|

市場調査レポート

商品コード

1690704

電子線硬化型コーティング:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Electron Beam Curable Coating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電子線硬化型コーティング:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

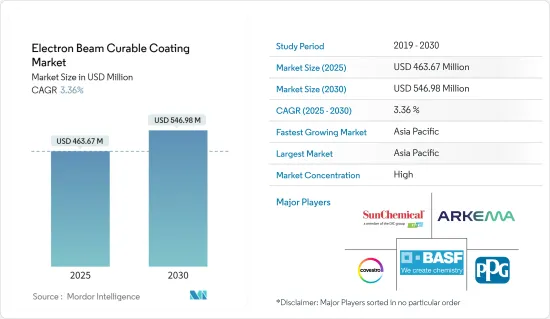

電子線硬化型コーティング市場規模は、2025年に4億6,367万米ドルと推定され、2030年には5億4,698万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは3.36%です。

COVID-19のパンデミックは、電子線硬化型コーティング市場の妨げとなりました。いくつかの国で全国的な封鎖が行われ、厳しい社会的遠ざけ措置が取られたため、航空宇宙、電気・電子、自動車、包装などのエンドユーザー産業が影響を受け、それによって市場も影響を受けました。しかし、規制が解除された後は、包装、電気・電子産業からの需要が回復したため、市場は大きな成長率を記録しました。

主要ハイライト

- 包装産業における製品需要の増加と航空宇宙産業における製品人気の高まりが、電子線硬化型コーティング市場を牽引すると予想されます。

- 電子線硬化型コーティングの製造コストが高いことが市場成長の妨げになると予想されます。

- 電気自動車セグメントからの需要の増加は、2024~2029年の間に市場に機会を創出すると予想されます。

- アジア太平洋が支配的な市場に浮上しました。また、この地域の拡大するエンドユーザー産業からの高い需要により、2024~2029年にかけて最も高いCAGRで推移すると予想されます。

電子線硬化型コーティング市場の動向

包装産業からの需要の増加

- 電子線硬化型コーティングは、クリーンで高速かつエネルギー効率の高い処理方法であるため、軟包装用途に広く採用されています。人口の増加、持続可能性への関心の高まり、最近の動向における消費力の増加、スマート包装に対する需要の高まりにより、包装ソリューションに対する需要は最近増加しています。

- 健康と安全は多くの企業にとって最優先事項となっており、その結果、食品や消費財メーカーによる保護包装や改ざん防止包装の需要が高まっています。保護・改ざん防止包装材により、企業は現在の包装容器の安全性を向上させることができ、また消費者は製品が危害を加えられたり改ざんされたりした場合に素早く識別することができます。

- さらに、デジタル化の急増を背景にeコマース産業が大きく成長する中、包装産業は世界中で急成長を遂げています。インド包装協会によると、インドの包装消費は過去10年間で200%増加し、2025年には2,048億1,000万米ドルに達すると予想されています。

- さらに、ドイツ国内のeコマースの大幅な増加や海外輸出の増加により、ドイツの包装産業も急成長しています。さらに、包装された食品や飲食品への嗜好の高まりも、包装産業の成長につながっています。

- 英国では、デザインの改善と技術革新が、包装にリサイクル可能な材料を使用する方向へのシフトと相まって、市場成長の多くの機会を提供すると期待されています。これにより、新製品を市場に投入する可能性が広がると期待されています。英国の包装製造業の年間売上高は110億英ポンド(約136億米ドル)です。政府の数字によると、同国では年間200万トン以上のプラスチック包装(主要製品セグメント)が使用されています。

- 米国では、飲食品市場の成長が同国の包装市場を後押ししています。産業レポートによると、食品産業からの収益は2024年に1兆109億7,000万米ドルに達すると予想されています。この収益は3.81%以上のCAGR(2024~2028年)を記録し、2028年には1兆1,737億4,000万米ドルの市場規模が予測されます。これにより、包装産業における電子線硬化型コーティング剤の需要が増加し、2024~2029年にかけて調査された市場が押し上げられると予想されます。

- したがって、前述の要因と近い将来における包装産業の成長は、2024~2029年にかけて電子線硬化型コーティング剤の市場需要を押し上げると予想されます。

アジア太平洋が市場を独占する見込み

- 2024~2029年にかけて、アジア太平洋が電子線硬化型コーティングの市場を独占すると予想されます。この地域では、中国、インド、日本が電子線硬化型コーティングの需要を牽引すると予想されます。

- 電子線硬化型コーティングは、インライン基板と多次元基板の両方に対して、大幅に縮小されたフットプリントで室温・色盲硬化を実現するという独自の利点を提供するため、よく知られ、有利な立場にあります。これにより、輸送産業における自動車軽量化規格に準拠するために設計された新しいプロセスを加速する機会が得られます。中国は世界で最も重要な自動車生産拠点です。2023年の自動車総生産台数は3,016万966台で、昨年の2,702万615台に比べ11.6%増加しました。国際貿易局(ITA)によると、国内の自動車生産台数は2025年までに3,500万台に達すると予想されています。

- 中国の包装産業は、世界の重要な包装産業のひとつです。同国の包装産業は成長が見込まれています。中国政府が発表した報告書では、2025年までに同産業の評価額が2兆人民元(2,900億米ドル)に達すると予測されています。

- インドでは、包装は同国で5番目に大きな産業であり、最も急速に成長しているセグメントのひとつでもあります。インドにおける包装製品の消費量は過去10年間で200%増加し、1人当たり年間4.3kgから8.6kgに増加しています。また、インド包装工業協会(PIAI)によると、包装部門はCAGR22%から25%近い成長率を示しています。同様に、インド貿易促進評議会によると、インドの包装産業は著しい成長を遂げており、2025年までに2,048億米ドルに達すると予想されています。

- さらに、日本の包装産業は、軟包装の人気の高まりにより、今後数年間で成長を示すことが期待されています。現在の市場シナリオでは、日本は包装材料の一人当たり消費量が世界で最も多いです。アジアでは、日本は中国に次いで包装食品の消費シェアが高いです。

- 日本ではエレクトロニクス産業が成長しています。電子情報技術産業協会(JEITA)によると、2023年12月の産業用電子機器の生産額は2,935億7,700万円(20億8,085万米ドル)で、毎年ほぼ100%増加しています。また、民生用電子機器の生産額は2023年12月に357億7,500万円(2億5,357万米ドル)となり、前年同期比112.2%の大幅増となりました。

- 上記の要因から、アジア太平洋が2024~2029年の間に市場を独占すると予想されます。

電子線硬化型コーティング産業概要

電子線硬化型コーティング市場は、その性質上、統合されています。同市場の主要企業には、Arkema、BASF SE、PPG Industries Inc.、Sun Chemical、Covestro AGなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 包装産業における製品需要の増加

- 航空宇宙産業における製品の人気上昇

- 抑制要因

- 生産コストの上昇

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 電気・電子

- 自動車

- 包装

- その他のエンドユーザー産業(バッテリー)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Abrisa Technologies

- Allnex GmbH

- Arkema

- BASF SE

- Beckers Group

- Cork Industries Inc.

- Covestro AG

- Dai Nippon Printing Co. Ltd

- Dainichiseika Color & Chemicals MFG Co. Ltd

- Estron

- IGM Resins BV

- INX International Ink Co.

- Polytex Environmental Inks

- PPG Industries Inc.

- R&D Coatings LLC

- Sun Chemical

第7章 市場機会と今後の動向

- 電気自動車セグメントからの需要増加

The Electron Beam Curable Coating Market size is estimated at USD 463.67 million in 2025, and is expected to reach USD 546.98 million by 2030, at a CAGR of 3.36% during the forecast period (2025-2030).

The COVID-19 pandemic hampered the electron beam curable coating market as nationwide lockdowns in several countries and strict social distancing measures affected the end-user industries such as aerospace, electrical and electronics, automotive, and packaging, thereby affecting the market. However, the market registered a significant growth rate after the restrictions were lifted due to the recovering demand from the packaging, electrical, and electronic industries.

Key Highlights

- The increasing product demand in the packaging industry and the rising product popularity in the aerospace industry are expected to drive the market for electron beam curable coating.

- Higher production costs of electron beam curable coatings are expected to hinder the market's growth.

- The increasing demand from the electric vehicles segment is expected to create opportunities for the market between 2024 and 2029.

- Asia-Pacific emerged as the dominant market. It is also expected to register the highest CAGR from 2024 to 2029 due to the high demand from the expanding end-user industries in the region.

Electron Beam Curable Coating Market Trends

Increasing Demand from the Packaging Industry

- Electron beam curable coatings are widely adopted in flexible packaging applications owing to their clean, fast, and energy-efficient way of processing. With the increasing population, growing sustainability concerns, more spending power in developing regions, and the growing demand for smart packaging, the demand for packaging solutions has been increasing recently.

- Health and safety have become a top priority for many businesses, resulting in the increasing demand for protective and tamper-evident packaging from food and consumer goods manufacturers. Protective and tamper-evident packaging materials enable businesses to improve the safety of their current packaging containers while also allowing consumers to quickly identify if their products have been compromised or tampered with.

- Additionally, amid the significant growth in the e-commerce industry backed by a surge in digitalization, the packaging industry is witnessing sharp growth across the world. According to the Indian Institute of Packaging, packaging consumption in India increased by 200% in the past decade and is expected to reach USD 204.81 billion by 2025.

- Furthermore, the packaging industry in Germany is also growing at a rapid pace, owing to the huge increase in domestic e-commerce and the rise in foreign exports. In addition, the increasing preference for packaged food and beverages is also leading to the growth of the packaging industry.

- In the United Kingdom, design improvements and innovation, combined with a shifting focus toward the usage of recyclable materials for packaging, are expected to offer numerous opportunities for market growth. This is expected to open up the possibility of launching new products into the market. The UK packaging manufacturing industry has annual sales of GBP 11 billion (~USD 13.6 billion). According to government figures, more than 2 million metric tons of plastic packaging (the leading product segment) are used in the country annually.

- In the United States, the growing food and beverage market is boosting the country's packaging market. According to the industry report, the revenue from the food industry is expected to reach USD 1,010.97 billion in 2024. The revenue is expected to register a CAGR of over 3.81% (2024-2028), resulting in a projected market value of USD 1,173.74 billion by 2028. This is expected to increase the demand for electron beam curable coatings in the packaging industry, thereby boosting the market studied between 2024 and 2029.

- Hence, the aforementioned factors and growth in the packaging industry in the near future are expected to boost the market demand for electron beam curable coatings from 2024 to 2029.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific is expected to dominate the market for electron beam curable coating between 2024 and 2029. China, India, and Japan are expected to drive the demand for electron beam curable coating in this region.

- The electron beam curing process for coatings is well-known and well-positioned, as it offers the unique advantage of delivering room-temperature, color-blind curing for both inline and multidimensional substrates within greatly reduced footprints. This enables opportunities to accelerate new processes designed for compliance with the automotive light-weighting standards within the transportation industry. China has the most significant automotive production base in the world. In 2023, total vehicle production was 30,160,966 units, an increase of 11.6% compared to 27,020,615 units produced last year. According to the International Trade Administration (ITA), domestic automotive production is expected to reach 35 million units by 2025.

- The Chinese packaging industry is one of the significant global packaging industries. The packaging industry in the country is expected to grow. The report published by the Chinese government foresees the industry achieving a valuation of CNY 2 trillion (USD 290 billion) by 2025.

- In India, packaging is the 5th largest industry in the country and is also one of the fastest-growing sectors. The consumption of packaging products in India has increased by 200% over the last decade, rising from 4.3 kg per person per year to 8.6 kg per person per year. Also, as per the Packaging Industry Association of India (PIAI), the packaging sector is growing at a CAGR of nearly 22% to 25%. Similarly, according to the Trade Promotion Council of India, the Indian packaging industry is experiencing remarkable growth and is expected to reach USD 204.8 billion by 2025.

- Moreover, the Japanese packaging industry is expected to witness growth in the coming years, owing to the increasing popularity of flexible packaging. In the present market scenario, Japan has the highest per capita consumption of packaging materials in the world. In Asia, Japan holds the second-highest packaged food consumption share, next to China.

- The electronics industry is growing in Japan. According to the Japan Electronics and Information Technology Industries (JEITA), the production value of industrial electronic devices stood at JPY 293,577 million (USD 2,080.85 million) in December 2023, increasing by almost 100% annually. Furthermore, the production value of consumer electronic equipment in the country stood at JPY 35,775 million (USD 253.57 million) in December 2023, increasing by a significant 112.2% during the same period last year.

- Owing to the above-mentioned factors, Asia-Pacific is expected to dominate the market between 2024 and 2029.

Electron Beam Curable Coating Industy Overview

The electron beam curable coating market is consolidated in nature. Some of the major players in the market are Arkema, BASF SE, PPG Industries Inc., Sun Chemical, and Covestro AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Product Demand in the Packaging Industry

- 4.1.2 Rising Product Popularity in the Aerospace Industry

- 4.2 Restraints

- 4.2.1 Higher Production Cost

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 End-user Industry

- 5.1.1 Aerospace

- 5.1.2 Electrical and Electronics

- 5.1.3 Automotive

- 5.1.4 Packaging

- 5.1.5 Other End-user Industries (Batteries)

- 5.2 Geography

- 5.2.1 Asia-pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Malaysia

- 5.2.1.6 Thailand

- 5.2.1.7 Indonesia

- 5.2.1.8 Vietnam

- 5.2.1.9 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Spain

- 5.2.3.6 Nordic Countries

- 5.2.3.7 Turkey

- 5.2.3.8 Russia

- 5.2.3.9 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 Qatar

- 5.2.5.3 United Arab Emirates

- 5.2.5.4 Nigeria

- 5.2.5.5 Egypt

- 5.2.5.6 South Africa

- 5.2.5.7 Rest of Middle East and Africa

- 5.2.1 Asia-pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers And Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Abrisa Technologies

- 6.4.2 Allnex GmbH

- 6.4.3 Arkema

- 6.4.4 BASF SE

- 6.4.5 Beckers Group

- 6.4.6 Cork Industries Inc.

- 6.4.7 Covestro AG

- 6.4.8 Dai Nippon Printing Co. Ltd

- 6.4.9 Dainichiseika Color & Chemicals MFG Co. Ltd

- 6.4.10 Estron

- 6.4.11 IGM Resins BV

- 6.4.12 INX International Ink Co.

- 6.4.13 Polytex Environmental Inks

- 6.4.14 PPG Industries Inc.

- 6.4.15 R&D Coatings LLC

- 6.4.16 Sun Chemical

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand from the Electric Vehicles Segment