ダイアタッチ装置:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Die Attach Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1643098

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

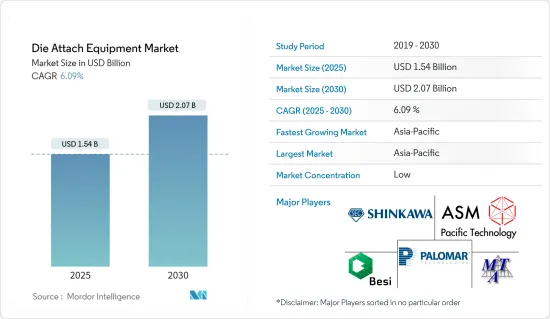

ダイアタッチ装置市場規模は2025年に15億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.09%で、2030年には20億7,000万米ドルに達すると予測されています。

成長の原動力となっているのは、モノのインターネット(IoT)機器における積層ダイ技術の利用拡大です。最近の動向では、医療、軍事、フォトニクス、ワイヤレスエレクトロニクスなどの新興と既存用途により、ハイブリッド回路の需要は堅調に推移しています。

主要ハイライト

- C2Wハイブリッド接合は、Cu-Cuの直接接合を可能にし、3Dスタックドメモリやハイエンドロジック用途のTCBを置き換えることができる有望な新技術です。しかし、C2Wハイブリッド接合はまだ初期段階にあります。2.5D構造のロジックデバイス向けには2022~23年に市場に登場し、装置市場の成長を大きく後押しすると期待されています。

- AuSn共晶ダイアタッチ技術の需要が市場を牽引します。従来は、金属充填導電性エポキシ、高鉛含有はんだ、金シリコンはんだなど、さまざまなダイアタッチ製品でチップを実装し、デバイスの寿命まで確実に機能させることができました。

- しかし、発熱の増加傾向、デバイスの小型化要求、RoHSやREACHの制定、GaAsチップへの移行により、従来の材料の使用は制限されました。デバイスの高信頼性への要求から、技術者はダイの取り付けに様々な新しい材料を評価するようになりました。

- 提案されたはんだプリフォームは共晶金-錫で、Palomar Technologiesのダイボンダーを使用して、大量生産または実験室での採用が可能です。この装置は、基板、共晶金錫プリフォーム、コンポーネントの高精度なピックアンドプレース、共晶ダイアタッチ、コンピュータ制御のパルスヒートステージ(PHS)を使用したパルスヒートリフローなど、完全なダイアタッチプロセスに対応できます。

- ディスクリートパワーデバイスの需要が市場を牽引しています。従来のワイヤ接合やリボン接合に代わるものとして、銅クリップの人気が高まっています。ダイアタッチ機能は、ディスクリートパワーコンポーネントの包装ソリューションの特徴です。ワイドバンドギャップ半導体ダイ技術(SiCとGaN)の採用は、銀焼結ダイアタッチ(材料にはエポキシ成形コンパウンドと相互接続材料が含まれる)を含む新しい革新的な包装ソリューションをもたらします。

- EV/HEV用途におけるディスクリートSiCからSiCモジュールへの漸進的な移行、組み込みダイ包装システム、マルチチップシステムにおけるGaNデバイスの統合は、このような動向のほんの一例に過ぎません。このため、ディスクリートパワーデバイス用のダイアタッチ装置の需要が高まっている

- しかし、主に加工中の寸法変化や耐用年数、装置を通した加工中の可動部品の機械的アンバランスが、装置の機能性に課題をもたらし、市場を抑制する可能性があります。

ダイアタッチ装置市場の動向

LEDが大きく成長

- ダイアタッチ材料は、中・高・超高出力LEDの性能と信頼性の鍵を握る。ダイアタッチ装置の需要は、LED普及率の上昇に伴って増加しています。特定のチップ構造と用途に適したダイアタッチ材料の選択は、包装プロセス(スループットと歩留まり)、性能(放熱出力と光出力)、信頼性(ルーメン維持)、コストなど、さまざまな考慮事項によって決まる。共晶金錫、銀入りエポキシ、はんだ、シリコーン、焼結材料はすべて、LEDのダイアタッチに使用されてきました。

- 例えば、SFEはエポキシ接着剤による接着方法を提供しており、LEDエポキシダイボンダーマシンは0.2秒/サイクル(90%の動作率)のインデックスタイム、250*250規格のチップサイズを特徴とし、2台のカメラによるリードフレーム認識を記載しています。そのソフトウェア機能は、自動マウントレベルとピックアップレベルのティーチング機能を記載しています。

- さらに、導電性接着剤(主に銀入りエポキシ)は、LEDの最も広範な熱ダイアタッチ材料(ユニット数)を構成しています。これらは既存の後プロセス包装装置と互換性があり、魅力的なコスト/性能バランス(通常、二次リフロー互換性で最大50W/mKの熱)を記載しています。ベアシリコンに固着するため、GaN on Siliconのようなバックエンドのメタライゼーションのないダイに最も好まれる材料です。

- さらに、LED市場には多くのライバルや競合他社が存在するが、ASMはこの市場で著名な参入企業の1つであり、同社のLEDエポキシ高速ダイボンダーAD830はLED市場を独占しています。より多くの国が従来の電球を廃止しようとしている中、LEDは市場のトップへの道を歩み続けています。Joint Research Centerによると、売上高によるLEDの普及率は上昇しており、2025年には75.8%の普及率に達すると予想されています。このことがダイアタッチ装置市場の需要を高めています。

- さらに、2022年9月、Palomar Technologiesは、2022 military+Aerospace electronics Innovation Awardを受賞した新型ダイボンダ3880-IIを発表しました。この新型機には、生産性を最大化し、プログラミング時間を最大95%短縮し、ボンダー全体の生産性を向上させるオプションが含まれています。

アジア太平洋が市場の大幅成長を占める

- アジア太平洋は、ダイアタッチ装置産業の著しい成長を占めています。世界中に存在するOSAT(Outsourced Semiconductor Assembly And Test)企業の60%以上がアジア太平洋に本社を置いています。これらのOSAT企業は、半導体製造プロセスでダイアタッチ装置を使用しています。さらに、同地域ではIDM(集積デバイス製造業者)の数が増加しており、間もなく市場成長を押し上げると予想されます。

- 中国と台湾では、スマートフォン、ウェアラブル端末、白物民生用電子機器などの電子製品の大量生産に、オプトエレクトロニクス、MEMS、MOEMSなど複数のデバイスが使用されています。これらのデバイスはすべて、部品の組み立てプロセスでダイアタッチ装置を必要とします。

- さらに、韓国、中国、主に日本の高齢者は、予測期間中に医療サービスの必要性を加速させると予想され、人工呼吸器、透析、MEMS圧力センサを構成する血圧モニタリング装置などのデバイスに余地を与えています。ESCAPは、この地域の60歳以上の高齢者は、現在の9.55人から2025年には10.64人に増加し、2050年には18.44人に増加すると予測しており、これは世界人口の60%を占めます。MEMS圧力センサのダイアタッチ装置の需要により、同市場の成長に貢献しています。

- さらに、インドでは政府の取り組みにより、多くのスマートシティが成長しており、モニタリング、メンテナンス、モニタリングなどの目的で電子ソリューションを取り入れることが期待されています。smartcities.gov.inによると、中央政府はこのような60のスマートシティの開発に9億7,700万米ドルを割り当てています。これは、より多くのCMOSイメージセンサの需要につながり、市場の成長をさらに後押ししています。

- ハイパワーレーザは、切断、溶接、加工を含む幅広い用途の産業セグメントで幅広い需要を見出しています。企業は、高性能と信頼性を活用するためにレーザ技術に移行しています。レーザダイオードの進歩は、エポキシや共晶接合の技術を加工する装置の需要を大幅に増加させています。

- IoT、AI、ADASの開発により、さらなるメモリ需要の増加が見込まれます。そのため、メモリチップ製造の生産性向上や後プロセスのデバイス信頼性向上が従来以上に求められます。これに対処するため、2022年8月、スタンフォード大学のエンジニアは、より効率的で柔軟なAIチップを作成し、メモリ製造におけるスループットと信頼性の向上に貢献する小さなエッジデバイスにAIの力をもたらす可能性があります。

ダイアタッチ装置産業概要

ダイアタッチ装置市場は、地場企業と世界参入企業の存在が市場の激しい競争を浸透させるため、セグメント化されています。さらに、各社は開発や提携を通じてスループットや歩留まりといった装置性能の向上に注力しており、市場競争は激化しています。主要参入企業は、Be Semiconductor Industries N.V.、ASM Pacific Technology Limited、Palomar Technologies Incなどです。

- 2022年10月、Hermetic Solutions Group(HSG)はRHP TechnologiesからDiaCoolの知的財産を取得しました。これにより、HSGの製品ラインナップが拡大し、顧客は長年にわたり、より多くの選択肢を得ることができます。HSGのヒートシンク、ダイタブ、ヒートスプレッダ用DiaCoolダイヤモンド複合材料は、従来のラミネートやMMC材料に比べ、顧客に大きな利点を記載しています。

- 2022年10月、Kulicke and Soffaは熱圧着ソリューションで複数の新規受注を獲得し、主要顧客への初のフラックスレス熱圧着ボンダー(TCB)の出荷に成功し、先進的なLEDアセンブリーでの地位を継続しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- AuSn共晶ダイアタッチ技術の需要拡大

- ディスクリートパワーデバイスの需要

- 著しい成長を遂げるLEDセグメント

- 市場抑制要因

- 加工中と耐用年数中の寸法変化と機械的アンバランス

- 産業バリューチェーン分析

- 産業の魅力-ファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場セグメンテーション

- タイプ

- ダイボンダー

- フリップチップボンダー

- 接合技術

- エポキシ

- 共晶

- ソフトソルダー

- ハイブリッド接合

- その他の接合技術

- 用途

- メモリー

- RF &MEMS

- LED

- CMOSイメージセンサ

- ロジック

- オプトエレクトロニクス/フォトニクス

- その他

- 地域

- 北米

- 欧州

- アジア

- オーストラリアとニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- Palomar Technologies, Inc.

- Shinkawa Ltd.

- MicroAssembly Technologies, Ltd.

- ASM Pacific Technology Limited

- Be Semiconductor Industries N.V.

- Kulicke and Soffa Industries, Inc.

- Dr. Tresky AG

- Fasford Technology Co Ltd.

- Inseto UK Limited

- Anza Technology Inc.

第7章 投資分析

第8章 市場機会と今後の動向

目次

The Die Attach Equipment Market size is estimated at USD 1.54 billion in 2025, and is expected to reach USD 2.07 billion by 2030, at a CAGR of 6.09% during the forecast period (2025-2030).

Growth is fueled by the increased use of stacked die technology in the Internet of Things (IoT) devices. In recent trends, the demand for hybrid circuits has remained strong due to emerging and existing applications in medical, military, photonics, wireless electronics, etc.

Key Highlights

- C2W hybrid bonding is a promising emerging technology that can enable direct Cu- Cu bonding and replace TCB for 3D stacked memory and high-end logic applications. However, C2W hybrid bonding is still in its early stages level. It is expected to hit the market in 2022/23 for logic devices with 2.5D structures, significantly assisting the equipment market's growth.

- The demand for the AuSn Eutectic Die-Attach technique drives the market. Traditionally, various die-attach products, which include metal-filled conductive epoxies, high lead-containing solders, and gold-silicon solders, were sufficient to mount the chip and have it perform reliably for the life of the device.

- However, the trend towards increasing heat generation, demand for compact devices, enactment of RoHS and REACH legislation, and the transition to GaAs chips limited the use of conventional materials. The demand for high device reliability has led engineers to evaluate various new materials for their die attachment.

- The suggested solder preforms are eutectic gold-tin and can be implemented for high volume or lab quantity adoption using a Palomar Technologies' die bonder. This equipment can handle the complete die-attach process, including high-accuracy pick-and-place of substrates, eutectic gold-tin preforms, and components; eutectic die-attach; and pulsed-heat reflow using a computer-controlled Pulse Heat Stage (PHS).

- The demand for discrete power devices drives the market. Copper clips are becoming increasingly popular as an alternative to traditional wire and ribbon bonding. Die-attach functionality is a feature of packaging solutions for discrete power components. The adoption of wide-bandgap semiconductor die technologies (SiC and GaN) brings new innovative packaging solutions, including silver sintering die-attach (materials include epoxy molding compounds and interconnection materials).

- The progressive transition from discrete SiC towards SiC modules in EV/HEV applications, the embedded-die packaged systems, and the integration of GaN devices in multichip systems are just a few examples of such a trend. This factor enhances the demand for the die attaches equipment for the discrete power devices.

- However, primarily dimensional changes during processing and service life and mechanical unbalance of moving parts during processing through equipment challenges the equipment's functionality which could restrain the market.

Die Attach Equipment Market Trends

LED to Witness Significant Growth

- Die attach material is key in the performance and reliability of mid, high, and super-high power LEDs. The demand for die-attach equipment is increasing with an increasing LED penetration rate. The selection of suitable die-attach material for a particular chip structure and application depends on various considerations, which include the packaging process (throughput and yield), performance (thermal dissipation output and light output), reliability (lumen maintenance), and cost. Eutectic gold-tin, silver-filled epoxies, solder, silicones, and sintered materials have all been used for LED die attach.

- For instance, SFE provides an Epoxy Adhesive bonding method where its LED Epoxy Die Bonder machine features an index time of 0.2 Sec /Cycle (90 Percent Rate of Operation) with a chip size of 250 * 250 standards, providing lead frame recognition through 2 Cameras. Its software function provides auto mount level & pick-up level teaching functions.

- Further, conductive adhesives (mostly silver-filled epoxies) constitute LEDs' most extensive thermal die-attach materials (by unit number). They are compatible with existing back-end packaging equipment and provide an attractive cost/performance balance (typically up to 50 W/mK thermals with secondary reflow compatibility). As they stick to bare silicon, they are the most preferred material for dies without back-end metallization like GaN on silicon.

- Further, in the LED market, there are a lot of rivals or competitors, and ASM is one of the prominent players in this market, and its LED Epoxy High speed die bonder AD830 dominates in the LED market. As more and more countries are getting close to phasing out conventional bulbs, LEDs are continuing their march to the top of the market. According to Joint Research Center, The penetration rate of LEDs based on sales is raising and is expected to reach a penetration rate of 75.8 % by 2025. This factor enhances the demand for the die attaches equipment market.

- Furthermore, in September 2022, Palomar Technologies launched a new 3880-II die-bonder, which won the 2022 military+Aerospace electronics Innovation Award. This new machine includes options to maximize productivity, reduce programming time by up to 95% and improve overall bonder productivity.

Asia-Pacific Accounts for Significant Market Growth

- Asia-Pacific accounted for the significant growth of the die-attach equipment industry. More than 60% of OSAT (Outsourced Semiconductor Assembly And Test) players present across the world have their headquarters in the APAC region. These OSAT companies use die-attach equipment in the semiconductor fabrication process. Additionally, an increasing number of IDMs (Integrated Device Manufacturers) in the region is expected to boost the market growth shortly.

- In China and Taiwan, the mass production of electronic products, including smartphones, wearables, and white goods, uses several devices, such as optoelectronics, MEMS, and MOEMS. All these devices require die-attach equipment in the assembly process of these components.

- Further, South Korea, China, and mostly Japan's old age population are anticipated to accelerate the need for healthcare services during the forecast period, thus providing scope for devices, such as ventilators, dialysis, and blood pressure monitoring devices constituting MEMS pressure sensors. ESCAP estimates that the geriatric population in the region, aged 60 years and older, could penetrate at the rate of 10.64 by 2025 with 9.55 in the current year and raise to 18.44 by 2050, which represent 60 percent of the worlds population. The instance caters to the growth of the market due to the demand for die-attach equipment for MEMS pressure sensor.

- Furthermore, India is also witnessing growth in a number of smart cities, due to government initiatives and are expected to incorporate electronic solutions for purposes, such as surveillance, maintenance, monitoring, etc. According to smartcities.gov.in, the central government has allotted USD 977 million into the development of 60 such smart cities. This leads to the demand for a higher number of CMOS image sensors, which further supports the market growth.

- High Power lasers are finding extensive demand in industrial sectors for a wide range of applications, including cutting, welding, and fabrication. Companies are moving towards Laser technologies to take advantage of high performance and reliability. The advancement in laser diode significantly increases the demand for equipment, which processes the technique of Epoxy and Eutectic bonding.

- Further memory demand is expected to increase with the development of IoT, AI, and ADAS. As a result, productivity improvement in memory chip manufacturing and improvement of post-processing device reliability will be required more than in the past. To address this, in August 2022, Stanford engineers created a more efficient and flexible AI chip, which could bring the power of AI into tiny edge devices that contributes to improved throughput and reliability in memory production.

Die Attach Equipment Industry Overview

The die-attach equipment market is fragmented as the presence of local and global players penetrates the intense rivalry in the market. Further, players are focusing on improving their equipment performance in terms of throughput and yield through development and partnership, making the market more competitive. Key players are Be Semiconductor Industries N.V., ASM Pacific Technology Limited, Palomar Technologies Inc, etc. Recent developments in the market are -

- In October 2022, Hermetic Solutions Group (HSG) acquired the Intellectual property of DiaCool, from RHP Technologies. This expands HSG's product lineup and offers customers significantly more options for many years. HSG's DiaCool diamond composite material for heat sinks, die tabs, and heat spreaders provide customers with significant advantages over conventional laminate or MMC materials.

- In October 2022, Kulicke and Soffa received multiple new purchase orders for its thermo-compression solution and successfully shipped its first Fluxless Thermo-Compression Bonder (TCB) to a key customer and continues its position in the advanced LED Assembly.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand of AuSn Eutectic Die-Attach Technology

- 4.2.2 Demand of Discrete Power Devices

- 4.2.3 LED Segment to Witness Significant Growth

- 4.3 Market Restraints

- 4.3.1 Dimensional Changes During Processing and Service Life and Mechanical Unbalance

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Die Bonder

- 5.1.2 Flip Chip Bonder

- 5.2 Bonding Technique

- 5.2.1 Epoxy

- 5.2.2 Eutectic

- 5.2.3 Soft Solder

- 5.2.4 Hybrid Bonding

- 5.2.5 Other Bonding Techniques

- 5.3 Application

- 5.3.1 Memory

- 5.3.2 RF & MEMS

- 5.3.3 LED

- 5.3.4 CMOS Image Sensor

- 5.3.5 Logic

- 5.3.6 Optoelectronics / Photonics

- 5.3.7 Other Applications

- 5.4 Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia

- 5.4.4 Australia and New Zealand

- 5.4.5 Latin America

- 5.4.6 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Palomar Technologies, Inc.

- 6.1.2 Shinkawa Ltd.

- 6.1.3 MicroAssembly Technologies, Ltd.

- 6.1.4 ASM Pacific Technology Limited

- 6.1.5 Be Semiconductor Industries N.V.

- 6.1.6 Kulicke and Soffa Industries, Inc.

- 6.1.7 Dr. Tresky AG

- 6.1.8 Fasford Technology Co Ltd.

- 6.1.9 Inseto UK Limited

- 6.1.10 Anza Technology Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日