|

|

市場調査レポート

商品コード

1621727

ワークフロー自動化市場の成長機会、成長促進要因、産業動向分析、2024~2032年予測Workflow Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2024 - 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ワークフロー自動化市場の成長機会、成長促進要因、産業動向分析、2024~2032年予測 |

|

出版日: 2024年10月07日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

世界のワークフロー自動化市場は、2023年に203億米ドルと評価され、2024~2032年にかけて10.1%のCAGRで成長すると予測されています。

この成長の原動力となっているのは、さまざまな産業でデジタルトランスフォーメーションへの取り組みが増加していることです。自動化は手作業を大幅に削減し、ミスを最小限に抑え、全体的な効率を向上させるため、企業にとって不可欠なものとなりつつあります。こうしたメリットは、業務効率が収益性に直結する製造、物流、金融などのセグメントで特に重要です。ワークフローを自動化することで、企業は従業員をより価値のある仕事に集中させることができ、リソース配分と労働生産性を高めることができます。

市場は組織規模別に区分され、2023年には大企業が市場シェアの65%以上を占める。このセグメントは2032年までに250億米ドルを超えると予測されています。複数の部門にまたがる複雑なワークフローを管理することが多い大企業は、業務の合理化、調整の改善、コンプライアンスの維持のために自動化に大きく依存しています。自動化は、手作業を減らし、ミスを最小限に抑え、リソースを最適化することでコスト削減に貢献します。また、スケーラビリティも提供するため、企業は増大する業務需要を効率的に管理することができます。エンドユーザー別では、ワークフロー自動化市場には、BFSI、医療、小売、IT・通信、製造、運輸・物流、政府・防衛、その他などのセグメントが含まれます。

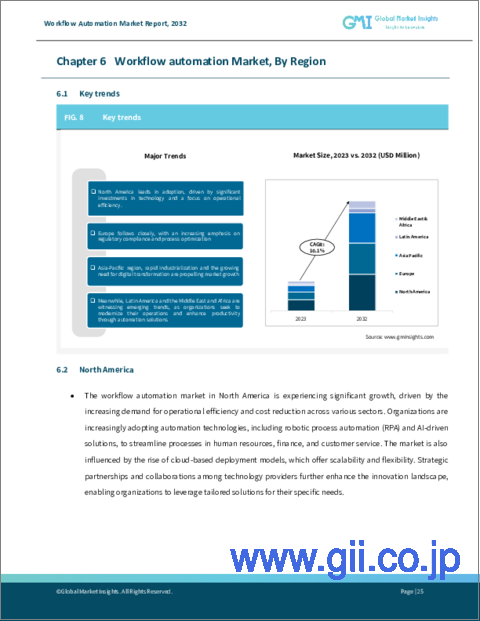

2023年には、BFSIセグメントが市場シェアの約24%を占めました。自動化は金融セクターにとって特に有益であり、金融機関が厳格な規制コンプライアンスを遵守する一方で、手作業によるミスを減らし、報告の正確性を高めるのに役立っています。先進的分析を統合することで、BFSIセグメントの自動化ツールは大量の取引データを迅速に分析し、潜在的な不正行為へのタイムリーな対応を可能にします。北米のワークフロー自動化市場は2023年に35%以上のシェアを占め、2032年には約150億米ドルに達すると予測されています。この地域では、ソフトウェアとITの急速な技術進歩が自動化ソリューションの採用に拍車をかけています。

| 市場範囲 | |

|---|---|

| 開始年 | 2023年 |

| 予測年 | 2024~2032年 |

| 開始金額 | 203億米ドル |

| 予測金額 | 468億米ドル |

| CAGR | 10.1% |

医療、金融、製造業など、さまざまなセグメントの企業がAIや機械学習を活用し、業務の合理化や効率化を図り、コスト削減やパフォーマンスの最適化を実現する動きが加速しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 産業洞察

- エコシステム分析

- サプライヤーの状況

- ソフトウェアプロバイダー

- クラウドサービスプロバイダー

- システムインテグレーター

- エンドユーザー

- 利益率分析

- 技術とイノベーションの展望

- ケーススタディ

- 主要ニュース&イニシアチブ

- 規制状況

- 影響要因

- 促進要因

- 業務効率化のためのデジタルソリューション導入の増加

- 中小企業におけるワークフロー自動化ソフトウェアの採用拡大

- クラウドベースの自動化プラットフォームの急成長

- ロボティックプロセスオートメーション(RPA)とAI統合の成長

- 産業の潜在的リスク・課題

- 高い導入コスト

- 複雑性と熟練労働者の不足

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニングマトリックス

- 戦略展望マトリックス

第5章 市場推定・予測:コンポーネント別、2021~2032年

- 主要動向

- ソフトウェア

- ロボティックプロセスオートメーション(RPA)

- ビジネスプロセス管理(BPM)

- AIによる自動化

- ドキュメントの自動化

- エンタープライズ・コンテンツ管理(ECM)

- CRMオートメーション

- サービス

- 実装とインテグレーション

- コンサルティング

- サポートとメンテナンス

- トレーニングと教育

第6章 市場推定・予測:展開モデル別、2021~2032年

- 主要動向

- オンプレミス

- クラウド

第7章 市場推定・予測、組織規模別、2021~2032年

- 主要動向

- 大企業

- 中小企業

第8章 市場推定・予測:用途別、2021~2032年

- 主要動向

- 人的リソース

- 財務・会計

- 営業・マーケティング

- カスタマーサービス

- オペレーション

- IT部門

- その他

第9章 市場推定・予測:最終用途別、2021~2032年

- 主要動向

- BFSI

- IT・通信

- 医療

- 製造業

- 小売

- 運輸・物流

- 政府・防衛

- その他

第10章 市場推定・予測:地域別、2021~2032年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Amazon Web Services(AWS)

- Appian Corporation

- Automation Anywhere, Inc.

- Blue Prism Group plc

- IBM Corporation

- Kofax Inc.

- Microsoft Corporation

- Nintex Global Ltd.

- Oracle Corporation

- Pegasystems Inc.

- Salesforce, Inc.

- SAP SE

- ServiceNow, Inc.

- Smartsheet Inc.

- TIBCO Software Inc.

- UiPath, Inc.

- WorkFusion, Inc.

- Xerox Corporation

- Zapier, Inc.

- Zoho Corporation

The Global Workflow Automation Market was valued at USD 20.3 billion in 2023 and is anticipated to grow at a CAGR of 10.1% between 2024 and 2032. This growth is driven by the increasing adoption of digital transformation initiatives across various industries. Automation is becoming essential for businesses as it significantly reduces manual work, minimizes errors, and improves overall efficiency. These benefits are particularly critical in sectors like manufacturing, logistics, and finance, where operational efficiency directly impacts profitability. By automating workflows, companies can free employees to focus on more valuable tasks, thus enhancing resource allocation and workforce productivity.

The market is segmented by organization size, with large enterprises dominating over 65% of the market share in 2023. This segment is projected to surpass USD 25 billion by 2032. Large organizations, which often manage complex workflows across multiple departments, rely heavily on automation to streamline operations, improve coordination, and maintain compliance. Automation helps reduce costs by decreasing manual labor, minimizing errors, and optimizing resources. It also provides scalability, enabling these enterprises to manage growing operational demands efficiently. In terms of end-users, the workflow automation market includes sectors such as BFSI, healthcare, retail, IT & telecom, manufacturing, transportation & logistics, government & defense, and others.

In 2023, the BFSI segment held approximately 24% of the market share. Automation is particularly beneficial for the financial sector, helping institutions adhere to strict regulatory compliance while reducing manual errors and enhancing reporting accuracy. With the integration of advanced analytics, automation tools in the BFSI sector can quickly analyze large volumes of transaction data, enabling timely responses to potential fraud. North America workflow automation market accounted for over 35% share in 2023 and is projected to reach around USD 15 billion by 2032. The region's rapid technological advancements in software and IT have fueled the adoption of automation solutions.

| Market Scope | |

|---|---|

| Start Year | 2023 |

| Forecast Year | 2024-2032 |

| Start Value | $20.3 Billion |

| Forecast Value | $46.8 Billion |

| CAGR | 10.1% |

Businesses across various sectors, including healthcare, finance, and manufacturing, are increasingly leveraging AI and machine learning to streamline operations and improve efficiency, all while reducing costs and optimizing performance

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Software providers

- 3.2.2 Cloud service providers

- 3.2.3 System integrators

- 3.2.4 End-users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Case Studies

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing adoption of digital solutions to streamline business operations

- 3.8.1.2 Growing adoption of workflow automation software among SME

- 3.8.1.3 Rapid growth in cloud-based automation platforms

- 3.8.1.4 Growth of Robotic Process Automation (RPA) and AI integration

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High implementation costs

- 3.8.2.2 Complexity and lack of skilled workforce

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2032 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Robotic Process Automation (RPA)

- 5.2.2 Business Process Management (BPM)

- 5.2.3 AI-Driven automation

- 5.2.4 Document automation

- 5.2.5 Enterprise Content Management (ECM)

- 5.2.6 CRM automation

- 5.3 Services

- 5.3.1 Implementation and integration

- 5.3.2 Consulting

- 5.3.3 Support and maintenance

- 5.3.4 Training and education

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2032 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2032 ($Bn)

- 7.1 Key trends

- 7.2 Large enterprises

- 7.3 SME

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2032 ($Bn)

- 8.1 Key trends

- 8.2 Human resources

- 8.3 Finance and accounting

- 8.4 Sales and marketing

- 8.5 Customer service

- 8.6 Operations

- 8.7 IT

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2032 ($Bn)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 IT and telecom

- 9.4 Healthcare

- 9.5 Manufacturing

- 9.6 Retail

- 9.7 Transportation and logistics

- 9.8 Government and defense

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2032 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Amazon Web Services (AWS)

- 11.2 Appian Corporation

- 11.3 Automation Anywhere, Inc.

- 11.4 Blue Prism Group plc

- 11.5 IBM Corporation

- 11.6 Kofax Inc.

- 11.7 Microsoft Corporation

- 11.8 Nintex Global Ltd.

- 11.9 Oracle Corporation

- 11.10 Pegasystems Inc.

- 11.11 Salesforce, Inc.

- 11.12 SAP SE

- 11.13 ServiceNow, Inc.

- 11.14 Smartsheet Inc.

- 11.15 TIBCO Software Inc.

- 11.16 UiPath, Inc.

- 11.17 WorkFusion, Inc.

- 11.18 Xerox Corporation

- 11.19 Zapier, Inc.

- 11.20 Zoho Corporation