|

|

市場調査レポート

商品コード

1530814

オフィスオートメーションの世界市場予測(~2030年): タイプ、展開、組織規模、技術、用途、エンドユーザー、地域別の分析Office Automation Market Forecasts to 2030 - Global Analysis By Type (Hardware, Software and Services), Deployment, Organization Size, Technology, Application, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| オフィスオートメーションの世界市場予測(~2030年): タイプ、展開、組織規模、技術、用途、エンドユーザー、地域別の分析 |

|

出版日: 2024年08月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

世界のオフィスオートメーションの市場規模は、2024年に4億2,527万米ドルを占め、予測期間中にCAGR12.1%で成長し、2030年には8億8,273万米ドルに達すると予測されています。 オフィスオートメーションとは、オフィス業務やプロセスをより効率的に実行するための技術活用を指します。

様々なシステムやソフトウェアを統合してワークフローを合理化し、生産性を高めることが含まれます。反復作業をオートメーションし、情報をデジタル管理することで、オフィスオートメーションは手作業を減らし、エラーを最小限に抑え、組織内のコミュニケーションを改善します。

2019年シンガポール政府貿易統計によると、米国はシンガポールのオートメーション機器の市場シェアの約20%を占めています。

リモートワークとハイブリッドワークモデルの台頭

リモートワークやハイブリッドワークモデルの台頭により、リモートでのコラボレーション、コミュニケーション、生産性をサポートするデジタルツールの需要が高まっています。クラウドベースのプラットフォーム、バーチャルコラボレーションツール、ワークフロー管理システムなどのオートメーションソリューションは、分散したチーム間でのシームレスなやり取りと効率化を可能にします。組織は柔軟な労働環境に適応するため、業務の継続性を維持し、チーム・コラボレーションを強化し、プロセスを合理化するオートメーション技術を求めており、オフィスオートメーション市場へのさらなる投資と拡大を促進しています。

セキュリティへの懸念

オフィスオートメーションにおけるセキュリティ上の懸念は、機密データを扱うオートメーションシステムの脆弱性に起因しており、データ漏洩やサイバー攻撃のリスクを高めています。こうした懸念は、データの完全性やプライバシーが損なわれることを恐れ、企業がオートメーション技術に投資する意欲をなくすことで、市場の成長を妨げる可能性があります。セキュリティ・インシデントによって経済的・風評的に大きなダメージを受ける可能性があるため、監視の目が厳しくなり、コンプライアンス・コストが上昇し、採用率が鈍化し、最終的に市場全体の拡大に影響を及ぼす可能性があります。

カスタマイズ可能なオートメーションソリューションの採用拡大

カスタマイズにより、システムの効率性、柔軟性、既存のワークフローとの統合が強化され、さまざまな業界で幅広い導入が促進されます。企業が独自のプロセスに適合し、成長に合わせて拡張できるソリューションを求めるにつれ、カスタマイズ可能なオートメーションツールはより魅力的になり、市場の需要拡大につながります。この適応性は、多様な使用事例をサポートし、イノベーションを促進し、投資を促し、最終的に市場の成長と拡大を促進します。

導入の複雑さ

オフィスオートメーション導入の複雑さは、新しいシステムを既存のインフラと統合し、ソフトウェアを設定し、ワークフローを適応させることから生じます。このプロセスには専門的な知識、綿密な計画、現在のプロセスへの潜在的な調整が必要になることが多く、時間とコストがかかります。その結果、オートメーション技術の適用範囲が限定され、潜在的な効率向上が幅広い市場で実現されなくなるため、採用率の低迷が市場成長の妨げとなっています。

COVID-19の影響

COVID-19は、企業がリモートワークにシフトし、デジタルコラボレーションと効率性を強化する必要があったため、オフィスオートメーションの採用を加速させました。パンデミックは、クラウドベースのソリューション、仮想コミュニケーションツール、リモート業務をサポートするオートメーションソフトウェアへの需要を促進しました。このシフトは、急速に変化する労働環境において事業継続性と生産性を維持する役割を強調し、オフィスオートメーション技術の市場成長を増加させました。

予測期間中、人的資源管理セグメントが最大となる見込み

人的資源管理セグメントは、有利な成長を遂げると推定されます。人事管理では、オフィスオートメーションが採用、給与計算、業績管理などの業務を効率化します。オートメーションされたシステムは、従業員の記録を管理し、オンライン申請を容易にし、福利厚生管理を行うことで、手作業による労力とミスを削減します。スケジューリング、データ分析、コミュニケーションをオートメーションするツールは、効率性と正確性を高めます。オートメーションを活用することで、人事部門は戦略的な活動に集中し、従業員の経験や組織の有効性を全体的に向上させることができます。

予測期間中にCAGRが最も高くなると予測されるのは企業オフィスセグメントです。

企業オフィスセグメントは、予測期間中に最も高いCAGR成長が見込まれます。企業オフィスでは、文書管理、コミュニケーション、スケジューリングのためのソフトウェアを統合することで、オフィスオートメーションが日常業務を最適化します。オートメーションシステムは、レポート作成、会議調整、ワークフロー管理などのタスクを合理化し、効率性とコラボレーションを強化します。このテクノロジーは、手作業のプロセスを減らし、エラーを最小限に抑え、データ主導の意思決定をサポートします。日常業務をオートメーションすることで、企業のオフィスは生産性を向上させ、コストを削減し、より機敏な職場環境を育むことができます。

最大のシェアを占める地域:

アジア太平洋は、急速な技術進歩やデジタルソリューションの採用増加により、予測期間中に最大の市場シェアを占めると予測されています。この拡大を促進する要因としては、効率的なビジネスプロセスに対する需要の高まり、リモートワークの動向、クラウドコンピューティングやAI技術への投資の拡大などが挙げられます。中国、インド、日本などの国々は、堅牢なインフラと拡大する企業ニーズでリードしています。同地域の企業は生産性の向上と運用コストの削減を目指しており、オフィスオートメーションソリューション市場は引き続き急拡大しています。

CAGRが最も高い地域:

北米は、高い技術導入率と業務効率の改善に注力していることから、予測期間中のCAGRが最も高くなると予測されます。米国とカナダの企業は、クラウドサービス、AI、機械学習を含む高度なオートメーションソリューションに投資し、プロセスの合理化と生産性の向上を図っています。この地域は、イノベーションとデジタルトランスフォーメーションを重視しており、市場の成長を支えています。金融、ヘルスケア、製造業などの主要セクターは、ワークフローの最適化、コスト削減、ダイナミックなビジネス環境での競合維持のためにオフィスオートメーションを活用しており、大きな貢献をしています。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場企業の包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 技術分析

- 用途分析

- エンドユーザー分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界のオフィスオートメーション市場:タイプ別

- ハードウェア

- コンピューターとワークステーション

- プリンターとスキャナー

- コピー機

- 通信機器

- ソフトウェア

- コミュニケーションソフトウェア

- エンタープライズリソースプランニング(ERP)ソフトウェア

- カスタマーリレーションマネジメント(CRM)ソフトウェア

- サービス

- インストール・統合サービス

- メンテナンス・サポートサービス

- マネージドサービス

- コンサルティングサービス

第6章 世界のオフィスオートメーション市場:展開別

- オンプレミス

- クラウドベース

第7章 世界のオフィスオートメーション市場:組織規模別

- 中小企業

- 大企業

第8章 世界のオフィスオートメーション市場:技術別

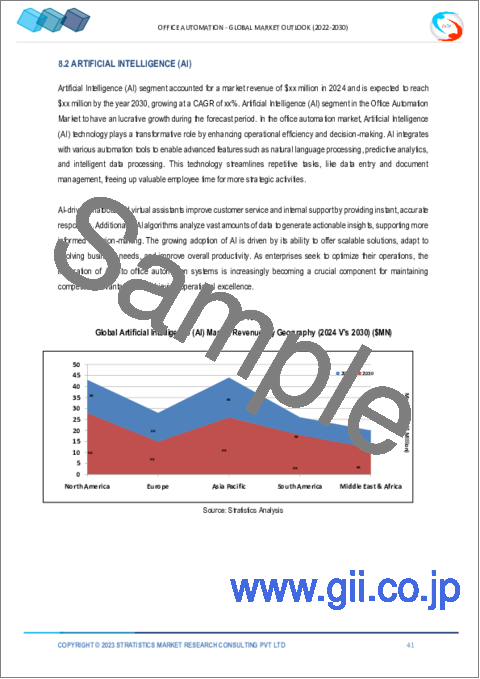

- 人工知能(AI)

- ロボティックプロセスオートメーション(RPA)

- モノのインターネット(IoT)

- 機械学習

- その他の技術

第9章 世界のオフィスオートメーション市場:用途別

- ドキュメント管理

- データ管理

- 会計と財務管理

- 人事管理

- その他の用途

第10章 世界のオフィスオートメーション市場:エンドユーザー別

- 企業オフィス

- 政府

- ヘルスケア

- 教育

- 小売

- 製造

- その他のエンドユーザー

第11章 世界のオフィスオートメーション市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東・アフリカ

第12章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第13章 企業プロファイリング

- Microsoft

- IBM

- Apple

- HP

- Canon

- Ricoh

- Xerox

- Epson

- Kyocera

- Brother

- Sharp

- Toshiba

- D-Link

- Cisco

List of Tables

- Table 1 Global Office Automation Market Outlook, By Region (2022-2030) ($MN)

- Table 2 Global Office Automation Market Outlook, By Type (2022-2030) ($MN)

- Table 3 Global Office Automation Market Outlook, By Hardware (2022-2030) ($MN)

- Table 4 Global Office Automation Market Outlook, By Computers & Workstations (2022-2030) ($MN)

- Table 5 Global Office Automation Market Outlook, By Printers & Scanners (2022-2030) ($MN)

- Table 6 Global Office Automation Market Outlook, By Photocopiers (2022-2030) ($MN)

- Table 7 Global Office Automation Market Outlook, By Telecommunication Equipment (2022-2030) ($MN)

- Table 8 Global Office Automation Market Outlook, By Software (2022-2030) ($MN)

- Table 9 Global Office Automation Market Outlook, By Communication Software (2022-2030) ($MN)

- Table 10 Global Office Automation Market Outlook, By Enterprise Resource Planning (ERP) Software (2022-2030) ($MN)

- Table 11 Global Office Automation Market Outlook, By Customer Relationship Management (CRM) Software (2022-2030) ($MN)

- Table 12 Global Office Automation Market Outlook, By Services (2022-2030) ($MN)

- Table 13 Global Office Automation Market Outlook, By Installation & Integration Services (2022-2030) ($MN)

- Table 14 Global Office Automation Market Outlook, By Maintenance & Support Services (2022-2030) ($MN)

- Table 15 Global Office Automation Market Outlook, By Managed Services (2022-2030) ($MN)

- Table 16 Global Office Automation Market Outlook, By Consulting Services (2022-2030) ($MN)

- Table 17 Global Office Automation Market Outlook, By Deployment (2022-2030) ($MN)

- Table 18 Global Office Automation Market Outlook, By On-premise (2022-2030) ($MN)

- Table 19 Global Office Automation Market Outlook, By Cloud-based (2022-2030) ($MN)

- Table 20 Global Office Automation Market Outlook, By Organization Size (2022-2030) ($MN)

- Table 21 Global Office Automation Market Outlook, By Small & Medium Enterprises (SMEs) (2022-2030) ($MN)

- Table 22 Global Office Automation Market Outlook, By Large Enterprises (2022-2030) ($MN)

- Table 23 Global Office Automation Market Outlook, By Technology (2022-2030) ($MN)

- Table 24 Global Office Automation Market Outlook, By Artificial Intelligence (AI) (2022-2030) ($MN)

- Table 25 Global Office Automation Market Outlook, By Robotic Process Automation (RPA) (2022-2030) ($MN)

- Table 26 Global Office Automation Market Outlook, By Internet Of Things (IoT) (2022-2030) ($MN)

- Table 27 Global Office Automation Market Outlook, By Machine Learning (2022-2030) ($MN)

- Table 28 Global Office Automation Market Outlook, By Other Technologies (2022-2030) ($MN)

- Table 29 Global Office Automation Market Outlook, By Application (2022-2030) ($MN)

- Table 30 Global Office Automation Market Outlook, By Document Management (2022-2030) ($MN)

- Table 31 Global Office Automation Market Outlook, By Data Management (2022-2030) ($MN)

- Table 32 Global Office Automation Market Outlook, By Accounting & Financial Management (2022-2030) ($MN)

- Table 33 Global Office Automation Market Outlook, By Human Resource Management (2022-2030) ($MN)

- Table 34 Global Office Automation Market Outlook, By Other Applications (2022-2030) ($MN)

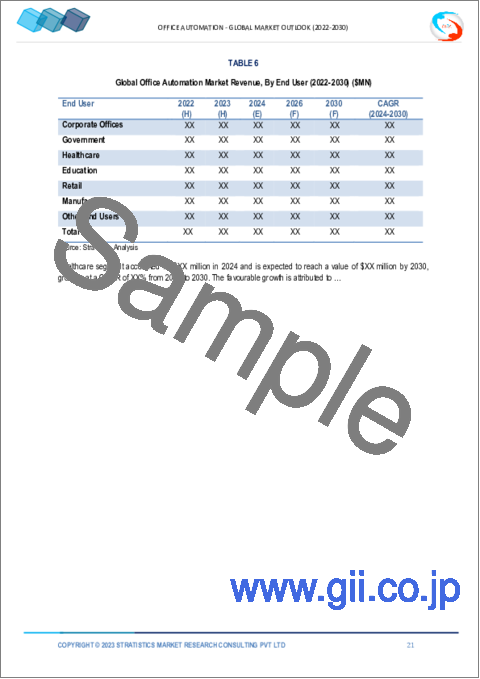

- Table 35 Global Office Automation Market Outlook, By End User (2022-2030) ($MN)

- Table 36 Global Office Automation Market Outlook, By Corporate Offices (2022-2030) ($MN)

- Table 37 Global Office Automation Market Outlook, By Government (2022-2030) ($MN)

- Table 38 Global Office Automation Market Outlook, By Healthcare (2022-2030) ($MN)

- Table 39 Global Office Automation Market Outlook, By Education (2022-2030) ($MN)

- Table 40 Global Office Automation Market Outlook, By Retail (2022-2030) ($MN)

- Table 41 Global Office Automation Market Outlook, By Manufacturing (2022-2030) ($MN)

- Table 42 Global Office Automation Market Outlook, By Other End Users (2022-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Office Automation Market is accounted for $425.27 million in 2024 and is expected to reach $882.73 million by 2030 growing at a CAGR of 12.1% during the forecast period. Office automation refers to the use of technology to perform office tasks and processes more efficiently. It involves integrating various systems and software to streamline workflows and enhance productivity. By automating repetitive tasks and managing information digitally, office automation reduces manual labor, minimizes errors, and improves communication within an organization.

According to the 2019 Singapore Government Trade Figures, the U.S. holds nearly 20% of Singapore's market share for automation equipment.

Market Dynamics:

Driver:

Rise of remote work and hybrid work models

The rise of remote and hybrid work models increases the demand for digital tools that support remote collaboration, communication, and productivity. Automation solutions such as cloud-based platforms, virtual collaboration tools, and workflow management systems enable seamless interactions and efficiency across distributed teams. As organizations adapt to flexible work environments, they seek automation technologies to maintain operational continuity, enhance team collaboration, and streamline processes, driving further investment and expansion in the office automation market.

Restraint:

Security concerns

Security concerns in office automation stem from vulnerabilities in automated systems that handle sensitive data, increasing the risk of data breaches and cyber-attacks. These concerns can hamper market growth by discouraging businesses from investing in automation technologies due to fears of compromising their data integrity and privacy. The potential for significant financial and reputational damage from security incidents can lead to increased scrutiny, higher compliance costs, and slower adoption rates, ultimately affecting overall market expansion.

Opportunity:

Growing adoption customizable automation solutions

Customization enhances system efficiency, flexibility, and integration with existing workflows, driving broader adoption across various industries. As businesses seek solutions that align with their unique processes and scale with their growth, customizable automation tools become more attractive, leading to increased market demand. This adaptability supports diverse use cases, fosters innovation, and encourages investment, ultimately fueling market growth and expansion.

Threat:

Complexity of implementation

The complexity of implementing office automation arises from integrating new systems with existing infrastructure, configuring software, and adapting workflows. This process often requires specialized knowledge, detailed planning, and potential adjustments to current processes, which can be time-consuming and costly. As a result, the slow adoption rate hampers market growth by limiting the reach of automation technologies and preventing potential efficiency gains from being realized across the broader market.

Covid-19 Impact

Covid-19 accelerated the adoption of office automation as businesses shifted to remote work and needed to enhance digital collaboration and efficiency. The pandemic drove demand for cloud-based solutions, virtual communication tools, and automation software to support remote operations. This shift increased market growth for office automation technologies, highlighting their role in maintaining business continuity and productivity in a rapidly changing work environment.

The human resource management segment is expected to be the largest during the forecast period

The human resource management segment is estimated to have a lucrative growth. In human resource management, office automation streamlines tasks like recruitment, payroll, and performance management. Automated systems manage employee records, facilitate online applications, and handle benefits administration, reducing manual effort and errors. Tools for automated scheduling, data analysis and communication enhance efficiency and accuracy. By leveraging automation, HR departments can focus on strategic activities and improve overall employee experience and organizational effectiveness.

The corporate offices segment is expected to have the highest CAGR during the forecast period

The corporate offices segment is anticipated to witness the highest CAGR growth during the forecast period. In corporate offices, office automation optimizes daily operations by integrating software for document management, communication, and scheduling. Automated systems streamline tasks such as report generation, meeting coordination, and workflow management, enhancing efficiency and collaboration. This technology reduces manual processes, minimizes errors, and supports data-driven decision-making. By automating routine activities, corporate offices can improve productivity, reduce costs, and foster a more agile work environment.

Region with largest share:

Asia Pacific is projected to hold the largest market share during the forecast period due to rapid technological advancements and increasing adoption of digital solutions. Factors driving this expansion include the rising demand for efficient business processes, remote work trends, and growing investments in cloud computing and AI technologies. Countries like China, India, and Japan are leading the way with robust infrastructure and expanding enterprise needs. As businesses in the region seek to enhance productivity and reduce operational costs, the market for office automation solutions continues to expand rapidly.

Region with highest CAGR:

North America is projected to have the highest CAGR over the forecast period, owing to high technology adoption and a focus on improving operational efficiency. Businesses across the U.S. and Canada are investing in advanced automation solutions, including cloud services, AI, and machine learning, to streamline processes and enhance productivity. The region's strong emphasis on innovation and digital transformation supports market growth. Key sectors like finance, healthcare, and manufacturing are major contributors, leveraging office automation to optimize workflows, reduce costs, and stay competitive in a dynamic business environment.

Key players in the market

Some of the key players profiled in the Office Automation Market include Microsoft, IBM, Google, Apple, HP, Canon, Ricoh, Xerox, Epson, Kyocera, Brother, Sharp, Toshiba, D-Link and Cisco.

Key Developments:

In May 2024, IBM released a family of Granite models into open source and launched InstructLab, a first-of-its-kind capability, in collaboration with Red Hat. The 20B parameter Granite base code model was used to train IBM watsonx Code Assistant (WCA) for specialized domains.

In November 2023, Microsoft launched the new AI tool "Copilot". It is more than just another AI tool, with the ability to draft and even refine emails. Copilot can condense extensive email chains into concise summaries, such as those regarding product launches.

Types Covered:

- Hardware

- Software

- Services

Deployments Covered:

- On-premise

- Cloud-based

Organization Sizes Covered:

- Small & Medium Enterprises (SMEs)

- Large Enterprises

Technologies Covered:

- Artificial Intelligence (AI)

- Robotic Process Automation (RPA)

- Internet Of Things (IoT)

- Machine Learning

- Other Technologies

Applications Covered:

- Document Management

- Data Management

- Accounting & Financial Management

- Human Resource Management

- Other Applications

End Users Covered:

- Corporate Offices

- Government

- Healthcare

- Education

- Retail

- Manufacturing

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2022, 2023, 2024, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Technology Analysis

- 3.7 Application Analysis

- 3.8 End User Analysis

- 3.9 Emerging Markets

- 3.10 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Office Automation Market, By Type

- 5.1 Introduction

- 5.2 Hardware

- 5.2.1 Computers & Workstations

- 5.2.2 Printers & Scanners

- 5.2.3 Photocopiers

- 5.2.4 Telecommunication Equipment

- 5.3 Software

- 5.3.1 Communication Software

- 5.3.2 Enterprise Resource Planning (ERP) Software

- 5.3.3 Customer Relationship Management (CRM) Software

- 5.4 Services

- 5.4.1 Installation & Integration Services

- 5.4.2 Maintenance & Support Services

- 5.4.3 Managed Services

- 5.4.4 Consulting Services

6 Global Office Automation Market, By Deployment

- 6.1 Introduction

- 6.2 On-premise

- 6.3 Cloud-based

7 Global Office Automation Market, By Organization Size

- 7.1 Introduction

- 7.2 Small & Medium Enterprises (SMEs)

- 7.3 Large Enterprises

8 Global Office Automation Market, By Technology

- 8.1 Introduction

- 8.2 Artificial Intelligence (AI)

- 8.3 Robotic Process Automation (RPA)

- 8.4 Internet Of Things (IoT)

- 8.5 Machine Learning

- 8.6 Other Technologies

9 Global Office Automation Market, By Application

- 9.1 Introduction

- 9.2 Document Management

- 9.3 Data Management

- 9.4 Accounting & Financial Management

- 9.5 Human Resource Management

- 9.6 Other Applications

10 Global Office Automation Market, By End User

- 10.1 Introduction

- 10.2 Corporate Offices

- 10.3 Government

- 10.4 Healthcare

- 10.5 Education

- 10.6 Retail

- 10.7 Manufacturing

- 10.8 Other End Users

11 Global Office Automation Market, By Geography

- 11.1 Introduction

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 Italy

- 11.3.4 France

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 Japan

- 11.4.2 China

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 New Zealand

- 11.4.6 South Korea

- 11.4.7 Rest of Asia Pacific

- 11.5 South America

- 11.5.1 Argentina

- 11.5.2 Brazil

- 11.5.3 Chile

- 11.5.4 Rest of South America

- 11.6 Middle East & Africa

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 Qatar

- 11.6.4 South Africa

- 11.6.5 Rest of Middle East & Africa

12 Key Developments

- 12.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 12.2 Acquisitions & Mergers

- 12.3 New Product Launch

- 12.4 Expansions

- 12.5 Other Key Strategies

13 Company Profiling

- 13.1 Microsoft

- 13.2 IBM

- 13.3 Google

- 13.4 Apple

- 13.5 HP

- 13.6 Canon

- 13.7 Ricoh

- 13.8 Xerox

- 13.9 Epson

- 13.10 Kyocera

- 13.11 Brother

- 13.12 Sharp

- 13.13 Toshiba

- 13.14 D-Link

- 13.15 Cisco