|

|

市場調査レポート

商品コード

1343611

リチウムイオン電池の電解質:技術動向と市場予測 (2030年まで)<2023> Lithium-Ion Battery Electrolyte Technology Trends and Market Forecast (~2030) |

||||||

|

|

|||||||

|

|||||||

| リチウムイオン電池の電解質:技術動向と市場予測 (2030年まで) |

|

出版日: 2023年08月24日

発行: SNE Research

ページ情報: 英文 474 Pages

納期: お問合せ

|

- 全表示

- 概要

- 目次

二次電池市場は近年、小型IT用途からESSや電気自動車へと拡大しています。Panasonicのように二次電池を開発し、業界を開拓した日本企業はLGESのような韓国の強豪に敗れつつあり、CATL、BYD、CALBのような中国企業は中国政府の支援と無限の国内市場を背景にM/Sをさらに拡大しています。韓・中・日の「三極体制」は当面続くと予想されていますが、電気自動車市場の拡大により、北米や欧州も大容量二次電池の製造・材料市場に継続的な関心を示しています。特に、市場情勢など各国の規制と政策により、二次電池市場の様相が大きく変化することが予想されます。

電解質は主に溶剤、リチウム塩、添加剤で構成されます。製品の性質に応じて、電解質はリチウムイオン二次電池メーカーと共同で開発されます。小型ITタイプの製品であれば開発期間は3~4ヶ月と短いですが、xEV用の電解質は1年以上かけて開発・評価されます。顧客ニーズに応じた多様な製品の開発・対応には、優れた研究開発力が求められます。

電解質市場は、かつては日本と韓国が独占していましたが、近年の中国企業の急成長により、トップ3のシェアを中国企業に奪われています。韓国では、Donghwa ElectrolyteとSoulbrain、Enchemの3社が、リチウムイオン二次電池大手3社 (Samsung SDI、LG Energy Solution、SK energy) と共に電解質サプライヤーとして成長することができました。日本では、Mitsubishi ChemicalがIT小型セル、xEV中型セル、大型セルを生産する顧客ポートフォリオを多様化しています。中国では、Tinci、Guotai-Huarong、Capchemが市場を独占しています。

電解質の主成分であるリチウム塩 (LiPF6) は、これまでは日本企業による供給が多かったのですが、中国企業の生産能力拡大で様相が変わってきました。韓国ではFoosungが汎用リチウム塩 (LiPF6) を、Chunboが特殊リチウム塩 (LiFSI、LiPO2F2、LiDFOP、LiBOB) を量産しています。添加剤は、リチウムイオン二次電池の寿命や安定性を向上させるため、電解質の製造工程で添加されるもので、SEI保護、過充電防止剤、導電性などがあります。添加剤市場は日本企業が独占していますが、韓国ではChunboとChemtrosが主なサプライヤーです。

電解質は二次電池を構成する4つの主要材料の一つです。一般的なリチウムイオン二次電池の製造コスト構成では、負極材>セパレーター>正極材>電解質の順で重要視されます。単位セル当たりのエネルギー密度を高めるため、二次電池メーカーは負極材と正極材の投入量を増やし、電解質の投入量を減らしています。しかし、2022年から2030年にかけて、電池市場は年平均約23% (容量比) の成長が見込まれます。それに伴い、電解質市場も成長すると予想されます。

電気自動車・ESS向けの大型二次電池では、電解質の使用量が単位セルあたりIT向けの約200倍~4,000倍となるため、安定性の確保が特に重要な課題となっています。現在実用化されている液体電解質やゲル状高分子電解質 (ポリマー) に加え、高温安定性に優れた固体高分子電解質や全固体セラミック電解質の安定性向上のための研究開発が進められています。

当レポートでは、リチウムイオン二次電池に使用される電解質の完成品や成分に関する詳細な技術情報を提供するとともに、バインダーの需要と市場について、当社の各種予測結果に基づき予測し、読者が全体的な規模を理解できるようになっています。

最後に、主要電池メーカーの電解質需要と、電解質メーカーの供給状況・見通しをまとめ、この分野の研究者や関係者に技術から市場まで幅広い知見を提供することを目的としています。

当レポートの特長

- 1. 電解質の完成品と成分に関する全体的な概要と技術情報

- 2. 従来のLiB以外の次世代電池に適用される固体電解質・高分子電解質の概略

- 3. 当社の予測データに基づく、電解質市場展望の客観的データ提供

- 4. 韓国・中国・日本の主要電解質メーカーの製品・生産状況を詳細に紹介

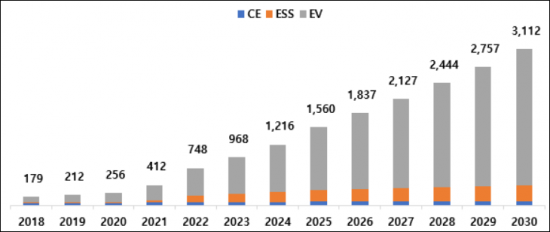

<世界の電解質市場の需要予測 (2030年まで) >

*SNEの電池需要予測に基づく

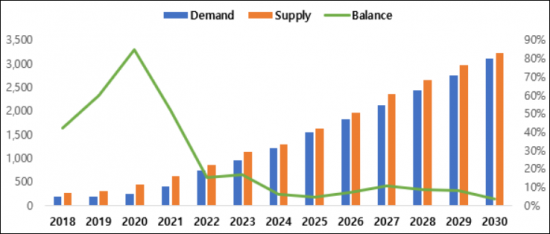

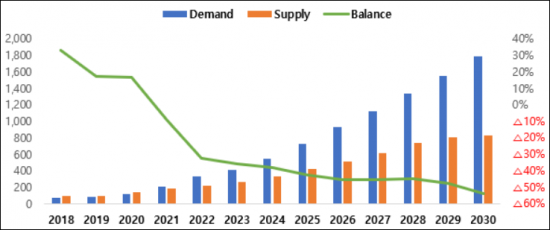

<世界の電解質の需給見通し (2018年~2030年) >

<中国以外の市場の電解質の需給見通し (2018年~2030年) >

*中国市場の需給を除く。

目次

報告書の概要

第1章 電解質の概要

- 電解質とは何か

- 電解質の開発動向と主な課題

第2章 液体電解質の開発動向

- 液体電解質の組成

- 液体電解質の特徴

- 難燃性材料

第3章 高分子電解質の開発動向

- 高分子電解質の種類

- 高分子電解質の特徴

- 高分子電解質の製造方法

第4章 固体電解質

- 固体電解質の開発の必要性

- 固体電解質の種類と技術的特徴

- 固体電解質の開発動向

第5章 電解質の最新開発動向

- 高電圧電解質溶媒

- リチウム塩

- 添加剤

- 高分子電解質

第6章 電解質溶媒

- 環状炭酸塩

- 線形炭酸塩

- 電極表面に保護膜を形成する添加剤によるガス発生メカニズム

第7章 電解質添加剤

- 高Niカソード界面安定化のための電解質添加剤

- 出力特性を向上させる電解質添加剤

- LiFSI塩を使用した電解質

- 熱安定性を向上させる難燃剤添加剤

- 高容量アノード界面安定化のための添加剤

第8-1章 電解質市場の動向と展望

- 電解質の需要量:国別

- 電解質の使用量:用途別

- 市場状況:サプライヤー別

- 電解質の需要:LiB企業別

- (SDI/LGES/SKon/Panasonic/CATL/ATL/BYD/Lishen/Guoxuan(Gotion)/AESC)

- 電解質の需要の見通し

- 電解質の生産能力と需給見通し

- 電解質の価格動向

- 電解質の市場規模の予測

第8-2章 電解質材料のステータス

- 一般リチウム塩 (LiPF6)

- 非LiPF6リチウム塩

- 機能性添加剤

第9章 電解質メーカーのステータス

- 韓国の電解質企業

- Dongwha Electrolyte / Soulbrain / Enchem / Foosung / Chunbo / Chemtros

- 日本の電解質企業

- Mitsubishi / Ube / Centralglass / Tomiyama / MUIS / Nippon Shokubai

- 中国の電解質企業

- Tinci / Capchem / Guotai Huarong / Shanshan / Jinniu / DFD / Shinghwa

Recently, the secondary battery market has expanded from small IT applications to ESS and electric vehicles. Japanese companies such as Panasonic, which developed secondary batteries and pioneered the industry, are losing out to Korean powerhouses such as LGES, while Chinese companies such as CATL, BYD, and CALB are further expanding their M/S with the support of the Chinese government and an unlimited domestic market. Although the Korean, Chinese, and Japanese "trilateral system" is expected to continue for the foreseeable future, North America and Europe are also showing continued interest in the large-capacity secondary battery manufacturing and materials market due to the expansion of the electric vehicle market. In particular, the policies and regulations of each country, such as the IRA, are expected to significantly change the landscape of the secondary battery market.

The electrolyte is mainly composed of solvents, lithium salts, and additives. Depending on the nature of the product, the electrolyte will be developed in collaboration with lithium-ion secondary battery manufacturers. For small IT-type products, the development period is as short as three to four months, while electrolytes for xEVs are developed and evaluated for more than a year. Excellent R&D capabilities are required to develop and respond to various products according to customer needs.

In the past, the electrolyte market was dominated by Japan and South Korea, but with the recent rapid growth of Chinese companies, the top three market shares have been taken over by Chinese companies. In Korea, Donghwa Electrolyte, Soulbrain, and Enchem have been able to grow together as electrolyte suppliers with the three major lithium-ion secondary battery companies (Samsung SDI, LG Energy Solution, and SK energy). In Japan, Mitsubishi Chemical has diversified its portfolio of customers producing IT small, xEV medium and large cells. In China, Tinci, Guotai-Huarong, and Capchem dominate the market.

Lithium salts (LiPF6), the main ingredient of electrolyte, have been mostly supplied by Japanese companies in the past, but the game has changed as Chinese companies have increased their CAPA. In South Korea, Foosung provides general-purpose lithium salts (LiPF6), while Chunbo mass-produces specialized lithium salts (LiFSI, LiPO2F2, LiDFOP, LiBOB). Additives are added during the electrolyte manufacturing process to improve the lifespan and stability of Li-ion secondary batteries, such as SEI protection, overcharge prevention agents, and conductive properties. While Japanese companies dominate the additives market, in Korea Chunbo and Chemtros are among the main suppliers.

Electrolyte is one of the four key materials that make up a secondary battery. In the manufacturing cost composition of a typical Li-ion battery, the order of importance is anode material > separator > cathode material > electrolyte. To increase the energy density per unit cell, secondary battery manufacturers are increasing the input of anode and cathode materials, while reducing the input of electrolyte. However, from 2022 to 2030, the battery market is expected to grow at an average annual rate of around 23% (by capacity). The electrolyte market is expected to grow accordingly.

For large-scale rechargeable batteries for electric vehicles and ESS, the amount of electrolyte used is about 200 times to 4,000 times higher on a unit cell basis than for IT, so securing stability is becoming a particularly important issue. In addition to liquid electrolytes and gel polymer electrolytes (polymers) that are currently commercialized, research and development is underway to improve the stability of solid polymer electrolytes and all-solid ceramic electrolytes with excellent high temperature stability.

This report provides detailed technical information on finished electrolyte products and their components for application in lithium-ion secondary batteries and forecasts the demand and market for binders based on our various forecasts to help readers understand the overall scale.

Finally, by summarizing the electrolyte demand of major battery manufacturers and the supply status and outlook of electrolyte companies, the report aims to provide researchers and interested parties in this field with a wide range of insights from technology to market.

Strong points of this report:

- 1. overall overview and technical information on electrolyte finished products and components

- 2. Introduction to solid and polymer electrolytes that will be applied to next-generation batteries other than conventional LIBs

- 3. Provides objective data on the electrolyte market outlook based on our forecast data

- 4. Detailed information on the product and production status of major electrolyte players in Korea, China, and Japan

<Global Electrolytes Market Demand Forecas (~2030)>

*Based on SNE battery demand forecasts.

<Global Electrolyte Supply and Demand Outlook (2018~2030)>

<Electrolyte Supply and Demand Outlook for Non-Chinese Markets (2018~2030)>

*Except for Chinese market supply and demand.

Table of Contents

Outline of Report

Chapter I. Electrolyte Overview

- 1.1. Understanding of electrolytes

- 1.2. Development trends and major issues of electrolytes

Chapter II. Development Trend of Liquid Electrolytes

- 2.1. Composition of liquid electrolytes

- 2.2. Characteristics of liquid electrolytes

- 2.3. Flame retardant material

Chapter III. Development Trend of Polymer Electrolyte

- 3.1. Types of polymer electrolytes

- 3.2. Characteristics of polymer electrolytes

- 3.3. Manufacturing method of polymer electrolytes

Chapter IV. Solid Electrolytes

- 4.1. Necessity for development of solid electrolytes

- 4.2. Types and technical characteristics of solid electrolytes

- 4.3. Development trends of solid electrolytes

Chapter V. Latest Development Trends of Electrolytes

- 5.1. High voltage electrolyte solvents

- 5.2. Lithium salts

- 5.3. Additives

- 5.4. Polyelectrolytes

Chapter VI. Electrolyte Solvents

- 6.1. Cyclic carbonate

- 6.2. Linear carbonate

- 6.3. Gas generation mechanism by additives for forming the protective film on the electrode surface

Chapter VII. Electrolyte Additives

- 7.1. Electrolyte additives for high-Ni cathode interface stabilization

- 7.2. Electrolyte additives for improved output characteristics

- 7.3. Electrolytes using LiFSI salts

- 7.4. Flame retardant additives for improved thermal stability

- 7.5. Additives for high-capacity anode interface stabilization

Chapter VIII-1. Electrolyte Market Trends and Outlook

- 8.1.1. Electrolyte demand by country

- 8.1.2. Electrolyte usage by application

- 8.1.3. Market status by suppliers

- 8.1.4. Electrolyte demand by LIB companies

- (SDI/LGES/SKon/Panasonic/CATL/ATL/BYD/Lishen/Guoxuan(Gotion)/AESC)

- 8.1.5. Electrolyte demand outlook

- 8.1.6. Electrolyte CAPA and supply & demand outlook

- 8.1.7. Electrolyte price trends

- 8.1.8. Electrolyte market size forecast

Chapter VIII-2. Electrolyte Material Status

- 8.2.1. General lithium salts (LiPF6)

- 8.2.2. Non-LiPF6 lithium salts

- 8.2.3. Functional additives

Chapter IX. Electrolyte Manufacturer Status

- 9.1. Korean electrolyte companies

- Dongwha Electrolyte / Soulbrain / Enchem / Foosung / Chunbo / Chemtros

- 9.2. Japanese electrolyte companies

- Mitsubishi / Ube / Centralglass / Tomiyama / MUIS / Nippon Shokubai

- 9.3. Chines electrolyte companies

- Tinci / Capchem / Guotai Huarong / Shanshan / Jinniu / DFD / Shinghwa