6% during the forecast period. Oncology molecular diagnostics are tests that expose inherited material, proteins, associated molecules and assess metabolic functions, drug metabolism, and disease induction grounded on DNA, RNA, and proteins that deliver oncological information. As stated by World Health Organization (WHO), cancer reckoned for roughly 10 million demises in 2020. Furthermore, as per the 2021 statistics by the American Cancer Society, by 2040, the global burden of carcinoma is anticipated to raise to 27.5 million fresh cases and 16.3 million cancer deceases. Such like high figures denote that the evaluated rising frequency of cancer is chipping into the accelerating requirement for primitive diagnosis and preventive cure. There are numerous methods to diagnose carcinoma comprehending PCR, INAAT, and NGS etc. Among all the conception of PCR (polymerase chain reaction) led to an enormous advancement in clinical DNA testing. PCR-based methodologies demand straightforward instrumentation and infrastructure, exploit only minute quantities of biological material and are extensively harmonious with clinical routine.

Although the cost of PCR is lofty, most accurate real-time PCR approach (with more than 99% accuracy) is the one substantially used in numerous developed countries including Korea, while developing countries substantially exploit the conventional PCR (more than 90% accuracy), which is affordable than real-time PCR. Because of the high prices of the other options, underdeveloped countries generally use Rapid PCR (60 - 70% accuracy). Within the field of oncology molecular diagnostics, NGS is another technology flaunting the loftiest rate of growth. Numerous companies are working intensely to make economic use of this technology. For instance, in April 2021, Illumina Inc. blazoned its partnership with Kartos Therapeutics to co-develop an NGS- Based TP53 Companion Diagnostic, which aided to reduce the costs associated with storing and managing of genomic data.

Molecular Diagnostics Market, By Technology-Based Insights

Based on technology, the molecular diagnostics market is segmented into polymerase chain reaction, isothermal nucleic acid amplification technology, DNA sequencing & Next-Generation sequencing, DNA microarrays, in-situ hybridization, and others. The PCR is further sub segmented into RT-PCR, qPCR, Multiplex PCR, and others. The PCR segment held the largest share of the market in 2022, and the same segment is anticipated to register the highest CAGR of 12.7% in the market during the forecast period. PCR is mainly used to make or amplify DNA by copying the nucleic acid strands. Thermal cyclers are employed to denature and anneal DNA strands during amplification, along with reagents such as enzymes, nucleotides, and buffers to build the novel DNA. This technique is widely used in various application such as functional analysis of genes, diagnosis of hereditary, DNA cloning, paternity testing, detection of infectious diseases, and forensic sciences. Polymerase chain reaction has been classified into traditional PCR, real-time PCR, and digital PCR. However, ongoing technological advances and surging demand amid the pandemic will continue to fuel the need for PCR tests in India as well as other Asia Pacific countries. Consistent prevalence of diseases like tuberculosis, Hepatitis, flu, and serious infections will foster PoC molecular diagnostic industry trends. Presently, the outbreak of novel COVID-19 pandemic would create lucrative growth aspects for the market as this approach is highly critical to detect virus in individuals who exhibit no symptoms of signs of disease. PCR's exquisite sensitivity, relative simplicity, and cost-effectiveness makes PCR stand apart from other nucleic acid amplification techniques, cementing it as a mainstay in molecular laboratories. PCR has become an indispensable tool for various clinical and diagnostic applications or examinations due to continuous research & development on PCR technologies. Therefore, it offers many opportunities for rapid point-of-care diagnostics for various infectious diseases. For instance, F. Hoffmann-La Roche Ltd is continuously working on the advancements of Digital PCR (dPCR) techniques. dPCR has extended its applications to the clinical field and has emerged as an important clinical tool. dPCR offers ultrasensitive and absolute nucleic acid quantification without reference standard. Thus, it offers a broader aspect for standardizing and comparing results between laboratories.During pandemic outbreak, one of the first mover startup, Mylab PathoDetect COVID-19 Qualitative PCR kit was among the first in the country to receive commercial approval from the Central Drugs Standard Control Organisation (CDSCO) last year. Following the approval, Mylab had partnered with biotech giant Serum Institute of India and local firm AP Globale. PCR is further sub-segmented into RT-PCR, qPCR, multiplex PCR and others. Molecular Diagnostics Market, By Purchase Mode-Based Insights.

Based on product & services, the molecular diagnostics market is segmented into assays & kits, instruments, and services & software. The assays and kits segment are held the largest share of the market in 2022, and it is anticipated to register the highest CAGR in the market during the forecast period. Molecular Diagnostics assays are among the widely used technique for analysis. Various types of assays such as rapid molecular assays, reverse transcription-polymerase chain reaction (RT-PCR), antigens, and others are used to identify and analyze various diseases such as influenza COVID 19, tuberculosis, and others. As part of product innovation and business strategies, the market players offer diagnostic kits for different test kits. The regional players are actively involved in business development related to the segment. For instance, In September 2021, Mylab Discovery Solutions acquired a majority stake in Sanskritech, developer of a platform Swayam a point of care testing system that can perform about 70 tests on the point. Moreover, in the COVID19 pandemic, various global market players offer their kits through their regional business divisions. Based on the above factors, the segment is expected to contribute remarkably during the forecast period.

Based on end user, the molecular diagnostics market is segmented into hospitals & clinics, diagnostic laboratories, research & academic institutions, and others. In 2022, the diagnostic laboratories segment held the largest share of the market. Moreover, the segment is also expected to witness growth in its demand at a fastest CAGR of 12.7% during 2022 to 2030, owing to the rise in the detection and diagnosis of various medical conditions across the regions. Diagnostic laboratories are the primary uses for molecular diagnostics products and services. It has well-established facilities as per the regulatory requirements. The laboratories use all possible molecular diagnostic products and services. The sample collected from the patients is analyzed and studied using different instruments, reagents, methods, and technologies. The labs provide services to hospitals, clinics, at-home care, and others. The increasing prevalence of chronic diseases, infectious diseases, outsourcing the molecular diagnostics activities by individual researchers are among the factors supporting the segment growth during the forecast period.

Molecular Diagnostics Market: Competitive Landscape and Key Developments

Abbott Laboratories, Agilent Technologies Inc., Thermo Fisher Scientific Inc, F. Hoffman-La Roche Ltd., Qiagen NV, bioMerieux SA, Illumnia Inc., Danaher, Siemens Healthineers AG, Novartis AG, and TBG Diagnostics Limited are among the leading companies operating in the molecular diagnostics market.

Market players are launching new products to the market. Below are few instances:

In January 2023, Agilent to Collaborate with Quest Diagnostics to Extend Access to the Agilent Resolution ctDx FIRST Liquid Biopsy Test. The agreement between Quest and Agilent will enable broad adoption for ctDx FIRST, a single-site premarket approved (ssPMA) test performed at the Resolution Bioscience CLIA laboratory in Washington.

In July 2023, Thermo Fisher launched new software for molecular diagnostics labs. This software helps in streamlining routine diagnostics testing for standardization and rapid time-to-results. It can enhance the potential of a lab to dynamically respond to quickly changing testing environments by connecting workflow steps within a single interface.

In October 2021, Agilent Technologies Inc. has announced its Ki-67 IHC MIB-1 pharmDx (Dako Omnis) is now FDA approved as an aid in identifying patients with early breast cancer (EBC) at high risk of disease recurrence, for whom adjuvant treatment with Verzenio (abemaciclib) in combination with endocrine therapy.

Reasons to Buy:

- Save and reduce time carrying out entry-level research by identifying the growth, size, leading players and segments in the molecular diagnostics market.

- Highlights key business priorities in order to assist companies to realign their business strategies.

- The key findings and recommendations highlight crucial progressive industry trends in the global molecular diagnostics market, thereby allowing players across the value chain to develop effective long-term strategies.

- Develop/modify business expansion plans by using substantial growth offering developed and emerging markets.

- Scrutinize in-depth global market trends and outlook coupled with the factors driving the market, as well as those hindering it.

- Enhance the decision-making process by understanding the strategies that underpin security interest with respect to client products, segmentation, pricing and distribution

Table Of Contents

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Molecular Diagnostics Market Landscape

- 4.1 Overview

- 4.2 PEST Analysis

- 4.2.1 North America PEST Analysis

- 4.2.2 Europe PEST Analysis

- 4.2.3 Asia Pacific PEST Analysis

- 4.2.4 South & Central America PEST Analysis

- 4.2.5 Middle East & Africa PEST Analysis

5. Molecular Diagnostics Market - Key Industry Dynamics

- 5.1 Key Market Drivers:

- 5.1.1 Development of New Products and Increase in Demand for Point-of-Care Testing

- 5.1.2 Surging Prevalence of Associated Diseases

- 5.2 Market Restraints

- 5.2.1 Limitations Associated with Molecular Testing

- 5.3 Market Opportunities

- 5.3.1 Advancements in Molecular Diagnostics Technologies

- 5.4 Future Trends

- 5.4.1 Molecular Diagnostics in Personalized Medicine

- 5.5 Impact Analysis:

6. Molecular Diagnostics Market - Global Market Analysis

- 6.1 Molecular Diagnostics Market Revenue (US$ Mn), 2022 - 2030

7. Global Molecular Diagnostics Market - Revenue and Forecast to 2030 - by Disease Area

- 7.1 Overview

- 7.2 Molecular Diagnostics Market Revenue Share, by Disease Area 2022 & 2030 (%)

- 7.3 Oncology

- 7.3.1 Overview

- 7.3.2 Oncology: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 7.4 Infectious Disease

- 7.4.1 Overview

- 7.4.2 Infectious Disease: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 7.5 Genetic Testing

- 7.5.1 Overview

- 7.5.2 Genetic Testing: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 7.6 Cardiac Diseases

- 7.6.1 Overview

- 7.6.2 Cardiac Diseases: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 7.7 Immune System Disorders

- 7.7.1 Overview

- 7.7.2 Immune System Disorders: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 7.8 Others

- 7.8.1 Overview

- 7.8.2 Others: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

8. Global Molecular Diagnostics Market - Revenue and Forecast to 2030 - by Technology

- 8.1 Overview

- 8.2 Molecular Diagnostics Market Revenue Share, by Technology 2022 & 2030 (%)

- 8.3 Polymerase Chain Reaction

- 8.3.1 Overview

- 8.3.2 PCR: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 8.3.2.1 RT-PCR

- 8.3.2.1.1 Overview

- 8.3.2.1 RT-PCR

- 8.3.3 RT-PCR: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 8.3.3.1 qPCR

- 8.3.3.1.1 Overview

- 8.3.3.1 qPCR

- 8.3.4 PCR: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 8.3.4.1 Multiplex PCR

- 8.3.4.1.1 Overview

- 8.3.4.1 Multiplex PCR

- 8.3.5 Multiplex PCR: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 8.3.5.1 Others

- 8.3.5.1.1 Overview

- 8.3.5.1 Others

- 8.3.6 Others: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 8.4 Isothermal Nucleic Acid Amplification Technology (INAAT)

- 8.4.1 Overview

- 8.4.2 Isothermal Nucleic Acid Amplification Technology (INAAT): Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 8.5 DNA Sequencing and Next-Generation Sequencing (NGS)

- 8.5.1 Overview

- 8.5.2 DNA Sequencing and Next-Generation Sequencing (NGS): Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 8.6 DNA Microarrays

- 8.6.1 Overview

- 8.6.2 DNA Microarrays: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 8.7 In-Situ Hybridization (ISH)

- 8.7.1 Overview

- 8.7.2 In-Situ Hybridization (ISH): Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 8.8 Others

- 8.8.1 Overview

- 8.8.2 Others: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

9. Global Molecular Diagnostics Market - Revenue and Forecast to 2030 - by Product and Services

- 9.1 Overview

- 9.2 Molecular Diagnostics Market Revenue Share, by Product and Services 2022 & 2030 (%)

- 9.3 Assays and Kits

- 9.3.1 Overview

- 9.3.2 Assays and Kits: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 9.4 Instruments

- 9.4.1 Overview

- 9.4.2 Instruments: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 9.5 Services and Software

- 9.5.1 Overview

- 9.5.2 Services and Software: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

10. Global Molecular Diagnostics Market - Revenue and Forecast to 2030 - by End User

- 10.1 Overview

- 10.2 Molecular Diagnostics Market Revenue Share, by End User 2022 & 2030 (%)

- 10.3 Hospitals and Clinics

- 10.3.1 Overview

- 10.3.2 Hospitals and Clinics: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 10.4 Diagnostics Laboratories

- 10.4.1 Overview

- 10.4.2 Diagnostics Laboratories: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 10.5 Research and Academic Institutes

- 10.5.1 Overview

- 10.5.2 Research and Academic Institutes: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

- 10.6 Others

- 10.6.1 Overview

- 10.6.2 Others: Molecular Diagnostics Market - Revenue and Forecast to 2030 (US$ Million)

11. Molecular Diagnostics Market - Geographical Analysis

- 11.1 North America Molecular Diagnostics Market, Revenue And Forecast To 2030

- 11.1.1 Overview

- 11.1.2 North America Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.1.3 North America Molecular Diagnostics Market, by Disease Area

- 11.1.4 North America Molecular Diagnostics Market, by Technology

- 11.1.4.1 North America Molecular Diagnostics Market, by Polymerase Chain Reaction (PCR)

- 11.1.5 North America Molecular Diagnostics Market, by Product and Services

- 11.1.6 North America Molecular Diagnostics Market, by End User

- 11.1.6.1 North America Molecular Diagnostics Market, by Country

- 11.1.7 US

- 11.1.7.1 Overview

- 11.1.8 US Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.1.9 US Molecular Diagnostics Market, by Disease Area

- 11.1.10 US Molecular Diagnostics Market, by Technology

- 11.1.10.1 US Molecular Diagnostics Market, by Polymerase Chain Reaction (PCR)

- 11.1.11 US Molecular Diagnostics Market, by Product and Services

- 11.1.12 US Molecular Diagnostics Market, by End User

- 11.1.13 Canada

- 11.1.13.1 Overview

- 11.1.14 Canada Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.1.15 Canada Molecular Diagnostics Market, by Disease Area

- 11.1.16 Canada Molecular Diagnostics Market, by Technology

- 11.1.16.1 Canada Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.1.17 Canada Molecular Diagnostics Market, by Product and Services

- 11.1.18 Canada Molecular Diagnostics Market, by End User

- 11.1.19 Mexico

- 11.1.19.1 Overview

- 11.1.20 Mexico Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.1.21 Mexico Molecular Diagnostics Market, by Disease Area

- 11.1.22 Mexico Molecular Diagnostics Market, by Technology

- 11.1.22.1 Mexico Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.1.23 Mexico Molecular Diagnostics Market, by Product and Services

- 11.1.24 Mexico Molecular Diagnostics Market, by End User

- 11.2 Europe Molecular Diagnostics Market, Revenue And Forecast to 2030

- 11.2.1 Overview

- 11.2.2 Europe Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.2.3 Europe Molecular Diagnostics Market, by Disease Area

- 11.2.4 Europe Molecular Diagnostics Market, by Technology

- 11.2.4.1 Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.2.5 Europe Molecular Diagnostics Market, by Product and Services

- 11.2.6 Europe Molecular Diagnostics Market, by End User

- 11.2.6.1 Europe Molecular Diagnostics Market by Country

- 11.2.7 Germany

- 11.2.7.1 Overview

- 11.2.8 Germany Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.2.9 Germany Molecular Diagnostics Market, by Disease Area

- 11.2.10 Germany Molecular Diagnostics Market, by Technology

- 11.2.10.1 Germany Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.2.11 Germany Molecular Diagnostics Market, by Product and Services

- 11.2.12 Germany Molecular Diagnostics Market, by End User

- 11.2.13 UK

- 11.2.13.1 Overview

- 11.2.14 UK Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.2.15 UK Molecular Diagnostics Market, by Disease Area

- 11.2.16 UK Molecular Diagnostics Market, by Technology

- 11.2.16.1 UK Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.2.17 UK Molecular Diagnostics Market, by Product and Services

- 11.2.18 UK Molecular Diagnostics Market, by End User

- 11.2.19 France

- 11.2.19.1 Overview

- 11.2.20 France Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.2.21 France Molecular Diagnostics Market, by Disease Area

- 11.2.22 France Molecular Diagnostics Market, by Technology

- 11.2.22.1 France Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.2.23 France Molecular Diagnostics Market, by Product and Services

- 11.2.24 France Molecular Diagnostics Market, by End User

- 11.2.25 Italy

- 11.2.25.1 Overview

- 11.2.26 Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.2.27 Italy Molecular Diagnostics Market, by Disease Area

- 11.2.28 Italy Molecular Diagnostics Market, by Technology

- 11.2.28.1 Italy Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.2.29 Italy Molecular Diagnostics Market, by Product and Services

- 11.2.30 Italy Molecular Diagnostics Market, by End User

- 11.2.31 Spain

- 11.2.31.1 Overview

- 11.2.32 Spain Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.2.33 Spain Molecular Diagnostics Market, by Disease Area

- 11.2.34 Spain Molecular Diagnostics Market, by Technology

- 11.2.34.1 Spain Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.2.34.1.1 Spain Molecular Diagnostics Market, by Product and Services

- 11.2.34.1 Spain Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.2.35 Spain Molecular Diagnostics Market, by End User

- 11.2.36 Rest of Europe

- 11.2.36.1 Overview

- 11.2.37 Rest of Europe Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.2.38 Rest of Europe Molecular Diagnostics Market, by Disease Area

- 11.2.39 Rest of Europe Molecular Diagnostics Market, by Technology

- 11.2.39.1 Rest of Europe Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.2.40 Rest of Europe Molecular Diagnostics Market, by Product and Services

- 11.2.41 Rest of Europe Molecular Diagnostics Market, by End User

- 11.3 Asia Pacific Molecular Diagnostics Market, Revenue And Forecast to 2030

- 11.3.1 Overview

- 11.3.2 Asia Pacific Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.3.3 Asia Pacific Molecular Diagnostics Market, by Disease Area

- 11.3.4 Asia Pacific Molecular Diagnostics Market, by Technology

- 11.3.4.1 Asia Pacific Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.3.5 Asia Pacific Molecular Diagnostics Market, by Product and Services

- 11.3.6 Asia Pacific Molecular Diagnostics Market, by End User

- 11.3.6.1 Asia Pacific Molecular Diagnostics Market by Country

- 11.3.7 China

- 11.3.7.1 Overview

- 11.3.8 China Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.3.9 China Molecular Diagnostics Market, by Disease Area

- 11.3.10 China Molecular Diagnostics Market, by Technology

- 11.3.10.1 China Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.3.11 China Molecular Diagnostics Market, by Product and Services

- 11.3.12 China Molecular Diagnostics Market, by End User

- 11.3.13 Japan

- 11.3.13.1 Overview

- 11.3.14 Japan Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.3.15 Japan Molecular Diagnostics Market, by Disease Area

- 11.3.16 Japan Molecular Diagnostics Market, by Technology

- 11.3.16.1 Japan Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.3.17 Japan Molecular Diagnostics Market, by Product and Services

- 11.3.18 Japan Molecular Diagnostics Market, by End User

- 11.3.19 India

- 11.3.19.1 Overview

- 11.3.20 India Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.3.21 India Molecular Diagnostics Market, by Disease Area

- 11.3.22 India Molecular Diagnostics Market, by Technology

- 11.3.22.1 India Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.3.23 India Molecular Diagnostics Market, by Product and Services

- 11.3.24 India Molecular Diagnostics Market, by End User

- 11.3.25 Australia

- 11.3.25.1 Overview

- 11.3.26 Australia Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.3.27 Australia Molecular Diagnostics Market, by Disease Area

- 11.3.28 Australia Molecular Diagnostics Market, by Technology

- 11.3.28.1 Australia Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.3.29 Australia Molecular Diagnostics Market, by Product and Services

- 11.3.30 Australia Molecular Diagnostics Market, by End User

- 11.3.31 South Korea

- 11.3.31.1 Overview

- 11.3.32 South Korea Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.3.33 South Korea Molecular Diagnostics Market, by Disease Area

- 11.3.34 South Korea Molecular Diagnostics Market, by Technology

- 11.3.34.1 South Korea Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.3.35 South Korea Molecular Diagnostics Market, by Product and Services

- 11.3.36 South Korea Molecular Diagnostics Market, by End User

- 11.3.37 Singapore

- 11.3.37.1 Overview

- 11.3.38 Singapore Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.3.39 Singapore Molecular Diagnostics Market, by Disease Area

- 11.3.40 Singapore Molecular Diagnostics Market, by Technology

- 11.3.40.1 Singapore Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.3.41 Singapore Molecular Diagnostics Market, by Product and Services

- 11.3.42 Singapore Molecular Diagnostics Market, by End User

- 11.3.43 Malaysia

- 11.3.43.1 Overview

- 11.3.44 Malaysia Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.3.45 Malaysia Molecular Diagnostics Market, by Disease Area

- 11.3.46 Malaysia Molecular Diagnostics Market, by Technology

- 11.3.46.1 Malaysia Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.3.47 Malaysia Molecular Diagnostics Market, by Product and Services

- 11.3.48 Malaysia Molecular Diagnostics Market, by End User

- 11.3.49 Philippines

- 11.3.49.1 Overview

- 11.3.50 Philippines Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.3.51 Philippines Molecular Diagnostics Market, by Disease Area

- 11.3.52 Philippines Molecular Diagnostics Market, by Technology

- 11.3.52.1 Philippines Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.3.53 Philippines Molecular Diagnostics Market, by Product and Services

- 11.3.54 Philippines Molecular Diagnostics Market, by End User

- 11.3.55 Thailand

- 11.3.55.1 Overview

- 11.3.56 Thailand Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.3.57 Thailand Molecular Diagnostics Market, by Disease Area

- 11.3.58 Thailand Molecular Diagnostics Market, by Technology

- 11.3.58.1 Thailand Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.3.59 Thailand Molecular Diagnostics Market, by Product and Services

- 11.3.60 Thailand Molecular Diagnostics Market, by End User

- 11.3.61 Indonesia

- 11.3.61.1 Overview

- 11.3.62 Indonesia Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.3.63 Indonesia Molecular Diagnostics Market, by Disease Area

- 11.3.64 Indonesia Molecular Diagnostics Market, by Technology

- 11.3.64.1 Indonesia Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.3.65 Indonesia Molecular Diagnostics Market, by Product and Services

- 11.3.66 Indonesia Molecular Diagnostics Market, by End User

- 11.3.67 Vietnam

- 11.3.67.1 Overview

- 11.3.68 Vietnam Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.3.69 Vietnam Molecular Diagnostics Market, by Disease Area

- 11.3.70 Vietnam Molecular Diagnostics Market, by Technology

- 11.3.70.1 Vietnam Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.3.71 Vietnam Molecular Diagnostics Market, by Product and Services

- 11.3.72 Vietnam Molecular Diagnostics Market, by End User

- 11.3.73 Rest of Asia Pacific

- 11.3.73.1 Overview

- 11.3.74 Rest of Asia Pacific Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.3.75 Rest of Asia Pacific Molecular Diagnostics Market, by Disease Area

- 11.3.76 Rest of Asia Pacific Molecular Diagnostics Market, by Technology

- 11.3.76.1 Rest of Asia Pacific Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.3.77 Rest of Asia Pacific Molecular Diagnostics Market, by Product and Services

- 11.3.78 Rest of Asia Pacific Molecular Diagnostics Market, by End User

- 11.4 Middle East & Africa Molecular Diagnostics Market, Revenue And Forecast to 2030

- 11.4.1 Overview

- 11.4.2 Middle East & Africa Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.4.3 Middle East & Africa Molecular Diagnostics Market, by Disease Area

- 11.4.4 Middle East & Africa Molecular Diagnostics Market, by Technology

- 11.4.4.1 Middle East & Africa Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.4.5 Middle East & Africa Molecular Diagnostics Market, by Product and Services

- 11.4.6 Middle East & Africa Molecular Diagnostics Market, by End User

- 11.4.6.1 Middle East & Africa Molecular Diagnostics Market by Country

- 11.4.7 UAE

- 11.4.7.1 Overview

- 11.4.8 UAE Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.4.9 UAE Molecular Diagnostics Market, by Disease Area

- 11.4.10 UAE Molecular Diagnostics Market, by Technology

- 11.4.10.1 UAE Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.4.11 UAE Molecular Diagnostics Market, by Product and Services

- 11.4.12 UAE Molecular Diagnostics Market, by End User

- 11.4.13 Saudi Arabia

- 11.4.13.1 Overview

- 11.4.14 Saudi Arabia Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.4.15 Saudi Arabia Molecular Diagnostics Market, by Disease Area

- 11.4.16 Saudi Arabia Molecular Diagnostics Market, by Technology

- 11.4.16.1 Saudi Arabia Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.4.17 Saudi Arabia Molecular Diagnostics Market, by Product and Services

- 11.4.18 Saudi Arabia Molecular Diagnostics Market, by End User

- 11.4.19 South Africa

- 11.4.19.1 Overview

- 11.4.20 South Africa Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.4.21 South Africa Molecular Diagnostics Market, by Disease Area

- 11.4.22 South Africa Molecular Diagnostics Market, by Technology

- 11.4.22.1 South Africa Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.4.23 South Africa Molecular Diagnostics Market, by Product and Services

- 11.4.24 South Africa Molecular Diagnostics Market, by End User

- 11.4.25 Rest of Middle East & Africa

- 11.4.25.1 Overview

- 11.4.26 Rest of Middle East & Africa Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.4.27 Rest of Middle East & Africa Molecular Diagnostics Market, by Disease Area

- 11.4.28 Rest of Middle East & Africa Molecular Diagnostics Market, by Technology

- 11.4.28.1 Rest of Middle East & Africa Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.4.29 Rest of Middle East & Africa Molecular Diagnostics Market, by Product and Services

- 11.4.30 Rest of Middle East & Africa Molecular Diagnostics Market, by End User

- 11.5 South & Central America Molecular Diagnostics Market, Revenue And Forecast to 2030

- 11.5.1 Overview

- 11.5.2 South & Central America Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.5.3 South & Central America Molecular Diagnostics Market, by Disease Area

- 11.5.4 South & Central America Molecular Diagnostics Market, by Technology

- 11.5.4.1 South & Central America Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.5.5 South & Central America Molecular Diagnostics Market, by Product and Services

- 11.5.6 South & Central America Molecular Diagnostics Market, by End User

- 11.5.6.1 South & Central America Molecular Diagnostics Market by Country

- 11.5.7 Brazil

- 11.5.7.1 Overview

- 11.5.8 Brazil Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.5.9 Brazil Molecular Diagnostics Market, by Disease Area

- 11.5.10 Brazil Molecular Diagnostics Market, by Technology

- 11.5.10.1 Brazil Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.5.11 Brazil Molecular Diagnostics Market, by Product and Services

- 11.5.12 Brazil Molecular Diagnostics Market, by End User

- 11.5.13 Argentina

- 11.5.13.1 Overview

- 11.5.14 Argentina Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.5.15 Argentina Molecular Diagnostics Market, by Disease Area

- 11.5.16 Argentina Molecular Diagnostics Market, by Technology

- 11.5.16.1 Argentina Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.5.17 Argentina Molecular Diagnostics Market, by Product and Services

- 11.5.18 Argentina Molecular Diagnostics Market, by End User

- 11.5.19 Rest of South & Central America

- 11.5.19.1 Overview

- 11.5.20 Rest of South & Central America Molecular Diagnostics Market Revenue and Forecast to 2030 (US$ Mn)

- 11.5.21 Rest of South & Central America Molecular Diagnostics Market, by Disease Area

- 11.5.22 Rest of South & Central America Molecular Diagnostics Market, by Technology

- 11.5.22.1 Rest of South & Central America Molecular Diagnostics Market, Polymerase Chain Reaction (PCR)

- 11.5.23 Rest of South & Central America Molecular Diagnostics Market, by Product and Services

- 11.5.24 Rest of South & Central America Molecular Diagnostics Market, by End User

12. Pre & Post Covid-19 Impact

- 12.1 Pre & Post Covid-19 Impact

13. Molecular Diagnostics Market Industry Landscape

- 13.1 Overview

- 13.2 Growth Strategies Done by the Companies in the Market (%)

- 13.3 Organic Developments

- 13.3.1 Overview

- 13.4 Inorganic Developments

- 13.4.1 Overview

14. Molecular Diagnostics Market, Key Company Profiles

- 14.1 Abbott Laboratories

- 14.1.1 Key Facts

- 14.1.2 Business Description

- 14.1.3 Products and Services

- 14.1.4 Financial Overview

- 14.1.5 SWOT Analysis

- 14.1.6 Key Developments

- 14.2 Agilent Technologies Inc

- 14.2.1 Key Facts

- 14.2.2 Business Description

- 14.2.3 Products and Services

- 14.2.4 Financial Overview

- 14.2.5 SWOT Analysis

- 14.2.6 Key Developments

- 14.3 Thermo Fisher Scientific Inc

- 14.3.1 Key Facts

- 14.3.2 Business Description

- 14.3.3 Products and Services

- 14.3.4 Financial Overview

- 14.3.5 SWOT Analysis

- 14.3.6 Key Developments

- 14.4 F. Hoffmann-La Roche Ltd

- 14.4.1 Key Facts

- 14.4.2 Business Description

- 14.4.3 Products and Services

- 14.4.4 Financial Overview

- 14.4.5 SWOT Analysis

- 14.4.6 Key Developments

- 14.5 Qiagen NV

- 14.5.1 Key Facts

- 14.5.2 Business Description

- 14.5.3 Products and Services

- 14.5.4 Financial Overview

- 14.5.5 SWOT Analysis

- 14.5.6 Key Developments

- 14.6 bioMerieux SA

- 14.6.1 Key Facts

- 14.6.2 Business Description

- 14.6.3 Products and Services

- 14.6.4 Financial Overview

- 14.6.5 SWOT Analysis

- 14.6.6 Key Developments

- 14.7 Illumina Inc

- 14.7.1 Key Facts

- 14.7.2 Business Description

- 14.7.3 Products and Services

- 14.7.4 Financial Overview

- 14.7.5 SWOT Analysis

- 14.7.6 Key Developments

- 14.8 Danaher

- 14.8.1 Key Facts

- 14.8.2 Business Description

- 14.8.3 Products and Services

- 14.8.4 Financial Overview

- 14.8.5 SWOT Analysis

- 14.8.6 Key Developments

- 14.9 Siemens Healthineers AG

- 14.9.1 Key Facts

- 14.9.2 Business Description

- 14.9.3 Products and Services

- 14.9.4 Financial Overview

- 14.9.5 SWOT Analysis

- 14.9.6 Key Developments

- 14.10 Novartis AG

- 14.10.1 Key Facts

- 14.10.2 Business Description

- 14.10.3 Products and Services

- 14.10.4 Financial Overview

- 14.10.5 SWOT Analysis

- 14.10.6 Key Developments

- 14.11 TBG Diagnostics Limited

- 14.11.1 Key Facts

- 14.11.2 Business Description

- 14.11.3 Products and Services

- 14.11.4 Financial Overview

- 14.11.5 SWOT Analysis

- 14.11.6 Key Developments

15. Appendix

- 15.1 About Us

- 15.2 Glossary of Terms