|

|

市場調査レポート

商品コード

1308668

電池材料の2030年までの世界市場予測- タイプ別、材料別、用途別、地域別の世界分析Battery Materials Market Forecasts to 2030 - Global Analysis By Type (Lithium Ion, Lead-Acid and Other Types), Material (Separator, Cathode, Electrolyte, Anode and Other Materials), Application and By Geography |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 電池材料の2030年までの世界市場予測- タイプ別、材料別、用途別、地域別の世界分析 |

|

出版日: 2023年07月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 175+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の電池材料市場は2023年に668億1,000万米ドルを占め、予測期間中のCAGRは11.2%で成長し、2030年には1,404億6,000万米ドルに達すると予測されています。

電池材料は、電池の生産に使用される基本的な部品や原材料です。これらは主にニッケル、コバルト、リチウムなどの金属でできています。これらは、鉱石や塩水ブラインから電池用金属を精製する上流の採掘作業から得られます。電子機器は、エネルギー密度の高い電池材料の恩恵を受けています。蓄電容量が大きく、比エネルギーが高いのです。バッテリーパックは最終製品であり、自動車、家電、エネルギー貯蔵産業など、さまざまな最終市場で使用されています。

インド・ブランド・エクイティ財団(IBEF)のレビュー・レポートによると、インドでは2025年までにスマートフォンが4億1,000万台、電動二輪車が23万1,000台以上販売されると予想されています。

市場力学:

促進要因

電気自動車需要の増加

リチウムイオン電池(LIB)は、最も広く使用されている電気自動車技術です。一般的な自動車用LIBは、リチウム(Li)、コバルト(Co)、ニッケル(Ni)でできたカソードと、黒鉛でできたアノードを持ち、アルミニウムや銅を含むさまざまなセルやパックの部品が使われています。電池は自己発熱率が低く、特に電気自動車に有用であるため、電池原料の需要が高まっています。温室効果ガス排出量削減への取り組みの強化や、高速で高性能の充電ステーションの導入は、電気自動車販売、ひいては電池原料業界の改善につながる可能性が高いです。

阻害要因

不十分な充電インフラ

充電インフラが不十分なため、乗用車用電気自動車の発売は困難です。電気自動車の大半はリチウムイオン電池を利用するため、充電インフラが利用可能かどうかは業界の存続にとって極めて重要な要素です。EV充電インフラが不足しているため、EVは特定の地域でしか機能しないです。充電ステーションの不適切な配置の結果、送電網の電力需要が不均等になり、電力品質が低下し、電力損失が大きくなり、電力の安定性が低下します。エラーやスイッチング操作によって引き起こされる電圧降下は、市場の拡大を妨げる可能性があります。

機会:

エネルギー貯蔵装置の利用拡大

再生可能エネルギーのより良い利用は、エネルギー貯蔵装置によって可能になります。必要なときにいつでも利用できるように、蓄電池を利用して電力を蓄えることが不可欠です。蓄電装置は電気代と二酸化炭素排出量を最小限に抑えます。蓄電装置は送電網への依存度が低いです。高度なソフトウェアと組み合わされているため、障害が発生してもバックアップ電力を供給することができます。これらのエネルギー貯蔵システムは、経済的な節約、緊急時のバックアップ電力、太陽光発電の自給自足の強化などの利点を提供します。こうしたいくつかの要素が、市場拡大を加速させています。

脅威

鉛蓄電池材料に関する環境問題

鉛蓄電池の主成分である鉛は有害物質です。中国では、鉛蓄電池の鉛の44%から70%が廃棄され、環境に投棄されていると考えられています。ガソリンの数倍の汚染レベルが常に存在することになります。さらに、鉛蓄電池にさらされた人は、神経障害、心身の成長低下、集中力や学習能力の低下などを引き起こす可能性があります。こうした物質の使用には、専門的な知識、安全対策、適切な指導が必要です。こうした要因が市場の拡大を妨げています。

COVID-19影響:

サプライチェーンのあらゆる面がCOVID-19の流行によって大きな影響を受けています。エネルギー貯蔵業界は、製造、出荷停止、プロジェクト拡大、研究開発で困難を経験しました。電池関連製品の販売と生産速度はともに低下しました。電池原料の輸出入が制限された結果、供給と物流にも大きな混乱が生じた。中国メーカーが経験した困難は、注文の減少と請求書の未払いをもたらしました。大手電池メーカーは売上が減少する恐れがあったため、十分なキャッシュフローを確保するために、大手企業は小規模メーカーの顧客を奪って顧客を再編成しました。

予測期間中、リチウムイオン・セグメントが最大になると予想される:

リチウムイオン・セグメントは、その高いエネルギー密度、低い放電頻度、電圧容量により、有利な成長を遂げると推定されます。現在、最も普及しているエネルギー貯蔵技術はリチウムイオン電池です。リチウム、グラファイト、コバルト、マンガンはすべてリチウムイオン電池の成分です。鉛蓄電池に比べ、寿命は10倍にもなります。従来のバッテリーに比べ、リチウムイオンバッテリーはよりコンパクトで強力です。繰り返しの充放電にも効果的に耐えます。急速充電と自己放電防止機能がこの分野の拡大を促進しています。

予測期間中、正極のCAGRが最も高くなると予想される:

正極分野は予測期間中に最も速いCAGRの成長が見込まれます。二次電池の性能は正極材料に大きく依存します。電荷の流れは正極によって促進されます。酸化(電子の損失)は負極で起こり、還元(電子の獲得)は正極で起こる。正極材料の主な活性元素は、コバルト、ニッケル、マンガンです。コスト効率が高く、優れた性能を持ち、コバルトを含まず、ニッケルが少ないという利点が、その他の利点に加えてこのセグメントの成長を促進しています。

最大のシェアを占める地域:

予測期間中、アジア太平洋地域が最大の市場シェアを占めると予測されます。中国、日本、韓国は世界最大の電池メーカーであるため、電池原料の使用割合が大きいです。安価な生産インプットと有利な政府政策が利用可能なため、大規模なFDIがこの地域に引き寄せられ、複数の工業施設の存在がこの地域の優位性に寄与しています。さらに、この地域の電池材料市場は、ノートパソコン、スマートフォン、その他の携帯電子機器のような消費者向け電子製品で、携帯用電池パックや充電式電池パックの使用量が増加していることによって、おそらく加速しています。

CAGRが最も高い地域:

北米は、その技術的向上により、予測期間中に最も高いCAGRを示すと予測されています。同地域では、家電製品の利用が急速に増加しています。電気自動車や電気自転車の導入も急速に進んでいます。電気自動車や再生可能エネルギー分野への投資家も、政府からの支援を受けています。北米の市場が急速に成熟しつつあるのは、自動車の排ガスを規制する政府の厳しい法律、消費者の裁量所得の高さ、持続可能性と環境保全に対する消費者の意識の高まりなど、さまざまな要因が絡み合っているためです。

主な発展:

2023年2月、世界で最もエネルギー密度の高いリチウムイオン18650セルを実現する新興電池材料会社ナノグラフは、6,500万米ドルのシリーズB資金調達ラウンドを発表しました。ボルタ・エナジー・テクノロジーズとCCインダストリーズは、この投資ラウンドを共同で主導した(CCI)。バイデン大統領のインフレ削減法に従い、ナノグラフのシリーズB投資は、シカゴでのシリコン負極生産のオンショア化、革新的なリチウムイオン技術の継続的な開発、生産、提供を支援します。

2023年2月、ユミコアはテラファム社と低炭素で持続可能な高品位硫酸ニッケルの長期供給契約に合意しました。ユミコアとテラファム社の提携は、欧州における持続可能な電池材料のバリューチェーン構築に対する両社の揺るぎないコミットメントを再確認するものです。この提携は、ユミコアがポーランドに保有する正極材製造装置における将来のニッケル需要の大部分をカバーすることになります。これは正極材に特化した欧州初のギガファクトリーです。

レポート内容

- 地域および国レベルセグメントの市場シェア評価

- 新規参入企業への戦略的提言

- 2021年、2022年、2023年、2026年、2030年の市場データをカバー

- 市場動向(市場促進要因、阻害要因、機会、脅威、課題、投資機会、推奨事項)

- 市場推定に基づく主要ビジネスセグメントにおける戦略的提言

- 主要な共通トレンドをマッピングした競合情勢

- 詳細な戦略、財務、最近の動向を含む企業プロファイル

- 最新の技術動向をマッピングしたサプライチェーン動向

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下のいずれかの無料カスタマイズオプションをご提供いたします:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- アプリケーション分析

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の電池材料市場:タイプ別

- リチウムイオン

- 鉛酸

- その他

第6章 世界の電池材料市場:材料別

- セパレータ

- カソード

- 電解質

- アノード

- その他

第7章 世界の電池材料市場:用途別

- 産業用

- 自動車

- 家電

- その他

第8章 世界の電池材料市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第9章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第10章 企業プロファイル

- Mitsubishi Chemical Holdings

- BASF SE

- Hitachi Chemical Co Ltd

- Glencore PLC

- Kureha Corporation

- Norlisk Nickel

- NanoGraf

- NEI Corporation

- Asahi Kasei

- Umicore Cobalt & Specialty Materials

- Albemarle

- Targray Technology International

- TCI Chemicals Pvt. Ltd

- Livent Corporation

- Nichia Corporation

- Sheritt International Corporation

- SQM

- Vale S.A.

- Shanghai Shanshan Tech Co

- Teck Resources

List of Tables

- Table 1 Global Battery Materials Market Outlook, By Region (2021-2030) ($MN)

- Table 2 Global Battery Materials Market Outlook, By Type (2021-2030) ($MN)

- Table 3 Global Battery Materials Market Outlook, By Introduction (2021-2030) ($MN)

- Table 4 Global Battery Materials Market Outlook, By Lithium Ion (2021-2030) ($MN)

- Table 5 Global Battery Materials Market Outlook, By Lead-Acid (2021-2030) ($MN)

- Table 6 Global Battery Materials Market Outlook, By Other Types (2021-2030) ($MN)

- Table 7 Global Battery Materials Market Outlook, By Material (2021-2030) ($MN)

- Table 8 Global Battery Materials Market Outlook, By Separator (2021-2030) ($MN)

- Table 9 Global Battery Materials Market Outlook, By Cathode (2021-2030) ($MN)

- Table 10 Global Battery Materials Market Outlook, By Electrolyte (2021-2030) ($MN)

- Table 11 Global Battery Materials Market Outlook, By Anode (2021-2030) ($MN)

- Table 12 Global Battery Materials Market Outlook, By Other Materials (2021-2030) ($MN)

- Table 13 Global Battery Materials Market Outlook, By Application (2021-2030) ($MN)

- Table 14 Global Battery Materials Market Outlook, By Industrial (2021-2030) ($MN)

- Table 15 Global Battery Materials Market Outlook, By Automotive (2021-2030) ($MN)

- Table 16 Global Battery Materials Market Outlook, By Consumer Electronics (2021-2030) ($MN)

- Table 17 Global Battery Materials Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 18 North America Battery Materials Market Outlook, By Country (2021-2030) ($MN)

- Table 19 North America Battery Materials Market Outlook, By Type (2021-2030) ($MN)

- Table 20 North America Battery Materials Market Outlook, By Introduction (2021-2030) ($MN)

- Table 21 North America Battery Materials Market Outlook, By Lithium Ion (2021-2030) ($MN)

- Table 22 North America Battery Materials Market Outlook, By Lead-Acid (2021-2030) ($MN)

- Table 23 North America Battery Materials Market Outlook, By Other Types (2021-2030) ($MN)

- Table 24 North America Battery Materials Market Outlook, By Material (2021-2030) ($MN)

- Table 25 North America Battery Materials Market Outlook, By Separator (2021-2030) ($MN)

- Table 26 North America Battery Materials Market Outlook, By Cathode (2021-2030) ($MN)

- Table 27 North America Battery Materials Market Outlook, By Electrolyte (2021-2030) ($MN)

- Table 28 North America Battery Materials Market Outlook, By Anode (2021-2030) ($MN)

- Table 29 North America Battery Materials Market Outlook, By Other Materials (2021-2030) ($MN)

- Table 30 North America Battery Materials Market Outlook, By Application (2021-2030) ($MN)

- Table 31 North America Battery Materials Market Outlook, By Industrial (2021-2030) ($MN)

- Table 32 North America Battery Materials Market Outlook, By Automotive (2021-2030) ($MN)

- Table 33 North America Battery Materials Market Outlook, By Consumer Electronics (2021-2030) ($MN)

- Table 34 North America Battery Materials Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 35 Europe Battery Materials Market Outlook, By Country (2021-2030) ($MN)

- Table 36 Europe Battery Materials Market Outlook, By Type (2021-2030) ($MN)

- Table 37 Europe Battery Materials Market Outlook, By Introduction (2021-2030) ($MN)

- Table 38 Europe Battery Materials Market Outlook, By Lithium Ion (2021-2030) ($MN)

- Table 39 Europe Battery Materials Market Outlook, By Lead-Acid (2021-2030) ($MN)

- Table 40 Europe Battery Materials Market Outlook, By Other Types (2021-2030) ($MN)

- Table 41 Europe Battery Materials Market Outlook, By Material (2021-2030) ($MN)

- Table 42 Europe Battery Materials Market Outlook, By Separator (2021-2030) ($MN)

- Table 43 Europe Battery Materials Market Outlook, By Cathode (2021-2030) ($MN)

- Table 44 Europe Battery Materials Market Outlook, By Electrolyte (2021-2030) ($MN)

- Table 45 Europe Battery Materials Market Outlook, By Anode (2021-2030) ($MN)

- Table 46 Europe Battery Materials Market Outlook, By Other Materials (2021-2030) ($MN)

- Table 47 Europe Battery Materials Market Outlook, By Application (2021-2030) ($MN)

- Table 48 Europe Battery Materials Market Outlook, By Industrial (2021-2030) ($MN)

- Table 49 Europe Battery Materials Market Outlook, By Automotive (2021-2030) ($MN)

- Table 50 Europe Battery Materials Market Outlook, By Consumer Electronics (2021-2030) ($MN)

- Table 51 Europe Battery Materials Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 52 Asia Pacific Battery Materials Market Outlook, By Country (2021-2030) ($MN)

- Table 53 Asia Pacific Battery Materials Market Outlook, By Type (2021-2030) ($MN)

- Table 54 Asia Pacific Battery Materials Market Outlook, By Introduction (2021-2030) ($MN)

- Table 55 Asia Pacific Battery Materials Market Outlook, By Lithium Ion (2021-2030) ($MN)

- Table 56 Asia Pacific Battery Materials Market Outlook, By Lead-Acid (2021-2030) ($MN)

- Table 57 Asia Pacific Battery Materials Market Outlook, By Other Types (2021-2030) ($MN)

- Table 58 Asia Pacific Battery Materials Market Outlook, By Material (2021-2030) ($MN)

- Table 59 Asia Pacific Battery Materials Market Outlook, By Separator (2021-2030) ($MN)

- Table 60 Asia Pacific Battery Materials Market Outlook, By Cathode (2021-2030) ($MN)

- Table 61 Asia Pacific Battery Materials Market Outlook, By Electrolyte (2021-2030) ($MN)

- Table 62 Asia Pacific Battery Materials Market Outlook, By Anode (2021-2030) ($MN)

- Table 63 Asia Pacific Battery Materials Market Outlook, By Other Materials (2021-2030) ($MN)

- Table 64 Asia Pacific Battery Materials Market Outlook, By Application (2021-2030) ($MN)

- Table 65 Asia Pacific Battery Materials Market Outlook, By Industrial (2021-2030) ($MN)

- Table 66 Asia Pacific Battery Materials Market Outlook, By Automotive (2021-2030) ($MN)

- Table 67 Asia Pacific Battery Materials Market Outlook, By Consumer Electronics (2021-2030) ($MN)

- Table 68 Asia Pacific Battery Materials Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 69 South America Battery Materials Market Outlook, By Country (2021-2030) ($MN)

- Table 70 South America Battery Materials Market Outlook, By Type (2021-2030) ($MN)

- Table 71 South America Battery Materials Market Outlook, By Introduction (2021-2030) ($MN)

- Table 72 South America Battery Materials Market Outlook, By Lithium Ion (2021-2030) ($MN)

- Table 73 South America Battery Materials Market Outlook, By Lead-Acid (2021-2030) ($MN)

- Table 74 South America Battery Materials Market Outlook, By Other Types (2021-2030) ($MN)

- Table 75 South America Battery Materials Market Outlook, By Material (2021-2030) ($MN)

- Table 76 South America Battery Materials Market Outlook, By Separator (2021-2030) ($MN)

- Table 77 South America Battery Materials Market Outlook, By Cathode (2021-2030) ($MN)

- Table 78 South America Battery Materials Market Outlook, By Electrolyte (2021-2030) ($MN)

- Table 79 South America Battery Materials Market Outlook, By Anode (2021-2030) ($MN)

- Table 80 South America Battery Materials Market Outlook, By Other Materials (2021-2030) ($MN)

- Table 81 South America Battery Materials Market Outlook, By Application (2021-2030) ($MN)

- Table 82 South America Battery Materials Market Outlook, By Industrial (2021-2030) ($MN)

- Table 83 South America Battery Materials Market Outlook, By Automotive (2021-2030) ($MN)

- Table 84 South America Battery Materials Market Outlook, By Consumer Electronics (2021-2030) ($MN)

- Table 85 South America Battery Materials Market Outlook, By Other Applications (2021-2030) ($MN)

- Table 86 Middle East & Africa Battery Materials Market Outlook, By Country (2021-2030) ($MN)

- Table 87 Middle East & Africa Battery Materials Market Outlook, By Type (2021-2030) ($MN)

- Table 88 Middle East & Africa Battery Materials Market Outlook, By Introduction (2021-2030) ($MN)

- Table 89 Middle East & Africa Battery Materials Market Outlook, By Lithium Ion (2021-2030) ($MN)

- Table 90 Middle East & Africa Battery Materials Market Outlook, By Lead-Acid (2021-2030) ($MN)

- Table 91 Middle East & Africa Battery Materials Market Outlook, By Other Types (2021-2030) ($MN)

- Table 92 Middle East & Africa Battery Materials Market Outlook, By Material (2021-2030) ($MN)

- Table 93 Middle East & Africa Battery Materials Market Outlook, By Separator (2021-2030) ($MN)

- Table 94 Middle East & Africa Battery Materials Market Outlook, By Cathode (2021-2030) ($MN)

- Table 95 Middle East & Africa Battery Materials Market Outlook, By Electrolyte (2021-2030) ($MN)

- Table 96 Middle East & Africa Battery Materials Market Outlook, By Anode (2021-2030) ($MN)

- Table 97 Middle East & Africa Battery Materials Market Outlook, By Other Materials (2021-2030) ($MN)

- Table 98 Middle East & Africa Battery Materials Market Outlook, By Application (2021-2030) ($MN)

- Table 99 Middle East & Africa Battery Materials Market Outlook, By Industrial (2021-2030) ($MN)

- Table 100 Middle East & Africa Battery Materials Market Outlook, By Automotive (2021-2030) ($MN)

- Table 101 Middle East & Africa Battery Materials Market Outlook, By Consumer Electronics (2021-2030) ($MN)

- Table 102 Middle East & Africa Battery Materials Market Outlook, By Other Applications (2021-2030) ($MN)

According to Stratistics MRC, the Global Battery Materials Market is accounted for $66.81 billion in 2023 and is expected to reach $140.46 billion by 2030 growing at a CAGR of 11.2% during the forecast period. Battery materials are the basic components and raw materials used in the production of batteries. They are mostly made of metals like nickel, cobalt, and lithium. They come from upstream mining operations that purify battery metals from mineral ores or saltwater brines. Electronic gadgets benefit from high energy density battery materials. They have a large storage capacity and high specific energy. Battery packs are the final products, and they are used in many different end markets, including the automotive, consumer electronics, and energy storage industries.

According to the India Brand Equity Foundation (IBEF) review report, 410 million units of smart phones and over 231 thousand units of electric two wheelers are expected to be sold in India by 2025.

Market Dynamics:

Driver:

Increasing demand for electric vehicles

Lithium-ion batteries (LIBs) are the most extensively used EV technology. A typical car LIB has a cathode made of lithium (Li), cobalt (Co), and nickel (Ni), and an anode made of graphite and different cell and pack components including aluminum and copper. The demand for battery raw materials is rising as batteries have a low self-heating rate and are especially useful in electric vehicles. The increased efforts to decrease greenhouse gas emissions, as well as the implementation of high-speed and sophisticated charging stations, are likely to improve electric vehicle sales and hence the battery material industry.

Restraint:

Inadequate charging infrastructure

Launching of passenger electric vehicles would be challenging due to inadequate charging infrastructure. The majority of electric cars utilize lithium ion batteries, therefore the availability of charging infrastructure is a crucial component for the industry's viability. Due to a lack of EV charging infrastructure, EVs can only function in a certain geographic region. The grid's power demand becomes more unequal as a result of improper charging station placement, which leads to poor power quality, greater power loss, and decreased power stability. Voltage drops brought on by errors or switching operations could hinder market expansion.

Opportunity:

Raising usage of energy storage devices

Better usage of renewable energy is made possible by energy storage devices. It is essential to utilize batteries to store this power so that it is available whenever you need it. They minimize electricity costs and carbon footprint. The energy storage devices are less dependent on the grid. When there are disturbances, they can supply backup power since they are combined with sophisticated software. These energy storage systems offer advantages including financial savings, emergency backup power, and enhancing solar self-supply. These several elements are accelerating the market expansion.

Threat:

Environmental concerns regarding lead-acid battery materials

Lead, the primary component of lead-acid batteries, is a hazardous substance. In the PRC, it is thought that between 44% and 70% of the lead from lead acid batteries is wasted and dumped into the environment. There will always be pollution levels that are several times higher than those of gasoline. Additionally, they may result in neurological damage, decreased physical and mental growth, and difficulty with focus and learning for the individual exposed to them. Such material usage calls for specialized knowledge, safety measures, and appropriate instruction. These factors are impeding market expansion.

COVID-19 Impact:

All facets of the supply chain have been extensively impacted by the COVID-19 epidemic. The energy storage industry experienced challenges with manufacturing, shipping hold-ups, project expansion, and R&D. Sales of battery-related products and the rate at which they are produced have both decreased. As a result of the restrictions on the import and export of raw materials for batteries, there were also significant disruptions in supply and logistics. The difficulties experienced by Chinese manufacturers resulted in fewer orders and unpaid invoices. Big battery makers ran the danger of seeing their sales decline; therefore larger businesses realigned their clientele by snatching up some of the small manufacturers' customers in order to generate enough cash flow.

The lithium-ion segment is expected to be the largest during the forecast period:

The lithium-ion segment is estimated to have a lucrative growth, due to its high energy density, low discharge frequency, and voltage capacity. Currently, the most popular energy storage technology is lithium-ion batteries. Lithium, graphite, cobalt, and manganese are all components of lithium-ion batteries. Compared to lead-acid batteries, their lifespan can be up to 10 times longer. Compared to conventional batteries, lithium-ion batteries are more compact and potent. They withstand repeated charging and discharging effectively. Their quick charging and anti-self-discharge features are promoting the segment's expansion.

The cathode segment is expected to have the highest CAGR during the forecast period:

The cathode segment is anticipated to witness the fastest CAGR growth during the forecast period. The performance of rechargeable batteries is highly dependent on the cathode materials. The electric charge flow is facilitated by the cathode. While oxidation (loss of electrons) happens at the anode, reduction (gain of electrons) takes place at the cathode, which is the positive electrode. The main active elements in cathode materials are cobalt, nickel, and manganese. The benefits of being cost-effective, exceptional performance, cobalt-free, and low in nickel are propelling the segment's growth in addition to these other benefits.

Region with largest share:

Asia Pacific is projected to hold the largest market share during the forecast period. China, Japan, and South Korea use a significant proportion of battery raw materials since they constitute the world's largest battery manufacturers. Large FDIs have been drawn to this area as a result of the availability of inexpensive production inputs and favourable government policies, and the existence of several industrial facilities has contributed to the region's supremacy. Additionally, the market for battery materials in the area is probably being accelerated by the rising usage of portable and rechargeable battery packs in consumer electronics products like laptops, smart phones, and other portable electronic devices.

Region with highest CAGR:

North America is projected to have the highest CAGR over the forecast period, owing to its technical improvements. The usage of consumer electronics in this region has been rapidly increasing. Electric automobiles and bicycles are being adopted quickly. Investors in the electric car and renewable energy sectors are also receiving help from the government. The market in North America is maturing quickly due to a combination of factors including severe government laws regulating car emissions, high consumer discretionary income, and growing consumer awareness of sustainability and environmental preservation.

Key players in the market

Some of the key players profiled in the Battery Materials Market include Mitsubishi Chemical Holdings, BASF SE, Hitachi Chemical Co Ltd, Glencore PLC, Kureha Corporation, Norlisk Nickel, NanoGraf, NEI Corporation, Asahi Kasei, Umicore Cobalt & Specialty Materials, Albemarle, Targray Technology International, TCI Chemicals Pvt. Ltd, Livent Corporation, Nichia Corporation, Sheritt International Corporation, SQM, Vale S.A., Shanghai Shanshan Tech Co and Teck Resources.

Key Developments:

In February 2023, NanoGraf, a start-up battery Materials Company and enabler of the world's most energy-dense lithium-ion 18650 cells, announced a USD 65 million Series B fundraising round. Volta Energy Technologies and CC Industries co-led the investment round (CCI). In accordance with President Biden's Inflation Reduction Act, NanoGraf's Series B investment supports the onshoring of its silicon anode production in Chicago, as well as the continuous development, production, and delivery of innovative lithium-ion technology.

In February 2023, Umicore agreed to a long-term supply arrangement with Terrafame Ltd. for low-carbon, sustainable high-grade nickel sulfate. Umicore and Terrafame's collaboration reaffirms their unwavering commitment to building a sustainable battery materials value chain in Europe. This arrangement will cover a significant portion of Umicore's future nickel demand at its cathode materials unit in Poland. This is Europe's first gigafactory dedicated to cathode materials.

Types Covered:

- Lithium Ion

- Lead-Acid

- Other Types

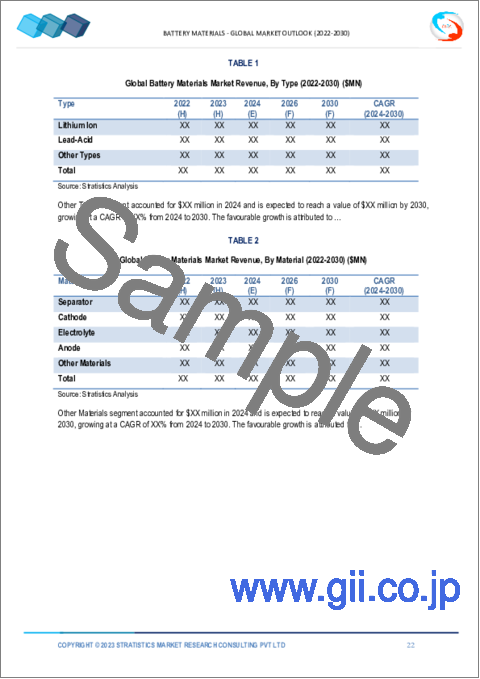

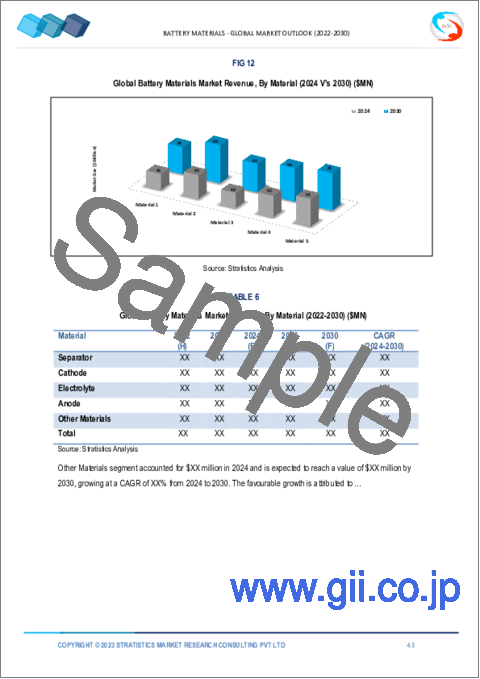

Materials Covered:

- Separator

- Cathode

- Electrolyte

- Anode

- Other Materials

Applications Covered:

- Industrial

- Automotive

- Consumer Electronics

- Other Applications

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2021, 2022, 2023, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Application Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Battery Materials Market, By Type

- 5.1 Introduction

- 5.2 Lithium Ion

- 5.3 Lead-Acid

- 5.4 Other Types

6 Global Battery Materials Market, By Material

- 6.1 Introduction

- 6.2 Separator

- 6.3 Cathode

- 6.4 Electrolyte

- 6.5 Anode

- 6.6 Other Materials

7 Global Battery Materials Market, By Application

- 7.1 Introduction

- 7.2 Industrial

- 7.3 Automotive

- 7.4 Consumer Electronics

- 7.5 Other Applications

8 Global Battery Materials Market, By Geography

- 8.1 Introduction

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Italy

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 New Zealand

- 8.4.6 South Korea

- 8.4.7 Rest of Asia Pacific

- 8.5 South America

- 8.5.1 Argentina

- 8.5.2 Brazil

- 8.5.3 Chile

- 8.5.4 Rest of South America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 Qatar

- 8.6.4 South Africa

- 8.6.5 Rest of Middle East & Africa

9 Key Developments

- 9.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 9.2 Acquisitions & Mergers

- 9.3 New Product Launch

- 9.4 Expansions

- 9.5 Other Key Strategies

10 Company Profiling

- 10.1 Mitsubishi Chemical Holdings

- 10.2 BASF SE

- 10.3 Hitachi Chemical Co Ltd

- 10.4 Glencore PLC

- 10.5 Kureha Corporation

- 10.6 Norlisk Nickel

- 10.7 NanoGraf

- 10.8 NEI Corporation

- 10.9 Asahi Kasei

- 10.10 Umicore Cobalt & Specialty Materials

- 10.11 Albemarle

- 10.12 Targray Technology International

- 10.13 TCI Chemicals Pvt. Ltd

- 10.14 Livent Corporation

- 10.15 Nichia Corporation

- 10.16 Sheritt International Corporation

- 10.17 SQM

- 10.18 Vale S.A.

- 10.19 Shanghai Shanshan Tech Co

- 10.20 Teck Resources