|

市場調査レポート

商品コード

1920864

医薬品受託製造市場(第5版):2035年までの動向と予測 - 製品タイプ別、原薬タイプ別、原薬効力別、FDF別、剤形別、経口固形剤別、エンドユーザー別、地域別、主要企業別Pharmaceutical Contract Manufacturing Market (5th Edition): Trends and Forecast Till 2035 - Distribution by Type of Product Manufactured, Type of API, API Potency, FDF, Dosage Form, Oral Solid, End User, Geographical Regions and Key Players |

||||||

カスタマイズ可能

|

|||||||

| 医薬品受託製造市場(第5版):2035年までの動向と予測 - 製品タイプ別、原薬タイプ別、原薬効力別、FDF別、剤形別、経口固形剤別、エンドユーザー別、地域別、主要企業別 |

|

出版日: 2026年01月23日

発行: Roots Analysis

ページ情報: 英文 545 Pages

納期: 即日から翌営業日

|

概要

医薬品受託製造市場:概要

Roots Analysisの調査によると、医薬品受託製造の市場規模は、2035年までの予測期間においてCAGR 4.5%で成長し、現在の1,003億米ドルから2035年までに1,554億米ドルに達すると推定されています。

医薬品受託製造市場:成長と動向

受託製造とは、特定の開発および/または生産業務を外部サービスプロバイダーに委託することを指します。これは、ある企業が別の企業のラベルやブランドを使用して製品を開発することを意味します。製薬企業によって最も頻繁に委託される業務には、製剤設計、剤形開発、臨床/商業生産、包装、物流などが含まれます。

興味深いことに、現代の医薬品候補パイプラインはますます複雑化しており、専門的な施設、設備、および運用知識が必要とされています。慢性疾患に罹患する人々の数も大幅に増加しており、革新的な医薬品への継続的な需要が生じています。この増加する需要に対応するため、様々な中小規模の企業や一部の大手製薬会社は、生産活動を受託サービスプロバイダーにアウトソーシングし始めています。技術開発と革新的な治療法に対する市場のニーズも、その発展を継続させています。

特筆すべきは、CMO(受託製造機関)がカスタム治療法、継続的製造プロセス、デジタルヘルス統合技術の導入を通じて新たな動向に適応している点です。イノベーション、持続可能性、チームワークの採用により、製薬CMOは医療分野に大きな影響を与え、今後数年間で顕著な成長を遂げると見込まれます。

成長の促進要因:市場拡大の戦略的基盤

バイオ医薬品、モノクローナル抗体、ADC(抗体薬物複合体)やGLP-1薬剤などの新規治療法に対する需要の高まりが、高度な能力を有する専門CMOへのアウトソーシングを促進しています。さらに、主要バイオ医薬品の特許切れや先発医薬品の価格設定課題により、製薬企業は費用対効果の高い受託製造戦略を追求せざるを得ません。加えて、慢性疾患の増加率と新薬への需要が、拡張可能な製造能力と迅速な市場投入を実現するCMOへの依存度を高めています。

市場の課題:進展を阻む重大な障壁

医薬品受託製造市場は、FDAやEMAなどの規制当局による厳格な規制遵守や、生産技術のコスト上昇など、成長を阻害する重大な障壁に直面しています。これらの障壁は、受託製造業者に高いコンプライアンス費用を負担させています。さらに、世界の貿易不安定化が原薬(API)や原材料のサプライチェーンを混乱させ、米国や欧州における価格圧力が高まることで、コスト管理上の課題が深刻化しています。

医薬品受託製造市場:主要な知見

当レポートは、医薬品受託製造市場の現状を詳細に分析し、業界内の潜在的な成長機会を特定しています。主な調査結果は以下の通りです:

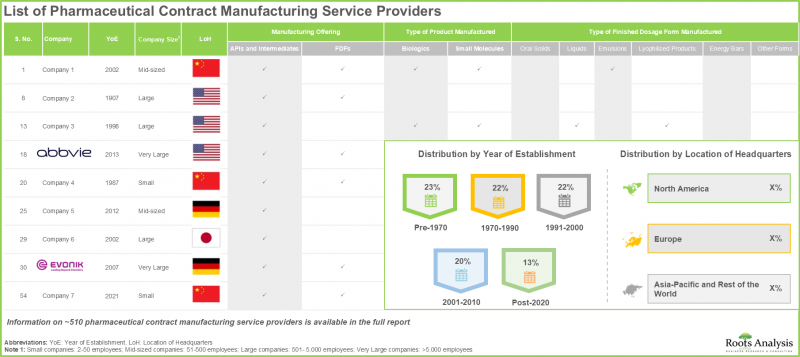

- 現在の市場情勢では、世界中で医薬品受託製造サービスを提供すると主張する約510社の企業が存在しており、その50%はアジア太平洋地域に本社を置いています。

- 医薬品受託製造企業の大半(約90%)が最終剤形調製サービスの提供を行っており、さらに75%以上の企業が充填・包装・ラベリングサービスを提供しています。

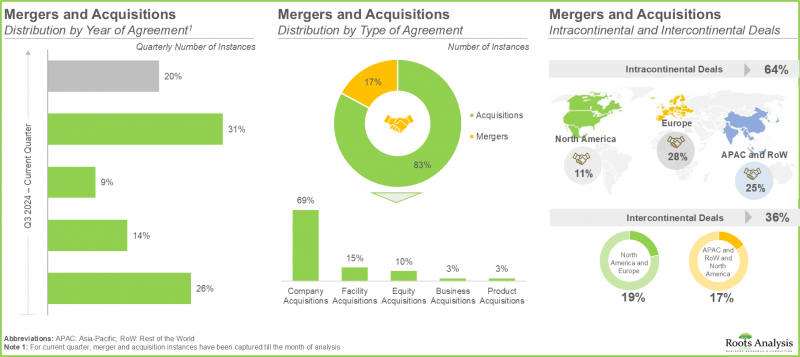

- M&Aにより、企業はワンストップショップとしての地位を確立し、絶えず進化する市場情勢において競争優位性を構築することが可能となります。

- 低分子医薬品に対する需要の高まりに対応するため、CMOは既存の生産能力と技術力の拡充に多額の投資を行ってきました。最近では、この動向が欧州で最も顕著に見られます。

- 世界の医薬品受託製造能力は、世界各地の様々な施設に均等に分散しています。特に、大規模および超大規模の企業が総生産能力の85%以上を占めています。

- 自社生産施設の設立・維持に伴う高額な設備投資や運営コストを削減するため、医薬品受託製造の需要は大幅に増加すると予想されます。

- 現在、医薬品受託製造市場シェアの大部分は北米が占めております。これは、先進的な医療インフラが整備されており、各社が広範な調査を実施できることに起因するものでございます。

- 経口固形剤サブセグメントは、その費用対効果、投与の容易さ、および患者の高いコンプライアンスにより、今年度は市場全体の大部分を占めると推定されています。

- 北米は医薬品受託製造市場全体において大きなシェアを占めると予想されており、この動向は今後も変わらない見込みです。

- 米国における医薬品受託製造市場は、CAGR 4.3%で成長すると予測されています。これは低分子化合物の需要増加に伴い、高度な製造能力の必要性が高まっているためです。

- 低分子化合物の需要増加に加え、合併・買収や事業拡大の動きが活発化していることから、医薬品CMO市場は今後数年間で大幅な成長を遂げると見込まれます。

医薬品受託製造市場

市場規模および機会分析は以下のパラメータ別に分類されています:

製造製品タイプ別

- 原薬(API)及び中間体

- FDF(完成医薬品)

原薬タイプ別

- 先発医薬品用API

- ジェネリックAPI

原薬効力別

- 低効力API

- 高効力API

FDFタイプ別

- 先発品FDF

- ジェネリックFDF

剤形別

- 経口固形剤

- 液剤

- エマルジョン

- その他の剤形

経口固形剤タイプ別

- 錠剤

- カプセル

- その他

提供される包装タイプ別

- 瓶

- ブリスター包装

- バイアル

- プレフィルドシリンジ

- カートリッジ

- アンプル

- 経口液剤用ボトル

- その他

事業規模別

- 臨床

- 商業

エンドユーザー別

- 小規模

- 中規模

- 大企業および超大企業

地域別

- 北米

- 米国

- カナダ

- 欧州

- ベルギー

- スイス

- 英国

- ドイツ

- アイルランド

- オランダ

- イタリア

- フランス

- スウェーデン

- その他欧州

アジア太平洋地域およびその他の地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域およびその他の国々

医薬品受託製造市場:主要セグメント

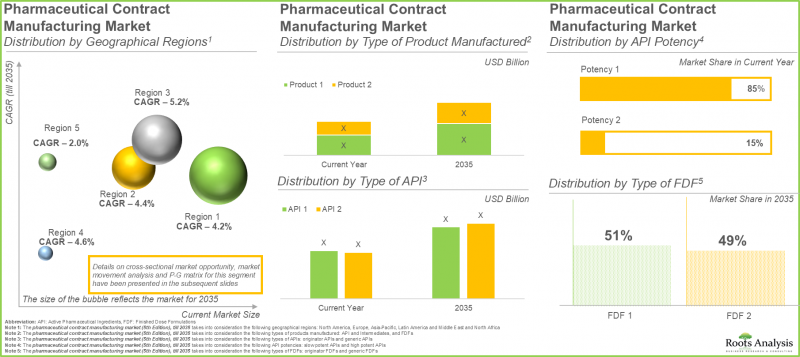

低効力APIの製造が医薬品受託製造市場を主導

現在、低効力APIは市場全体の85%を占めております。これは主に、その大規模な製造と拡張性のある製造方法によるものです。加えて、これらのAPIは、糖尿病や感染症など様々な疾患の治療に製薬企業によって利用されております。この広範な利用により、世界的に持続的に高い需要が生じております。特に、高効力APIのセグメントはより速いペースで拡大すると予想されます。標的治療や精密医療への需要増加がこの拡大を後押ししており、これらの治療法は強力な治療効果により、最小限の投与量でも非常に効果的であることが証明されているためです。

医薬品受託製造分野では経口固形製剤が圧倒的な需要で主導

経口固形製剤製造分野は、医薬品受託製造市場における総収益の約55%を占めております。これは、低コスト、患者様にとっての利便性、大量生産における効率性によるものです。今後、予測期間を通じて、医薬品受託製造市場において液剤カテゴリーがより大きな成長を示すと予想されております。

北米が医薬品受託製造分野を主導

北米は医薬品受託製造市場をリードし、総収益の約45%を占めております。高度に発達した製薬セクター、強固な規制システム、そして確立された世界の大手製薬企業の存在が、この地域における医薬品受託製造業者への需要を牽引しております。

医薬品受託製造市場における代表的な参入企業

- Albemarle

- Aspen Pharmacare

- Bausch Health Sciences

- Catalent

- Delpharm

- Eurofins Scientific

- Evonik Industries

- Fareva

- Fresenius Kabi

- Intas Pharmaceuticals

- Lonza

- Micro Labs

- Nipro Patch

- Patheon

- PiSA Farmaceutica

- Recipharm

- Sandoz

- West Pharmaceutical Services

- Wockhardt

- WuXi AppTec

医薬品受託製造市場:調査範囲

- 市場規模と機会分析:当レポートでは、医薬品受託製造市場について、主要市場セグメンテーションに焦点を当てた詳細な分析を掲載しています。対象セグメントには、[A]製品タイプ、[B]原薬タイプ、[C]原薬効力、[D]FDFタイプ、[E]剤形、[F]経口固形剤タイプ、[G]提供される包装タイプ、[H]事業規模、[I]エンドユーザー、[J]地理的地域といった主要市場セグメントに焦点を当てた詳細な分析を提供しております。

- 市場情勢:低分子医薬品向け受託製造サービスを提供する企業の現状について、詳細な概要を提示します。これには、[A]設立年、[B]製造施設の所在地、[C]提供サービスタイプ、[D]製造する医薬品タイプ、[E]事業規模、[F]提供サービスタイプ、[G]製造する最終剤形タイプ、[H]提供される包装タイプ。

- 企業プロファイル:ペプチド治療薬製造市場に参入している北米、欧州、アジア太平洋地域の主要企業について、[A]設立年、[B]本社所在地、[C]製品ポートフォリオ、[D]最近の動向、[E]将来展望に基づく詳細なプロファイル。

- 自社製造か外部委託かの判断基準:医薬品開発企業が自社製品を自社製造するか、CMO(受託製造機関)のサービスを利用するかを決定する際に考慮すべき様々な要素を強調した定性分析。

- 合併・買収(M&A):本分野における様々な合併・買収を、[A]合意年、[B]合意形態、[C]地域、[D]最も活発な参入企業(合意件数ベース)、所有権変更マトリックス、買収合意の主要価値ドライバーなど、複数の関連パラメータに基づき詳細に分析します。

- 最近の拡張動向:医薬品受託製造分野における拡張事例の詳細な分析。拡張時期、拡張状況、拡張形態、施設所在地、投資額、製造医薬品種類、提供サービス形態、主要参入企業といった関連パラメータに基づく分析。

- 地域別生産能力分析:北米、欧州、アジア太平洋、世界のその他の地域(ROW)における医薬品受託製造施設の地域別生産能力の詳細な分析。

- 生産能力分析:公開情報に基づき、利害関係者から報告されたデータをもとに、医薬品製造の総設備能力を推定します。利用可能な生産能力の分布を、[A]製造業者規模(小規模、中規模、大規模および超大規模)および[B]地域(北米、欧州、アジア太平洋、世界のその他の地域)に基づいて明らかにします。

- 需要分析:低分子医薬品の年間需要に関する情報に基づいた推定値を、[A]操業規模、[B]原薬タイプ、[C]原薬の効力、[D]地理的地域といった複数の関連パラメータにわたって提示します。

- 市場影響分析:世界の医薬品受託製造市場の成長に影響を与え得る要因に関する詳細な分析です。また、[A]主要な促進要因、[B]潜在的な制約要因、[C]新たに生じつつある機会、[D]既存の課題の特定と分析も特徴としています。

目次

第1章 序文

第2章 調査手法

第3章 市場力学

第4章 マクロ経済指標

第5章 エグゼクティブサマリー

第6章 イントロダクション

- 章の概要

- サードパーティメーカータイプ

- 医薬品受託製造の概要

- 医薬品受託製造の進化

- 製薬業界におけるアウトソーシングの必要性

- 医薬品受託製造業界の最近の動向

- 契約製造組織が提供するサービス

- 契約製造組織を選択する際に考慮すべき重要な点

- 医薬品製造業務のアウトソーシングに伴うリスクと課題

- 将来の展望

第7章 医薬品受託製造組織:規制状況

- 章の概要

- 北米の規制状況

- 欧州の規制状況

- アジア太平洋と世界のその他の地域における規制状況

- 規制当局からの承認取得状況別医薬品受託製造組織の分析

- 規制状況:地域ベンチマーク分析

第8章 医薬品受託製造組織:市場情勢

- 章の概要

- 医薬品受託製造組織:市場情勢

第9章 企業プロファイル主要参入企業

- 章の概要

- 北米の医薬品受託製造機関

- Albemarle

- Bausch Health Services

- Catalent

- Patheon

- PiSA Farmaceutica

- West Pharmaceutical Services

- 欧州の医薬品受託製造機関

- Delpharm

- Eurofins Scientific

- Evonik Industries

- Fareva

- Fresenius Kabi

- Lonza

- Recipharm

- Sandoz

- アジア太平洋およびその他の地域の医薬品受託製造機関

- Aspen Pharmacare

- Intas Pharmaceuticals

- Micro Labs

- Nipro Patch

- WuXi AppTec

- Wockhardt

第10章 製造か購入かの意思意思決定の枠組み

- 章の概要

- 前提と主要なパラメータ

- 医薬品受託製造業者:製造か購入かの意思決定

- 結論

第11章 合併と買収

- 章の概要

- 合併と買収タイプ

- 医薬品受託製造組織:合併と買収

第12章 最近の拡張

- 章の概要

- 拡張タイプ

- 医薬品受託製造組織:最近の拡大

第13章 地域能力分析

- 章の概要

- 前提と主要なパラメータ

- 医薬品受託製造施設の全体像