自動車用ガラス市場:産業動向・世界の予測 (~2035年):製品タイプ・技術・用途・車両タイプ・流通タイプ・企業規模・主要地域別

Automotive Glass Market, Till 2035: Distribution by Type of Product, Type of Technology, Type of Application, Type of Vehicle, Type of Distribution, Company Size, and Key Geographical Regions: Industry Trends and Global Forecasts- 発行日

- ページ情報

- 英文 248 Pages

- 納期

- 7~10営業日

- 商品コード

- 1803904

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

- 医薬品関連専門 医薬品関連専門を専門とする市場調査会社です。

概要

自動車用ガラス市場の概要

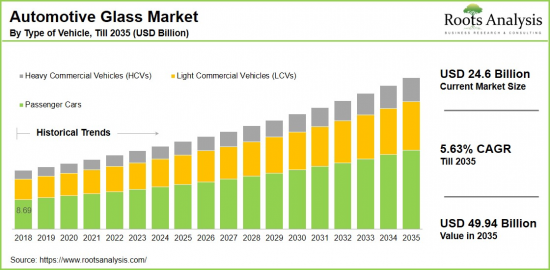

世界の自動車用ガラスの市場規模は、現在の246億米ドルから、予測期間中はCAGR 5.63%で推移し、2035年には499億4,000万米ドルに成長すると予測されています。

自動車用ガラス市場の機会:分類

製品タイプ

- 合わせガラス

- 強化ガラス

- その他

技術タイプ

- スマートガラス

- 標準ガラス

用途

- フロントガラス

- サイドライト

- バックライト (リアガラス)

- リアクォーターガラス

- サンルーフ

車両タイプ

- 乗用車

- 小型商用車 (LCV)

- 大型商用車 (HCV)

流通タイプ

- OEM

- アフターマーケット

企業規模

地域

- 北米

- 米国

- カナダ

- メキシコ

- その他

- 欧州

- オーストリア

- ベルギー

- デンマーク

- フランス

- ドイツ

- アイルランド

- イタリア

- オランダ

- ノルウェー

- ロシア

- スペイン

- スウェーデン

- スイス

- 英国

- その他

- アジア

- 中国

- インド

- 日本

- シンガポール

- 韓国

- その他

- ラテンアメリカ

- ブラジル

- チリ

- コロンビア

- ベネズエラ

- その他

- 中東・北アフリカ

- エジプト

- イラン

- イラク

- イスラエル

- クウェート

- サウジアラビア

- アラブ首長国連邦

- その他の中東・北アフリカ諸国

- 世界のその他の地域

- オーストラリア

- ニュージーランド

- その他

自動車用ガラス市場:成長と動向

自動車セクターの成長は、商用車、乗用車、電気自動車の製造・販売の増加によって特徴づけられ、自動車用ガラス市場に新たな道を開きました。自動車用ガラスは、乗用車、バス、トラックを含む車両に使用される特別に設計されたガラスであり、乗員の安全性、視認性、快適性を確保する役割を担っています。このガラスは走行中に受けるさまざまなストレスや衝撃に耐えられるように設計されており、重要な構造的支持と保護を提供します。

市場では、合わせガラスや強化ガラスなど多様な製品が提供されており、フロントガラス (ウィンドシールド) 、サイドライト、サイドウィンドウ、バックライト、リアウィンドウ、リアクォーターガラス、サンルーフといった用途に使用されています。特にフロントガラスは、自動車用ガラス市場の需要を牽引する重要な用途です。通常、合わせガラスで構成されており、これは2枚のガラス層の間にプラスチック中間膜 (一般的にはポリビニルブチラール) が挟まれた構造で、衝撃を受けても鋭利な破片に割れにくく、安全性を高めます。さらに、産業オートメーションの導入によって、自動車用ガラスの製造プロセスは革新されています。

加えて、自動車用ガラス分野における継続的な技術革新として、スマート機能や先進運転支援システム (ADAS) の導入が進み、まぶしさや熱を軽減することで安全性と快適性を高めるスマートガラスやゴリラガラスの需要が拡大しています。これらの進歩は空調依存を減らすことで省エネルギー化を促進し、さらに美観やプライバシーの向上にもつながります。同様に、サンルーフ向けスマートガラスの生産も世界各地で急増しており、市場成長を後押ししています。

その結果、自動車用ガラスメーカーは、これらの技術革新を活かして、乗員の快適性やエネルギー効率を改善しつつ、新しい機能を備えた先進的な製品やサービスを提供しています。さらに、進化する顧客ニーズに対応するため、研究開発への継続的な投資も行っています。これらの要素を踏まえると、自動車用ガラス市場は予測期間中に大きな成長を遂げると見込まれます。

当レポートでは、世界の自動車用ガラスの市場を調査し、 市場概要、背景、市場影響因子の分析、市場規模の推移・予測、各種区分・地域別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

第1章 序文

第2章 調査手法

第3章 経済的およびその他のプロジェクト特有の考慮事項

第4章 マクロ経済指標

第5章 エグゼクティブサマリー

第6章 イントロダクション

第7章 競合情勢

第8章 企業プロファイル

- 章の概要

- AGC

- Central Glass

- Corning Incorporated

- Fuyao Glass

- Guardian Industries

- Magna International

- Nippon Sheet Glass

- Saint Gobain

- Webasto Group

- Xinyi Glass Holdings

第9章 バリューチェーン分析

第10章 SWOT分析

第11章 世界の自動車用ガラス市場

第12章 製品タイプ別の市場機会

第13章 技術別の市場機会

第14章 用途別の市場機会

第15章 車両タイプ別の市場機会

第16章 流通形態別の市場機会

第17章 企業規模別の市場機会

第18章 北米における自動車用ガラスの市場機会

第19章 欧州における自動車用ガラスの市場機会

第20章 アジアの自動車用ガラスの市場機会

第21章 中東・北アフリカにおける自動車用ガラスの市場機会

第22章 ラテンアメリカにおける自動車用ガラスの市場機会

第23章 世界のその他の地域の自動車用ガラスの市場機会

第24章 表形式データ

第25章 企業・団体一覧

第26章 カスタマイズの機会

第27章 ROOTSサブスクリプションサービス

第28章 著者詳細

目次

Automotive Glass Market Overview

As per Roots Analysis, the global automotive glass market size is estimated to grow from USD 24.6 billion in the current year to USD 49.94 billion by 2035, at a CAGR of 5.63% during the forecast period, till 2035.

The opportunity for automotive glass market has been distributed across the following segments:

Type of Product

- Laminated Glass

- Tempered Glass

- Others

Type of Technology

- Smart Glass

- Standard Glass

Type of Application

- Windshield

- Sidelite (Side Windows)

- Backlite (Rear Windows)

- Rear Quarter Glass

- Sunroof

Type of Vehicle

- Passenger Cars

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

Type of Distribution

- OEM (Original Equipment Manufacturer)

- Aftermarket

Company Size

- Type of Distribution

- OEM (Original Equipment Manufacturer)

- Aftermarket

Geographical Regions

- North America

- US

- Canada

- Mexico

- Other North American countries

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Other European countries

- Asia

- China

- India

- Japan

- Singapore

- South Korea

- Other Asian countries

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Other Latin American countries

- Middle East and North Africa

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Other MENA countries

- Rest of the World

- Australia

- New Zealand

- Other countries

Automotive Glass Market: Growth and Trends

The growth of the automotive sector, characterized by a rise in the manufacturing and sale of commercial, passenger, and electric vehicles, has opened up new avenues for the automotive glass market. Automotive glass is a type of specially engineered glass utilized in vehicles, including cars, buses, and trucks, to ensure the safety, visibility, and comfort of those inside. This glass is designed to endure various stresses and impacts faced during vehicle operation, offering crucial structural support and protection.

The market offers a wide variety of glasses, such as laminated and tempered glass, which are used for applications like windshields, sidelites, side windows, backlites, rear windows, rear quarter glass, and sunroofs. Notably, the windshield is a significant application that has driven demand in the automotive glass sector. Typically made of laminated glass, which consists of two glass layers with a plastic interlayer (usually polyvinyl butyral) sandwiched in between, this construction prevents the glass from breaking into sharp shards upon impact, thereby enhancing safety. Moreover, the adoption of industrial automation has revolutionized the process of manufacturing automotive glass.

In addition, ongoing technological advancements within the automotive glass sector, including the incorporation of smart features and Advanced Driver Assistance Systems (ADAS), have led to a growing demand for smart and gorilla glasses that provide enhanced safety and comfort for both drivers and passengers by reducing glare and heat. These advancements also promote energy efficiency by decreasing dependence on air conditioning and provide both aesthetic appeal and privacy benefits. Similarly, there is a rapid increase in the production of smart glass options for sunroofs across various regions, fueling market growth.

As a result, by capitalizing on these technological innovations, manufacturers of automotive glass are introducing advanced products and services to improve passenger comfort and energy efficiency while incorporating new functionalities. In addition, they are consistently investing in research and development to meet the evolving needs of customers in the automotive glass market. Considering these elements, the automotive glass market is expected to experience significant growth during the forecast period.

Automotive Glass Market: Key Segments

Market Share by Type of Product

Based on type of product, the global automotive glass market is segmented into laminated glass, tempered glass, and others. According to our estimates, currently, the laminated glass segment captures the majority share of the market. This can be attributed to the fact that it is a well-established protective solution that provides safety benefits, such as maintaining its structure when broken and minimizing the risk of injury from shattering glass pieces. Additionally, it is predominantly used for windshields due to its superior safety compared to tempered glass for front windows

However, the tempered glass segment is expected to grow at a higher CAGR during the forecast period, due to its affordability and strong protective qualities.

Market Share by Type of Technology

Based on type of technology, the automotive glass market is segmented into standard glass and smart glass. According to our estimates, currently, the smart glass segment captures the majority of the market. This growth can be attributed to various types of smart glass, including electrochromic, Polymer Dispersed Liquid Devices (PDLC), and Suspended Particle Devices (SPD), along with their associated advantages.

Furthermore, ongoing advancements in technology, an increasing preference for high-end luxury vehicles, and features such as dynamic tinting, glare reduction, improved comfort, and safety for drivers and passengers are likely to drive demand within the automotive sector. However, the smart glass segment is expected to grow at a higher CAGR during the forecast period.

Market Share by Type of Application

Based on type of application, the automotive glass market is segmented into windshield, sidelite (side windows, backlite (rear windows), rear quarter glass, and sunroof. According to our estimates, currently, the windshield segment captures the majority share of the market.

As a vital part of any passenger vehicle, the windshield protects both the driver and passengers from debris and environmental hazards while ensuring clear visibility for the driver. Windshields are generally constructed from laminated glass, which is specifically engineered to avoid shattering on impact. Moreover, contemporary windshields provide numerous additional benefits, such as sound insulation, UV protection, heads-up displays (HUD), and rain sensors.

However, the side windows segment is expected to grow at a higher CAGR during the forecast period, driven by increasing concerns related to vehicle security and the enforcement of stricter safety regulations.

Market Share by Type of Vehicle

Based on type of vehicle, the automotive glass market is segmented into passenger cars, light commercial vehicles, and heavy commercial vehicles. According to our estimates, currently, the passenger car segment captures the majority share of the market. This is due to the growing demand for electric and light commercial vehicles.

Additionally, the increasing focus on emission control and environmental regulations is driving the production of electric and hybrid vehicles, fueling the growth of the market.

Market Share by Type of Distribution

Based on type of distribution, the automotive glass market is segmented into OEM (original equipment manufacturer) and aftermarket. According to our estimates, currently, the OEM segment captures the majority share of the market, due to its advantages in durability, high quality, and precise fitting with the vehicle's design.

However, the aftermarket segment is expected to grow at a higher CAGR during the forecast period, driven by the need for glass replacement and vehicle maintenance.

Market Share by Company Size

Based on company size, the automotive glass market is segmented into small and medium-sized enterprises (SMEs) and large enterprises. According to our estimates, currently, the large enterprises segment captures the majority share of the market. This can be attributed to their expansive distribution networks, significant capital investments in product innovation, and advanced manufacturing technologies.

Moreover, their ability to scale production and deliver high-quality products to meet the increasing demands of both OEM and aftermarket sectors helps them maintain their leading position. Given these factors, the segment of large enterprises is expected to continue propelling the market at an accelerated growth rate during the forecast period.

Market Share by Geographical Regions

Based on geographical regions, the automotive glass market is segmented into North America, Europe, Asia, Latin America, Middle East and North Africa, and the rest of the world. According to our estimates, currently, Asia Pacific captures the majority share of the market, due to the expanding aftermarket sector and the increasing customer base in the area.

Example Players in Automotive Glass Market

- AGC

- Central Glass

- Corning Incorporated

- Fuyao Glass

- Guardian Industries

- Magna International

- Nippon Sheet Glass

- Pilkington Group

- Saint Gobain

- Taiwan Glass Industry

- Vitro S.A.B. de C.V.

- Webasto Group

- Xinyi Glass Holdings

Automotive Glass Market: Research Coverage

The report on the automotive glass market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the automotive glass market, focusing on key market segments, including [A] type of product, [B] type of technology, [C] type of application, [D] type of vehicle, [E] type of distribution, [F] company size, and [G] key geographical regions.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the automotive glass market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the automotive glass market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] automotive glass portfolio, [J] moat analysis, [K] recent developments, and an informed future outlook.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

- Value Chain Analysis: A comprehensive analysis of the value chain, providing information on the different phases and stakeholders involved in the automotive glass market

Key Questions Answered in this Report

- How many companies are currently engaged in automotive glass market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

- 3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.2.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7 Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.5.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.5.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of Automotive Glass

- 6.2.1. Type of Product

- 6.2.2. Type of Technology

- 6.2.3. Type of Application

- 6.2.4. Type of Vehicle

- 6.3. Future Perspective

7. COMPETITIVE LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Automotive Glass: Overall Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters

- 7.2.4. Analysis by Ownership Structure

8. COMPANY PROFILES

- 8.1. Chapter Overview

- 8.2.1. AGC*

- 8.2.1.1. Company Overview

- 8.2.1.2. Company Mission

- 8.2.1.3. Company Footprint

- 8.2.1.4. Management Team

- 8.2.1.5. Contact Details

- 8.2.1.6. Financial Performance

- 8.2.1.7. Operating Business Segments

- 8.2.1.7. Service / Product Portfolio (project specific)

- 8.2.1.9. MOAT Analysis

- 8.2.1.10. Recent Developments and Future Outlook

- 8.2.2. Central Glass

- 8.2.3. Corning Incorporated

- 8.2.4. Fuyao Glass

- 8.2.5. Guardian Industries

- 8.2.6. Magna International

- 8.2.7. Nippon Sheet Glass

- 8.2.8. Saint Gobain

- 8.2.9. Webasto Group

- 8.2.10. Xinyi Glass Holdings

- 8.2.1. AGC*

9. VALUE CHAIN ANALYSIS

10. SWOT ANALYSIS

11. GLOBAL AUTOMOTIVE GLASS MARKET

- 11.1. Chapter Overview

- 11.2. Key Assumptions and Methodology

- 11.3. Trends Disruption Impacting Market

- 11.4. Global Automotive Glass Market, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 11.5. Multivariate Scenario Analysis

- 11.5.1. Conservative Scenario

- 11.5.2. Optimistic Scenario

- 11.6. Key Market Segmentations

12. MARKET OPPORTUNITIES BASED ON TYPE OF PRODUCT

- 12.1. Chapter Overview

- 12.2. Key Assumptions and Methodology

- 12.3. Revenue Shift Analysis

- 12.4. Market Movement Analysis

- 12.5. Penetration-Growth (P-G) Matrix

- 12.6. Automotive Glass Market for Laminated Glass: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 12.7. Automotive Glass Market for Tempered Glass: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 12.8. Automotive Glass Market for Others: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 12.9. Data Triangulation and Validation

13. MARKET OPPORTUNITIES BASED ON TYPE OF TECHNOLOGY

- 13.1. Chapter Overview

- 13.2. Key Assumptions and Methodology

- 13.3. Revenue Shift Analysis

- 13.4. Market Movement Analysis

- 13.5. Penetration-Growth (P-G) Matrix

- 13.6. Automotive Glass Market for Smart Glass: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 13.7. Automotive Glass Market for Standard Glass: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 13.8. Data Triangulation and Validation

14. MARKET OPPORTUNITIES BASED ON TYPE OF APPLICATION

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Revenue Shift Analysis

- 14.4. Market Movement Analysis

- 14.5. Penetration-Growth (P-G) Matrix

- 14.6. Automotive Glass Market for Windshield: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.7. Automotive Glass Market for Sidelite (Side Windows): Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.8. Automotive Glass Market for Backlite (Read Windows): Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.9. Automotive Glass Market for Rear Quarter Glass: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.10. Automotive Glass Market for Sunroof: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 14.11. Data Triangulation and Validation

15. MARKET OPPORTUNITIES BASED ON TYPE OF VEHICLE

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Revenue Shift Analysis

- 15.4. Market Movement Analysis

- 15.5. Penetration-Growth (P-G) Matrix

- 15.6. Automotive Glass Market for Passenger Cars: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 15.7. Automotive Glass Market for Light Commercial Vehicles: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 15.8. Automotive Glass Market for Heavy Commercial Vehicles: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 15.9. Data Triangulation and Validation

16. MARKET OPPORTUNITIES BASED ON TYPE OF DISTRIBUTION

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Revenue Shift Analysis

- 16.4. Market Movement Analysis

- 16.5. Penetration-Growth (P-G) Matrix

- 16.6. Automotive Glass Market for Original Equipment Manufacturer (OEM): Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.7. Automotive Glass Market for Aftermarket: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.8. Data Triangulation and Validation

17. MARKET OPPORTUNITIES BASED ON COMPANY SIZE

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Revenue Shift Analysis

- 17.4. Market Movement Analysis

- 17.5. Penetration-Growth (P-G) Matrix

- 17.6. Automotive Glass Market for Small and Medium-sized Enterprises (SMEs): Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.7. Automotive Glass Market for Large Enterprises: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.8. Data Triangulation and Validation

18. MARKET OPPORTUNITIES FOR AUTOMOTIVE GLASS IN NORTH AMERICA

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Revenue Shift Analysis

- 18.4. Market Movement Analysis

- 18.5. Penetration-Growth (P-G) Matrix

- 18.6. Automotive Glass Market in North America: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 18.6.1. Automotive Glass Market in the US: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 18.6.2. Automotive Glass Market in Canada: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 18.6.3. Automotive Glass Market in Mexico: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 18.6.4. Automotive Glass Market in Other North American Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 18.7. Data Triangulation and Validation

19. MARKET OPPORTUNITIES FOR AUTOMOTIVE GLASS IN EUROPE

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. Automotive Glass Market in Europe: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.1. Automotive Glass Market in the Austria: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.2. Automotive Glass Market in Belgium: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.3. Automotive Glass Market in Denmark: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.4. Automotive Glass Market in France: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.5. Automotive Glass Market in Germany: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.6. Automotive Glass Market in Ireland: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.7. Automotive Glass Market in Italy: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.8. Automotive Glass Market in Netherlands: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.9. Automotive Glass Market in Norway: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.10. Automotive Glass Market in Russia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.11. Automotive Glass Market in Spain: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.12. Automotive Glass Market in Sweden: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.13. Automotive Glass Market in Switzerland: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.14. Automotive Glass Market in the UK: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.6.15. Automotive Glass Market in Other European Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.7. Data Triangulation and Validation

20. MARKET OPPORTUNITIES FOR AUTOMOTIVE GLASS IN ASIA

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. Automotive Glass Market in Asia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.6.1. Automotive Glass Market in China: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.6.2. Automotive Glass Market in India: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.6.3. Automotive Glass Market in Japan: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.6.4. Automotive Glass Market in Singapore: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.6.5. Automotive Glass Market in South Korea: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.6.6. Automotive Glass Market in Other Asian Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.7. Data Triangulation and Validation

21. MARKET OPPORTUNITIES FOR AUTOMOTIVE GLASS IN MIDDLE EAST AND NORTH AFRICA

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. Automotive Glass Market in Middle East and North Africa (MENA): Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.6.1. Automotive Glass Market in Egypt: Historical Trends (Since 2018) and Forecasted Estimates (Till 205)

- 21.6.2. Automotive Glass Market in Iran: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.6.3. Automotive Glass Market in Iraq: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.6.4. Automotive Glass Market in Israel: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.6.5. Automotive Glass Market in Kuwait: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.6.6. Automotive Glass Market in Saudi Arabia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.6.7. Automotive Glass Market in United Arab Emirates (UAE): Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.6.8. Automotive Glass Market in Other MENA Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.7. Data Triangulation and Validation

22. MARKET OPPORTUNITIES FOR AUTOMOTIVE GLASS IN LATIN AMERICA

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. Automotive Glass Market in Latin America: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.6.1. Automotive Glass Market in Argentina: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.6.2. Automotive Glass Market in Brazil: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.6.3. Automotive Glass Market in Chile: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.6.4. Automotive Glass Market in Colombia Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.6.5. Automotive Glass Market in Venezuela: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.6.6. Automotive Glass Market in Other Latin American Countries: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.7. Data Triangulation and Validation

23. MARKET OPPORTUNITIES FOR AUTOMOTIVE GLASS IN REST OF THE WORLD

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. Automotive Glass Market in Rest of the World: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.6.1. Automotive Glass Market in Australia: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.6.2. Automotive Glass Market in New Zealand: Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.6.3. Automotive Glass Market in Other Countries

- 23.7. Data Triangulation and Validation

24. TABULATED DATA

25. LIST OF COMPANIES AND ORGANIZATIONS

26. CUSTOMIZATION OPPORTUNITIES

27. ROOTS SUBSCRIPTION SERVICES

28. AUTHOR DETAIL

- 発行日

- 発行

- Roots Analysis

- ページ情報

- 英文 248 Pages

- 納期

- 7~10営業日