|

市場調査レポート

商品コード

1689886

ワークフローオートメーション:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Workflow Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ワークフローオートメーション:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

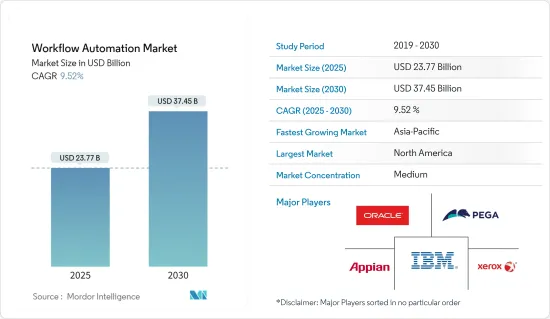

ワークフローオートメーション市場規模は2025年に237億7,000万米ドルと推定され、2030年には374億5,000万米ドルに達すると予測され、予測期間(2025年~2030年)のCAGRは9.52%です。

ワークフローの概念は、製造業やオフィスにおけるプロセスの概念から発展したものであり、そのようなプロセスは工業化の時代から存在し、作業活動のルーチンな側面に集中することで効率を急上昇させることを追求した結果です。プロセスは通常、作業活動を明確に定義されたタスク、ルール、役割、手順に分離し、製造業やオフィスワークの大部分を規制します。当初、工程はすべて人間が物理的な物体を操作して行っていました。

主なハイライト

- 情報技術の導入により、職場のプロセスは部分的または全体的に情報システムによってオートメーションされ、コンピュータプログラムがタスクを実行し、以前は人間が実施していたルールを実施するようになりました。ワークフローのオートメーションは、製造や管理に関わるワークフロープロセスにベストプラクティスを取り入れることで、生産性と品質を向上させるために開発されました。これは、データソースから取得したデータと、特定のステージの実行が行われる様々なステージのネットワークロケーションから、ジョブチケットの生成とともにワークフロープロセスを定義することを容易にします。このシステムは、ユーザーにジョブチケットのステータスを視覚的に表示するとともに、外部要因の介入なしにジョブチケットを自動的に移動させることができます。システムはまた、特定の段階での変更に適応可能です。

- 組織からのワークフローソフトウェアに対する需要の高まりは、より洗練された効率的なソフトウェア開発への急速な投資につながっています。Signavio社によると、62%の組織が業務の25%までをモデル化しているが、全プロセスをモデル化しているのはわずか2%です。さらに、調査対象組織の13%がインテリジェントなオートメーションソリューションを大規模に導入していると回答しており、23%が導入中、37%が試験的にオートメーションを実施しています。

- 組織によるワークフローソフトウェアへの需要の高まりは、より洗練された効率的なソフトウェア開発への急速な投資につながっています。コンピュータ・ビジョン、コグニティブ・オートメーション、機械学習からロボティック・プロセス・オートメーションに至るまで、人工知能や関連する新技術の採用が増加しています。このようなテクノロジーの融合は、顧客のビジネス価値と競合優位性を劇的に高めるオートメーション機能を生み出します。

- あらゆる新しいテクノロジーの導入とは異なり、ワークフローのオートメーションは、人間および人間以外のアカウントに向けられたサイバー攻撃のリスクを生み出す可能性があります。そのため、プロセス・オートメーションのセキュリティは極めて重要です。RPAボットは機密データを扱うことが多く、あるシステムから別のシステムへデータを転送します。データが保護されていない場合、データが悪用され、企業に数百万米ドルの損害を与える可能性があります。

- COVID-19の発生により、サプライチェーンの脆弱性が露呈しました。ほとんどのIT組織にとって、脆弱なエコシステムには重要なITサービスのプロバイダーが含まれます。さらに、在宅勤務の義務化により、サービス・プロバイダーは、ミッション・クリティカルな企業の顧客が、提供するサービスのスピード、セキュリティ、品質、総合的な有効性を実現するために必要なツールやテクノロジーを確実に利用できるようになりました。

ワークフローオートメーション市場の動向

ソフトウェアセグメントが大幅な成長を記録する見込み

- IoTの導入は、アプリケーションやビジネスモデルの出現、デバイスコストの削減により、各業界で急増しています。IoT接続の急増に伴い、ワークフローオートメーションソフトウェア、ワークフロー管理ソフトウェア、ワークフローシステム、ビジネスプロセスオートメーション(BPA)など、ワークフローのオートメーションに使用されるツールが大きな需要を観察しています。ワークフローオートメーションソフトウェアには、付加価値機能を含む様々な利点があり、オートメーションの範囲を広げる統合機能を提供します。このような採用は、ワークフローオートメーション市場全体のソフトウェア・セグメントにさらなる需要をもたらすと思われます。

- いくつかの特徴には、ソフトウェアの実装と保守に必要なITサポート量を削減する機能が含まれます。ビジネス・ユーザーは、直感的なビジュアル・インターフェイスを通じて、いくつかの機能に便利にアクセスすることができ、オートメーションを迅速化し、ビジネス・チームをワークフロー最適化のための共同創造的な役割にすることができます。ローコードはまた、ITバックログへのプレッシャーを軽減します。例えば、Integrifyはローコードワークフローオートメーションプラットフォームであり、使いやすいビルダー、柔軟なカスタマイズ、複数の価格オプション、専任のカスタマーサポートを提供しています。

- ワークフローオートメーションソフトウェアは、カスタマイズ可能なフォームなどの機能により、プロセスを標準化し、エラーを回避し、重複したデータ入力を排除することで、リクエスト管理を簡素化するソリューションを提供します。ポータルは、社内外のパートナーとのフォームの整理と安全な共有を容易にします。ワークフローのオートメーションにおいて重要な役割を果たすその他の機能には、統合、テンプレートやルールの存在、条件ロジックなどがあります。

- 例えば、2023年10月、ビジネスソフトウェア用のローコード開発プラットフォームであるRetool Inc.は、Retool Workflowsの一般提供を発表しました。この非常に革新的なオートメーションツールは、開発者がコーディングに優先順位をつけ、監視・保守ツールとともにタスクをシームレスにオートメーションできるようにすることで、開発者を大幅に支援することを目的として設計されています。Retoolワークフローでは、開発者は、定期的なジョブ、カスタマイズされたアラート、および情報管理タスクの効率的なプロトタイピングと構築を可能にする、コーディングツールの広範な配列を提供するユーザーフレンドリーで視覚的に魅力的なインターフェイスを提供されます。さらに、このツールはトリガーに基づくデータの抽出、変換、ロードを容易にします。

予測期間中、アジア太平洋が最速の成長を記録する見込み

- 中国市場の競争激化に伴い、同国のさまざまな業界がデジタル変革を通じてワークフローを改善しています。例えば、Dongfeng Nissanは、効率性を向上させ、新車のマーケティングプロセスをスピードアップするためにデジタル変革プログラムを開始しました。同社は、既存のワークフローを改善し、社内業務を合理化し、全体的な効率化を促進することを目的として、データの有効活用を促進するデジタルトランスフォーメーション戦略を開始しました。このプログラムの一環として、同社は反復的なデジタル・タスクをオートメーションするために、ロボット・プロセス・オートメーション(RPA)ソフトウェア、UiPathを導入しました。

- チャイナユニコムのインテリジェント・ネットワーク・イノベーション・センターは、2021年にファーウェイと協力し、ファーウェイのAUTINシステムをベースとしたAI搭載のネットワーク管理・運用プラットフォームを開発・展開しました。同社はAIベースのネットワーク管理・運用プラットフォームを導入し、データを活用して全国ネットワークの運用、計画、管理を簡素化・オートメーションするとともに、5Gネットワークとサービスを展開する中で費用対効果、顧客体験、持続可能性を向上させました。

- オートメーションは、未来の仕事のアプローチに関連する最も重要な部分の1つであり、日本はAIを通じて革新を進めています。野村総合研究所によると、日本のAI分野は2035年までに大きな飛躍を遂げるといいます。アベジャやNECなどのオートメーション企業は、日本のGDPを押し上げるために、より生産効率を高める技術革新を行っています。

- インドの経済開発においても、オートメーションは大きな役割を果たしています。同国は現在、テクノロジーとイノベーションの導入により、ほとんどの分野で転換期を迎えています。人工知能国家戦略(NSAI)は、AIが2035年までにインドの年間成長率を1.3%加速させると予測していることを強調しました。

- その他アジア太平洋では、東南アジアとオーストラリアが顕著な地域です。東南アジアの企業は、AIを中心とした未来に向けて従業員を準備し、新しい技術を取り入れています。このため、企業は適切なスキルアップ戦略を通じてスキルギャップを埋める必要があります。デジタル化は、この地域が地元企業にとって世界的に競争力のあるパートナーシップを構築するのに役立つだけでなく、世界展開の可能性を高め、技術と知識の移転を成功させるのをサポートします。

ワークフローオートメーション産業の概要

ワークフローオートメーション市場は、細分化され競争が激しいです。この市場には、IBM Corporation、Oracle Corporation、Pegasystems Inc.、Xerox Corporation、Appian Corporationなど、複数の大手企業が参入しています。これらの企業は、戦略的協業イニシアティブを活用して市場シェアと収益性を高めています。

- 2023年11月世界なクラウドプラットフォームであり、財務、調達、カスタマーサービス機能向けのAI主導型プロセスオートメーションソリューションの業界リーダーであるEskerは、Teknionが業務効率を高めるためにEskerの買掛金オートメーションソリューションを採用したと発表しました。Eskerの革新的な技術を活用することで、テクニオンは世界拠点全体のシステムとERPワークフローの合理化を目指しています。Teknionは特に、財務システムの継続的な変革のために、複数のERPからの情報を効果的に組み合わせるオートメーションと人工知能を組み込んだソリューションを求めていました。

- 2023年9月セールスフォースは、Slackプラットフォームにいくつかの素晴らしい進化を導入しました。これには、SlackネイティブのジェネレーティブAI機能の統合、構造化されたワークフローに役立つリスト機能、オートメーションプラットフォームのさまざまな機能強化などが含まれます。一方、Slackも、独自のネイティブLLMテクノロジーを搭載した独自のSlack AIを発表し、大きく前進しました。さらにSlackは、タスク、承認、情報を整理するためのリスト機能など、ワークフローのオートメーションに価値ある追加を行いました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- 市場促進要因

- 業界全体におけるIoT導入の増加

- ビジネスプロセス管理におけるRPA導入の増加

- 市場抑制要因

- データセキュリティへの懸念

第5章 市場セグメンテーション

- 展開別

- オンプレミス

- クラウド

- ソリューション別

- ソフトウェア

- サービス別

- エンドユーザー産業別

- 銀行

- テレコム

- 小売

- 製造・物流

- ヘルスケア・医薬品

- エネルギー・公益事業

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他のアジア太平洋

- 世界のその他の地域(ラテンアメリカ、中東・アフリカ)

- 北米

第6章 競合情勢

- 企業プロファイル

- IBM Corporation

- Oracle Corporation

- Xerox Corporation

- Pegasystems Inc.

- Appian Corporation

- Bizagi

- Software AG

- IPsoft Inc.

- Newgen Software Technologies Limited

- Nintex Global Limited

第7章 投資分析

第8章 市場動向と将来機会

The Workflow Automation Market size is estimated at USD 23.77 billion in 2025, and is expected to reach USD 37.45 billion by 2030, at a CAGR of 9.52% during the forecast period (2025-2030).

The workflow concept has evolved from the notion of process in manufacturing and the office, and such processes have existed since the time of industrialization and are the outcome of a search to surge efficiency by concentrating on the routine aspects of work activities. They typically separate work activities into well-defined tasks, rules, roles, and procedures that regulate most of the manufacturing and office work. Initially, processes were carried out entirely by humans who manipulated physical objects.

Key Highlights

- With the introduction of information technology, processes in the workplace are partially or totally automated by information systems through computer programs performing tasks and enforcing rules that humans previously implemented. Workflow automation is developed to enhance productivity and quality by incorporating best practices in workflow processes involved in manufacturing as well as management. It facilitates defining workflow processes from the data fetched from the data sources and the network location of the various stages at which the execution of that particular stage is performed, along with the generation of job ticket. The system is able to move the job ticket automatically without any intervention of any external factor along with providing the user, a visual display of status of any job ticket at any point of time. The system is also adaptable to changes at a particular stage.

- The growing demand for workflow software from organizations is leading to rapid investment in the development of more sophisticated and efficient software. According to Signavio, 62% of the organizations have modeled up to 25% of their businesses, but a meager 2% have all their processes modeled. Moreover, 13% of the surveyed organizations say that they are implementing intelligent automation solutions at scale; 23% are implementing, and 37% are piloting automation.

- The increasing demand for workflow software by organizations is leading to rapid investment in the development of more sophisticated and efficient software. There is increasing adoption of artificial intelligence and related new technologies ranging from computer vision, cognitive automation, and machine learning to robotic process automation. This convergence of technologies produces automation capabilities that dramatically elevate business value and competitive advantages for customers.

- Unlike any new technology implementation, workflow automation can create risks for cyberattacks directed at both human and non-human accounts. As a result, process automation security is of critical importance. RPA bots often work on confidential data, transferring it from one system to another. If data is not protected, it can be leveraged, costing businesses millions.

- With the onset of COVID-19, the vulnerability of supply chains has been exposed. For most IT organizations, a fragile ecosystem includes providers of critical IT services. In addition, work-from-home mandates led the service providers to ensure that mission-critical enterprise customers have the necessary tools and technologies to enable the speed, security, quality, and overall efficacy of services provided.

Workflow Automation Market Trends

Software Segment is Expected to Register Significant Growth

- The adoption of IoT is surging among industries owing to the emergence of applications and business models and reduced device costs. With surging IoT connective, the tools used to automate workflows, including workflow automation software, workflow management software, workflow systems, or business process automation (BPA) are observing significant demand. The workflow automation software has various advantages, including value-adding features, and provides integration capabilities to increase the range of automation one can implement. Such adoption will bring more demand for the software segment across the workflow automation market.

- Some features include the capability of reducing the amount of IT support required to implement and maintain the software. Business users can conveniently access some features through an intuitive visual interface, making the automation faster and putting business teams in a co-creative role for optimizing workflows. Low code also relieves pressure on the IT backlog. For instance, Integrify is a low-code workflow automation platform that offers an easy-to-use builder, flexible customization, multiple pricing options, and dedicated customer support.

- Moreover, capturing and consolidating incoming data can be challenging for any team, and workflow automation software facilitates a solution with features such as customizable forms to simplify request management by standardizing processes, avoiding errors, and eliminating duplicate data entry. Portals make organizing and securely sharing forms with internal or external partners easy. Other features that play a crucial role in the workflow automation includes integrations, presence of templates and rules as well as conditional logic.

- For instance, In October 2023, Retool Inc., a low-code development platform for business software, announced the general availability of Retool Workflows. This highly innovative automation tool has been designed with the aim of greatly assisting developers by enabling them to prioritize coding and then seamlessly automate tasks alongside monitoring and maintenance tools. With Retool Workflows, developers are offered a user-friendly and visually appealing interface that provides an extensive array of coding tools, allowing for efficient prototyping and construction of periodic jobs, customized alerts, and information management tasks. Furthermore, this tool facilitates data extraction, transformation, and loading based on triggers.

Asia-Pacific Expected to Register the Fastest Growth During the Forecast Period

- With the increasing competition in the Chinese market, various industries in the country have been improving workflow through digital transformation. For instance, Dongfeng Nissan initiated its digital transformation program to improve efficiency and speed up the process of marketing a line of new vehicles. The company launched its digital transformation strategy for promoting the better use of data aimed to improve existing workflows, streamline internal business operations, and promote overall efficiency. As part of the program, the company implemented robotic process automation (RPA) software, UiPath, to automate repetitive digital tasks.

- China Unicom's Intelligent Network Innovation Center worked with Huawei in 2021 to develop and deploy an AI-powered network management and operations platform based on Huawei's AUTIN system. The company deployed an AI-based network management and operations platform to use data to simplify and automate national network operation, planning, and management while improving cost-effectiveness, customer experience, and sustainability as it rolled out 5G networks and services.

- Automation is one of the most crucial parts related to the future of work approach, and Japan is innovating through AI. According to the Nomura Research Institute, the AI sector in the country will see a massive stride by 2035. Automation companies such as Abeja, NEC, and others innovate to bring more production efficiency to push Japan's GDP.

- Automation has been playing a major role in India's economic development. The country is currently witnessing a transition in most sectors through the implementation of technology and innovation. The National Strategy for Artificial Intelligence (NSAI) highlighted that AI is predicted to accelerate India's annual growth rate by 1.3% by 2035.

- Southeast Asia and Australia are prominent regions in the Rest of Asia-Pacific. Southeast Asian companies are preparing employees for an AI-centered future and embracing new technologies. This would require enterprises to plug the skills gap through a proper upskilling strategy. Digitization would help the region to create globally competitive partnerships for local companies as well as improve the potential for global expansion and support a successful technology and knowledge transfer.

Workflow Automation Industry Overview

The Workflow Automation Market is fragemented and highly competitive. This market consists of several major players, such as IBM Corporation, Oracle Corporation, Pegasystems Inc., Xerox Corporation, and Appian Corporation. These companies leverage strategic collaborative initiatives to increase their market share and profitability.

- November 2023: Esker, a global cloud platform and industry leader in AI-driven process automation solutions for Finance, Procurement, and Customer Service functions, announced Teknion has selected Esker's Accounts Payable automation solution to enhance its operational efficiencies. By leveraging Esker's innovative technology, Teknion aims to streamline its systems and ERP workflow across its global sites. Teknion specifically sought a solution incorporating automation and artificial intelligence to effectively combine information from multiple ERPs for their ongoing transformation of financial systems.

- September 2023: Salesforce has introduced some impressive advancements to its Slack platform. These include integrating Slack-native generative AI capabilities, a helpful lists function for structured workflow, and various enhancements to its automation platform. On the other hand, Slack has also made significant strides by launching its own Slack AI, which is powered by its own native LLM technology. Additionally, Slack has made valuable additions to its workflow automation, such as a lists feature for organized tasks, approvals, and information.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Market Drivers

- 4.3.1 Increasing Adoption of IoT across industries

- 4.3.2 Rise in Implementation of RPA in Business Process Management

- 4.4 Market Restraints

- 4.4.1 Data Security Concerns

5 MARKET SEGMENTATION

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By Solution

- 5.2.1 Software

- 5.2.2 Service

- 5.3 By End-user Industry

- 5.3.1 Banking

- 5.3.2 Telecom

- 5.3.3 Retail

- 5.3.4 Manufacturing and Logistics

- 5.3.5 Healthcare and Pharmaceuticals

- 5.3.6 Energy and Utilities

- 5.3.7 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 Rest of the World (Latin America, Middle East and Africa)

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 IBM Corporation

- 6.1.2 Oracle Corporation

- 6.1.3 Xerox Corporation

- 6.1.4 Pegasystems Inc.

- 6.1.5 Appian Corporation

- 6.1.6 Bizagi

- 6.1.7 Software AG

- 6.1.8 IPsoft Inc.

- 6.1.9 Newgen Software Technologies Limited

- 6.1.10 Nintex Global Limited