|

|

市場調査レポート

商品コード

1371938

点滴液市場の2030年までの予測: タイプ別、組成別、溶液タイプ別、バッグタイプ別、用途別、エンドユーザー別、地域別の世界分析Intravenous Solutions Market Forecasts to 2030 - Global Analysis By Type, Composition, Solution Type, Bag Type, Application, End User and By Geography |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 点滴液市場の2030年までの予測: タイプ別、組成別、溶液タイプ別、バッグタイプ別、用途別、エンドユーザー別、地域別の世界分析 |

|

出版日: 2023年10月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、静脈内ソリューションの世界市場は2023年に130億9,000万米ドルを占め、予測期間中にCAGR 10.0%で成長し、2030年には255億米ドルに達すると予測されています。

輸液とも呼ばれる静脈注射液は、無菌の液体治療薬で、静脈ラインを使って患者の静脈に注入されます。静脈注射液は、特に経口摂取が不十分な場合や迅速な吸収が必要な場合に、患者の水分と電解質のバランスを回復・維持するために使用されます。必要な水分や薬液を血流に直接供給することで、病院から外来患者まで、さまざまな臨床現場で効率的な治療と患者サポートを保証しています。

米国非経口・経腸栄養学会(ASPEN)のガイドラインによると、2020年には、早期胃経腸栄養が不可能なハイリスク患者には、できるだけ早期に非経口栄養を開始すべきであるとしています。

輸液の新展開

安定性、溶解性、および生物学的利用能が改善された特殊な製剤が開発されています。さらに、最新の成分技術により、複雑な薬物や栄養素など、より多様な治療薬を輸送できる静脈内溶液の作成が可能になっています。こうした発展の結果、治療効果の向上により、より幅広い医療疾患の治療が可能となり、市場の裾野が広がっています。そのため、静脈注射液市場は、より高度で専門的なソリューションを提供できるようになることで恩恵を受け、患者ケアと治療成績が向上し、市場の成長を大きく後押ししています。

高コスト

点滴製剤は、特に複雑な成分や専門的な製剤を使用する場合、価格が高くなる可能性があります。さらに、製造、包装、品質管理の価格が輸液の総コストに影響することもあります。そのため、特に資源が限られている地域やヘルスケアのインフラが貧弱な地域では、このような価格設定が市場参入を制限する可能性があります。

意識の高まり

人々の健康志向の高まりに伴い、予防的かつホリスティックなヘルスケア手法の需要が高まっています。静脈注射液は、医療だけでなく、健康や活力のためにも需要があります。水分補給、免疫学的サポート、栄養補給などに頻繁に使用されています。さらに、オーダーメイドの点滴療法は、欠乏症を減らし、エネルギーを高め、健康全般を改善する方法として、ますます人気が高まっています。さらに、クリニックやプロバイダーは、健康志向の高い世代のウェルネスやパフォーマンスの目的に合った点滴ソリューションを提供しており、これが市場規模を押し上げています。

標準化と品質の欠如

患者の安全にとって不可欠な製品の性能と品質の一貫性は、さまざまな品質・安全基準によって阻害される可能性があります。さらに、地域間で統一された規制がないため、製造慣行や製品ラベリングにばらつきが生じ、医療従事者が点滴液の信頼性を確保することが課題となります。したがって、このような標準化と規制監督の欠如は、市場におけるリスクと複雑さを増大させる結果となり、これらの重要な医療製品の安全性と有効性を確保するための包括的で世界的に認められたガイドラインの必要性を強調しています。

COVID-19の影響

点滴液市場はCOVID-19の流行によって大きな悪影響を受けた。ヘルスケア施設は稀に見る資源の逼迫に見舞われ、しばしば過重な負担を強いられました。その結果、これらの重要な医療用輸液の所在を確認し、調剤する際の不足と物流上の困難が生じた。さらに、ヘルスケア産業への投資は、経済破綻と不確実性によって妨げられました。そのため、需要の増加にもかかわらず、パンデミックは静脈注射液市場に物流面および財政面での課題をもたらし、入手しやすさと供給の両方に悪影響を及ぼしました。

予測期間中、デキストラン・セグメントが最大となる見込み

デキストラン分野は、ヘルスケア施設において、主に手術やその他の医療処置の際に血流を促進し、血栓形成の可能性を低下させるために使用されるため、最大のシェアを占めると推定されます。さらに、デキストランをベースとしたこれらの静脈注射液は、血漿拡張剤として機能し、血液循環を促進し、血圧維持を補助します。これらは、患者が出血を経験したり、血行動態のサポートを必要としたりする状況において極めて重要です。このように、デキストランをベースとする静脈注射液は、医療活動中の患者の健康を維持するために不可欠であるため、ヘルスケア分野におけるより大きな静脈注射液市場にとって不可欠な要素となっています。

大容量バッグ分野は予測期間中に最も高いCAGRが見込まれる

大容量バッグセグメントは、予測期間中にCAGRが最も高くなると予測されています。ヘルスケアでは、栄養供給、薬物投与、水分補給など様々な用途があり、これらのバッグは不可欠です。さらに、病院、診療所、その他の医療施設では、患者に効果的かつ制御された静脈内治療を提供するために大容量バッグが頻繁に利用されています。大容量バッグは、さまざまな種類の輸液を柔軟に受け入れることができ、長時間の治療を必要とする患者にとって特に重要であるため、ヘルスケア産業における点滴ソリューション市場の屋台骨となっています。

最大のシェアを占める地域

欧州は、医療システムの膨大な患者数、重要なプレイヤーの台頭、薬剤の入手しやすさ、医療システムの高度化、有利な償還慣行により、予測期間中に最大の市場シェアを獲得しました。さらに、欧州の静脈注射液市場は、国民保健サービスや健康保険に対する政府の支援、業界の技術進歩の結果、おそらく発展すると思われます。さらに、英国の静脈注射液市場が最も高い市場シェアを占め、フランスの静脈注射液市場は欧州大陸で最も急速に拡大しました。

CAGRが最も高い地域:

アジア太平洋地域は、急速な成長により、予測期間中に最も高いCAGRを記録することが予想されます。これは、官民双方による研究への高額投資、技術開発、ヘルスケア産業、大学などのさまざまな利害関係者間の協力関係の増加に起因しています。したがって、不健康な食品消費パターンによってもたらされる慢性疾患の有病率の上昇と、費用対効果の高いケアに対する選択の増加は、アジア太平洋地域における市場成長を促進すると予測される2つの重要な要因です。

無料のカスタマイズ提供:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- アプリケーション分析

- エンドユーザー分析

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の点滴ソリューション市場:タイプ別

- 完全非経口栄養学

- 部分非経口栄養法

第6章 世界の点滴薬市場:構成別

- 炭水化物

- ビタミンとミネラル

- 非経口脂質エマルジョン

- 単回投与アミノ酸

- その他の構成

第7章 世界の点滴ソリューション市場:ソリューションタイプ別

- デキストラン

- 生理食塩水

- 高張食塩水

- アミノ酸

- 生理食塩水

- 乳酸リンゲル液

- ヘパリンと微量元素

- ビタミンとミネラル

- 混合ソリューション

第8章 世界の点滴薬市場:バッグの種類別

- 大容量バッグ

- 小容量バッグ

第9章 世界の点滴ソリューション市場:アプリケーション別

- 栄養点滴液

- 輸血液

- 基本的なIVソリューション

- 灌漑IVソリューション

- 薬物点滴液

第10章 世界の点滴ソリューション市場:エンドユーザー別

- クリニック

- 病院

- 外来手術センター

- ホームケア設定

第11章 世界の点滴ソリューション市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第12章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第13章 企業プロファイル

- ICU Medical, Inc.

- B. Braun Melsungen Ag

- JW Life Science

- Baxter International Inc.

- Fresenius Kabi USA, LLC

- Vifor Pharma Management Ltd

- Amanta Healthcare

- Grifols, S.A

- Salius Pharma Private Limited.

- Pfizer, Inc.

- Axa Parenterals Ltd

- Ajinomoto Co., Inc.

- Otsuka Pharmaceutical Co., Ltd

- Sichuan Kelun Pharmaceutical Co Ltd

- Soxa Formulations & Research Pvt. Ltd

- Braun Melsungen AG

List of Tables

- Table 1 Global Intravenous Solutions Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Intravenous Solutions Market Outlook, By Type (2021-2030) ($MN)

- Table 3 Global Intravenous Solutions Market Outlook, By Total Parenteral Nutrition (2021-2030) ($MN)

- Table 4 Global Intravenous Solutions Market Outlook, By Partial Parenteral Nutrition (2021-2030) ($MN)

- Table 5 Global Intravenous Solutions Market Outlook, By Composition (2021-2030) ($MN)

- Table 6 Global Intravenous Solutions Market Outlook, By Carbohydrates (2021-2030) ($MN)

- Table 7 Global Intravenous Solutions Market Outlook, By Vitamins And Minerals (2021-2030) ($MN)

- Table 8 Global Intravenous Solutions Market Outlook, By Parenteral Lipid Emulsion (2021-2030) ($MN)

- Table 9 Global Intravenous Solutions Market Outlook, By Single Dose Amino Acids (2021-2030) ($MN)

- Table 10 Global Intravenous Solutions Market Outlook, By Other Compositions (2021-2030) ($MN)

- Table 11 Global Intravenous Solutions Market Outlook, By Solution Type (2021-2030) ($MN)

- Table 12 Global Intravenous Solutions Market Outlook, By Dextran (2021-2030) ($MN)

- Table 13 Global Intravenous Solutions Market Outlook, By Saline (2021-2030) ($MN)

- Table 14 Global Intravenous Solutions Market Outlook, By Hypertonic Saline (2021-2030) ($MN)

- Table 15 Global Intravenous Solutions Market Outlook, By Amino Acid (2021-2030) ($MN)

- Table 16 Global Intravenous Solutions Market Outlook, By Normal Saline (2021-2030) ($MN)

- Table 17 Global Intravenous Solutions Market Outlook, By Lactated Ringer's (2021-2030) ($MN)

- Table 18 Global Intravenous Solutions Market Outlook, By Heparin And Trace Elements (2021-2030) ($MN)

- Table 19 Global Intravenous Solutions Market Outlook, By Vitamins & Minerals (2021-2030) ($MN)

- Table 20 Global Intravenous Solutions Market Outlook, By Mixed Solutions (2021-2030) ($MN)

- Table 21 Global Intravenous Solutions Market Outlook, By Bag Type (2021-2030) ($MN)

- Table 22 Global Intravenous Solutions Market Outlook, By Large Volume Bags (2021-2030) ($MN)

- Table 23 Global Intravenous Solutions Market Outlook, By Small Volume Bags (2021-2030) ($MN)

- Table 24 Global Intravenous Solutions Market Outlook, By Application (2021-2030) ($MN)

- Table 25 Global Intravenous Solutions Market Outlook, By Nutritional IV Solution (2021-2030) ($MN)

- Table 26 Global Intravenous Solutions Market Outlook, By Blood IV Solution (2021-2030) ($MN)

- Table 27 Global Intravenous Solutions Market Outlook, By Basic IV Solution (2021-2030) ($MN)

- Table 28 Global Intravenous Solutions Market Outlook, By Irrigation IV Solution (2021-2030) ($MN)

- Table 29 Global Intravenous Solutions Market Outlook, By Drug IV Solution (2021-2030) ($MN)

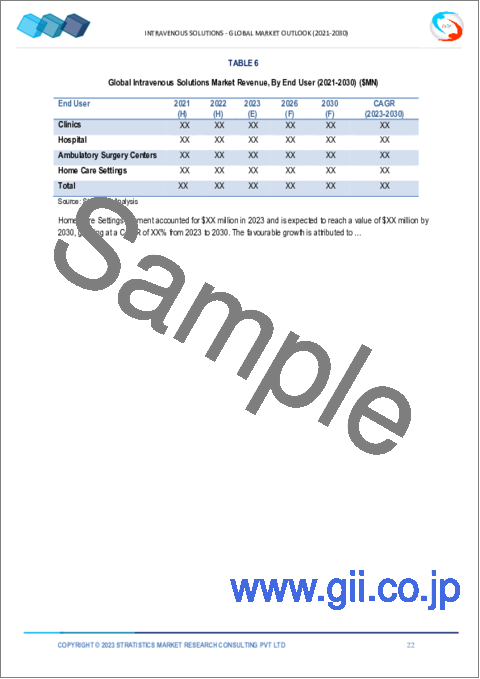

- Table 30 Global Intravenous Solutions Market Outlook, By End User (2021-2030) ($MN)

- Table 31 Global Intravenous Solutions Market Outlook, By Clinics (2021-2030) ($MN)

- Table 32 Global Intravenous Solutions Market Outlook, By Hospital (2021-2030) ($MN)

- Table 33 Global Intravenous Solutions Market Outlook, By Ambulatory Surgery Centers (2021-2030) ($MN)

- Table 34 Global Intravenous Solutions Market Outlook, By Home Care Settings (2021-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Intravenous Solutions Market is accounted for $13.09 billion in 2023 and is expected to reach $25.5 billion by 2030 growing at a CAGR of 10.0 % during the forecast period. Intravenous solutions, also called IV solutions, are sterile liquid treatments that are injected into a patient's veins by means of an intravenous line. These treatments are used for a variety of essential medical functions, such as rehydration, medicine delivery, and nutritional support, IV solutions are used to restore and maintain a patient's fluid and electrolyte balance, particularly when oral intake is insufficient or rapid absorption is required. They are composed of a precisely balanced blend of water, nutrients, and sometimes drugs and are a crucial part of contemporary healthcare, guaranteeing efficient treatment and patient support in a range of clinical settings, from hospitals to outpatient care, by supplying necessary fluids and medicinal chemicals straight into the bloodstream.

According to the guidelines by American Society for Parenteral and Enteral Nutrition (ASPEN), in 2020, the early parenteral nutrition should be initiated as soon as possible in the high-risk patient for whom early gastric enteral nutrition is not feasible.

Market Dynamics:

Driver:

New developments in IV solutions

As the developments involve the creation of specialized formulations with improved stability, solubility, and bioavailability. Additionally, modern ingredient technology makes it possible to create intravenous solutions that can transport a wider variety of therapeutic agents, such as complicated drugs and nutrients. As a result of these developments, it is now possible to treat a wider range of medical diseases by improving treatment efficacy and broadening the market's capacities. Therefore, the market for intravenous solutions benefits from being able to provide more sophisticated and specialized solutions, which enhance patient care and treatment outcomes and thus significantly drives the market growth.

Restraint:

High cost

IV solutions can be pricey, especially when made with complicated ingredients or in specialist formulations. Moreover, the price of manufacturing, packaging, and quality control can affect the overall cost of IV solutions. Hence, this pricing aspect may restrict market access, particularly in areas with limited resources or poor healthcare infrastructure.

Opportunity:

Increase in awareness

Preventive and holistic healthcare methods are in greater demand as people grow more health-conscious. Intravenous solutions are in demand not just for medical treatment but also for wellness and vitality reasons. They are frequently used for rehydration, immunological support, and nutrient supplementation. Furthermore, customized IV therapy is becoming more and more popular as a way to reduce deficiencies, increase energy, and improve general wellbeing. Moreover, clinics and providers offer intravenous solutions that meet the wellness and performance objectives of a health-conscious generation, which thus propel the market size.

Threat:

Lack of standardization and quality

The consistency of product performance and quality, which is essential for patient safety, might be hampered by varying quality and safety standards. Moreover, the absence of unified regulations across regions can lead to disparities in manufacturing practices and product labeling, making it challenging for healthcare providers to ensure the reliability of intravenous solutions. Therefore, this lack of standardization and regulatory oversight can result in increased risks and complexities in the market, emphasizing the need for comprehensive, globally recognized guidelines to ensure the safety and efficacy of these critical medical products.

COVID-19 Impact

The market for intravenous solutions was significantly negatively impacted by the COVID-19 epidemic. Healthcare facilities experienced rare resource pressures and were frequently overburdened, which resulted in shortages and logistical difficulties when locating and dispensing these vital medical fluids. Additionally, investments in the healthcare industry were impeded by the economic collapse and uncertainties. Therefore, despite rising demand, the pandemic posed logistical and financial challenges for the market for intravenous solutions, adversely impacting both accessibility and supply.

The Dextran segment is expected to be the largest during the forecast period

The Dextran segment is estimated to hold the largest share, as these treatments are used in healthcare facilities to boost blood flow and lower the chance of clot formation, primarily during operations and other medical procedures. Additionally, these IV solutions based on dextran, function as plasma expanders, enhancing circulation and assisting in blood pressure maintenance. They are crucial in circumstances where patients can experience bleeding or need hemodynamic support. Thus, intravenous solutions based on dextran are an essential part of the larger intravenous solutions market in the healthcare sector since they are essential in sustaining patient wellbeing during medical operations.

The large volume bags segment is expected to have the highest CAGR during the forecast period

The large volume bags segment is anticipated to have highest CAGR during the forecast period, due to a variety of uses in healthcare, such as nutrient delivery, medicine administration, and hydration, these bags are essential. Moreover, in hospitals, clinics, and other medical facilities, large-volume bags are frequently utilized to deliver effective and controlled intravenous therapy to patients. Hence, they are a backbone of the intravenous solutions market in the healthcare industry because they are flexible in accepting different types of solutions and are especially important for patients needing prolonged treatments.

Region with largest share:

Europe commanded the largest market share during the extrapolated period owing to the healthcare system's enormous patient population, the prominence of important players, the accessibility of drugs, the sophistication of the healthcare systems, and the advantageous reimbursement practices. Furthermore, the market for intravenous (IV) solutions in Europe will probably develop as a result of government support for the National Health Service and health insurance as well as industry technological advancements. Additionally, the intravenous solution market in the United Kingdom had the highest market share, while the intravenous solution market in France had the quickest rate of expansion in the continent of Europe.

Region with highest CAGR:

Asia Pacific is expected to witness highest CAGR over the projection period, owing to rapid growth, which can be attributed to the high investment made in research by both public and private entities, as well as technological developments and an increase in the number of cooperative relationships between different stakeholders, including the healthcare industry, universities, and others. Therefore, the rising prevalence of chronic diseases brought on by unhealthy food consumption patterns and the growing choice for cost-effective care are two significant factors that are projected to propel market growth in the Asia Pacific region.

Key players in the market:

Some of the key players in the Intravenous Solutions Market include: ICU Medical, Inc., B. Braun Melsungen Ag, JW Life Science, Baxter International Inc., Fresenius Kabi USA, LLC, Vifor Pharma Management Ltd, Amanta Healthcare, Grifols, S.A, Salius Pharma Private Limited., Pfizer, Inc., Axa Parenterals Ltd, Ajinomoto Co., Inc., Otsuka Pharmaceutical Co., Ltd, Sichuan Kelun Pharmaceutical Co Ltd, Soxa Formulations & Research Pvt. Ltd and Braun Melsungen AG.

Key Developments:

In March 2022, Otsuka Pharmaceutical received regulatory approval in Japan for the sale of SAMTASU intravenous infusion for treating cardiac edema.

In February 2022, B. Braun Medical received the US FDA approval to begin operations at its new IV saline solution manufacturing facility in Daytona Beach, Florida.

In September 2021, B. Braun Medical Inc. launched CARESAFE IV Administration Sets with an Optional AirStop component.

In July 2021, Grifols S.A. announced the establishment of an intravenous (IV) solutions production plant in Nigeria.

Types Covered:

- Total Parenteral Nutrition

- Partial Parenteral Nutrition

Compositions Covered:

- Carbohydrates

- Vitamins and Minerals

- Parenteral Lipid Emulsion

- Single Dose Amino Acids

- Other Compositions

Solution Types Covered:

- Dextran

- Saline

- Hypertonic Saline

- Amino Acid

- Normal Saline

- Lactated Ringer's

- Heparin And Trace Elements

- Vitamins & Minerals

- Mixed Solutions

Bag Types Covered:

- Large Volume Bags

- Small Volume Bags

Applications Covered:

- Nutritional IV Solution

- Blood IV Solution

- Basic IV Solution

- Irrigation IV Solution

- Drug IV Solution

End Users Covered:

- Clinics

- Hospital

- Ambulatory Surgery Centers

- Home Care Settings

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 End User Analysis

- 3.8 Emerging Markets

- 3.9 Impact Of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Intravenous Solutions Market, By Type

- 5.1 Introduction

- 5.2 Total Parenteral Nutrition

- 5.3 Partial Parenteral Nutrition

6 Global Intravenous Solutions Market, By Composition

- 6.1 Introduction

- 6.2 Carbohydrates

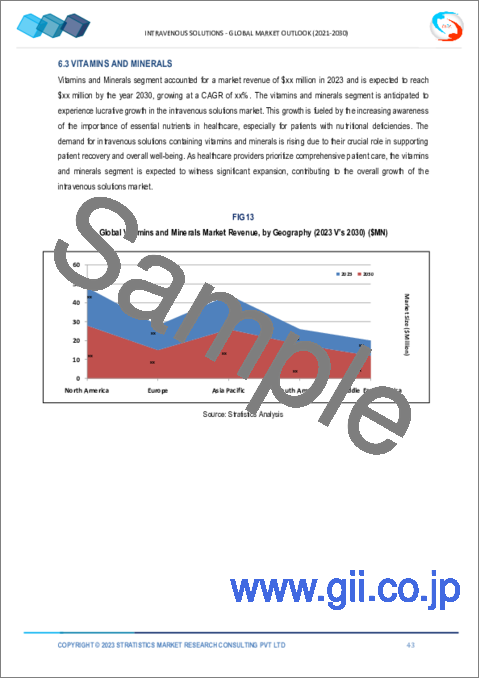

- 6.3 Vitamins And Minerals

- 6.4 Parenteral Lipid Emulsion

- 6.5 Single Dose Amino Acids

- 6.6 Other Compositions

7 Global Intravenous Solutions Market, By Solution Type

- 7.1 Introduction

- 7.2 Dextran

- 7.3 Saline

- 7.4 Hypertonic Saline

- 7.5 Amino Acid

- 7.6 Normal Saline

- 7.7 Lactated Ringer's

- 7.8 Heparin And Trace Elements

- 7.9 Vitamins & Minerals

- 7.1 Mixed Solutions

8 Global Intravenous Solutions Market, By Bag Type

- 8.1 Introduction

- 8.2 Large Volume Bags

- 8.3 Small Volume Bags

9 Global Intravenous Solutions Market, By Application

- 9.1 Introduction

- 9.2 Nutritional IV Solution

- 9.3 Blood IV Solution

- 9.4 Basic IV Solution

- 9.5 Irrigation IV Solution

- 9.6 Drug IV Solution

10 Global Intravenous Solutions Market, By End User

- 10.1 Introduction

- 10.2 Clinics

- 10.3 Hospital

- 10.4 Ambulatory Surgery Centers

- 10.5 Home Care Settings

11 Global Intravenous Solutions Market, By Geography

- 11.1 Introduction

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 Italy

- 11.3.4 France

- 11.3.5 Spain

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 Japan

- 11.4.2 China

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 New Zealand

- 11.4.6 South Korea

- 11.4.7 Rest of Asia Pacific

- 11.5 South America

- 11.5.1 Argentina

- 11.5.2 Brazil

- 11.5.3 Chile

- 11.5.4 Rest of South America

- 11.6 Middle East & Africa

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 Qatar

- 11.6.4 South Africa

- 11.6.5 Rest of Middle East & Africa

12 Key Developments

- 12.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 12.2 Acquisitions & Mergers

- 12.3 New Product Launch

- 12.4 Expansions

- 12.5 Other Key Strategies

13 Company Profiling

- 13.1 ICU Medical, Inc.

- 13.2 B. Braun Melsungen Ag

- 13.3 JW Life Science

- 13.4 Baxter International Inc.

- 13.5 Fresenius Kabi USA, LLC

- 13.6 Vifor Pharma Management Ltd

- 13.7 Amanta Healthcare

- 13.8 Grifols, S.A

- 13.9 Salius Pharma Private Limited.

- 13.10 Pfizer, Inc.

- 13.11 Axa Parenterals Ltd

- 13.12 Ajinomoto Co., Inc.

- 13.13 Otsuka Pharmaceutical Co., Ltd

- 13.14 Sichuan Kelun Pharmaceutical Co Ltd

- 13.15 Soxa Formulations & Research Pvt. Ltd

- 13.16 Braun Melsungen AG