|

市場調査レポート

商品コード

1642958

自動車におけるエッジコンピューティング:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Edge Computing In Automotive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車におけるエッジコンピューティング:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

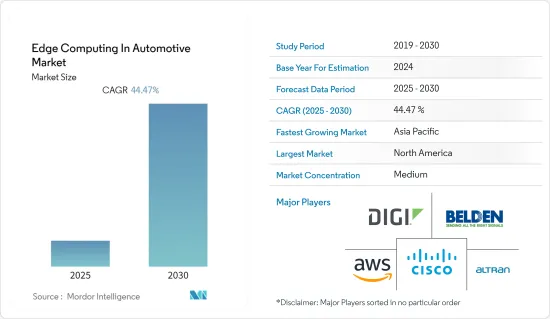

自動車におけるエッジコンピューティング市場は、予測期間中に44.47%のCAGRで推移すると予測されます。

自律走行車とコネクテッドカーインフラの進化、エッジコンピューティングソリューションの効率を高める軽量フレームワークとシステムの要件は、エッジコンピューティングベンダーに豊富なビジネスチャンスをもたらすと予測されます。

主なハイライト

- 自動車業界の企業は、センサーやその他のデータ生成・収集デバイス、分析ツールなど、さまざまな技術革新を導入することで、新たなレベルのパフォーマンスと生産性を追求し始めています。従来、データ管理と分析はクラウドやデータセンターで行われてきました。しかし、スマート・マニュファクチャリングやスマート・シティなど、ネットワーク関連技術やイニシアティブの浸透が進むにつれ、そのシナリオは変わりつつあるようです。

- コネクテッド・カーが期待される価値を提供するためには、このデータをリアルタイムで調合できるデバイスが必要です。エッジ・コンピューティングとは、IoT(モノのインターネット)機器から発生するデータを処理する方法です。エッジでは、収集されたデータは発生源で精査されます。

- さらに、産業用ロボットや様々なセンサーを搭載したコネクテッド・カーによって生成される、増加するデータをより速いペースで処理することは問題であり、5Gアプリケーションは低遅延と高信頼性によってこのような問題を解決し、この処理ニーズの一部をエッジまたはクラウドベースのサーバーにオフロードすることを容易にし、その結果、複雑さを最小限に抑えます。

- さらに、「世界な」国境が存在せず、ネットワークを通じて協力しなければならない多数の個人によって管理される単一の所有者を持つエコシステムは、それをさらに脆弱なものにしています。インフラの一部が、局所的な影響を及ぼす高度に局所的な攻撃の支配下に置かれる可能性があります。

自動車におけるエッジコンピューティング市場動向

IoTの普及が自動車用エッジコンピューティング市場の成長を牽引

- IoT技術は、製造業における労働力不足を克服しつつあります。より多くの企業にとって、ロボット化のようなインダストリー4.0技術の利用は日常業務の一部となっています。

- エッジネットワーク上のIoTデバイスを使用してデータを収集・転送するロボットは、クラウドベースの設計を使用するよりもはるかに迅速に異常を検出し、非効率を排除することができます。このようなシステムは、分散型設計により耐障害性が大幅に向上し、より高いレベルのアップタイム生産性も確保されます。

- 自動車産業におけるIoTの利用拡大は、主に低遅延とネットワーク・スライシング機能によって促進される5G運用によって加速されます。現在、産業用IoTサービスプロバイダーやアグリゲーターのかなりの部分が、5G対応のネットワークオプションを提供しており、今後数年間で、大量のデータを処理するためにエッジコンピューティングが組み込まれると予想されています。

- エッジコンピューティングの可能性により、産業用製造業は変貌を遂げつつあります。今後数十年で、エッジ・コンピューティング・アプリケーションは、コストを下げながら効率と生産を向上させるため、製造業を根本的に変えると思われます。これは、新世代のインテリジェントなIoTエッジデバイスと組み合わせることで達成されると思われます。予測期間中、これは市場の成長に好影響を与えると予想されます。

- さらに、企業におけるクラウドの採用は、主に柔軟性、拡張性、費用対効果によるものであり、調査対象市場における車両機能の高度化に役立つ可能性があります。

北米が最大の市場シェアを占める

- 北米は最大の市場シェアを占めており、同地域の消費者部門とビジネス部門がIoTデバイスに依存していることから、予測期間を通じて優位性を維持すると予測されています。同地域ではクラウドの導入が進んでおり、テクノロジーへの移行が進んでいます。また、同地域における自律走行車などの革新的なコンセプトの開発も、今後数年間における同地域の市場成長を促進すると予測されます。

- さらに、この地域は、エッジコンピューティングサプライヤーの数が非常に多く、5Gなどの新技術を活用するための技術が北米企業の間で受け入れられつつあることから、予測期間中に最大の市場を占めると予測されています。

- 2022年3月、連邦自動車安全規制当局は、ハンドルやペダルのような手動操作のない無人運転車の開発と使用にゴーサインを出しました。

- 5G技術はまだ試験段階です。しかし、将来的に実を結ぶことが期待されています。例えば、米国ではAT&Tとベライゾンがフィールドテストを行っています。米国最大の携帯電話サイト運営会社であり、エッジ・コンピューティングのスペシャリストであるヴェイパーIO社への出資者でもあるクラウン・キャッスルのように、企業パートナーの支援を受けているところもあります。

自動車におけるエッジコンピューティング業界の概要

自動車におけるエッジコンピューティング市場の競争は激しく、複数の大手企業が参入しています。現在、市場シェアの大部分を占める大手企業はほとんどなく、北米と欧州を中心とした新興国市場で大きなシェアを占めています。日本や中国のような新興国市場では、市場は非常に混乱しており、地域や地元の販売業者が優位を占めています。国際的なプレーヤーは、潜在的なビジネスチャンスの大きさを認識するようになり、徐々に供給ネットワークを構築し、M&Aを通じてこれらの非構造化マーケットプレースに参入しています。

2023年1月、ベルデンは、産業および輸送業務を含む過酷な環境におけるイーサネット接続の可能性を最適化するために設計された接続製品のシングルペアイーサネット(SPE)ポートフォリオを発表しました。SPEポートフォリオには、クリーンエリア接続用のIP20規格のPCBジャック、パッチコード、コードセット、および信頼性の高いフィールドデバイス産業用イーサネット接続用のIP65/IP67規格の円形M8/M12パッチコード、コードセット、リセプタクルが含まれます。

2022年11月、Belden Inc.は、Hirschmann GDMEヘビーデューティバルブコネクタとBelden HorizonTMエッジオーケストレーションプラットフォームを含む、ネットワークセキュリティ、堅牢化、展開簡素化のためのソリューションの発売を発表しました。このプラットフォームは、OT機器やアプリケーションの安全かつ容易な展開、接続、管理を維持しながら、リモート機器への安全なアクセスを可能にするソフトウェアを管理します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- バリューチェーン/サプライチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場力学

- 市場促進要因

- IoTの採用増加

- 指数関数的に増加するデータ量とネットワークトラフィック

- 市場抑制要因

- インフラの初期設備投資

- プライバシーとセキュリティへの懸念

第6章 市場セグメンテーション

- 用途別

- コネクテッドカー

- 交通管理

- スマートシティ

- 輸送・物流

- その他の用途

- 地域別

- 北米

- 欧州

- アジア

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Altran Inc

- Belden Inc.

- Digi International Inc.

- Cisco Systems, Inc.

- Amazon Web Services(AWS), Inc.

- General Electric Company

- Hewlett Packard Enterprise Development LP

- Huawei Technologies Co., Ltd.

- Litmus Automation

- Azion Technologies Ltd.

第8章 投資分析

第9章 市場機会と今後の動向

The Edge Computing In Automotive Market is expected to register a CAGR of 44.47% during the forecast period.

The evolution of autonomous vehicles and connected car infrastructure and the requirement for lightweight frameworks and systems to heighten the efficiency of edge computing solutions are anticipated to generate abundant opportunities for edge computing vendors.

Key Highlights

- Enterprises across automotive are beginning to drive new levels of performance and productivity by deploying different technological innovations, like sensors and other data-producing and collecting devices, along with analysis tools. Traditionally, data management and analysis are performed in the cloud or data centers. However, the scenario seems to be changing with the increasing penetration of network-related technologies and initiatives, such as smart manufacturing and smart cities.

- For connected cars to give the value they are expected to, there is a device that can concoct this data in real time. Edge computing is the method of processing data from IoT (Internet of Things) devices where it is generated. With the edge, the data being gathered gets examined right at the source.

- Moreover, processing increasing amounts of data at a faster pace, generated by industrial robots and connected cars equipped with various sensors, is problematic, and 5G applications are solving such issues with their low latency and high reliability, making it easier to offload part of this processing need to edge or cloud-based servers, thus, minimizing the complexity.

- Additionally, the absence of a "global" border and an ecosystem with a single owner that is governed by numerous individuals who must cooperate through networks makes it even more vulnerable. A piece of the infrastructure may be under the control of highly localized attacks with localized impact.

Edge Computing In Automotive Market Trends

Rising Adoption of IOT to Witness the Growth Edge Computing in Automotive Market

- IoT technologies are overcoming the labor shortage in the manufacturing sector. For more organizations, using Industry 4.0 technologies, like robotization, is part of day-to-day operations.

- Robots collecting and transferring data using IoT devices on an edge network can detect anomalies and eliminate inefficiencies far faster than they could use a cloud-based design. Such a system is substantially more resilient due to its distributed design, which also ensures higher levels of uptime productivity.

- The growing use of IoT in the automotive industry is accelerated by 5G operations, principally fueled by lower latency and network slicing capabilities. A sizable portion of industrial IoT service providers and aggregators currently offer 5 G-enabled network options, which are anticipated to incorporate edge computing over the next few years to handle the massive volume of data.

- Due to the potential of edge computing, industrial manufacturing is transforming. In the upcoming decades, edge computing applications will radically alter manufacturing to increase efficiency and production while lowering costs. This would be accomplished by combining them with a new generation of intelligent IoT edge devices. Over the projected period, this is expected to have a favorable effect on the market's growth.

- Furthermore, the adoption of the cloud in enterprises is primarily due to flexibility, scalability, and cost-effectiveness, which can help the advancement of vehicle capabilities in the studied market.

North America Occupies the Largest Market Share

- North America has accounted for the largest market share and is projected to maintain dominance throughout the forecast years as the consumer and business sectors in the region rely on IoT devices. Higher cloud adoption in the region contributes to the continued transition toward technology. The development of innovative concepts, such as autonomous cars, within the area is also expected to propel regional market growth in the years to come.

- Additionally, the region is anticipated to represent the largest market during the forecast period due to a significant number of edge computing suppliers and the growing acceptance of technology among North American businesses for utilizing new technologies, such as 5G.

- In March 2022, Federal vehicle safety regulators gave the go-ahead for developing and using driverless cars without manual controls like steering wheels or pedals.

- 5G technology is still in the testing stage. However, it is hoped that it will be fruitful in the future. For example, AT&T and Verizon conduct field tests in the United States. Some are backed by corporate partners, such as Crown Castle, the largest US mobile phone website operator and an investor in his Vapor IO, an edge computing specialist.

Edge Computing In Automotive Industry Overview

Edge computing in the automotive market is moderately competitive and consists of several major players. Few major companies today hold a disproportionate amount of the market share, which continues to be significant in all developed nations, particularly in North America and Europe. The market is highly disorganized in developing nations like Japan and China, where regional or local sellers predominate. International players are gradually creating supply networks and entering these unstructured marketplaces through mergers and acquisitions as they become aware of the significant potential opportunities.

In January 2023, Belden introduced its Single Pair Ethernet (SPE) portfolio of connectivity products designed to optimize Ethernet connection possibilities in harsh environments, including industrial and transportation operations. The SPE portfolio includes IP20-rated PCB jack, patch cords, and cord sets for clean-area connections and IP65/IP67-rated circular M8/M12 patch cords, cord sets, and receptacles for reliable field device industrial ethernet connections.

In November 2022 - Belden Inc. announced the launch of solutions for network security, ruggedization, and simplified deployment, including the Hirschmann GDME Heavy-Duty Valve Connectors and the Belden HorizonTM edge orchestration platform. The platform manages software that allows secure access to remote equipment while sustaining secure and easy deployment, connection, and management of OT devices and applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain / Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers/Consumers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Adoption of IOT

- 5.1.2 Exponentially Growing Data Volumes And Network Traffic

- 5.2 Market Restraints

- 5.2.1 Initial Capital Expenditure For Infrastructure

- 5.2.2 Privacy and Security Concerns

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Connected Cars

- 6.1.2 Traffic Management

- 6.1.3 Smart Cities

- 6.1.4 Transportation & Logistics

- 6.1.5 Other Applications

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Latin America

- 6.2.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Altran Inc

- 7.1.2 Belden Inc.

- 7.1.3 Digi International Inc.

- 7.1.4 Cisco Systems, Inc.

- 7.1.5 Amazon Web Services (AWS), Inc.

- 7.1.6 General Electric Company

- 7.1.7 Hewlett Packard Enterprise Development LP

- 7.1.8 Huawei Technologies Co., Ltd.

- 7.1.9 Litmus Automation

- 7.1.10 Azion Technologies Ltd.