|

|

市場調査レポート

商品コード

1444438

アフェレシスの世界市場:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Apheresis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフェレシスの世界市場:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

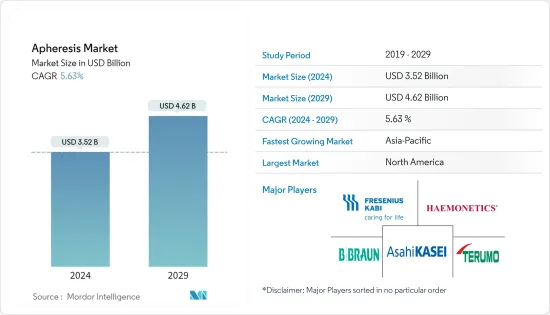

世界のアフェレシスの市場規模は、2024年に35億2,000万米ドルに達し、2024~2029年の予測期間中にCAGR 5.63%で成長し、2029年までに46億2,000万米ドルに達すると予測されてます。

COVID-19パンデミックは、COVID-19患者の治療に血漿療法が広範に適用されたため、アフェレシス市場の成長に大きな影響を与えました。 2021年12月にJournal of Clinical Apheresisに掲載された研究によると、物資、特にRBCユニットとアフェレシスキットの不足が、COVID-19パンデミック中のアフェレシス施設での患者治療における主な問題の1つでした。「ステイホーム」の指示と新型コロナウイルス感染症(SARS)への懸念により、献血者数は激減しました。したがって、調査対象の市場は当初、パンデミックの影響を受けていました。さらに、COVID-19を治療するワクチンや薬剤は存在せず、ほとんどの医師は、COVID-19で重篤な影響を受けた患者に対する回復期血漿療法を選択しました。この治療では、治癒した患者の血液から血漿交換法により抽出した血漿を、治療を受ける患者に輸血します。したがって、COVID-19患者の治療におけるアフェレシスユニットの広範な使用と、米国食品医薬品局(FDA)による製品承認の増加を考慮すると、アフェレシス市場はパンデミック中にプラスの成長を記録しましたが、パンデミックが沈静化している現在、市場はある程度の牽引力を失いましたが、調査の予測期間中は安定した成長が見込まれています。

アフェレシス市場の成長を促進する要因には、疾患の負担の増大、血液成分とそれに関連する安全性の需要の高まり、新しいアフェレシス技術の開発における技術進歩、償還政策とアフェレシス手順の資金の増加などが含まれます。たとえば、2022年 6月、英国のNHS Englandは、NHS MedTech Funding Mandate(MTFM)を通じて、鎌状赤血球症の治療に同社のSpectra Optia Apheresis Systemで実行される自動赤血球交換(RBCX)治療を選択しました。この選択により、Spectra Optiaは英国全土の病院でより頻繁に使用されることになります。鎌状赤血球症患者はこの治療法をより簡単に利用できるようになります。したがって、アフェレシスに関連する資金調達イニシアチブの増加が市場の成長を促進しています。

臨床症状のある患者におけるアフェレシスの使用は日に日に増加しており、血栓性血小板減少性紫斑病、溶血性尿毒症症候群、薬物毒性、自己免疫疾患、敗血症、劇症肝不全など、さまざまな疾患の主治療または他の治療の補助として広く使用されています。

これらの要因に加えて、製品の革新と承認の増加が市場の成長を促進しています。たとえば、2021年 7月、Terumo Blood and Cell Technologiesは、医師が患者のベッドサイドで体外フォトフェレーシス免疫療法(ECP)処置を行うための直接サービスを発表しました。同社はSpectra Optiaの機能を拡張しました。 UVA PITシステムECPは、単核球収集(MNC)および連続単核球収集(CMNC)プロトコルを備えた、機能的に閉鎖されたオンラインの多段階システムとしてこれらのデバイスを使用して実行できるようになりました。したがって、前述の要因により、アフェレシス市場は予測期間中に健全な成長が見込まれると予想されます。しかし、熟練した専門家の不足、血液汚染、アフェレシス手順に関連するコストが市場の成長を抑制しています。

アフェレシス市場動向

血液疾患セグメントは予測期間中に大幅な成長が見込まれる

血液疾患は、赤血球、白血球、血小板、骨髄、リンパ節、脾臓の問題を含む血液および造血器官の疾患です。血液疾患は、世界中の個人の罹患率と死亡率に大きく寄与しています。 CDCによる2022年 5月の最新情報によると、鎌状赤血球症(SCD)は約10万人のアメリカ人に影響を与えています。黒人またはアフリカ系アメリカ人の出生365人に約1人の割合で発生します。早期の診断と治療が、血球疾患患者の命を守る最善の方法です。したがって、血液疾患の発生率の負担の増加と血液疾患の治療法としてのアフェレシスの応用の拡大により、研究対象セグメントは予測期間中に成長すると予想されます。

ここ数年、治療上のアフェレシスが増加しています。たとえば、免疫吸着、二重濾過、およびサイトアフェレシスは、原発性および続発性の自己免疫性腎疾患の治療に容易に使用されます。さらに、ClinicalTrails.govによると、2022年 11月の時点で、血液悪性腫瘍に対するアフェレシスに関する研究が51件報告されており、そのうち約27件の研究が完了し、8件の研究が現在、世界中でさまざまな血液疾患の発症に対するアフェレシスの募集を行っています。

さらに、アフェレシスは鎌状赤血球貧血症の管理において重要な役割を果たします。 2021年 11月にSage Journalに掲載された研究によると、アフェレシス装置は鎌状赤血球で行われる赤血球交換治療処置の管理を改善することが判明しました。したがって、前述の要因により、さまざまな血液疾患の治療におけるアフェレシスの適用は、最終的にセグメントの成長を促進します。

北米は予測期間中に健全な成長を遂げると予想される

北米は、腎臓病、代謝性疾患、がん、神経疾患など、血液に関連するさまざまな病気の負担の増大、確立されたヘルスケアインフラの存在、患者の意識レベルの高さにより、予測期間中に成長すると予想されています。 2021年の白血病リンパ腫協会(LLS)によると、米国では約3分に1人が血液がんと診断されています。白血病、リンパ腫、骨髄腫の新規症例は、2021年に米国で新たにがんと診断された合計1,898,160件の9.8%を占めました。対象疾患の高い発生率が調査対象市場の成長を促進しています。

国内ではアフェレシス処置や器具に対する償還政策が強化されており、アフェレシスの需要が高まっています。 2022年1月、United Healthcare GroupはUnitedHealthcare Commercial Medica Policyという文書を発行しました。この文書は、骨髄/幹細胞移植で使用する幹細胞の収集または収集を除く、複数の適応症に対して実行されるアフェレシス手順に関する医療ポリシーを規定しています。これらの処置に対して利用可能な政策は、対象となる人々の間で処置に対する需要を増大させており、それが最終的に国内のアフェレシス市場を促進しています。

さらに、米国アフェレシス協会(ASFA)は、2021年9月21日をアフェレシス啓発デーと宣言し、今後は毎年9月の第3火曜日に開催すると発表しました。これは、アフェレシス医療を促進し、アフェレシス医療の意識を高めるために、証拠に基づいた実践を採用することで他者を救うことに人生を捧げた多数のドナー、患者、アフェレシス専門家を表彰することを目的としていました。したがって、これらの前述の要因により、予測期間中の北米市場はアフェレシスの普及が大幅に促進されることが期待されています。

アフェレシス産業の概要

調査対象の市場は適度に競争があり、少数の大手企業によって支配されています。現在、この市場は多くの分野で確立されており、初期の成功を収めています。ただし、発展途上地域ではその可能性を最大限に発揮できるかどうかはまだわかっていません。政府の取り組みが進むにつれ、人々の意識も高まり、調査対象市場の成長がさらに促進されています。さらに、大手企業による戦略的提携や製品の発売が市場の成長を促進すると予想されます。市場の主要企業としては、B. Braun SE、Asahi Kasei Corporation、Fresenius SE & Co. KGAA、Terumo Corporation (Terumo BCT Inc.) などが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 病気の負担の増加により、血液成分とそれに関連する安全性の需要が増大

- 新しいアフェレシス技術の開発における技術の進歩

- 償還政策とアフェレシス手順への資金提供の増加

- 市場抑制要因

- アフェレシス手順に関連する多額の設備投資とコスト

- 熟練した専門家の不足

- 血液汚染のリスク

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

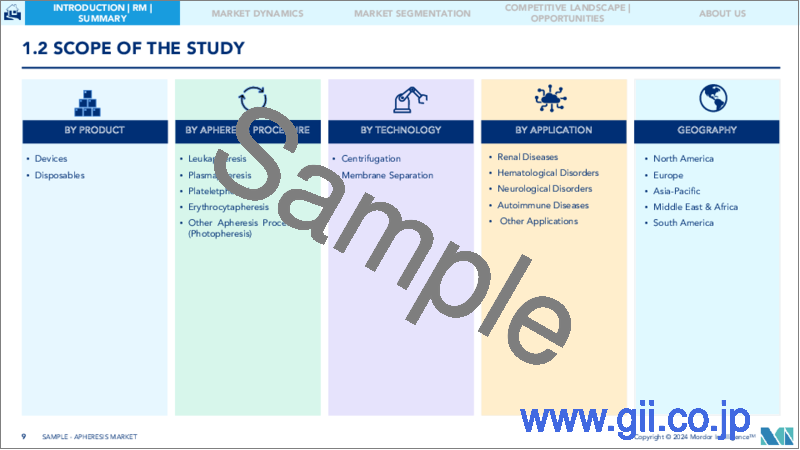

第5章 市場セグメンテーション

- 製品別

- デバイス

- 消耗品

- アフェレシス手順別

- 白血球除去療法

- 血漿交換

- 血小板フェレーシス

- 赤血球除去療法

- その他のアフェレシス手順

- 技術別

- 遠心分離

- 膜分離

- 用途別

- 腎疾患

- 血液疾患

- 神経学的障害

- 自己免疫疾患

- その他の用途

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Asahi Kasei Corporation

- B. Braun SE

- Fresenius SE &Co. KGAA(Fresenius Kabi AG)

- Haemonetics Corporation

- Terumo Corporation(Terumo BCT Inc.)

- Kaneka Corporation

- Sumitomo Bakelite Company Limited(Kawasumi Laboratories Inc.)

- Medica SPA

- Baxter International

- Cerus Corporation

- Macopharma SA

- Otsuka Holdings Co. Ltd(JIMRO Co., Ltd)

第7章 市場機会と将来の動向

The Apheresis Market size is estimated at USD 3.52 billion in 2024, and is expected to reach USD 4.62 billion by 2029, growing at a CAGR of 5.63% during the forecast period (2024-2029).

The COVID-19 pandemic had a profound impact on the growth of the Apheresis market, due to the extensive application of plasma therapy to treat patients infected with COVID-19. According to the study published in the Journal of Clinical Apheresis in December 2021, the Lack of supplies, notably RBC units and apheresis kits, was one of the main problems with patient treatment in the apheresis facility during the COVID-19 pandemic. Due to "stay home" instructions and concern about SARS CoV2 infection, the number of blood donors drastically reduced. Thus the studied market was initially impacted by the pandemic. Moreover, there were no vaccines or drugs to treat COVID-19, and most doctors opted for convalescent plasma therapy in patients who were severely affected by COVID-19. In this treatment, the plasma extracted from the blood of cured patients by the plasmapheresis technique was transfused into the patient who underwent treatment. Thus, given the wide usage of apheresis units in treating COVID-19 patients and increasing product approvals by the United States Food and Drug Administration (FDA), the apheresis market marked a positive growth during the pandemic, however currently as the pandemic subsided, the market lost some traction, however it is expected to have a stable growth during the forecast period of the study.

The propelling factors for the growth of the apheresis market include the increasing burden of diseases, a rise in the demand for blood components and their associated safety, technological advancements in the development of new apheresis techniques, and an increase in the reimbursement policies and funding for apheresis procedures. For instance, in June 2022, through the NHS MedTech Funding Mandate (MTFM), NHS England in the United Kingdom has chosen the automated red blood cell exchange (RBCX) treatment carried out on the business's Spectra Optia Apheresis System to treat sickle cell disease. Due to this choice, Spectra Optia will be used more frequently in hospitals all around England. Patients with sickle cell illness will now have better access to this therapy. Thus, the increasing funding initiatives related to apheresis are propelling the market growth.

The use of apheresis in clinically ill patients is increasing day by day, and it has been widely used as the primary therapy or as an adjunct to other treatments for various diseases, such as thrombotic thrombocytopenic purpura, hemolytic uremic syndrome, drug toxicities, autoimmune disease, sepsis, and fulminant hepatic failure.

Along with these factors, the increasing product innovations and approvals have been driving the market growth. For instance, in July 2021, Terumo Blood and Cell Technologies announced a direct offering for physicians to perform extracorporeal photopheresis immunotherapy (ECP) procedures at the patient's bedside. The company has expanded the functionality of Spectra Optia. The UVA PIT System ECP can now be performed using these devices as a functionally closed, online, multistep system with mononuclear cell collection (MNC) and continuous mononuclear cell collection (CMNC) protocols.Thus, owing to the aforementioned factors, the apheresis market is expected to witness healthy growth over the forecast period. However, lack of skilled professionals, blood contamination and cost associated with apheresis procedures restrain the market growth.

Apheresis Market Trends

Hematological Disorders Segment is Expected to Witness Significant Growth During the Forecast Period

Hematologic disorders are the disorders of blood and blood-forming organs which include problems with red blood cells, white blood cells, platelets, bone marrow, lymph nodes, and spleen. Hematological disorders make a substantial contribution to the morbidity and mortality of individuals across the globe. As per the May 2022 update by the CDC, sickle cell disease (SCD) affects approximately 100,000 Americans. It occurs among about 1 out of every 365 Black or African American births. Early diagnosis and treatment are the best ways to protect the life of a patient with a blood cell disorder. Hence, owing to the increasing burden of hematological incidences and growing applications of apheresis as a treatment method for hematological disorders, the studied segment is expected to experience growth in the forecast period.

There has been a rise in therapeutic aphereses over the past few years; for instance, immunoadsorption, double filtration, and cytapheresis are readily used in the treatment of both primary and secondary autoimmune renal diseases. Additionally, as per ClinicalTrails.gov, as of November 2022, there are 51 studies reported on apheresis for hematological malignancy among which about 27 studies that were completed and 8 studies are currently recruiting for apheresis for different hematological disease development across the globe.

Furthermore, apheresis has a vital role in the management of sickle cell anemia disease. As per the study published in Sage Journal in November 2021, apheresis equipment was found to provide better management in red cell exchange therapeutic procedures being performed in sickle cell. Thus, owing to the aforementioned factors, the application of apheresis in treating various hematological disorders will ultimately drive the segment growth.

North America is Expected to Witness Healthy Growth Over the Forecast Period

North America is expected to grow over the forecast period due to the growing burden of various ailments related to blood, such as kidney diseases, metabolic diseases, cancer, and neurological disorders, the presence of established healthcare infrastructure, and high patient awareness levels. According to the Leukemia & Lymphoma Society (LLS) 2021, approximately every three minutes, one person in the United States is diagnosed with blood cancer. The new cases of leukemia, lymphoma, and myeloma accounted for 9.8% of the total 1,898,160 new cancer cases diagnosed in the United States in 2021. The high incidence of target diseases is driving the growth of the market studied.

The increasing reimbursement policies in the country for apheresis procedures and devices is increasing the demand for apheresis. In January 2022, United Healthcare Group issued a document UnitedHealthcare Commercial Medica Policy, the document provides a medical policy for apheresis procedures which are performed for multiple indications except for stem cell collection or harvesting for use in bone marrow/stem cell transplantation. These, available policies for the procedures are increasing demand for the procedures among the target population, which is ultimately driving the market for apheresis in the country.

Furthermore, the American Society for Apheresis (ASFA) declared September 21, 2021, to be Apheresis Awareness Day, and stated that it would take place every year on the third Tuesday in September moving forward. This was intended to recognize numerous donors, patients, and apheresis professionals who have dedicated their lives to saving others by employing evidence-based practice to promote apheresis medicine and raise awareness of apheresis medicine.Thus, these aforementioned factors are expected to significantly boost the apheresis market in North America over the forecast period.

Apheresis Industry Overview

The market studied is moderately competitive and dominated by a few major players. Currently, the market is well established in many areas and has shown nascent success. However, its full potential is yet to be determined in developing regions. With increasing government initiatives, awareness among people is also increasing, which is further driving the growth of the market studied. Additionally, strategic alliances and product launches by major companies are expected to drive market growth. Some of the major players in the market are B. Braun SE, Asahi Kasei Corporation, Fresenius SE & Co. KGAA and Terumo Corporation (Terumo BCT Inc.) among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Disease Burden Resulting in Rise in Demand for Blood Components and Associated Safety

- 4.2.2 Technological Advancements in Development of New Apheresis Techniques

- 4.2.3 Rise in Reimbursement Policies and Funding for Apheresis Procedures

- 4.3 Market Restraints

- 4.3.1 High Capital Investment and Costs Associated with Apheresis Procedures

- 4.3.2 Shortage of Skilled Professionals

- 4.3.3 Risk of Blood Contamination

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Product

- 5.1.1 Devices

- 5.1.2 Disposables

- 5.2 By Apheresis Procedure

- 5.2.1 Leukapheresis

- 5.2.2 Plasmapheresis

- 5.2.3 Plateletpheresis

- 5.2.4 Erythrocytapheresis

- 5.2.5 Other Apheresis Procedures

- 5.3 By Technology

- 5.3.1 Centrifugation

- 5.3.2 Membrane Separation

- 5.4 By Application

- 5.4.1 Renal Disorders

- 5.4.2 Hematological Disorders

- 5.4.3 Neurological Disorders

- 5.4.4 Autoimmune Disorders

- 5.4.5 Other Applications

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Asahi Kasei Corporation

- 6.1.2 B. Braun SE

- 6.1.3 Fresenius SE & Co. KGAA (Fresenius Kabi AG)

- 6.1.4 Haemonetics Corporation

- 6.1.5 Terumo Corporation (Terumo BCT Inc.)

- 6.1.6 Kaneka Corporation

- 6.1.7 Sumitomo Bakelite Company Limited (Kawasumi Laboratories Inc.)

- 6.1.8 Medica SPA

- 6.1.9 Baxter International

- 6.1.10 Cerus Corporation

- 6.1.11 Macopharma SA

- 6.1.12 Otsuka Holdings Co. Ltd (JIMRO Co., Ltd)