|

|

市場調査レポート

商品コード

1447078

船舶修理およびメンテナンスサービス市場の2030年までの予測:船舶タイプ、サービス、エンドユーザー、地域別の世界分析Ship Repair and Maintenance Services Market Forecasts to 2030 - Global Analysis By Vessel Type, Service, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 船舶修理およびメンテナンスサービス市場の2030年までの予測:船舶タイプ、サービス、エンドユーザー、地域別の世界分析 |

|

出版日: 2024年03月03日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の船舶修理およびメンテナンスサービス市場は2023年に425億米ドルを占め、予測期間中にCAGR 6.7%で成長し、2030年には669億2,000万米ドルに達する見込みです。

船舶修理およびメンテナンスサービスには、船舶の運航の完全性、安全性、効率性を確保するために必要なさまざまな活動が含まれます。これらのサービスには、検査、溶接、船体洗浄、塗装、機械修理、電気工事、機械のオーバーホールなどが含まれます。彼らの専門知識は、腐食、漏水、構造的損傷への対処、船舶性能と業界規制への準拠を強化するためのアップグレードや改造の実施にまで及んでいます。

ロシア・ブリーフィング・レポートによると、北極海航路の輸送量は、北極海航路全体で2025年までに年間8,000万トンに増加すると予想されています。

海上貿易の増加

海上貿易は世界の商業の基幹を担っており、海上輸送される物品の量が増加するにつれて、それに対応する船舶の修理・整備活動も増加する必要があります。海上貿易に関わる船隊は、コンテナ船、ばら積み貨物船、タンカー、その他の船種で構成されています。さらに、海運業界の競合は、ダウンタイムを最小化し、業務効率を最大化するために、船隊を最適な状態に維持することを船舶運航者に強います。

高い資本コスト

船舶の修理・メンテナンス活動には、インフラ、設備、熟練労働力への多額の投資が必要であり、新規参入企業にとっては大きな障壁となっています。この市場には、船舶の修理・メンテナンスの様々な側面に精通した熟練労働力が必要であり、これがさらにコストを押し上げています。さらに、大型船舶の場合、乾ドックや大規模な修理が必要になることがあり、多額の材料費、人件費、プロジェクト管理のオーバーヘッドがかかるため、市場拡大の妨げになります。

技術の進歩

海事技術の進化に伴い、船舶はますます洗練され、高度なシステムや部品を装備するようになっています。予知保全システムやコンディション・ベース・モニタリングなどの先進技術により、船舶のオペレーターは潜在的な問題を検知できるようになります。さらに、ロボットシステムや自動化された機械が船舶の修理・保守作業に採用されることが増えており、これが市場拡大を後押ししています。

教育の欠如

船舶修理およびメンテナンスサービスに特化した教育・訓練プログラムの不足が、熟練労働者の不足を招いています。教育機関は一般的な海事学に重点を置くことが多く、有資格者の数が限られている特定の技能を軽視しています。しかし、教育の機会や職業開拓プログラムの不足は、市場における熟練労働者の不足をさらに悪化させています。

COVID-19の影響

COVID-19パンデミックは世界の船舶修理およびメンテナンスサービス市場に大きな影響を与え、業界に多くの課題と混乱をもたらしました。港の閉鎖や物流のボトルネックと相まって、世界の商品需要の減少が、修理・メンテナンス・サービスを必要とする船舶数の減少につながっています。この需要減退は、造船所や修理施設の収入減につながった。さらに、ウイルスの蔓延を防ぐための厳格な衛生・安全プロトコルの実施により、修理業務に追加コストと複雑さが加わり、この市場の足かせとなっています。

予測期間中、コンテナ船セグメントが最大となる見込み

コンテナ船セグメントは、標準化されたコンテナで商品を輸送する世界貿易に不可欠なコンテナ船特有の保守・修理ニーズにより、最大のシェアを占めると推定されます。サービスには、腐食や構造的完全性の問題に対処するための船体の洗浄、検査、修理が含まれます。さらに、コンテナ船は貨物容量、燃料効率、環境性能を最適化するために改造やアップグレードを行うことが多く、これがこのセグメントの拡大を後押ししています。

補助サービス分野は予測期間中に最も高いCAGRが見込まれる

補助サービス分野は、主要機能以外にも、船舶の全体的な運用準備、安全性、コンプライアンスを確保するために不可欠な幅広い専門的支援活動により、予測期間中のCAGRが最も高くなると予想されます。補助サービスには、ケータリング施設、居住区、レクリエーションエリアなどの船内設備の維持管理が含まれます。さらに、これらのサービスには、乗組員の福利厚生と快適性を確保するための船内設備の維持管理も含まれるため、このセグメントの成長を牽引しています。

最大のシェアを占める地域

北米は、海事産業においてダイナミックで不可欠なセクターであり、この地域で運航されている商業船舶、海軍船舶、オフショア構造物の膨大な船隊にサービスを提供しているため、予測期間中に最大の市場シェアを獲得しました。この産業は、米国、カナダ、メキシコの沿岸に加え、内陸の水路や港まで、多種多様な船舶にサービスを提供しています。さらに、この地域は主要航路や港に近いことから、信頼性が高く高品質の修理サービスを求める船舶運航業者にとって戦略的な選択肢となっており、この地域の成長を後押ししています。

CAGRが最も高い地域:

予測期間中、欧州のCAGRが最も高くなると予想されます。欧州の船舶修理およびメンテナンスサービス市場は、卓越した職人技と厳格な安全・環境規制の遵守を特徴としています。この地域には、BAE Systems plc、Damen Shipyards Group、Keppel Corporation Limitedといった大手企業があります。さらに、この地域は熟練した労働力、最先端のインフラ、強力な協力関係から恩恵を受けており、これがこの地域の規模を押し上げています。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレーヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- エンドユーザー分析

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の船舶修理およびメンテナンスサービス市場:船舶タイプ別

- コンテナ船

- 物流コンテナ船

- 旅客船

- オフショア船

- タンカー船

- 石油タンカー運搬船

- ばら積み貨物船

- 海軍艦艇

- 特殊用途船

- その他の容器タイプ

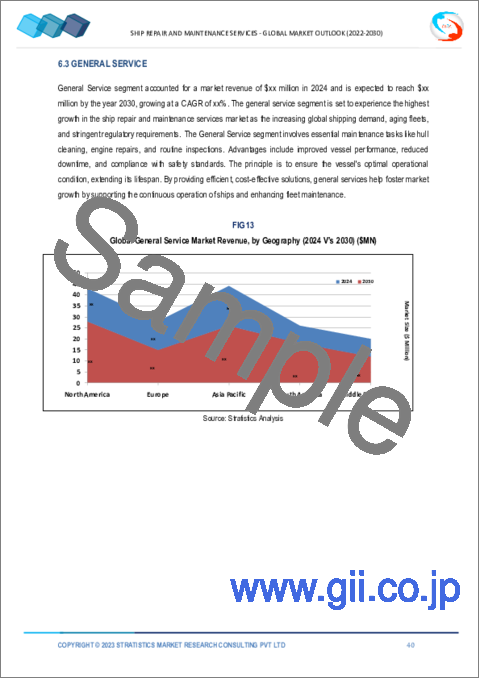

第6章 世界の船舶修理およびメンテナンスサービス市場:サービス別

- エンジン部品

- 一般的なサービス

- ドックアップ

- ドライドックサービス

- ウェットドックサービス

- 電気工事

- 船体部分

- 補助サービス

- 他のサービス

第7章 世界の船舶修理およびメンテナンスサービス市場:エンドユーザー別

- 配送会社

- 海洋産業

- 海軍

- クルーズおよびレジャー産業

- 政府機関

- 海上物流

- その他のエンドユーザー

第8章 世界の船舶修理およびメンテナンスサービス市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第9章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第10章 企業プロファイル

- BAE Systems

- Garden Reach Shipbuilders and Engineers Limited

- General Dynamics NASSCO

- Sembcorp Marine Ltd

- Damen Shipyards Group

- Larsen & Toubro Ltd

- Dundee Marine & Industrial Services Pte Ltd.

- HD Hyundai Heavy Industries Co., Ltd

- ST Engineering

- Varren Marines Shipping Pvt. Ltd.

- United Shipbuilding Corporation

- Desan Shipyard

- Hyundai Mipo Dockyard

- Cosco Shipyard Group Co.,Ltd

- Allied Shipbuilders Ltd

List of Tables

- Table 1 Global Ship Repair and Maintenance Services Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Ship Repair and Maintenance Services Market Outlook, By Vessel Type (2021-2030) ($MN)

- Table 3 Global Ship Repair and Maintenance Services Market Outlook, By Container Ships (2021-2030) ($MN)

- Table 4 Global Ship Repair and Maintenance Services Market Outlook, By Logistics Container Carriers (2021-2030) ($MN)

- Table 5 Global Ship Repair and Maintenance Services Market Outlook, By Passenger Ships (2021-2030) ($MN)

- Table 6 Global Ship Repair and Maintenance Services Market Outlook, By Offshore Ships (2021-2030) ($MN)

- Table 7 Global Ship Repair and Maintenance Services Market Outlook, By Tanker Ships (2021-2030) ($MN)

- Table 8 Global Ship Repair and Maintenance Services Market Outlook, By Oil Tanker Carriers (2021-2030) ($MN)

- Table 9 Global Ship Repair and Maintenance Services Market Outlook, By Bulk Carriers (2021-2030) ($MN)

- Table 10 Global Ship Repair and Maintenance Services Market Outlook, By Naval Ships (2021-2030) ($MN)

- Table 11 Global Ship Repair and Maintenance Services Market Outlook, By Special Purpose Ships (2021-2030) ($MN)

- Table 12 Global Ship Repair and Maintenance Services Market Outlook, By Other Vessel Types (2021-2030) ($MN)

- Table 13 Global Ship Repair and Maintenance Services Market Outlook, By Service (2021-2030) ($MN)

- Table 14 Global Ship Repair and Maintenance Services Market Outlook, By Engine Parts (2021-2030) ($MN)

- Table 15 Global Ship Repair and Maintenance Services Market Outlook, By General Service (2021-2030) ($MN)

- Table 16 Global Ship Repair and Maintenance Services Market Outlook, By Dockage (2021-2030) ($MN)

- Table 17 Global Ship Repair and Maintenance Services Market Outlook, By Dry Dock Services (2021-2030) ($MN)

- Table 18 Global Ship Repair and Maintenance Services Market Outlook, By Wet Dock Services (2021-2030) ($MN)

- Table 19 Global Ship Repair and Maintenance Services Market Outlook, By Electric Works (2021-2030) ($MN)

- Table 20 Global Ship Repair and Maintenance Services Market Outlook, By Hull Part (2021-2030) ($MN)

- Table 21 Global Ship Repair and Maintenance Services Market Outlook, By Auxiliary services (2021-2030) ($MN)

- Table 22 Global Ship Repair and Maintenance Services Market Outlook, By Other Services (2021-2030) ($MN)

- Table 23 Global Ship Repair and Maintenance Services Market Outlook, By End User (2021-2030) ($MN)

- Table 24 Global Ship Repair and Maintenance Services Market Outlook, By Shipping Companies (2021-2030) ($MN)

- Table 25 Global Ship Repair and Maintenance Services Market Outlook, By Offshore Industry (2021-2030) ($MN)

- Table 26 Global Ship Repair and Maintenance Services Market Outlook, By Naval Forces (2021-2030) ($MN)

- Table 27 Global Ship Repair and Maintenance Services Market Outlook, By Cruise and Leisure Industry (2021-2030) ($MN)

- Table 28 Global Ship Repair and Maintenance Services Market Outlook, By Government Agencies (2021-2030) ($MN)

- Table 29 Global Ship Repair and Maintenance Services Market Outlook, By Maritime Logistics (2021-2030) ($MN)

- Table 30 Global Ship Repair and Maintenance Services Market Outlook, By Other End Users (2021-2030) ($MN)

Table Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Ship Repair and Maintenance Services Market is accounted for $42.5 billion in 2023 and is expected to reach $66.92 billion by 2030 growing at a CAGR of 6.7% during the forecast period. Ship repair and maintenance services encompass the range of activities required to ensure the operational integrity, safety, and efficiency of maritime vessels. These services include inspections, welding, hull cleaning, painting, mechanical repairs, electrical work, and machinery overhauls. Their expertise extends to addressing corrosion, leaks, and structural damage, as well as implementing upgrades and modifications to enhance vessel performance and compliance with industry regulations.

According to Russia Briefing Report, traffic on the Northern Sea Route is expected to rise to 80 million tons of shipments per year by 2025 across Arctic shipping.

Market Dynamics:

Driver:

Increasing maritime trade

Maritime trade serves as the backbone of global commerce, and the rising volume of goods being transported by sea necessitates a corresponding increase in ship repair and maintenance activities. The expanding fleet involved in maritime trade comprises container ships, bulk carriers, tankers, and other vessel types. Moreover, the competitive nature of the shipping industry compels vessel operators to maintain their fleets in optimal condition to minimize downtime and maximize operational efficiency, which is driving this market growth.

Restraint:

High capital costs

Ship repair and maintenance activities require substantial investments in infrastructure, equipment, and skilled labor, making a significant barrier to entry for new players in the market. The market demands a skilled workforce with expertise in various aspects of ship repair and maintenance, further adding to the costs. Furthermore, large vessels may require dry docking or extensive repairs that involve significant material costs, labor expenses, and project management overheads, which thereby impede this market expansion.

Opportunity:

Technological advancements

As maritime technology evolves, vessels become increasingly sophisticated and equipped with advanced systems and components. Advanced technologies, such as predictive maintenance systems and condition-based monitoring, enable ship operators to detect potential issues. Furthermore, robotic systems and automated machinery are increasingly being employed in ship repair and maintenance operation, which propels this market expansion.

Threat:

Lack of education

The lack of education and training programs tailored specifically for ship repair and maintenance services contributes to the scarcity of skilled workers. Educational institutions often focus more on general maritime studies, neglecting specific skills that have a limited pool of qualified individuals. However, the lack of educational opportunities and professional development programs further exacerbates the shortage of skilled workers in the market.

Covid-19 Impact

The COVID-19 pandemic has significantly impacted the ship repair and maintenance services market worldwide, presenting numerous challenges and disruptions to the industry. Reduced global demand for goods, coupled with port closures and logistical bottlenecks, has led to a decrease in the number of vessels requiring repair and maintenance services. This decline in demand has resulted in decreased revenue for shipyards and repair facilities. Moreover, the implementation of strict health and safety protocols to prevent the spread of the virus has added additional costs and complexities to repair operations, which have hampered this market.

The container ships segment is expected to be the largest during the forecast period

The container ships segment is estimated to hold the largest share, due to the maintenance and repair needs specific to container vessels, which are essential for global trade, transporting goods in standardized containers. Services include hull cleaning, inspection, and repair to address corrosion and structural integrity issues. Furthermore, container ships often undergo modifications and upgrades to optimize cargo capacity, fuel efficiency, and environmental performance which are boosting this segment's expansion.

The auxiliary services segment is expected to have the highest CAGR during the forecast period

The auxiliary services segment is anticipated to have highest CAGR during the forecast period due to a broad array of specialized support activities vital for ensuring the overall operational readiness, safety, and compliance of maritime vessels beyond their primary functions. Auxiliary services encompass the upkeep of onboard amenities such as catering facilities, living quarters, and recreational areas. In addition, these services encompass the upkeep of onboard amenities to ensure the well-being and comfort of crew members, thereby driving this segment's growth.

Region with largest share:

North America commanded the largest market share during the extrapolated period owing to a dynamic and essential sector within the maritime industry, serving the vast fleet of commercial vessels, naval ships, and offshore structures operating in the region. This industry serves a wide variety of vessels, covering the coasts of the United States, Canada, and Mexico, in addition to inland waterways and ports. Moreover, the region's proximity to major shipping routes and ports also positions it as a strategic choice for vessel operators seeking reliable and high-quality repair services, which is propelling this region's growth.

Region with highest CAGR:

Europe is expected to witness highest CAGR over the projection period. In Europe, the ship repair and maintenance services market is characterized by a commitment to excellence in craftsmanship and adherence to rigorous safety and environmental regulations. This region is home to some of the major players, such as BAE Systems plc, Damen Shipyards Group, and Keppel Corporation Limited. Moreover, this region benefits from a skilled workforce, state-of-the-art infrastructure, and strong collaboration, which boosts this region's size.

Key players in the market

Some of the key players in the Ship Repair and Maintenance Services Market include BAE Systems, Garden Reach Shipbuilders and Engineers Limited, General Dynamics NASSCO, Sembcorp Marine Ltd, Damen Shipyards Group, Larsen & Toubro Ltd, Dundee Marine & Industrial Services Pte Ltd., HD Hyundai Heavy Industries Co., Ltd, ST Engineering, Varren Marines Shipping Pvt. Ltd., United Shipbuilding Corporation, Desan Shipyard, Hyundai Mipo Dockyard, Cosco Shipyard Group Co.,Ltd and Allied Shipbuilders Ltd.

Key Developments:

In February 2024, BAE Systems and the University of Portsmouth have launched the UK's first ever degree apprenticeship in Space Systems Engineering.

In October 2023, BAE Systems acquires Eurostep to deliver advanced digital asset management. BAE Systems has acquired Eurostep, a secure data sharing company headquartered in Sweden. The company will form part of BAE Systems' Digital Intelligence business.

In September 2023, Chinese shipyard group COSCO Shipping Heavy Industry Co. Ltd (CHI) has signed a memorandum of understanding with Silverstream to explore the possibility of licensing the installation of the Silverstream air lubrication system in CHI's shipyards.

Vessel Types Covered:

- Container Ships

- Passenger Ships

- Offshore Ships

- Tanker Ships

- Bulk Carriers

- Naval Ships

- Special Purpose Ships

- Other Vessel Types

Services Covered:

- Engine Parts

- General Service

- Dockage

- Electric Works

- Hull Part

- Auxiliary services

- Other Services

End Users Covered:

- Shipping Companies

- Offshore Industry

- Naval Forces

- Cruise and Leisure Industry

- Government Agencies

- Maritime Logistics

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 End User Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Ship Repair and Maintenance Services Market, By Vessel Type

- 5.1 Introduction

- 5.2 Container Ships

- 5.2.1 Logistics Container Carriers

- 5.3 Passenger Ships

- 5.4 Offshore Ships

- 5.5 Tanker Ships

- 5.5.1 Oil Tanker Carriers

- 5.6 Bulk Carriers

- 5.7 Naval Ships

- 5.8 Special Purpose Ships

- 5.9 Other Vessel Types

6 Global Ship Repair and Maintenance Services Market, By Service

- 6.1 Introduction

- 6.2 Engine Parts

- 6.3 General Service

- 6.4 Dockage

- 6.4.1 Dry Dock Services

- 6.4.2 Wet Dock Services

- 6.5 Electric Works

- 6.6 Hull Part

- 6.7 Auxiliary services

- 6.8 Other Services

7 Global Ship Repair and Maintenance Services Market, By End User

- 7.1 Introduction

- 7.2 Shipping Companies

- 7.3 Offshore Industry

- 7.4 Naval Forces

- 7.5 Cruise and Leisure Industry

- 7.6 Government Agencies

- 7.7 Maritime Logistics

- 7.8 Other End Users

8 Global Ship Repair and Maintenance Services Market, By Geography

- 8.1 Introduction

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Italy

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 New Zealand

- 8.4.6 South Korea

- 8.4.7 Rest of Asia Pacific

- 8.5 South America

- 8.5.1 Argentina

- 8.5.2 Brazil

- 8.5.3 Chile

- 8.5.4 Rest of South America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 Qatar

- 8.6.4 South Africa

- 8.6.5 Rest of Middle East & Africa

9 Key Developments

- 9.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 9.2 Acquisitions & Mergers

- 9.3 New Product Launch

- 9.4 Expansions

- 9.5 Other Key Strategies

10 Company Profiling

- 10.1 BAE Systems

- 10.2 Garden Reach Shipbuilders and Engineers Limited

- 10.3 General Dynamics NASSCO

- 10.4 Sembcorp Marine Ltd

- 10.5 Damen Shipyards Group

- 10.6 Larsen & Toubro Ltd

- 10.7 Dundee Marine & Industrial Services Pte Ltd.

- 10.8 HD Hyundai Heavy Industries Co., Ltd

- 10.9 ST Engineering

- 10.10 Varren Marines Shipping Pvt. Ltd.

- 10.11 United Shipbuilding Corporation

- 10.12 Desan Shipyard

- 10.13 Hyundai Mipo Dockyard

- 10.14 Cosco Shipyard Group Co.,Ltd

- 10.15 Allied Shipbuilders Ltd