|

市場調査レポート

商品コード

1892902

ドックスケジューリングソフトウェア市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Dock Scheduling Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| ドックスケジューリングソフトウェア市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月08日

発行: Global Market Insights Inc.

ページ情報: 英文 240 Pages

納期: 2~3営業日

|

概要

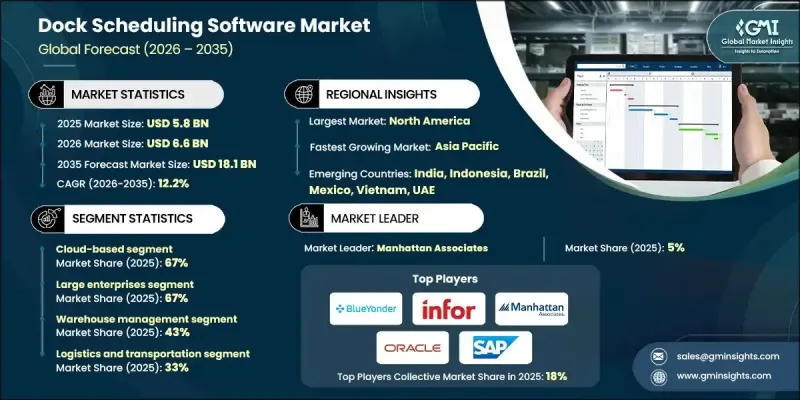

世界のドックスケジューリングソフトウェア市場は、2025年に58億米ドルと評価され、2035年までにCAGR12.2%で成長し、181億米ドルに達すると予測されております。

業務効率化への需要の高まりが導入を促進しており、トラックのドック滞在時間を最小化することは、コスト削減とターンアラウンドタイム短縮に不可欠です。ドックスケジューリングソフトウェアは、企業のドア使用の最適化と予約手配を可能にし、小売、食料品、電子商取引セクターにおける大量輸送を扱う運送業者のアイドル時間を削減し、サービスレベルを向上させます。人手不足と採用コストの上昇により、倉庫では人員配置をより戦略的に行う必要が生じています。スケジューリングソフトウェアは、予想される出荷量に基づいて人員要件を予測し、最も混雑するドックに従業員を割り当てます。さらに、規制順守と業界の安全基準をサポートし、ドライバーの勤務時間を追跡し、違反を報告し、運転時間の規制への順守を確保しながら、ドライバーの安全と業務効率を維持します。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 58億米ドル |

| 予測金額 | 181億米ドル |

| CAGR | 12.2% |

クラウドベースのセグメントは2025年に67%のシェアを占め、2035年までCAGR 12.5%で成長すると予測されています。クラウド導入により、SaaSサブスクリプションモデルを通じてリアルタイムの運送会社統合、モバイルアクセス、初期費用の削減が可能となり、IT管理負担も軽減されます。

大企業セグメントは、広範な倉庫ネットワーク、複数のドックドア、複雑な複数運送業者との連携業務を背景に、2025年に67%の市場シェアを占めました。これらの企業は、AIを活用した最適化、複数拠点の可視化、WMS(倉庫管理システム)およびTMS(輸送管理システム)との深い連携により、地域および全国の流通センターにおいて一貫したプロセスを維持しています。

米国のドックスケジューリングソフトウェア市場は2025年に47億6,000万米ドルの規模に達しました。成長の背景には、トラック輸送能力の逼迫、貨物輸送の高速化、滞留時間に対する規制当局の監視強化があります。自動化、IoTデバイス、セルフサービスポータルは、業務の正確性を高め、流通センターにおける製品受入の適時性を向上させます。

よくあるご質問

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 滞留時間の削減が必要

- 労働力の最適化

- 規制・コンプライアンス上の圧力

- 現代のサプライチェーンの複雑性

- 業界の潜在的リスク&課題

- 統合の複雑性

- 運送業者およびスタッフの採用抵抗

- 市場機会

- 中小企業(SMB)セグメントへの拡大

- 電子商取引(Eコマース)とオムニチャネル物流

- 新興市場(アジア太平洋地域、ラテンアメリカ、中東・アフリカ)

- 自動化とロボティクスの統合

- 促進要因

- 成長可能性分析

- 規制情勢

- 世界

- 安全及び性能基準

- 環境・サステナビリティ規制

- データプライバシー及び越境データ転送

- 輸送・貨物規制

- 業界固有のコンプライアンス

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 世界

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- スケジューリングエンジンと最適化アルゴリズム

- テレマティクス及び到着予定時刻(ETA)フィード

- リアルタイムヤード/トレーラー位置情報

- モバイルドライバーアプリと運送会社向けポータル

- 新興技術

- AIを活用した予測スケジューリングと異常検知

- ヤード・ドックフロー計画のためのデジタルツインとシミュレーション

- ブロックチェーンを活用した予約の追跡可能性と監査証跡

- 自律走行ヤード車両およびロボットによるドックハンドリング

- 現在の技術動向

- 価格分析

- 導入形態別価格設定

- 単位メトリクスに基づく価格設定

- 機能レベル別価格設定

- 専門サービス及び統合コスト

- コスト内訳分析

- ベンダーのコスト構造

- コスト構成要素の導入

- 継続的な運営コスト

- 間接的な顧客コスト

- 特許分析

- 主要ベンダーによる特許権の所有状況

- 実施の自由と知的財産訴訟の動向

- サステナビリティと環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- リスク評価・軽減フレームワーク

- サプライチェーンリスク

- 財務・経済リスク

- 規制・コンプライアンスリスク

- 業務リスク

- 技術・イノベーションリスク

- エンドユーザー行動と消費分析

- エンドユースセグメンテーションフレームワーク

- 3PLおよび物流プロバイダーの行動とマルチテナントのニーズ

- 小売業および電子商取引の採用パターン

- 製造およびJITユーザーの行動

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:導入形態別、2022-2035

- クラウドベース

- オンプレミス

- ハイブリッド

第6章 市場推計・予測:企業規模別、2022-2035

- 大企業

- 中小企業

第7章 市場推計・予測:用途別、2022-2035

- 倉庫管理

- 輸送管理

- ヤード管理

- クロスドッキング業務

- その他

第8章 市場推計・予測:ソリューション別、2022-2035

- スタンドアロン型ドックスケジューリングソフトウェア

- 統合サプライチェーン管理ソリューション

- ヤード管理システム(ドックスケジューリング機能付き)

第9章 市場推計・予測:コンポーネント別、2022-2035

- ソフトウェア

- サービス

第10章 市場推計・予測:最終用途別、2022-2035

- 物流・輸送

- 小売業および電子商取引

- 製造業

- 食品・飲料

- 医療・医薬品分野

- 卸売・流通

- その他

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- ポーランド

- ルーマニア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ANZ

- ベトナム

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- 世界企業

- Blue Yonder

- C3 Solutions

- Descartes Systems

- FourKites

- Infor

- Korber Supply Chain

- Manhattan Associates

- Oracle

- project44

- SAP

- Zebra Technologies

- 地域プレイヤー

- SIGHT Connect

- Alpega

- Dock411

- E2 open

- GoRamp

- Kale Logistics Solutions

- Opendock

- Softeon

- Transporeon

- Trimble Transportation

- Velostics

- YardView

- 新興企業

- Arrivy

- Conduit

- DataDocks

- Epicor Software

- Extensiv(formerly 3 PL Central)

- LoadingCalendar