|

|

市場調査レポート

商品コード

1690800

自動車用スマートガラス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Automotive Smart Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用スマートガラス:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

自動車用スマートガラスの市場規模は2025年に31億9,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは22.03%で、2030年には86億2,000万米ドルに達すると予測されます。

自動車用スマートガラス市場は、技術の進歩と先進的な車両機能に対する消費者の需要の高まりにより、著しい成長を遂げています。切替可能なガラスとしても知られるスマートガラスは、色合い調整、透明度調整、熱低減などの機能を提供し、自動車の快適性とエネルギー効率の両方を向上させます。

開発メーカーは、スマートガラス・ソリューションの性能と信頼性を向上させるため、新素材や新技術を継続的に開発しています。例えば、エレクトロクロミック技術やSPD(Suspended Particle Device)技術の進歩により、スマートガラス製品の応答時間の短縮、エネルギー効率の向上、耐久性の強化が可能になりました。

自動車メーカー、ガラスメーカー、技術プロバイダー間の提携も市場拡大の原動力となっています。ガラスメーカーと自動車メーカー双方の専門知識を活用し、高度な機能性と快適性を求める消費者の要求に応えることで、スマートガラス・ソリューションの新型車への統合を可能にしています。

さらに、自動車メーカーがユーザーエクスペリエンス、エネルギー効率、環境持続可能性を向上させる革新的な機能で自社製品の差別化を図る中、自動車用スマートガラス市場は継続的な成長が見込まれています。この進化は、自動車のデザインと機能の未来を形作る上で、スマートガラス技術の重要性が増していることを裏付けています。

自動車用スマートガラス市場の動向

自動車における浮遊粒子装置(SPD)の普及率の上昇

乗用車が自動車用スマートガラス市場の優位性を牽引していることは、業界の複数の要因や動向からも明らかです。2023年の世界の自動車販売台数は約6,520万台に急増し、2022年の約5,860万台から大幅に増加しました。このような自動車販売台数の増加傾向は、スマートガラスソリューションを含む先進的な自動車技術に対する需要の高まりを反映しています。

懸濁粒子デバイス(SPD)は、自動車分野で重要なイノベーションとして台頭しています。これらのデバイスは、自動車のガラスやプラスチックを動的に調整可能な光管理システムに変えることで、運転体験を向上させます。この技術は、特にサンルーフ、窓、バイザーに有益で、ユーザーの快適性と車の美観を大幅に向上させる。

SPDスマートグラスはその効率性で際立っており、PDLCスマートグラスが1平方メートルあたり3ワットを必要とするのに対し、SPDスマートグラスは1平方メートルあたりわずか1.5ワットしか消費しないです。このエネルギー消費の低さは、燃費の向上と環境負荷の低減につながります。例えば、コンチネンタルの報告によると、SPDスマートガラスは二酸化炭素排出量を1キロメートルあたり4グラム削減し、航続距離を5.5%伸ばすことができます。

さらに、SPDスマートガラスは車内の熱を大幅に低減することで、より快適で贅沢なドライビング体験に貢献します。メルセデス・ベンツは、SクラスセダンやSLロードスターなどのハイエンドモデルにSPDガラスを採用し、車内温度を最大10℃(華氏18度)低下させました。この低減は、乗員の快適性を高めるだけでなく、赤外線や紫外線による早期老化から内装材を保護する効果もあります。

スマートガラス技術の進展と大手自動車メーカーによる採用により、乗用車は自動車用スマートガラス市場において優位性を維持するものと思われます。コンチネンタルのような企業による研究開発への継続的な投資と、メルセデス・ベンツのような高級ブランドによる実用的なメリットの実証により、スマートガラスは今後も自動車業界の競争環境における重要な機能であり続けるでしょう。

このような統合は、快適性と効率性を求める消費者の需要に応えるだけでなく、より広範な環境・持続可能性の目標にも合致し、市場を牽引する乗用車の役割をさらに強固なものにしています。

欧州が市場で最速の成長率が見込まれる

高級車に対する需要は、特にパンデミック後、近年この地域全体で急増しています。この成長の原動力となっているのは、従来の機能から、サンルーフや自動着色ガラスといった高度な利便性機能へと大きくシフトしていることです。この動向は、自動車における快適性と高級感の向上に対する消費者の嗜好の高まりと一致しています。

欧州の主要市場における乗用車販売台数の増加、高級車の販売台数の増加、自動車のサンルーフに対する嗜好の高まりなど、いくつかの重要な要因が市場の成長を後押ししています。ドイツの自動車部門は数十年にわたり欧州産業の屋台骨を支え、ハイテク自動車生産と技術革新のリーダーへと発展してきました。特にドイツでは、自動車の研究開発費が60%以上純増しており、自動車用スマートガラスの需要を牽引する重要なイノベーション拠点としての役割を強調しています。例えば

- 韓国の主要化学企業であるLG化学は、ドイツの自動車部品サプライヤーであるベバストSEに切替可能なグレージングフィルムを供給する契約を獲得し、自動車用スマートガラスフィルム市場に参入しました。

- 2024年4月に発表された契約に基づき、LG Chemは自動車用サンルーフシステムの製造に使用される高度な切り替え可能ガラスフィルムをベバストに提供します。LG化学の技術が搭載されたこれらのシステムは、欧州中の自動車メーカーに供給される予定です。

マイクロソフトとフォルクスワーゲンは、2022年5月に拡張現実メガネを自動車に組み込むために協力しました。この提携は、未来のモビリティ・コンセプトの重要な要素である拡張現実をより現実に近づけることを目的としています。フォルクスワーゲンはマイクロソフトと協力し、複合現実メガネ「HoloLens 2」を移動車両で利用できるようにし、未来のモビリティを紹介します。

スマートグラスを搭載した新車の発売が相次ぎ、メーカー各社はこの分野での事業拡大を図っています。アウディ、BMW、日産、レンジローバーなどの著名な自動車メーカーは、それぞれQシリーズ、Xシリーズ、キャシュカイ、イヴォークなどの人気モデルにサンルーフオプションを提供しています。この動向は、自動車業界、特に高級車セグメントにおいて、先進的な利便性機能の重要性が高まっていることを裏付けています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- スマートガラス技術を搭載した高級車・プレミアム車の普及拡大

- 市場抑制要因

- 初期コストの高さが市場成長を抑制すると予測

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 技術タイプ別

- エレクトロクロミック

- ポリマー分散液デバイス(PDLC)

- 浮遊粒子デバイス(SPD)

- 用途タイプ別

- リア・サイドウィンドウ

- サンルーフガラス

- フロント・リアガラス

- 車両タイプ別

- 乗用車

- 商用車

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- ブラジル

- 南アフリカ

- その他の国

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Corning Inc.

- Guardian Industries

- Saint-Gobain SA

- AGP Glass

- Hitachi Chemical Co. Ltd

- Research Frontiers Inc.

- Nippon Sheet Glass Co. Ltd

- AGC Inc.

- Gentex Corporation

- Gauzy Ltd.

第7章 市場機会と今後の動向

- 車両コネクティビティやエレクトロニクスとの統合

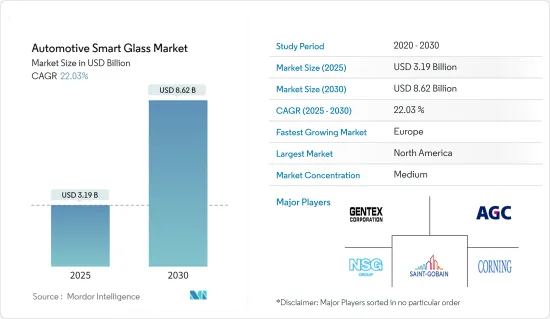

The Automotive Smart Glass Market size is estimated at USD 3.19 billion in 2025, and is expected to reach USD 8.62 billion by 2030, at a CAGR of 22.03% during the forecast period (2025-2030).

The Automotive Smart Glass Market is witnessing significant growth, driven by technological advancements and increasing consumer demand for advanced vehicle features. Smart glass, also known as switchable glass, offers functionalities such as tinting, transparency control, and heat reduction, enhancing both comfort and energy efficiency in automobiles.

Manufacturers are continually developing new materials and technologies to improve the performance and reliability of smart glass solutions. For instance, advancements in electrochromic and SPD (Suspended Particle Device) technologies have enabled faster response times, better energy efficiency, and enhanced durability of smart glass products.

Collaborations between automotive manufacturers, glass suppliers, and technology providers are also driving market expansion. Partnerships enable the integration of smart glass solutions into new vehicle models, leveraging the expertise of both glass manufacturers and automotive OEMs to meet consumer demands for advanced functionality and comfort.

Furthremore, the Automotive Smart Glass Market is poised for continued growth as automakers seek to differentiate their products with innovative features that enhance user experience, energy efficiency, and environmental sustainability. This evolution underscores the increasing importance of smart glass technologies in shaping the future of automotive design and functionality.

Automotive Smart Glass Market Trends

Rise in penetration of suspended particle devices (SPD) in vehicles

Passenger cars are driving the dominance of the Automotive Smart Glass Market, as evidenced by multiple factors and trends in the industry. In 2023, global car sales surged to approximately 65.2 million units, a significant increase from around 58.6 million in 2022. This upward trend in car sales reflects the growing demand for advanced automotive technologies, including smart glass solutions.

Suspended particle devices (SPD) are emerging as a critical innovation within the automotive sector. These devices enhance the driving experience by transforming car glass or plastic into a dynamically adjustable light-management system. This technology is particularly beneficial for sunroofs, windows, and visors, significantly improving user comfort and vehicle aesthetics.

SPD smart glasses stand out for their efficiency, consuming only 1.5 watts per square meter, compared to the 3 watts per square meter required by PDLC smart glass. This lower energy consumption translates into better fuel efficiency and reduced environmental impact. For example, Continental reports that SPD smart glass can reduce carbon dioxide emissions by 4 grams per kilometer and extend the driving range by 5.5%.

Moreover, SPD smart glass contributes to a more comfortable and luxurious driving experience by significantly reducing heat inside the vehicle. Mercedes-Benz has implemented SPD glass in high-end models like the S-class sedan and SL roadster, which has shown a reduction in interior temperature by up to 10 degrees Celsius (18 degrees Fahrenheit). This reduction not only enhances passenger comfort but also protects interior materials from premature aging caused by infrared and ultraviolet radiation.

Given the advancements in smart glass technology and its adoption by leading automotive manufacturers, passenger cars are positioned to continue their dominance in the Automotive Smart Glass Market. The ongoing investment in research and development by companies like Continental and the practical benefits demonstrated by luxury brands such as Mercedes-Benz ensure that smart glass will remain a key feature in the competitive landscape of the automotive industry.

This integration not only caters to consumer demand for comfort and efficiency but also aligns with broader environmental and sustainability goals, further solidifying the role of passenger cars in driving the market forward.

Europe is Expected to Grow at the Fastest Rate in the Market

The demand for luxury cars has surged across the region in recent years, particularly post-pandemic. This growth is driven by a significant shift from traditional features towards advanced convenience features, such as sunroofs and automatic tinted glass. This trend aligns with the increasing consumer preference for enhanced comfort and luxury in vehicles.

Several key factors are propelling the market's growth, including a rise in passenger car sales in major European markets, increasing sales of luxury cars, and a growing preference for vehicle sunroofs. The German automotive sector has been the backbone of the European industry for decades, evolving into a leader in high-tech automotive production and innovation. Notably, Germany has seen a net growth of over 60% in automotive R&D, highlighting its role as a critical innovation hub driving the demand for automotive smart glass. For instance,

- LG Chem Ltd., a leading South Korean chemical company, has entered the automotive smart glass film market by securing a contract to supply switchable glazing films to German auto parts supplier Webasto SE.

- Under the agreement announced in April 2024, LG Chem will provide its advanced switchable glass films to Webasto for use in manufacturing automotive sunroof systems. These systems, equipped with LG Chem's technology, will be supplied to car manufacturers across Europe.

Microsoft and Volkswagen collaborated to integrate augmented reality glasses into vehicles in May 2022. This partnership aims to bring augmented reality, a key element of future mobility concepts, closer to reality. Volkswagen has worked with Microsoft to make the HoloLens 2 mixed-reality glasses available in mobile vehicles, showcasing the future of mobility.

The market is further encouraged by several new car launches featuring smart glass, prompting manufacturers to expand their operations in this segment. Prominent car manufacturers like Audi, BMW, Nissan, and Range Rover are offering sunroof options in popular models such as the Q-series, X-series, Qashqai, and Evoque, respectively. This trend underscores the growing importance of advanced convenience features in the automotive industry, particularly within the luxury car segment.

Automotive Smart Glass Industry Overview

The automotive smart glass market is moderately consolidated, with a few major players such as Saint Gobin, AGC Inc., Nippon Sheet Glass Co. Ltd., Gentex Corporation, and Cornering Inc. having significant shares in the market due to their well-established and developed products among various automakers. The companies are focusing on innovative technologies and following strategies, like acquisition, licensing the technology, and partnership, to expand, sustain, and capture the potential demand for rapid adoption of technological trends in the automotive industry. For instance,

- In January 2023, Asahi India Glass partnered with Enormous Brands to create impactful brand films for AIS Windows, its doors and windows solutions brand. This move comes as the Indian system windows and doors market evolves, driven by changing lifestyles, urbanization, and smart city construction. AIS Windows caters to customer preferences with a range of aluminum and uPVC framing materials and diverse glass solutions, positioning itself to significantly impact the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rising Adoption Of Luxury And Premium Vehicles Equipped With Smart Glass Technologies

- 4.2 Market Restraints

- 4.2.1 High Initial Cost Is Anticipated To Restrain The Market Growth

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value USD Million)

- 5.1 By Technology Type

- 5.1.1 Electrochromic

- 5.1.2 Polymer Dispersed Liquid Device (PDLC)

- 5.1.3 Suspended Particle Device (SPD)

- 5.2 By Application Type

- 5.2.1 Rear and Side Windows

- 5.2.2 Sunroof Glass

- 5.2.3 Front and Rear Windshield

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 Brazil

- 5.4.4.2 South Africa

- 5.4.4.3 Other Countries

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Corning Inc.

- 6.2.2 Guardian Industries

- 6.2.3 Saint-Gobain SA

- 6.2.4 AGP Glass

- 6.2.5 Hitachi Chemical Co. Ltd

- 6.2.6 Research Frontiers Inc.

- 6.2.7 Nippon Sheet Glass Co. Ltd

- 6.2.8 AGC Inc.

- 6.2.9 Gentex Corporation

- 6.2.10 Gauzy Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Integration with Vehicle Connectivity and Electronics