|

市場調査レポート

商品コード

1437598

装甲車両ナビゲーションシステムの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Armored Vehicle Navigation Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 装甲車両ナビゲーションシステムの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

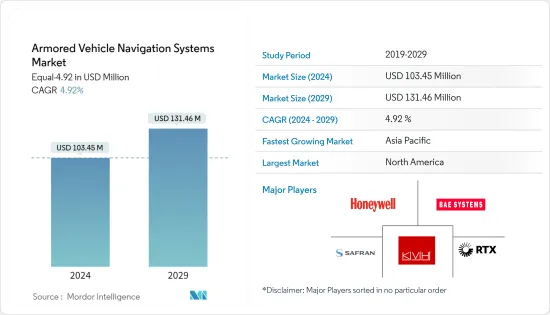

世界の装甲車両ナビゲーションシステムの市場規模は、2024年に1億345万米ドルと推定され、2029年には1億3,146万米ドルに達し、予測期間中(2024年~2029年)にCAGR4.92%で成長すると予測されています。

世界の防衛費の増加により、装甲車両ナビゲーションシステム市場が促進されています。米国、フランス、ロシアなどの主要国やインド、中国などの新興国は防衛費を急増させています。これらの国は装甲車両の開発と調達に多額の投資を行っています。さらに、艦隊の戦闘範囲と戦闘効率を向上させるために、装甲車両ナビゲーションシステムの分野で大幅な開発が行われています。人工知能や自動運転車両技術などの技術の開発と実装により、装甲車両ナビゲーションシステム市場の成長が推進されています。

装甲車両ナビゲーションシステム市場動向

最も高い成長率を示す慣性ナビゲーションシステム

世界中の主要な軍隊は、戦場における戦闘車両部隊の状況認識を向上させる取り組みを強化しており、これが慣性ナビゲーションシステムの大幅な改善につながっています。衛星測位システムと慣性ナビゲーションシステムの統合により、世界の装甲車両ナビゲーションシステム市場の成長が推進されています。 GPSが拒否されたゾーンでも正確に動作できる既存の慣性ナビゲーション技術を改善するために投資が行われています。慣性ナビゲーションシステムは、妨害やなりすましの影響を受けやすいGPSシステムとは異なり、安全かつ正確です。センサー技術の開発は慣性ナビゲーションシステム開発の中核を成します。たとえば、2023年11月、スウェーデンに本拠を置く企業Kebni ABは、新たな産業協力の一環として、RV ConnexからKebni SensAItion慣性ナビゲーションシステム(INS)のテストユニットを受注しました。この注文は、高度な用途におけるナビゲーションサポートの評価を目的としたテストユニットに関するものです。

センサーの使用の増加により、装甲車両ナビゲーションシステムの重量とスペースを削減する設計が促進されています。センサーと光ファイバージャイロ(FOG)は、慣性ナビゲーションシステムの不安定性を軽減し、信頼性を高めます。 FOGシステムは、自動運転車への応用により、予測期間中に高い成長率を示すと予想されます。

アジア太平洋は予測期間中に大幅な成長が見込まれる

アジア太平洋には日本、中国、インド、韓国などの軍事大国があり、これらの国々は国境紛争の上昇や地域のテロにより、装甲車両や装甲車両ナビゲーションシステムの調達と開発のための国防支出を大幅に増加させています。この地域での装甲車両の調達は、ナビゲーションシステムの需要を助けています。たとえば、2022年12月、日本の防衛省は、陸上自衛隊(JGSDF)の装輪装甲兵員輸送車(WAPC)プログラム向けに、フィンランド企業パトリアの装甲モジュラー車両(AMV)を調達する5か年計画の概要を発表しました。同国は29台、1億7,600万米ドル相当の車両を調達する計画を立てています。同様に、2023年9月にインド国防省は、無限軌道プラットフォームをベースとした170台の装甲回収車両(ARV)の調達を開始しました。これらの発展は、アジア太平洋の市場を支援すると期待されています。

装甲車両ナビゲーションシステム業界の概要

装甲車両ナビゲーションシステムの市場は半統合市場であり、Honeywell International Inc.、KVH Industries Inc.、Safran SA、RTX Corporation、BAE Systems PLCなどの大手企業が存在します。市場では、競争力のある低料金で提供できる、イノベーションと精密なテクノロジーの開発への投資が行われています。収益創出のために、大手企業は各国政府や防衛機関からの契約や取引を獲得することを目指しています。この市場は、世界中の主要経済国による防衛の近代化とアップグレードの取り組みにより、成長が見込まれています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 装甲車両タイプ

- 主力戦車

- 歩兵戦闘車

- 装甲兵員輸送車

- その他の装甲車両タイプ(戦術トラック、バス、MRAP)

- ナビゲーションシステム

- 慣性ナビゲーションシステム

- 衛星ナビゲーションシステム

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋

- ラテンアメリカ

- メキシコ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- その他中東・アフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Safran SA

- KVH Industries Inc.

- Hertz Systems

- Israel Aerospace Industries Ltd

- Bharat Electronics Limited(BEL)

- Advanced Navigation

- Honeywell International Inc.

- GEM elettronica

- BAE Systems PLC

- Northrop Grumman Corporation

- THALES

- RTX Corporation

第7章 市場機会と将来の動向

The Armored Vehicle Navigation Systems Market size is estimated at USD 103.45 million in 2024, and is expected to reach USD 131.46 million by 2029, growing at a CAGR of 4.92% during the forecast period (2024-2029).

The increase in defense expenditure globally has propelled the armored vehicle navigation system market. The major economies, such as the United States, France, and Russia, and emerging economies, such as India and China, have surged their defense expenditures. These countries are heavily investing in the development and procurement of armored vehicles. Moreover, to give fleets increased battle ranges and combat effectiveness, substantial developments are being made in the field of armored vehicle navigation systems. Development and implementation of technologies, such as artificial intelligence and autonomous vehicle technology, are propelling the growth of the market for armored vehicle navigation systems.

Armored Vehicle Navigation Systems Market Trends

Inertial Navigation Systems to Exhibit the Highest Growth Rate

Major military forces across the world are increasing their efforts to improve the situational awareness of combat vehicle units on the battlefield, and this is leading to significant improvements in inertial navigation systems. The integration of satellite positioning systems with inertial navigation systems is propelling the growth of the global armored vehicle navigation systems market. Investments are being made to improve the existing inertial navigation technology that can work precisely in GPS-denied zones. Inertial navigation systems are safe and accurate, unlike GPS systems that are prone to jamming and spoofing. Development in sensor technology stands at the core of inertial navigation system development. For instance, in November 2023, Kebni AB, a Sweden-based firm, was awarded an order for a test unit of Kebni SensAItion inertial navigation systems (INS) from RV Connex as part of a new industrial cooperation. The order pertains to a test unit intended for the evaluation of navigational support in advanced applications.

The increasing use of sensors is fueling the weight- and space-reduction design of armored vehicle navigation systems. Sensors and Fiber Optic Gyros (FOG) reduce the instability of inertial navigation systems and make them more reliable. FOG systems are expected to witness a high growth rate during the forecast period, owing to their autonomous vehicle applications.

Asia-Pacific is Projected to Significant Growth During the Forecast Period

Asia-Pacific is home to major military powers, such as Japan, China, India, and South Korea, and these countries are significantly increasing their defense expenditures for the procurement and development of armored vehicles and armored vehicle navigation systems, owing to the rising border conflicts and terrorism in the region. The procurement of armored vehicles in the region has aided the demand for its navigation systems. For instance, in December 2022, the Japanese Ministry of Defense outlined a five-year plan for the procurement of Finnish company Patria's armored modular vehicles (AMVs) for the Japan Ground Self-Defense Force's (JGSDF's) wheeled armored personnel carrier (WAPC) program. The country has plans to procure 29 vehicles worth USD 176 million. Similarly, in September 2023, the Indian Ministry of Defense initiated the procurement of 170 armored recovery vehicles (ARVs) based on a tracked platform. These developments are expected to aid the market in the Asia-Pacific region.

Armored Vehicle Navigation Systems Industry Overview

The market for armored vehicle navigation systems is a semi-consolidated one, with a presence of major players, such as Honeywell International Inc., KVH Industries Inc., Safran SA, RTX Corporation, and BAE Systems PLC. The market is witnessing investments in innovations and the development of precise technology that can be offered at low, competitive rates. For revenue generation, major players aim to win contracts and deals from national governments and defense agencies. The market is expected to see growth, owing to the defense modernization and upgrade efforts by major economies around the world.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Armored Vehicle Type

- 5.1.1 Main Battle Tanks

- 5.1.2 Infantry Fighting Vehicle

- 5.1.3 Armored Personnel Carrier

- 5.1.4 Other Armored Vehicle Types (Tactical Truck, Bus, MRAP)

- 5.2 Navigation System

- 5.2.1 Inertial Navigation System

- 5.2.2 Satellite Navigation System

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Mexico

- 5.3.4.2 Brazil

- 5.3.4.3 Rest Of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Safran SA

- 6.2.2 KVH Industries Inc.

- 6.2.3 Hertz Systems

- 6.2.4 Israel Aerospace Industries Ltd

- 6.2.5 Bharat Electronics Limited (BEL)

- 6.2.6 Advanced Navigation

- 6.2.7 Honeywell International Inc.

- 6.2.8 GEM elettronica

- 6.2.9 BAE Systems PLC

- 6.2.10 Northrop Grumman Corporation

- 6.2.11 THALES

- 6.2.12 RTX Corporation