|

|

市場調査レポート

商品コード

1503297

集積型パッシブデバイス市場の2030年までの予測: パッシブデバイス、基板、ワイヤレス技術、エンドユーザー、地域別の世界分析Integrated Passive Devices Market Forecasts to 2030 - Global Analysis By Passive Device, Substrate, Wireless Technology, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 集積型パッシブデバイス市場の2030年までの予測: パッシブデバイス、基板、ワイヤレス技術、エンドユーザー、地域別の世界分析 |

|

出版日: 2024年06月06日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、集積型パッシブデバイスの世界市場は2024年に22億2,000万米ドルを占め、2030年には44億3,000万米ドルに達すると予測され、予測期間中のCAGRは12.23%です。

集積型パッシブデバイス(IPDs)とは、基板上に直接製造される小型化された電子部品のことで、多くの場合、半導体製造技術を用いて製造されます。これらのデバイスは、抵抗器、コンデンサ、インダクタなどの複数の受動部品を1つのパッケージに統合することで、サイズ、重量、製造の複雑さを低減しています。IPDは、携帯電話、ウェアラブル機器、IoT機器など、スペースに制約のある現代の電子システムで広く使用されています。

インド・ブランド・エクイティ財団(IBEF)によると、インドの家電・民生用電子機器市場は2021年に98億4,000万米ドルと評価され、2025年には211億8,000万米ドルになると予想されています。

高周波アプリケーションへの需要の高まり

集積型パッシブデバイスは、ディスクリート受動部品に比べて小型で性能が向上し、コスト効率が高いため、モバイル通信、IoTデバイス、車載エレクトロニクスに不可欠な存在になりつつあります。これらのデバイスは、回路基板上のフットプリントの縮小、信頼性の向上、高周波動作に不可欠なシグナルインテグリティの向上などの利点を提供します。5Gネットワークの普及とIoTエコシステムの拡大に伴い、電子部品の小型化と効率化の必要性が高まっています。この動向は、メーカーに革新とIPD製品の拡充を促し、最新技術の進化するニーズに応えています。

設計の複雑さ

しかし、こうした集積デバイスの設計には、材料科学、回路設計、製造プロセスなど、さまざまな分野の複雑な知識が必要です。複雑さは、既存の電子システムとの互換性を確保しながら、電気的性能、熱管理、信頼性を最適化する必要性から生じる。さらに、高い歩留まりを達成し、費用対効果を維持することが、設計プロセスをさらに複雑にしています。その結果、IPDに投資する企業は、市場の可能性を生かすためにこれらの課題を克服しなければならないです。

無線周波数アプリケーションの増加

5Gのような無線通信技術が普及し続ける中、コンパクトで効率的なRF部品への需要が高まっています。抵抗器、コンデンサ、インダクタなどの受動部品を1つのデバイスに統合したIPDは、小型化、性能、信頼性の面で大きな利点を提供します。製造工程を合理化し、システム全体のフットプリントを削減できるIPDは、スマートフォン、IoT機器、車載電子機器、医療機器などのRFアプリケーションにとって特に魅力的です。さらに、RF回路の複雑化と性能要件の高まりにより、IPDが提供する高度な集積技術が必要とされています。

メーカーの利益率低下

コンデンサ、抵抗器、インダクタなどの部品を1つのパッケージに集積した集積型パッシブデバイスは、製造業者の利益率低下により大きな課題に直面しています。利益率が低下すると、メーカーは研究開発投資を削減し、技術革新や先進的なIPD技術の導入が制限される可能性があります。さらに、収益性の低下はマーケティング予算の抑制につながり、従来のディスクリート受動部品よりもIPDが優れていることを潜在顧客に宣伝・啓蒙する努力の妨げになる可能性があります。

COVID-19の影響:

当初、世界のサプライチェーンの混乱は製造の遅れや部品不足を引き起こし、IPDの生産と納品スケジュールに影響を与えました。世界中でロックダウンや規制が課されたため、民生用電子機器の需要が変動し、市場環境が不透明となり、技術アップグレードへの投資が減少しました。さらに、リモートワークとデジタル化へのシフトは、強固な接続性と効率性を備えた機器への需要を加速させ、メーカーが求めるIPDの種類に影響を与えました。こうした課題にもかかわらず、パンデミックはIPD設計の革新にも拍車をかけ、進化する消費者ニーズに対応するため、フォームファクタの小型化、低消費電力化、性能強化が重視されるようになった。

予測期間中、バランセグメントが最大になる見込み

予測期間中、バランセグメントが最大となる見込みです。これらのデバイスは、無線周波数(RF)アプリケーションにおける平衡信号と不平衡信号の変換に不可欠であり、効率的な信号の送受信を促進します。抵抗器、コンデンサ、インダクタなど複数の受動部品を1つのパッケージに統合するIPDにおいて、バランは信号損失を最小限に抑え、インピーダンス整合を確保することで回路性能を最適化する役割を果たします。この機能は、シグナルインテグリティの維持と効率の最大化が最重要課題である無線通信システムにおいて特に価値が高いです。

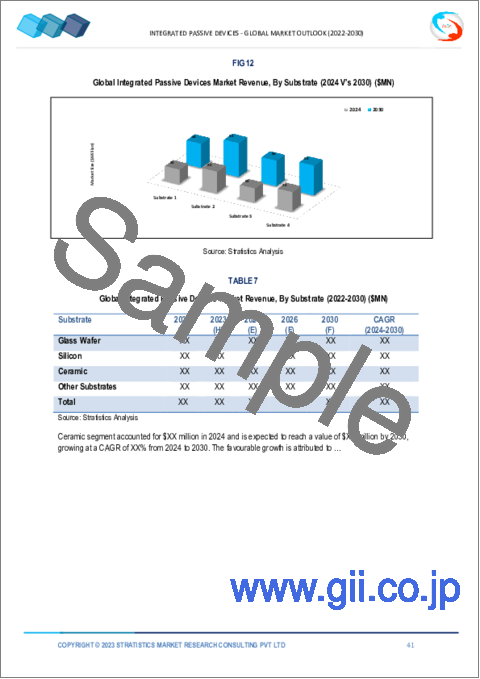

予測期間中、CAGRが最も高くなると予想されるのはガラスウエハ・セグメントです。

予測期間中、CAGRが最も高くなると予想されるのはガラスウエハー分野です。ガラス・ウエハは、シリコンやセラミックのような従来の基板に比べ、優れた電気特性、熱安定性、小規模での製造性など、いくつかの利点を提供します。ガラス・ウエハは、より高い集積密度と寄生効果を低減したIPDの精密な製造を可能にし、回路全体の性能を向上させる。フォトリソグラフィやエッチングなどの高度な製造技術との互換性は、IPDアプリケーションにおけるガラスの魅力をさらに高めています。さらに、ガラスの特定の波長における優れた透明性は、IPDのオプトエレクトロニクス用途にも活用できます。

最大シェアの地域

アジア太平洋地域が推定期間中、市場で最大のシェアを占めています。複数の受動部品を1つのパッケージにまとめた集積型パッシブデバイスは、エレクトロニクス製造、特にアジア太平洋地域の家電、通信、自動車分野でますます重要になってきています。これらのデバイスは、設置面積の縮小、性能の向上、組み立てコストの削減といった利点を提供し、この地域におけるコンパクトで高性能な電子機器の重視に合致しています。さらに、アジア太平洋地域の強固な製造基盤と技術的専門知識は、IPDの開発・製造の一大拠点となっています。

CAGRが最も高い地域:

欧州地域は、予測期間中に収益性の高い成長を維持する見込みです。同地域の規制枠組みは環境保護を優先しており、IPDメーカーはエネルギー効率が高く環境に優しいソリューションを開発する必要に迫られています。技術進歩と研究資金を支援する政策は、この分野の成長をさらに刺激します。こうした規制は、企業がIPD技術に投資しやすい環境を整え、競争力を高め、強固な市場エコシステムを育んでいます。さらに、欧州規格への準拠は市場の信頼性を高め、国際市場へのアクセスを容易にし、世界な投資を誘致します。

無料のカスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレーヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- エンドユーザー分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の集積型パッシブデバイス市場: パッシブデバイス別

- ダイプレクサー

- カスタムIPD

- カプラ

- バラン

- 共振器

- 減衰器

- 電力分配器/結合器

- その他の パッシブデバイス

第6章 世界の集積型パッシブデバイス市場:基板別

- ガラスウエハー

- ケイ素

- セラミック

- その他の基板

第7章 世界の集積型パッシブデバイス市場:ワイヤレス技術別

- セルラー

- Bluetooth

- 無線ローカルエリアネットワーク

- その他のワイヤレステクノロジー

第8章 世界の集積型パッシブデバイス市場:エンドユーザー別

- 自動車

- 家電

- 航空宇宙および防衛

- ヘルスケア

- ITおよび通信

- エネルギーとユーティリティ

- その他のエンドユーザー

第9章 世界の集積型パッシブデバイス市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第10章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第11章 企業プロファイリング

- NXP Semiconductors

- Murata Manufacturing Co., Ltd

- Infineon Technologies AG

- Taiwan Semiconductor Manufacturing Company

- Samsung Electro-Mechanics

- Qualcomm Technologies, Inc

- TDK Corporation

- Yageo Corporation

- Skyworks Solutions

- API Technologies

- Kyocera Corporation

List of Tables

- Table 1 Global Integrated Passive Devices Market Outlook, By Region (2022-2030) ($MN)

- Table 2 Global Integrated Passive Devices Market Outlook, By Passive Device (2022-2030) ($MN)

- Table 3 Global Integrated Passive Devices Market Outlook, By Diplexers (2022-2030) ($MN)

- Table 4 Global Integrated Passive Devices Market Outlook, By Customized IPDs (2022-2030) ($MN)

- Table 5 Global Integrated Passive Devices Market Outlook, By Couplers (2022-2030) ($MN)

- Table 6 Global Integrated Passive Devices Market Outlook, By Baluns (2022-2030) ($MN)

- Table 7 Global Integrated Passive Devices Market Outlook, By Resonators (2022-2030) ($MN)

- Table 8 Global Integrated Passive Devices Market Outlook, By Attenuators (2022-2030) ($MN)

- Table 9 Global Integrated Passive Devices Market Outlook, By Power Splitters/Combiners (2022-2030) ($MN)

- Table 10 Global Integrated Passive Devices Market Outlook, By Other Passive Devices (2022-2030) ($MN)

- Table 11 Global Integrated Passive Devices Market Outlook, By Substrate (2022-2030) ($MN)

- Table 12 Global Integrated Passive Devices Market Outlook, By Glass Wafer (2022-2030) ($MN)

- Table 13 Global Integrated Passive Devices Market Outlook, By Silicon (2022-2030) ($MN)

- Table 14 Global Integrated Passive Devices Market Outlook, By Ceramic (2022-2030) ($MN)

- Table 15 Global Integrated Passive Devices Market Outlook, By Other Substrates (2022-2030) ($MN)

- Table 16 Global Integrated Passive Devices Market Outlook, By Wireless Technology (2022-2030) ($MN)

- Table 17 Global Integrated Passive Devices Market Outlook, By Cellular (2022-2030) ($MN)

- Table 18 Global Integrated Passive Devices Market Outlook, By Bluetooth (2022-2030) ($MN)

- Table 19 Global Integrated Passive Devices Market Outlook, By Wireless local-area Network (2022-2030) ($MN)

- Table 20 Global Integrated Passive Devices Market Outlook, By Other Wireless Technologies (2022-2030) ($MN)

- Table 21 Global Integrated Passive Devices Market Outlook, By End User (2022-2030) ($MN)

- Table 22 Global Integrated Passive Devices Market Outlook, By Automotive (2022-2030) ($MN)

- Table 23 Global Integrated Passive Devices Market Outlook, By Consumer Electronics (2022-2030) ($MN)

- Table 24 Global Integrated Passive Devices Market Outlook, By Aerospace & Defense (2022-2030) ($MN)

- Table 25 Global Integrated Passive Devices Market Outlook, By Healthcare (2022-2030) ($MN)

- Table 26 Global Integrated Passive Devices Market Outlook, By IT & Telecommunication (2022-2030) ($MN)

- Table 27 Global Integrated Passive Devices Market Outlook, By Energy and Utility (2022-2030) ($MN)

- Table 28 Global Integrated Passive Devices Market Outlook, By Other End Users (2022-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Integrated Passive Devices Market is accounted for $2.22 billion in 2024 and is expected to reach $4.43 billion by 2030 growing at a CAGR of 12.23% during the forecast period. Integrated Passive Devices (IPDs) refer to miniaturized electronic components that are fabricated directly onto a substrate, often using semiconductor fabrication techniques. These devices consolidate multiple passive components, such as resistors, capacitors, and inductors, into a single package, thereby reducing size, weight, and manufacturing complexity. IPDs are widely used in modern electronic systems where space is constrained, such as mobile phones, wearables, and IoT devices.

According to the India Brand Equity Foundation (IBEF), the Indian appliances and consumer electronics market was valued at US$ 9.84 billion in 2021 and is expected to be valued at US$ 21.18 billion by 2025.

Market Dynamics:

Driver:

Rising demand for high-frequency applications

Integrated Passive Devices are becoming integral in mobile communication, IoT devices, and automotive electronics due to their compact size, improved performance, and cost-effectiveness compared to discrete passive components. These devices offer advantages such as reduced footprint on circuit boards, enhanced reliability, and better signal integrity, crucial for high-frequency operations. With the proliferation of 5G networks and the expanding IoT ecosystem, the need for miniaturization and efficiency in electronic components has intensified. This trend is prompting manufacturers to innovate and expand their IPD offerings, catering to the evolving needs of modern technology.

Restraint:

Design complexity

However, designing these integrated devices requires intricate knowledge of various disciplines including materials science, circuit design, and manufacturing processes. The complexity arises from the need to optimize electrical performance, thermal management, and reliability while ensuring compatibility with existing electronic systems. Moreover, achieving high yields and maintaining cost-effectiveness further complicates the design process. As a result, companies investing in IPDs must navigate these challenges to capitalize on the market's potential.

Opportunity:

Rising radio frequency applications

As wireless communication technologies like 5G continue to proliferate, there is a heightened demand for compact and efficient RF components. IPDs, which integrate passive components such as resistors, capacitors, and inductors into a single device, offer substantial advantages in terms of miniaturization, performance, and reliability. Their ability to streamline manufacturing processes and reduce overall system footprint makes them particularly attractive for RF applications in smartphones, IoT devices, automotive electronics, and medical devices. Moreover, the increasing complexity and performance requirements of RF circuits necessitate advanced integration techniques provided by IPDs.

Threat:

Declining profit margins of manufacturers

Integrated Passive Devices, which include components like capacitors, resistors, and inductors integrated into a single package, face significant challenges due to reduced profitability among their producers. As profit margins shrink, manufacturers may cut back on research and development investments, limiting innovation and the introduction of advanced IPD technologies. Furthermore, reduced profitability can lead to constrained marketing budgets, hindering efforts to promote and educate potential customers about the benefits of IPDs over traditional discrete passive components.

Covid-19 Impact:

Initially, disruptions in the global supply chain caused manufacturing delays and component shortages, affecting IPD production and delivery schedules. As lockdowns and restrictions were imposed worldwide, demand for consumer electronics fluctuated, leading to uncertain market conditions and reduced investments in technology upgrades. Additionally, the shift towards remote work and digitalization accelerated the demand for devices with robust connectivity and efficiency, influencing the types of IPDs sought by manufacturers. Despite these challenges, the pandemic also spurred innovation in IPD designs, emphasizing smaller form factors, lower power consumption, and enhanced performance to meet evolving consumer needs.

The Baluns segment is expected to be the largest during the forecast period

Baluns segment is expected to be the largest during the forecast period. These devices are crucial in converting between balanced and unbalanced signals in radio frequency (RF) applications, facilitating efficient signal transmission and reception. In IPD, which integrates multiple passive components like resistors, capacitors, and inductors into a single package, baluns serve to optimize circuit performance by minimizing signal loss and ensuring impedance matching. This capability is particularly valuable in wireless communication systems, where maintaining signal integrity and maximizing efficiency are paramount.

The Glass Wafer segment is expected to have the highest CAGR during the forecast period

Glass Wafer segment is expected to have the highest CAGR during the forecast period. Glass wafers offer several advantages over traditional substrates like silicon or ceramic, including superior electrical properties, thermal stability, and manufacturability at smaller scales. Glass wafers enable higher integration densities and precise fabrication of IPDs with reduced parasitic effects, enhancing overall circuit performance. Their compatibility with advanced manufacturing techniques such as photolithography and etching further boosts their appeal for IPD applications. Moreover, glass's excellent transparency in certain wavelengths can also be leveraged for optoelectronic applications in IPDs.

Region with largest share:

Asia Pacific region commanded the largest share of the market over the extrapolated period. Integrated Passive Devices, which combine multiple passive components into a single package, are becoming increasingly crucial in electronics manufacturing, particularly in consumer electronics, telecommunications, and automotive sectors across the region. These devices offer advantages such as smaller footprint, improved performance, and reduced assembly costs, aligning with the region's emphasis on compact, high-performance electronics in the region. Furthermore, Asia Pacific's robust manufacturing base and technological expertise make it a prime hub for IPD development and production.

Region with highest CAGR:

Europe region is poised to hold profitable growth during the projection period. The region's regulatory framework prioritizes environmental conservation, which compels IPD manufacturers to develop energy-efficient and eco-friendly solutions. Policies supporting technological advancement and research funding further stimulate growth in the sector. These regulations create a conducive environment for businesses to invest in IPD technologies, driving competitiveness and fostering a robust market ecosystem. Moreover, compliance with European standards enhances market credibility and facilitates international market access, attracting global investments.

Key players in the market

Some of the key players in Integrated Passive Devices market include NXP Semiconductors, Murata Manufacturing Co., Ltd, Infineon Technologies AG, Taiwan Semiconductor Manufacturing Company, Samsung Electro-Mechanics, Qualcomm Technologies, Inc, TDK Corporation, Yageo Corporation, Skyworks Solutions, API Technologies and Kyocera Corporation.

Key Developments:

In May 2022, STMicroelectronics, an electronics and semiconductor manufacturing company, collaborated with Microsoft, an ST authorized company, for leading the development of the IoT devices. This collaboration has brought about security features, provided secure boot and storage, and fulfilled customer demands for efficient and trusted solutions.

In March 2022, MACOM Technology announced availability of its 128 GBaud Transimpedance Amplifiers (TIAs) and Modulator Drivers for coherent optical networking applications. MACOM's new products support long-haul, metropolitan and Data Center Interconnect (DCI) optical module applications.

Passive Devices Covered:

- Diplexers

- Customized IPDs

- Couplers

- Baluns

- Resonators

- Attenuators

- Power Splitters/Combiners

- Other Passive Devices

Substrates Covered:

- Glass Wafer

- Silicon

- Ceramic

- Other Substrates

Wireless Technologies Covered:

- Cellular

- Bluetooth

- Wireless local-area Network

- Other Wireless Technologies

End Users Covered:

- Automotive

- Consumer Electronics

- Aerospace & Defense

- Healthcare

- IT & Telecommunication

- Energy and Utility

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2022, 2023, 2024, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 End User Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Integrated Passive Devices Market, By Passive Device

- 5.1 Introduction

- 5.2 Diplexers

- 5.3 Customized IPDs

- 5.4 Couplers

- 5.5 Baluns

- 5.6 Resonators

- 5.7 Attenuators

- 5.8 Power Splitters/Combiners

- 5.9 Other Passive Devices

6 Global Integrated Passive Devices Market, By Substrate

- 6.1 Introduction

- 6.2 Glass Wafer

- 6.3 Silicon

- 6.4 Ceramic

- 6.5 Other Substrates

7 Global Integrated Passive Devices Market, By Wireless Technology

- 7.1 Introduction

- 7.2 Cellular

- 7.3 Bluetooth

- 7.4 Wireless local-area Network

- 7.5 Other Wireless Technologies

8 Global Integrated Passive Devices Market, By End User

- 8.1 Introduction

- 8.2 Automotive

- 8.3 Consumer Electronics

- 8.4 Aerospace & Defense

- 8.5 Healthcare

- 8.6 IT & Telecommunication

- 8.7 Energy and Utility

- 8.8 Other End Users

9 Global Integrated Passive Devices Market, By Geography

- 9.1 Introduction

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 Italy

- 9.3.4 France

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 New Zealand

- 9.4.6 South Korea

- 9.4.7 Rest of Asia Pacific

- 9.5 South America

- 9.5.1 Argentina

- 9.5.2 Brazil

- 9.5.3 Chile

- 9.5.4 Rest of South America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 Qatar

- 9.6.4 South Africa

- 9.6.5 Rest of Middle East & Africa

10 Key Developments

- 10.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 10.2 Acquisitions & Mergers

- 10.3 New Product Launch

- 10.4 Expansions

- 10.5 Other Key Strategies

11 Company Profiling

- 11.1 NXP Semiconductors

- 11.2 Murata Manufacturing Co., Ltd

- 11.3 Infineon Technologies AG

- 11.4 Taiwan Semiconductor Manufacturing Company

- 11.5 Samsung Electro-Mechanics

- 11.6 Qualcomm Technologies, Inc

- 11.7 TDK Corporation

- 11.8 Yageo Corporation

- 11.9 Skyworks Solutions

- 11.10 API Technologies

- 11.11 Kyocera Corporation