|

|

市場調査レポート

商品コード

1690783

表面実装技術:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Surface Mount Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 表面実装技術:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 144 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

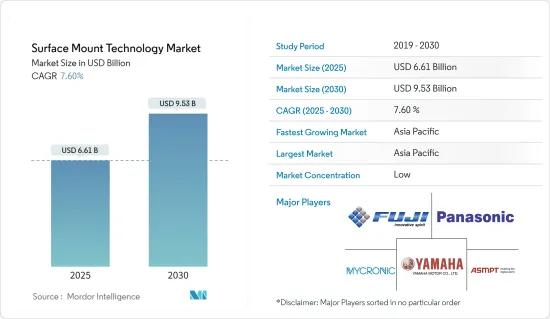

表面実装技術の市場規模は2025年に66億1,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは7.6%で、2030年には95億3,000万米ドルに達すると予測されます。

表面実装技術(SMT)は、プリント基板(PCB)の表面に部品を直接実装する電子回路の構築方法です。PCBに開けた穴に部品を挿入する旧来のスルーホール技術とは対照的です。SMTで使用される部品はSMDと呼ばれ、小さな金属タブまたはエンドキャップがあり、PCB表面に直接はんだ付けできます。これにより、1枚のPCBでより小さく、より軽く、より多くの部品を使用することができます。

パンデミックの影響後、ノートパソコンやサーバーの市場は需要の急増を目の当たりにしています。インド電子半導体協会(IESA)によると、在宅勤務の増加やコラボレーションツールの導入に伴い、より多くのデータがクラウド上に保存されるようになっています。需要の急増は、サーバー、データセンター、コンピューティング分野で見られます。米国のマイクロン・テクノロジー社も、リモートワーク経済、ゲーム、eコマースの活発化により、データセンターからの需要が高まっていると報告しています。さらにCloudsceneによると、2024年3月現在、米国には5,381のデータセンターがあり、これは世界のどの国よりも多いです。さらに521ヵ所がドイツに、514ヵ所が英国にあります。

電子部品の小型化により、どこにでも持ち運べる小型のポータブル・ハンドヘルド・コンピュータ・デバイスの製造が可能になりました。その結果、処理能力の高い、より小型で軽量な機器が市場に出回るようになりました。部品は(例えば衣服の袋に)簡単に埋め込むことができ、長期間持ち運ぶことができるため、よりウェアラブルになってきています。部品は小型化し、実装されるプリント基板の設計に新たな要求が突きつけられています。NCABグループは、超高密度ウルトラHDIプリント基板の規格を定義するIPCの取り組みにしっかりとコミットしており、2023年には顧客に提供できるようになると期待しています。

表面実装技術(SMT)は、現代の電子機器製造において極めて重要な要素となっており、その無数の利点により従来のスルーホール方式を凌駕しています。SMTの際立った利点は、必要なPCB穴あけを大幅に削減できる点にあります。製造業者は穴あけ工程を省くことで、時間とコストの両方を削減することができ、複雑で高密度な基板にとっては特筆すべきメリットとなります。このシフトは、生産を合理化し、人件費や材料費を削減し、製造プロセスの全体的な費用対効果を強化します。

表面実装技術は、より小さく、より効率的で、費用対効果の高い電子機器の製造を可能にすることで、電子機器製造業界に革命をもたらしました。しかし、数多くの利点があるにもかかわらず、SMTはすべての用途に適しているわけではありません。SMTは、トランスや電源回路などの大電力・高電圧部品には不向きです。これらの部品は熱を発生し、高い電気負荷がかかるため、SMTは効果的に処理するようには設計されていないです。

米国議会予算局によると、米国の国防費は2033年まで毎年増加すると予測されています。米国の国防費は、2023年には7,460億米ドルに達します。同予測では、2033年の国防費は1兆1,000億米ドルまで増加すると予測されています。

表面実装技術(SMT)市場動向

コンシューマーエレクトロニクス・エンドユーザー産業セグメントが大きな市場シェアを占める見込み

- 自動車業界では、SMTは電子制御ユニット(ECU)、ダッシュボードディスプレイ、レーダー・カメラモジュール、バッテリー管理システム(BMS)、安全支援システムなどに使用されています。SMTは、自動車用途において極めて重要な製造工程として浮上してきました。その効率、精度、信頼性で知られるSMTは、ADAS(先進運転支援システム)、インフォテインメントシステム、車両制御システムなど、さまざまな車載エレクトロニクス製品の強化に欠かせないです。

- 最新の自動車では、車載制御システムが自動車の「頭脳」の役割を果たし、電子部品の機能を監督し、調和させています。車載制御システムは、ナビゲーションからオーディオ、エアコンに至るまで、そのシームレスな動作において極めて重要です。これらの制御システムの信頼性の中心となるのがSMT技術です。この技術は、回路基板上に極小の電子部品を正確に実装することを可能にし、システムの効率的で信頼性の高い動作を保証します。

- エンジン・コントロール・ユニット(ECU)は、自動車の電子システムの核であり、エンジン性能、トランスミッション、ブレーキなどの重要な動作を監督しています。マイクロチップ、抵抗器、コンデンサー、その他の表面実装部品をECUに組み付けるには、表面実装技術(SMT)が不可欠です。

- さらに、人工知能技術は自動車分野での採用が増加する見通しです。電子部品組立における表面実装技術(SMT)の精度と効率は、AIチップとプロセッサーの生産を強化します。その結果、自動車用電子製品は自律的な意思決定能力が強化され、インテリジェントな運転と自動車の自動化が進むことになります。

- IEAが強調しているように、世界の自動車産業は大きな変革期を迎えており、エネルギー部門にも潜在的に大きな影響を及ぼしています。予測によると、電動化の進展により、2030年までに1日あたり500万バレルの石油が不要になると予想されています。

- IEAの報告書はまた、電気自動車の販売台数が大幅に増加することも明らかにしており、2023年には2022年比で350万台が販売され、35%の伸びを示しました。特筆すべきは、年間を通じて毎週25万台以上の新規登録が記録されたことです。2023年には、電気自動車が全販売台数の約18%を占め、5年前の2%、2022年の14%から大幅に増加しました。これらの動向は、電気自動車市場が成熟するにつれて、堅調な成長が持続すると予想されることを示しています。さらに、2023年には電気自動車ストックの70%がバッテリー電気自動車で構成されると予測されています。

アジア太平洋地域が最速の成長を遂げる見込み

- アジア太平洋、特に日本、中国、韓国、台湾、東南アジアなどの国々は、エレクトロニクス製造の世界のハブとなっています。この地域の強固な製造インフラ、熟練した労働力、政府の支援政策が多国籍企業を引きつけ、現地のエレクトロニクス産業の成長を促進しています。タブレット、スマートフォン、その他の電子機器の需要は伸び続けており、表面実装技術による効率的かつ大量生産能力が必要とされています。同社は、現地でSMT(表面実装技術)を導入することで、付加価値が現在の15%から25%に増加すると予測しています。

- 例えば、2023年8月、インド政府は、今後5~10年間で60~80%の大幅な増加を目標に、インドで組み立てられた製品の現地での付加価値向上を強化するため、世界のエレクトロニクス企業と積極的に関与しています。これを達成するため、政府はインドの産業界に対し、表面実装技術(SMT)ラインのような高度な生産方式を採用するよう促しています。

- 炭化ケイ素(SiC)は、高温耐性、優れた導電性、優れたエネルギー効率により、ますます脚光を浴びています。インダストリー4.0で電気自動車(EV)、ソーラーパネル、高度な電力管理の需要が高まる中、SiC製造の意義は高まっています。ワイドバンドギャップ導体は、これらの分野での電力消費を最小限に抑える必要性を考えれば、自然に適合します。

- 2024年2月、コンチネンタル・デバイス・インディア社(CDIL)は、SiC表面実装技術(SMT)部品専用の新しい組立ラインを稼働させ、重要な一歩を踏み出しました。これによりCDILは、SiC部品製造におけるインドのパイオニアとしての地位を確立しました。この強化により、CDILは、SiCショットキーダイオード、SiC MOSFET、ゼナー、整流器、TVSダイオードなどのさまざまなオートグレードデバイスを生産できるようになり、世界市場と国内市場の両方に対応できるようになりました。

- 2024年4月、TDK株式会社は、最大4.6 A(100 kHz、+125 °C時)に対応するハイブリッドポリマーコンデンサのラインアップ、B40910シリーズを発表しました。これらの表面実装部品は、室温で17mホウと22mホウという驚くべき低ESR値を誇ります。

- 液体電解質を使用した標準的な電解コンデンサとは異なり、TDKのコンデンサのESRは温度による変化がほとんどありません。10×10.2mmまたは10×12.5mm(D×H)の小型部品で、定格電圧は63V、静電容量は82μF~120μFです。このように、SMTメーカーは技術の統合と革新によって、この技術の必要性を推進しています。こうした努力は、さまざまな産業における表面実装技術(SMT)の広範な採用と成長に貢献しています。

表面実装技術(SMT)産業の概要

表面実装技術市場は、世界プレーヤーと中小企業の両方が存在するため、非常に断片化されています。同市場の主要企業には、富士フイルム、ヤマハ発動機、Mycronic AB、ASMPT、パナソニックなどがあります。同市場のプレーヤーは、製品ラインナップを強化し競争上の優位性を獲得するため、提携や買収を採用しています。

2024年3月- ノードソン・コーポレーションは、メキシコのケレタロを拠点とする新しいラテンアメリカ・テックセンターを導入し、同地域のメーカーがアセンブリ液、部品、基板、生産要件に最適な液剤塗布装置についてタイムリーなフィードバックを得られるようにしました。ラボには3Dプリンター、スケール、その他の測定機器が設置されており、各顧客固有のアプリケーション要件に適した液剤塗布装置を決定することができます。

2024年1月- ヤマハ発動機は、実装性能でクラス最速の称号を持つ表面実装機YRM10の発売を発表しました。52,000CPHという驚異的な速度で、1ビーム1ヘッドのカテゴリーで競合他社を圧倒します。本装置は、コンパクトで場所をとらず、様々な部品互換性と汎用性を提供し、高速モジュール組立のための次世代ソリューションとなっています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19が表面実装技術市場に与える影響

第5章 市場力学

- 技術の小型化に対する需要の高まり

- 他の技術に比べてプリント基板に開ける穴が少ない

- 市場の課題

- SMTは大型、高出力、高電圧部品や機械的ストレスが頻繁にかかる部品には不向き

- 高い初期コストとリワークの問題

第6章 市場セグメンテーション

- コンポーネント別

- 受動部品

- 抵抗器

- コンデンサー

- 能動部品

- トランジスタ

- 集積回路

- 受動部品

- エンドユーザー産業別

- コンシューマーエレクトロニクス

- 自動車

- 産業用エレクトロニクス

- 航空宇宙・防衛

- ヘルスケア

- その他のエンドユーザー産業

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Fuji Corporation

- Yamaha Motor Co. Ltd

- Mycronic AB

- ASMPT

- Panasonic Corporation

- Nordson Corporation

- Juki Corporation

- Hanwa Precision Machinery Co. Ltd

- Zhejiang Neoden Technology Co. Ltd

- Europlacer Limited

- Viscom SE

第8章 投資分析

第9章 市場機会と今後の動向

The Surface Mount Technology Market size is estimated at USD 6.61 billion in 2025, and is expected to reach USD 9.53 billion by 2030, at a CAGR of 7.6% during the forecast period (2025-2030).

Surface mount technology (SMT) is a method for constructing electronic circuits in which the components are mounted directly onto the surface of printed circuit boards (PCBs). This contrasts with older through-hole technology, where components are inserted into holes drilled into the PCB. Components used in SMT, known as SMDs, have small metal tabs or end caps that can be soldered directly onto the PCB surface. This allows for using smaller, lighter, and more components on a single PCB.

After the effect of the pandemic, the market for laptops and servers is witnessing a surge in demand. According to the India Electronics and Semiconductor Association (IESA), more data is stored on the cloud as work-from-home increases and more collaboration tools are deployed. A surge in demand is witnessed in the server, data centers, and computing segments. US-based Micron Technology also reported a more robust demand from data centers due to the remote-work economy, increased gaming, and e-commerce activity. Additionally, as per Cloudscene, as of March 2024, there are 5,381 data centers in the United States, the most of any country worldwide. A further 521 are in Germany, while 514 are in the United Kingdom.

Miniaturization of electronic components has made it possible to build small portable and handheld computer devices that can be carried anywhere. As a result, smaller, lighter devices with high processing capacity are available on the market. They are becoming more wearable since components can be easily embedded (for example, in clothing bags) and carried for long periods. Components are shrinking, putting new demands on the design of the PCBs they are mounted on. NCAB Group is firmly committed to IPC's efforts in defining standards for ultra-dense Ultra HDI PCBs and anticipates being able to provide them to clients in 2023.

Surface mount technology (SMT) has emerged as a pivotal element in modern electronics manufacturing, eclipsing traditional through-hole methods with its myriad benefits. A standout advantage of SMT lies in its drastic reduction of necessary PCB drilling. Manufacturers slash both time and costs by sidestepping the drilling process, a notable boon for intricate, high-density boards. This shift streamlines production and trims labor and material expenses, bolstering the overall cost-effectiveness of the manufacturing process.

Surface mount technology has revolutionized the electronics manufacturing industry by enabling the production of smaller, more efficient, and cost-effective electronic devices. However, despite its numerous advantages, SMT is unsuitable for all applications. SMT is unsuitable for high-power and high-voltage components, such as transformers and power circuitry. These components generate heat and carry high electric loads, which SMT is not designed to handle effectively.

According to the US Congressional Budget Office, defense spending in the United States is predicted to increase yearly until 2033. Defense outlays in the United States amounted to USD 746 billion in 2023. The forecast predicts an increase in defense outlays up to USD 1.1 trillion in 2033.

Surface Mount Technology (SMT) Market Trends

Consumer Electronics End-user Industry Segment is Expected to Hold Significant Market Share

- In the automotive industry, SMT is used in Electronic Control Units (ECU), dashboard displays, radar and camera modules, Battery Management Systems (BMS), safety assistance systems, and more. SMT has emerged as a pivotal manufacturing process in the automotive application. Renowned for its efficiency, precision, and reliability, SMT is crucial in bolstering various automotive electronic products, including advanced driver-assistance systems (ADAS), infotainment systems, and vehicle control systems.

- In modern cars, the on-board control system acts as the vehicle's 'brain,' overseeing and harmonizing the functions of its electronic components. The on-board control system is crucial in their seamless operation, from navigation to audio and air conditioning. Central to the reliability of these control systems is SMT technology. This technology enables the precise mounting of minuscule electronic components on circuit boards, ensuring the systems operate efficiently and reliably.

- The Engine Control Unit (ECU) is the automotive electronic system's nucleus, overseeing critical operations like engine performance, transmission, and braking. Surface-mount technology (SMT) is essential in assembling microchips, resistors, capacitors, and other surface-mounted components onto the ECU.

- Furthermore, Artificial Intelligence technology is poised to see increased adoption in the automotive sector. The precision and efficiency of Surface Mount Technology (SMT) in electronic assembly are set to bolster the production of AI chips and processors. Consequently, automotive electronic products will have enhanced autonomous decision-making abilities, advancing intelligent driving and vehicle automation.

- As highlighted by the IEA, the global automotive industry is undergoing a significant transformation, with potentially far-reaching implications for the energy sector. According to projections, the rise of electrification is anticipated to result in a daily elimination of the need for 5 million barrels of oil by 2030.

- The IEA's report also revealed a substantial increase in electric vehicle sales, with 3.5 million units sold in 2023 compared to 2022, marking a 35% growth. Notably, over 250,000 new registrations were recorded weekly, and over 250,000 new registrations were recorded weekly throughout the year. In 2023, electric vehicles accounted for approximately 18% of all vehicles sold, a significant increase from 2% five years ago and 14% in 2022. These trends indicate that solid growth is expected to persist as the electric vehicle market matures. Additionally, it was projected that 70% of the electric vehicle stock in 2023 would consist of battery electric vehicles.

Asia Pacific is Expected to Witness Fastest Growth

- Asia-Pacific, particularly countries like Japan, China, South Korea, Taiwan, and Southeast Asia, has become a global hub for electronics manufacturing. The region's robust manufacturing infrastructure, skilled labor force, and supportive government policies attract multinational corporations and promote the growth of local electronics industries. Demand for tablets, smartphones, and other electronic devices continues to grow, necessitating efficient and high-volume production capabilities by surface mount technology. The company projects that by implementing SMT (Surface Mount Technology) locally, the value addition will increase to 25% from the current 15%.

- For instance, in August 2023, the Indian government is actively engaging with global electronics firms to ramp up local value addition in products assembled in India, targeting a significant increase of 60-80% over the next five to ten years. To achieve this, the government is urging industries in India to adopt advanced production methods, like surface-mount technology (SMT) lines.

- Silicon Carbide (SiC) is increasingly in the spotlight for its high-temperature resilience, superior electrical conductivity, and remarkable energy efficiency. As the demand for electric vehicles (EVs), solar panels, and advanced power management rises with Industry 4.0, SiC manufacturing's significance has heightened. Wide Band Gap conductors are a natural fit given the imperative for minimal power consumption in these sectors.

- In February 2024, Continental Device India Limited (CDIL) took a significant step by inaugurating a new assembly line specifically for SiC Surface Mount Technology (SMT) components. This move positions CDIL as India's pioneer in SiC component manufacturing. With this enhancement, CDIL can now produce a range of auto-grade devices, such as SiC Schottky Diodes, SiC MOSFETs, Zeners, Rectifiers, and TVS Diodes, catering to both global and domestic markets.

- In April 2024, TDK Corporation introduced the B40910 series, a line of hybrid polymer capacitors designed to handle up to 4.6 A (at 100 kHz and +125 °C). These surface mount components boast impressively low ESR values of 17 mΩ and 22 mΩ at room temperature.

- Notably, unlike standard electrolytic capacitors with liquid electrolytes, the ESR of TDK's capacitors shows minimal variation with temperature. These compact components, measuring 10 x 10.2 mm or 10 x 12.5 mm (D x H), feature a rated voltage of 63 V and offer capacitances ranging from 82 µF to 120 µF. Thus, SMT manufacturers drive the need for the technology by integrating and innovating technologies. These efforts contribute to the widespread adoption and growth of surface mount technology (SMT) in various industries.

Surface Mount Technology (SMT) Industry Overview

Surface Mount Technology market is highly fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are Fuji Corporation, Yamaha Motor Co. Ltd, Mycronic AB, ASMPT, and Panasonic Corporation. Players in the market are adopting partnerships and acquisitions to enhance their product offerings and gain competitive advantage.

March 2024 - Nordson Corporation introduced a new Latin America Tech Center based in Queretaro, Mexico, to allow manufacturers in the region to get timely feedback on the best fluid dispensing equipment for their assembly fluid, parts, substrates, and production requirements. The lab has a 3D printer, scales, and other measurement equipment to determine the correct fluid dispensing equipment for each customer's unique application requirements.

January 2024 - Yamaha Motor Co. Ltd announced the launch of YRM10, a surface mounter with the title of being the fastest in its class regarding mounting performance. With an impressive speed of 52,000 CPH, it outshines its competitors in the 1-Beam/1-Head category. This device is compact and space-saving and offers a range of component compatibility and versatility, making it a next-generation solution for high-speed modular assembly.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Surface Mount Technology Market

5 MARKET DYNAMICS

- 5.1 Rising Demand For Miniaturization of Technology

- 5.1.1 Fewer Holes Required to Drill on PCBs Compared to Other Technologies

- 5.2 Market Challenges

- 5.2.1 SMT is Unsuitable for Any Large, High-Power and High-Voltage Parts and Parts Undergoing Frequent Mechanical Stress

- 5.2.2 High Initial Cost and Rework Issues

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Passive Components

- 6.1.1.1 Resistors

- 6.1.1.2 Capacitors

- 6.1.2 Active Components

- 6.1.2.1 Transistors

- 6.1.2.2 Integrated Circuits

- 6.1.1 Passive Components

- 6.2 By End-user Industry

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 Industrial Electronics

- 6.2.4 Aerospace and Defense

- 6.2.5 Healthcare

- 6.2.6 Other End-user Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fuji Corporation

- 7.1.2 Yamaha Motor Co. Ltd

- 7.1.3 Mycronic AB

- 7.1.4 ASMPT

- 7.1.5 Panasonic Corporation

- 7.1.6 Nordson Corporation

- 7.1.7 Juki Corporation

- 7.1.8 Hanwa Precision Machinery Co. Ltd

- 7.1.9 Zhejiang Neoden Technology Co. Ltd

- 7.1.10 Europlacer Limited

- 7.1.11 Viscom SE