|

市場調査レポート

商品コード

1687922

航空宇宙・防衛分野のM&A-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Mergers And Acquisitions (M&A) In Aerospace And Defense - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空宇宙・防衛分野のM&A-市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

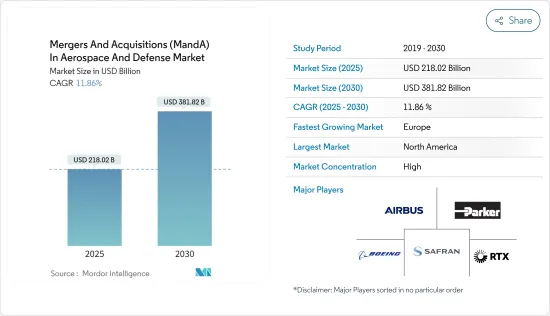

航空宇宙・防衛セグメントのM&A市場規模は、2025年に2,180億2,000万米ドルと推定され、2030年には3,818億2,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは11.86%です。

航空宇宙・防衛(A& D)セグメントのM&Aは、商業的に実行可能なビジネス戦略として台頭してきました。M&Aは、参加企業が技術的なノウハウを強化する一方で、技術的な混乱に伴うリスクを分担するのに役立ちます。M&Aは両社の存続を容易にし、ほとんどの場合、大手企業が競合他社よりも比較的速い成長を促進するのに役立っています。

近年、航空宇宙・防衛セグメントは目覚ましい成長を遂げています。航空交通量の増加、都市化の進展、航空機数の増加は、航空宇宙部門の重要な原動力の一部です。防衛予算の増加、軍事力強化への注目の高まり、戦況の高まりは、防衛セグメントの市場成長を後押ししています。両部門の支出の増加は、相手先商標製品メーカーや小規模参入企業が市場に参入し、事業を拡大するためのより良い機会を創出します。このため、航空宇宙・防衛セグメントの主要企業は、M&A、新規契約、協定、提携など、さまざまな戦略を通じて事業拡大に注力しています。

航空宇宙・防衛セグメントではM&Aに関する開発がいくつか行われているが、M&Aに関連する規制の高まりが長期的には市場の成長を妨げる可能性があります。航空宇宙・防衛セグメントのM&Aを規制するために、さまざまな規制が実施されています。連邦政府が存在する国では、M&Aに関する規制は連邦政府だけでなく、対象企業が法人化されている各州の管轄下にあります。こうした要因にもかかわらず、航空旅客輸送量の増加、航空機の新規納入、地政学的緊張の高まり、それに対応する新たな技術革新が市場の成長を支えるものと予想されます。

航空宇宙・防衛市場のM&A動向

予測期間中、航空宇宙セグメントが最も高い成長を遂げると予測

航空宇宙セグメントは近年、技術やイノベーションの著しい進歩によって顕著な拡大を経験してきました。しかし、パンデミック(世界的大流行)により航空旅客数が激減し、航空機需要が大幅に減少したため、同部門は未曾有の課題に直面しました。それにもかかわらず、このセクターは驚異的な回復力を示し、パンデミック後の2022年と2023年には力強い回復を見せた。

航空宇宙セクターの発展に伴い、大手企業は買収による事業拡大に注力しています。こうした戦略的イニシアチブは、自社の能力を強化し、市場での地位を向上させ、競争の激しい世界市場での成長を促進することを目的としています。例えば、2024年2月、BAE Systems PLCはBall CorporationからBall Aerospaceを55億米ドルで買収しました。この買収により、BAE Systemsは新たな宇宙・ミッションシステム部門のもと、科学、宇宙、防衛の機能をポートフォリオに加えることになります。同様に、2022年9月、モーションコントロール技術企業のParker-Hannifin Corp.は、航空宇宙・防衛部品メーカーのメギットPLCの買収を約63億英ポンドで完了しました。この買収により、Parker Aerospace Groupは、メギットの世界の防衛・航空宇宙技術でポートフォリオを拡大することを目指しています。

買収以外にも、さまざまな航空宇宙企業が世界市場での地位を固めるために合併に関与しています。例えば、2024年3月、XTI Aircraft CompanyとInpixonは事業部門を合併し、XTI Aerospace Inc.を設立しました。この合併により、両社はTriFan 600 Vertical Lift Crossover Airplaneで民間航空輸送に革命を起こすことに注力しています。同様に、2024年1月、Vistaraは、Tata Group傘下のAir Indiaとの合併案について、すべての法的承認を受ける見込みであると発表しました。この手続きは2024年前半までに完了する予定です。この合併は2022年11月にシンガポール航空が提案していました。このように、航空宇宙企業が新興企業や他社の事業領域の買収に力を入れるようになっていることが、予測期間中の市場の成長を促進すると予想されます。

予測期間中、欧州が最も高い成長を示す見込み

予測期間中、欧州が最も高い成長を記録すると予想されます。欧州は、エンドユーザーからの膨大な需要と、この地域のトップ航空・防衛企業の存在により、航空・防衛セグメントが十分に栄えています。Airbus SE、Saab AB、THALES、BAE Systems、Dassault Aviation SA、Safran SAは、航空宇宙・防衛セグメントで大きなシェアを持つ主要企業です。

航空旅行者の増加、新空港建設の増加、航空機納入の増加が、地域民間航空市場を牽引しています。ビジネスジェット機や一般旅客機に対する需要の高まりや、多くの用途に使用されるヘリコプターの調達増が航空セクターを牽引しています。

航空宇宙セグメントの主要企業は、事業拡大のためにM&Aに注力しています。例えば、2023年1月、Airbus Helicoptersはドイツを拠点とするZF Luftfahrttechnikの買収を完了しました。同社は世界の顧客基盤を持ち、関連サービスを含め、小型・中型ヘリコプター用のダイナミックコンポーネントを製造しています。また、同社は軍用ヘリコプターのMRO部品サプライヤーでもあります。この買収により、Airbus HelicoptersはMRO能力の範囲を拡大し、ダイナミックシステムのさらなる能力を確保しました。

また、2022年4月、Airbus Defence and SpaceはDSI Datensicherheit GmbH(DSI DS)の買収を発表しました。ドイツを拠点とするこの会社は、連邦情報セキュリティ局(BSI)の認証を受けた、航空、宇宙、海軍、地上向けの暗号と通信システムを提供しています。同社は、Aerospace Data Security GmbHという新しい社名で運営されます。この買収は、Airbusの暗号技術を強化し、エンド・ツー・エンドの安全なシステム開発を向上させています。

国境を越えた紛争、政治的紛争、近隣諸国間の緊張の高まりは、欧州に戦火をもたらしました。ロシア・ウクライナ戦争やNATO諸国による防衛力強化のための支出の増加は、この地域全体の市場の成長を助けた。例えば、2024年2月、THALESはCobham Aerospace Communicationsを11億米ドルで買収しました。THALESはこの買収を通じて、コネクテッドコックピットへの大きな動向を生み出すと期待されています。

このように、製品ポートフォリオを拡大するためにベンダーや他社からの事業調達への支出が増加することで、企業全体の業績や顧客基盤が改善され、予測期間中の市場の成長が促進されると予想されます。

航空宇宙・防衛産業の合併・買収(M&A)概要

航空宇宙・防衛産業は複数の参入企業で構成されており、市場競争は激しいです。同市場の有力企業には、Parker Hannifin Corporation、The Boeing Company、Airbus SE、RTX Corporation、Safranなどがあります。

各社は、重要な契約を獲得し、市場での存在感と優位性を高めるため、積極的な買収戦略を採用しています。多角的な成長戦略は、その国特有の景気低迷から企業を守る。このことが、市場の競争優位性を獲得するために、市場の既存企業が複数の競合製品ポートフォリオを買収する引き金となっています。さらに、2024年度末までに他のいくつかのM&A取引が完了する見込みであり、その結果、市場は大幅に統合されることになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 分野

- 航空宇宙

- 防衛

- 地域

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- The Boeing Company

- RTX Corporation

- Airbus SE

- General Electric Company

- Safran SA

- BAE Systems PLC

- Parker Hannifin Corporation

- L3Harris Technologies Inc.

- Leonardo SpA

- THALES

- Elbit Systems Ltd

- Rolls-Royce PLC

- Honeywell International Inc.

- Rheinmetall AG

第7章 市場機会と今後の動向

The Mergers And Acquisitions In Aerospace And Defense Market size is estimated at USD 218.02 billion in 2025, and is expected to reach USD 381.82 billion by 2030, at a CAGR of 11.86% during the forecast period (2025-2030).

Mergers and acquisitions (M&A) in the aerospace and defense (A&D) sector have emerged as a commercially viable business strategy. They help the participants enhance their technological know-how while dividing the risks associated with technological disruptions. An M&A facilitates the sustenance of both firms and, in most cases, helps the major players foster comparatively faster growth than their competitors.

In recent years, the aerospace and defense sector has showcased tremendous growth. The increasing air traffic, growing urbanization, and the rising number of aircraft are some of the critical drivers of the aerospace sector. The growing defense budget, increasing focus on strengthening military capabilities, and rising war situations are boosting the market's growth in the defense sector. Increasing expenditure in both sectors will create better opportunities for original equipment manufacturers and small players to enter the market and expand their operations. Thus, key players in the aerospace and defense sector focus on business expansion through various strategies, such as mergers and acquisitions, new contracts, agreements, and partnerships.

Although there have been several developments in mergers and associations in the aerospace and defense sector, rising regulations associated with mergers and acquisitions may hamper the market's growth in the long run. Various regulations have been implemented to regulate mergers and acquisitions within the aerospace and defense sector. In countries with a federal government, the regulations for merger and acquisition activities fall within the dual jurisdiction of the federal government as well as the individual state in which the target company has been incorporated. Despite these factors, rising air passenger traffic, new aircraft deliveries, rising geopolitical tensions, and corresponding new technological innovations are expected to support the market's growth.

Mergers And Acquisitions (M&A) In Aerospace And Defense Market Trends

The Aerospace Segment is Projected to Witness the Highest Growth During the Forecast Period

The aerospace sector has experienced a notable expansion in recent years, marked by significant advancements in technology and innovation. The sector, however, encountered unprecedented challenges due to the pandemic, which resulted in sharp declines in air travel and a significant decrease in demand for aircraft. Nevertheless, the sector demonstrated remarkable resilience and a strong recovery post-pandemic in 2022 and 2023.

As the aerospace sector evolves, major companies focus on business expansion through acquisitions. These strategic initiatives aim to enhance their capabilities, improve their market position, and drive growth in the highly competitive global market. For instance, in February 2024, BAE Systems PLC completed the acquisition of Ball Aerospace from Ball Corporation for USD 5.5 billion. Through this acquisition, BAE Systems will add science, space, and defense capabilities to its portfolio under the new Space and Mission Systems division. Similarly, in September 2022, Parker-Hannifin Corp., a motion and control technologies company, completed the acquisition of Meggitt PLC, an aerospace and defense components manufacturer, for approximately GBP 6.3 billion. With this acquisition, the Parker Aerospace Group aims to expand its portfolio with Meggitt's global defense and aerospace technologies.

Apart from acquisitions, various aerospace companies have been involved in mergers to solidify their position in the global market. For instance, in March 2024, XTI Aircraft Company and Inpixon merged their business units to form XTI Aerospace Inc. Through this merger, the companies are focusing on revolutionizing private air transportation with its TriFan 600 Vertical Lift Crossover Airplane. Similarly, in January 2024, Vistara announced that it expects to receive all legal approvals for its proposed merger with Tata Group-owned Air India. The process is expected to be completed by the first half of 2024. The merger was proposed by Singapore Airlines in November 2022. Thus, the increasing focus of aerospace companies to acquire start-ups or business domains of other companies is expected to drive the market's growth during the forecast period.

Europe is Expected to Exhibit the Highest Growth During the Forecast Period

Europe is expected to record highest growth during the forecast period. Europe has a well-flourished aviation and defense sector due to the massive demand from end users and the presence of top aviation and defense companies in the region. Airbus SE, Saab AB, THALES, BAE Systems, Dassault Aviation SA, and Safran SA are major players with significant market shares in the aerospace and defense sector.

An increasing number of air travelers, the growing construction of new airports, and rising aircraft deliveries are driving the regional commercial aviation market. The rising demand for business jets and general aviation aircraft and increasing procurement of helicopters for numerous applications are driving the aviation sector.

The key players in the aerospace sector focus on mergers and acquisitions to expand their business. For instance, in January 2023, Airbus Helicopters completed the acquisition of German-based ZF Luftfahrttechnik. The company has a global customer base and manufactures dynamic components for light and medium helicopters, including related services. In addition, the company is the MRO components supplier for military helicopters. With this acquisition, Airbus Helicopters expanded its range of MRO capabilities and secured additional competencies in dynamic systems.

Also, in April 2022, Airbus Defence and Space announced the acquisition of DSI Datensicherheit GmbH (DSI DS). This German-based company provides cryptography and communication systems for airborne, space, naval, and ground, certified by the Federal Office for Information Security (BSI). The company will operate under a new name: Aerospace Data Security GmbH. The acquisition would strengthen Airbus' cryptography capabilities and improve the development of end-to-end secured systems.

Growing cross-border conflicts, political disputes, and tensions among neighboring countries created a warfare situation in Europe. The Russia-Ukraine War and the growing expenditure from NATO countries to enhance defense capabilities aided the market's growth across the region. For instance, in February 2024, THALES acquired Cobham Aerospace Communications for USD 1.1 billion. THALES is expected to create a significant trend toward connected cockpits through this acquisition.

Thus, increasing expenditure on procurement by vendors and businesses from other companies to expand product portfolios is expected to improve the company's overall performance and customer base, driving the market's growth during the forecast period.

Mergers And Acquisitions (M&A) In Aerospace And Defense Industry Overview

The A&D sector comprises several players, and the market is highly competitive. Some prominent players in the market include Parker Hannifin Corporation, The Boeing Company, Airbus SE, RTX Corporation, and Safran, amongst others.

Companies are adopting aggressive acquisition strategies to gain significant contracts and increase their market presence and dominance. A diversified growth strategy protects a firm from country-specific economic slumps. This has triggered market incumbents' acquisition of several competitor product portfolios to gain a competitive advantage in the market. Moreover, several other M&A transactions were expected to be completed by the end of FY 2024, resulting in substantial market consolidation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Sector

- 5.1.1 Aerospace

- 5.1.2 Defense

- 5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia-Pacific

- 5.2.4 Latin America

- 5.2.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 The Boeing Company

- 6.1.2 RTX Corporation

- 6.1.3 Airbus SE

- 6.1.4 General Electric Company

- 6.1.5 Safran SA

- 6.1.6 BAE Systems PLC

- 6.1.7 Parker Hannifin Corporation

- 6.1.8 L3Harris Technologies Inc.

- 6.1.9 Leonardo SpA

- 6.1.10 THALES

- 6.1.11 Elbit Systems Ltd

- 6.1.12 Rolls-Royce PLC

- 6.1.13 Honeywell International Inc.

- 6.1.14 Rheinmetall AG