|

|

市場調査レポート

商品コード

1483043

集積受動素子(IPD)の世界市場(2024年~2031年)Global Integrated Passive Devices (IPDs) Market 2024-2031 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 集積受動素子(IPD)の世界市場(2024年~2031年) |

|

出版日: 2024年03月16日

発行: Orion Market Research

ページ情報: 英文 145 Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

世界の集積受動素子(IPD)の市場規模は、予測期間(2024年~2031年)に12.6%のCAGRで成長すると予測されています。 モバイル機器、IoT機器、5GインフラストラクチャなどのRF(Radio Frequency)用途における集積受動素子の需要増に伴う無線通信技術の採用拡大が、市場成長の原動力となっています。IPDは、ゲームシステム、ワイヤレススピーカー、ルーター、セットトップボックス、ドローン、ウェアラブル・ヒアラブル技術、スマートテレビ、スマート家電などの家電での使用が増加しています。

市場力学

RFフロントエンドモジュールの採用増加

RFフロントエンドモジュール(FEM)は、RF信号をブーストしてリンクの範囲、強度、耐障害性を拡張するために使用されます。RF IPD(RF-integrated Passive Device)は、コンデンサやインジケータなどの品質要素部品を集積するために高抵抗基板を使用します。IPD技術は、パワーコンバイナ/スプリッタ、カプラ、高調波フィルタ、インピーダンス整合ネットワーク、バランなど、幅広い部品の構築に使用できます。IPDは、ファウンドリーサービスに加えて、フィルターやバランのようなスタンドアロンのアイテムも提供しています。ワイヤーボンディング、マイクロバンピング、CSPなど、さまざまな組み立て方法との互換性により、完全なRFモジュールとして、またはメインプリント配線板(PWB)上に実装することができます。

高周波用途向けTGV(Through Glass-Via)基板を用いたIPDの進歩

モバイル高速接続の需要は増加の一途をたどっています。ガラス薄膜を用いたIPDは、TSV(Through Silicon-Via)基板を用いたIPDよりも好まれています。ガラス基板は、高い抵抗率、低い誘電損失、高い熱安定性、調整可能な熱膨張係数を持つため、受動デバイスの製造に使用されることが多くなりました。高周波電気特性、優れた耐熱性、耐薬品性、高い幾何公差を提供するガラス-ビア(TGV)基板を使用することで、ガラスは、電気機械、熱、光学、生物医学、RFデバイスなど、幅広いセンサーやMEMSパッケージング用途向けの汎用性の高い基板となっています。

市場セグメンテーション

集積受動素子の世界市場を詳細に分析した結果、受動デバイス、用途、エンドユーザー別に以下のように区分しました:

- 受動デバイス別では、市場はバラン、フィルター、カプラ、ダイプレクサ、カスタマイズIPDに細分化されます。

- 用途別では、EMI・EMS保護IPD、高周波(RF)IPD、デジタル&ミックスドシグナルIPDに細分化されます。

- エンドユーザー別では、家電、自動車、IT・通信、航空宇宙・防衛、ヘルスケア・ライフサイエンス、その他(エネルギー・ユーティリティ)に細分化されます。

EMI・EMS保護IPDが最大セグメントとなる見通し

集積受動素子の世界市場は、用途別にEMI・EMS保護IPD、RF IPD、デジタル&ミックスドシグナルIPDに細分化されます。このうち、EMI・EMS保護IPDサブセグメントが市場で最大のシェアを占めると予想されます。このセグメントの成長を支える主な要因としては、EMI・EMS保護IPDが提供するカスタマイズ・ソリューションの採用が拡大していることが挙げられます。このソリューションは、デリケートな部品を保護し、ノートパソコン、スマートフォン、自動車用電子機器、産業機械など、さまざまなガジェットで最高のパフォーマンスを保証します。多様な電子用途において、電磁干渉(EMI)シールドと静電気放電(EMS)保護ソリューションの需要が高まっています。電子機器の高密度化・小型化に伴い、干渉を低減し、静電気から保護することが不可欠となっています。エレクトロニクスの開発が進み、信頼性の高いEMI・EMS保護への需要が高まっています。EMS・EMI保護IPDが提供する堅牢な保護対策は、家電、自動車、通信などの分野が進化を続ける中で、依然として高い需要を維持しています。

市場セグメンテーションでは家電が大きなシェアを占める

集積受動素子の世界市場は、用途別に家電、自動車、IT・通信、航空宇宙・防衛、ヘルスケア・ライフサイエンス、その他(エネルギー・ユーティリティ)に細分化されます。このうち、家電のサブセグメントが市場のかなりのシェアを占めると予想されます。数多くの電子機器に対する需要の高まりにより、集積受動部品が利用されています。RFモジュール、ポータブル機器、携帯電話などです。IPDはさまざまな形態があり、設計を簡素化し、必要な接続数を最小限に抑えることで1つの回路にまとめることができます。さらに、チップの小型化などの技術開発により、電子機器の小型化が可能になり、ノートパソコン、LEDテレビ、タブレット、携帯電話などの家電の人気上昇につながっています。

地域別展望

集積受動素子の世界市場は、北米(米国、カナダ)、欧州(英国、イタリア、スペイン、ドイツ、フランス、その他欧州)、アジア太平洋(インド、中国、日本、韓国、その他アジア太平洋)、世界のその他の地域(中東とアフリカ、ラテンアメリカ)など、地域別にさらに細分化されています。

欧州で増加する集積受動素子(IPD)用途

- IPDの統合は、性能とエネルギー効率を提供することで、5G端末機器の数を大幅に改善しました。

- 英国政府(Gov.UK)によると、2023年11月、ワイヤレス接続に関する長期ビジョンが発表され、2030年までにすべての人口密集地域でスタンドアロン5Gを全国カバーするという新たな野望と、全国に5Gイノベーション地域を創設するための4,000万ポンド(4,329万6,000米ドル)の拠出が盛り込まれました。

世界の集積受動素子の地域別市場成長率(2024~2031年)

北米が主要市場シェアを占める

全地域の中で北米が大きなシェアを占めているのは、集積受動素子を提供するプロバイダーが非常に多いためです。主な市場企業には、Texas Instruments Inc.、Silicon Laboratories, Inc.、Intel Corp.、Semiconductor Components Industries, LLC、Analog Devices, Inc.などが含まれます。市場成長の背景には、半導体産業の増加、5G接続の増加によるモノのインターネット(IoT)の普及があります。例えば、Semiconductor Components Industries, LLCは、OnsemiのHigh-Q(TM)Integrated Passive Device(IPD)プロセス技術を提供しており、ポータブル、ワイヤレス、RF用途で使用されるバラン、フィルタ、カプラ、ダイプレクサなどの受動デバイスの製造に理想的な高抵抗シリコン上の銅プラットフォームを提供しています。

世界の集積受動素子市場に参入している主要企業には、アナログ・デバイセズ、村田製作所、NXPセミコンダクターズN.V.、STマイクロエレクトロニクスN.V.、テキサス・インスツルメンツなどがあります。市場競争力を維持するため、各社は提携、合併、買収などの戦略を駆使して事業拡大や製品開拓に力を入れるようになっています。例えば、

- 2023年10月、TDKとLEMは、電化用途向け次世代TMRベース集積受動素子センサーで協業しました。この協業により、TDKのTMR技術は、LEMが特にエネルギー貯蔵、モータードライブ、ソーラーインバータなどの急成長分野で深い専門知識を有する自動車・産業用市場で成功することができるようになります。

- 2023年4月、Cadence Design Systems, Inc.は、集積受動素子の合成と最適化を統合した新しいCadence(R)EMX(R)Designerを発表しました。この技術は、受動素子のデザインルールチェック(DRC)クリーンなパラメトリックセル(PCell)と正確な電磁気(EM)モデルを一瞬で提供します。

- 2023年4月、TDKは、車載、産業、医療、パワーエレクトロニクス、インテリジェントモーション、再生可能エネルギー、エネルギー管理向けの集積受動部品を発表しました。これには、DCリンク用途用の最も多様なコンデンサ技術、インダクタ、保護デバイス、リファレンス設計などが含まれます。

目次

第1章 レポート概要

- 業界の現状分析と成長ポテンシャルの展望

- 調査方法とツール

- 市場内訳

- セグメント別

- 地域別

第2章 市場概要と洞察

- 調査範囲

- アナリストの洞察と現在の市場動向

- 主な調査結果

- 推奨事項

- 結論

第3章 競合情勢

- 主要企業分析

- Analog Devices, Inc.

- 概要

- 財務分析

- SWOT分析

- 最近の動向

- NXP Semiconductors N.V

- 概要

- 財務分析

- SWOT分析

- 最近の動向

- STMicroelectronics N.V

- 概要

- 財務分析

- SWOT分析

- 最近の動向

- 主要戦略分析

第4章 市場セグメンテーション

- 集積受動素子の世界市場:受動素子別

- バラン

- フィルター

- カプラ

- ダイプレクサ

- カスタマイズIPD

- 集積受動素子の世界市場:用途別

- EMI(電磁干渉)・EMS(電磁感受性)保護IPD

- 高周波(RF)IPD

- デジタル&ミックスドシグナルIPD

- 集積受動素子の世界市場:エンドユーザー別

- 家電

- 自動車

- IT・通信

- 航空宇宙・防衛

- ヘルスケア&ライフサイエンス

- その他(エネルギー・ユーティリティ)

第5章 地域分析

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- イタリア

- スペイン

- フランス

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- 世界のその他の地域

第6章 企業プロファイル

- AVX Corp.

- Infineon Technologies AG

- Johanson Technology, Inc.

- KOA Speer Electronics, Inc.

- Mini-Circuits

- Murata Manufacturing Co., Ltd.

- Nordic Semiconductor

- Qorvo, Inc.

- Samsung Electro-Mechanics Co., Ltd.

- Semiconductor Components Industries, LLC

- Silicon Laboratories, Inc.

- Skyworks Solutions, Inc.

- Taiwan Semiconductor Manufacturing Company Ltd.

- TAIYO YUDEN CO., LTD.

- TDK Corp.

- Texas Instruments Inc.

- Wurth Elektronik Group

- Yageo Corp.

LIST OF TABLES

- 1.GLOBAL INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY PASSIVE DEVICES, 2023-2031 ($ MILLION)

- 2.GLOBAL BALUNS INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 3.GLOBAL FILTER INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 4.GLOBAL COUPLERS INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 5.GLOBAL DIPLEXERS INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 6.GLOBAL CUSTOMIZED INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 7.GLOBAL INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY APPLICATION, 2023-2031 ($ MILLION)

- 8.GLOBAL INTEGRATED PASSIVE DEVICES FOR EMI AND EMS PROTECTION MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 9.GLOBAL INTEGRATED PASSIVE DEVICES FOR RADIOFREQUENCY (RF) MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 10.GLOBAL INTEGRATED PASSIVE DEVICES FOR DIGITAL & MIXED-SIGNAL MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 11.GLOBAL INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY END-USERS, 2023-2031 ($ MILLION)

- 12.GLOBAL INTEGRATED PASSIVE DEVICES FOR CONSUMER ELECTRONICS MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 13.GLOBAL INTEGRATED PASSIVE DEVICES FOR AUTOMOTIVE MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 14.GLOBAL INTEGRATED PASSIVE DEVICES FOR IT & TELECOMMUNICATION MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 15.GLOBAL INTEGRATED PASSIVE DEVICES FOR AEROSPACE & DEFENSE MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 16.GLOBAL INTEGRATED PASSIVE DEVICES FOR HEALTHCARE & LIFESCIENCES MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 17.GLOBAL OTHER INTEGRATED PASSIVE DEVICES END-USERS MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 18.GLOBAL INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 19.NORTH AMERICAN INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY COUNTRY, 2023-2031 ($ MILLION)

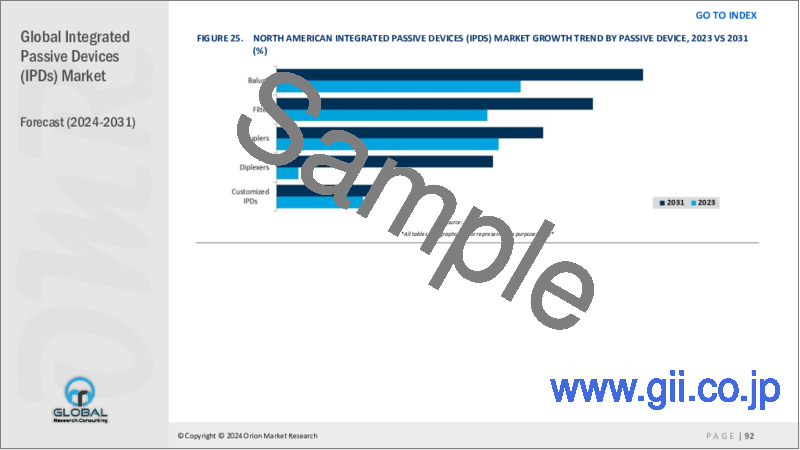

- 20.NORTH AMERICAN INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY PASSIVE DEVICES, 2023-2031 ($ MILLION)

- 21.NORTH AMERICAN INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY APPLICATION, 2023-2031 ($ MILLION)

- 22.NORTH AMERICAN INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY END-USERS, 2023-2031 ($ MILLION)

- 23.EUROPEAN INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY COUNTRY, 2023-2031 ($ MILLION)

- 24.EUROPEAN INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY PASSIVE DEVICES, 2023-2031 ($ MILLION)

- 25.EUROPEAN INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY APPLICATION, 2023-2031 ($ MILLION)

- 26.EUROPEAN INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY END-USERS, 2023-2031 ($ MILLION)

- 27.ASIA-PACIFIC INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY COUNTRY, 2023-2031 ($ MILLION)

- 28.ASIA-PACIFIC INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY PASSIVE DEVICES, 2023-2031 ($ MILLION)

- 29.ASIA-PACIFIC INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY APPLICATION, 2023-2031 ($ MILLION)

- 30.ASIA-PACIFIC INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY END-USERS, 2023-2031 ($ MILLION)

- 31.REST OF THE WORLD INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY REGION, 2023-2031 ($ MILLION)

- 32.REST OF THE WORLD INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY PASSIVE DEVICES, 2023-2031 ($ MILLION)

- 33.REST OF THE WORLD INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY APPLICATION, 2023-2031 ($ MILLION)

- 34.REST OF THE WORLD INTEGRATED PASSIVE DEVICES MARKET RESEARCH AND ANALYSIS BY END-USERS, 2023-2031 ($ MILLION)

LIST OF FIGURES

- 1.GLOBAL INTEGRATED PASSIVE DEVICES MARKET SHARE BY PASSIVE DEVICES, 2023 VS 2031 (%)

- 2.GLOBAL BALUNS INTEGRATED PASSIVE DEVICES MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 3.GLOBAL FILTER INTEGRATED PASSIVE DEVICES MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 4.GLOBAL COUPLERS INTEGRATED PASSIVE DEVICES MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 5.GLOBAL DIPLEXERS INTEGRATED PASSIVE DEVICES MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 6.GLOBAL CUSTOMIZED INTEGRATED PASSIVE DEVICES MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 7.GLOBAL INTEGRATED PASSIVE DEVICES MARKET SHARE BY APPLICATION, 2023 VS 2031 (%)

- 8.GLOBAL INTEGRATED PASSIVE DEVICES FOR EMI AND EMS PROTECTION MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 9.GLOBAL INTEGRATED PASSIVE DEVICES FOR RADIOFREQUENCY MARKET SHARE BY REGION, 2023 VS 2031 (%)

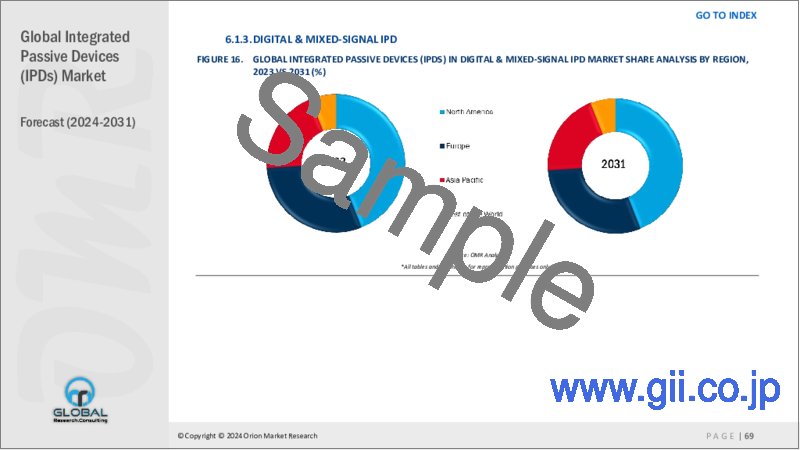

- 10.GLOBAL INTEGRATED PASSIVE DEVICES FOR DIGITAL & MIXED-SIGNAL MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 11.GLOBAL INTEGRATED PASSIVE DEVICES MARKET SHARE BY END-USERS, 2023 VS 2031 (%)

- 12.GLOBAL INTEGRATED PASSIVE DEVICES FOR CONSUMER ELECTRONICS MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 13.GLOBAL INTEGRATED PASSIVE DEVICES FOR AUTOMOTIVE MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 14.GLOBAL INTEGRATED PASSIVE DEVICES FOR IT & TELECOMMUNICATION MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 15.GLOBAL INTEGRATED PASSIVE DEVICES FOR AEROSPACE & DEFENSE MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 16.GLOBAL INTEGRATED PASSIVE DEVICES FOR HEALTHCARE & LIFESCIENCES MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 17.GLOBAL OTHER INTEGRATED PASSIVE DEVICES END-USERS MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 18.GLOBAL INTEGRATED PASSIVE DEVICES MARKET SHARE BY REGION, 2023 VS 2031 (%)

- 19.US INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 20.CANADA INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 21.UK INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 22.FRANCE INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 23.GERMANY INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 24.ITALY INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 25.SPAIN INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 26.REST OF EUROPE INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 27.INDIA INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 28.CHINA INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 29.JAPAN INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 30.SOUTH KOREA INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 31.REST OF ASIA-PACIFIC INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 32.LATIN AMERICA INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

- 33.THE MIDDLE EAST AND AFRICA INTEGRATED PASSIVE DEVICES MARKET SIZE, 2023-2031 ($ MILLION)

Integrated Passive Devices (IPDs) Market Size, Share & Trends Analysis Report by Passive Devices (Baluns, Filter, Couplers, Diplexers, and Customized IPDs), by Application (EMI and EMS protection IPD, RF IPD and Digital & Mixed-Signal IPD) and by End-User (Consumer Electronics, Automotive, IT & Telecommunication, Aerospace & Defense, Healthcare & Lifesciences and Others) Forecast Period (2024-2031)

IPD market is anticipated to grow at a CAGR of 12.6% during the forecast period (2024-2031). The growing adoption of wireless communication technologies with increased demand for integrated passive devices in RF (Radio Frequency) applications, such as mobile devices, IoT devices, and 5G infrastructure drive the growth of the market. IPDs are being increasingly used in consumer electronics such as gaming systems, wireless speakers, routers, set-top boxes, drones, Wearable and hearable technology, smart TVs, and smart appliances.

Market Dynamics

Increasing Adoption of RF Front-End Modules

RF front-end module (FEM) is used to boost RF signals to extend a link's range, strength, and resilience. A high-resistivity substrate is used by the RF-integrated passive device (RF IPD) to integrate quality factor parts including capacitors and indicators. IPD technology can be used to construct a wide range of components, including power combiners/splitters, couplers, harmonic filters, impedance matching networks, and baluns. IPDs offer stand-alone items like filters and baluns in addition to foundry services. Their compatibility with various assembly modalities, such as wire bonding, microbumping, and CSP, allows them to be mounted as a complete RF module or on the main printed wiring board (PWB).

Advancement in IPDs using Through- Glass-Via (TGV) Substrate for High-frequency Applications

The demand for mobile high-speed connections is constantly increasing. IPDs made with glass thin films are growing more favored over those made using through-silicon-via (TSV) substrate. Glass substrate's high resistivity, low dielectric loss, high thermal stability, and tunable coefficient of thermal expansion led to its increasing use in the manufacturing of passive devices. Using Glass-Via (TGV) Substrate that offers high-frequency electrical properties, remarkable heat and chemical resistance, and high geometrical tolerances, glass has become a highly versatile substrate for a wide range of sensor and MEMS packaging applications, including electromechanical, thermal, optical, biomedical, and RF devices.

Market Segmentation

Our in-depth analysis of the global integrated passive devices market includes the following segments by passive devices, applications and end-users:

- Based on passive devices, the market is sub-segmented into baluns, filters, couplers, diplexers and customized IPDs.

- Based on application, the market is sub-segmented into EMI and EMS protection IPD, radiofrequency (RF) IPD and digital & mixed-signal IPD.

- Based on end-user, the market is sub-segmented into consumer electronics, automotive, IT & telecommunication, aerospace & defense, healthcare & life sciences and others (energy and utility).

EMI and EMS protection IPD is Projected to Emerge as the Largest Segment

Based on the application, the global integrated passive devices market is sub-segmented into EMI and EMS protection IPD, RF IPD and digital & mixed-signal IPD. Among these, the EMI and EMS protection IPD sub-segment is expected to hold the largest share of the market. The primary factor supporting the segment's growth includes the growing adoption of customized solutions that are provided by EMS & EMI Protection IPDs, which protect delicate parts and guarantee peak performance in a range of gadgets, such as laptops, smartphones, automobile electronics, and industrial machinery. The increasing demand for electromagnetic interference (EMI) shielding and electrostatic discharge (EMS) protection solutions across diverse electronic applications. It is essential to reduce interference and provide protection against static electricity as electronic equipment gets denser and more compact. The ongoing development of electronics and the growing demand for reliable EMI and EMS protection. Robust protection measures offered by EMS & EMI Protection IPDs remain in high demand as sectors including consumer electronics, automotive, and telecommunications continue to evolve.

Consumer Electronics Sub-segment to Hold a Considerable Market Share

Based on application, the global integrated passive devices market is sub-segmented into consumer electronics, automotive, IT & telecommunication, aerospace & defense, healthcare & life sciences and others (energy and utility). Among these, consumer electronics sub-segment is expected to hold a considerable share of the market. The growing demand for numerous electronic devices makes use of integrated passive components. These consist of RF modules, portable gadgets, and cell phones. IPDs come in a variety of forms and can be combined into a single circuit by simplifying its design and minimizing the number of connections needed. Furthermore, technological developments like smaller chips have made it possible for electronic equipment to get smaller, which has led to a rise in the popularity of consumer electronics like laptops, LED televisions, tablets, and mobile phones.

Regional Outlook

The global Integrated Passive Devices market is further segmented based on geography including North America (the US, and Canada), Europe (UK, Italy, Spain, Germany, France, and the Rest of Europe), Asia-Pacific (India, China, Japan, South Korea, and Rest of Asia), and the Rest of the World (the Middle East & Africa, and Latin America).

An Increasing Integrated Passive Devices (IPD) Application in Europe

- The IPD integration has significantly improved the number of 5G terminal devices by providing performance and energy efficiency.

- According to the Gov.UK, in November 2023, long-term vision for wireless connectivity, including a new ambition for nationwide coverage of standalone 5G in all populated areas by 2030 and £40 million ($43.296 million) to create 5G innovation regions across the country.

Global Integrated Passive Devices Market Growth by Region 2024-2031

Source: OMR Analysis

North America Holds Major Market Share

Among all the regions, North America holds a significant share owing to the presence of an enormous number of providers offering integrated passive devices. The key market players include Texas Instruments Inc., Silicon Laboratories, Inc., Intel Corp., Semiconductor Components Industries, LLC, Analog Devices, Inc., and others. The market growth is attributed to the increase in the semiconductor industry, the Internet of Things (IoT) is widely used with an increase in 5G connectivity. For instance, Semiconductor Components Industries, LLC, offers High-Q(TM) Integrated Passive Device (IPD) process technology from Onsemi offers a copper on high resistivity silicon platform ideal for the production of passive devices such as baluns, filters, couplers, and diplexers that are used in portable, wireless and RF applications.

Market Players Outlook

Note: Major Players Sorted in No Particular Order.

The major companies serving the global integrated passive devices market include Analog Devices, Inc., Murata Manufacturing Co., Ltd., NXP Semiconductors N.V., STMicroelectronics N.V., and Texas Instruments Inc., among others. The market players are increasingly focusing on business expansion and product development by applying strategies such as collaborations, mergers, and acquisitions to stay competitive in the market. For instance,

- In October 2023, TDK and LEM collaborated on next-generation TMR-based integrated passive device sensors for electrification applications. This collaboration further positions TDK's TMR technology to succeed in the automotive and industrial markets, two sectors in which LEM brings deep expertise, especially in booming segments such as energy storage, motor drives, and solar inverters.

- In April 2023, Cadence Design Systems, Inc. introduced a new Cadence(R) EMX(R) Designer, an integrated passive device synthesis and optimization technology that delivers, in split seconds, design rule check (DRC)-clean parametric cells (PCells) and accurate electromagnetic (EM) models of passive devices.

- In April 2023, TDK Corp. introduced integrated passive components for automotive, industrial, and medical applications, power electronics, intelligent motion, renewable energy, and energy management. These include the most diverse capacitor technologies for DC link applications, inductors, protection devices, and reference designs.

The Report Covers:

- Market value data analysis of 2023 and forecast to 2031.

- Annualized market revenues ($ million) for each market segment.

- Country-wise analysis of major geographical regions.

- Key companies operating in the global integrated passive devices (IPD) market. Based on the availability of data, information related to new product launches, and relevant news is also available in the report.

- Analysis of business strategies by identifying the key market segments positioned for strong growth in the future.

- Analysis of market-entry and market expansion strategies.

- Competitive strategies by identifying 'who-stands-where' in the market.

Table of Contents

1.Report Summary

- Current Industry Analysis and Growth Potential Outlook

- 1.1.Research Methods and Tools

- 1.2.Market Breakdown

- 1.2.1.By Segments

- 1.2.2.By Region

2.Market Overview and Insights

- 2.1.Scope of the Report

- 2.2.Analyst Insight & Current Market Trends

- 2.2.1.Key Findings

- 2.2.2.Recommendations

- 2.2.3.Conclusion

3.Competitive Landscape

- 3.1.Key Company Analysis

- 3.2.Analog Devices, Inc.

- 3.2.1.Overview

- 3.2.2.Financial Analysis

- 3.2.3.SWOT Analysis

- 3.2.4.Recent Developments

- 3.3.NXP Semiconductors N.V

- 3.3.1.Overview

- 3.3.2.Financial Analysis

- 3.3.3.SWOT Analysis

- 3.3.4.Recent Developments

- 3.4.STMicroelectronics N.V

- 3.4.1.Overview

- 3.4.2.Financial Analysis

- 3.4.3.SWOT Analysis

- 3.4.4.Recent Developments

- 3.5.Key Strategy Analysis

4.Market Segmentation

- 4.1.Global Integrated Passive Devices Market by Passive Device

- 4.1.1.Baluns

- 4.1.2.Filter

- 4.1.3.Couplers

- 4.1.4.Diplexers

- 4.1.5.Customized IPDs

- 4.2.Global Integrated Passive Devices Market by Application

- 4.2.1.EMI (Electromagnetic Interference) and EMS (Electromagnetic Susceptibility) protection IPD

- 4.2.2.Radiofrequency (RF) IPD

- 4.2.3.Digital & Mixed-Signal IPD

- 4.3.Global Integrated Passive Devices Market by End-Users

- 4.3.1.Consumer Electronics

- 4.3.2.Automotive

- 4.3.3.IT & Telecommunication

- 4.3.4.Aerospace & Defense

- 4.3.5.Healthcare & Lifesciences

- 4.3.6.Others (Energy and Utility)

5.Regional Analysis

- 5.1.North America

- 5.1.1.United States

- 5.1.2.Canada

- 5.2.Europe

- 5.2.1.UK

- 5.2.2.Germany

- 5.2.3.Italy

- 5.2.4.Spain

- 5.2.5.France

- 5.2.6.Rest of Europe

- 5.3.Asia-Pacific

- 5.3.1.China

- 5.3.2.India

- 5.3.3.Japan

- 5.3.4.South Korea

- 5.3.5.Rest of Asia-Pacific

- 5.4.Rest of the World

6.Company Profiles

- 6.1.AVX Corp.

- 6.2.Infineon Technologies AG

- 6.3.Johanson Technology, Inc.

- 6.4.KOA Speer Electronics, Inc.

- 6.5.Mini-Circuits

- 6.6.Murata Manufacturing Co., Ltd.

- 6.7.Nordic Semiconductor

- 6.8.Qorvo, Inc.

- 6.9.Samsung Electro-Mechanics Co., Ltd.

- 6.10.Semiconductor Components Industries, LLC

- 6.11.Silicon Laboratories, Inc.

- 6.12.Skyworks Solutions, Inc.

- 6.13.Taiwan Semiconductor Manufacturing Company Ltd.

- 6.14.TAIYO YUDEN CO., LTD.

- 6.15.TDK Corp.

- 6.16.Texas Instruments Inc.

- 6.17.Wurth Elektronik Group

- 6.18.Yageo Corp.