|

市場調査レポート

商品コード

1690707

ゴム用プロセスオイル:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Rubber Process Oils - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ゴム用プロセスオイル:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

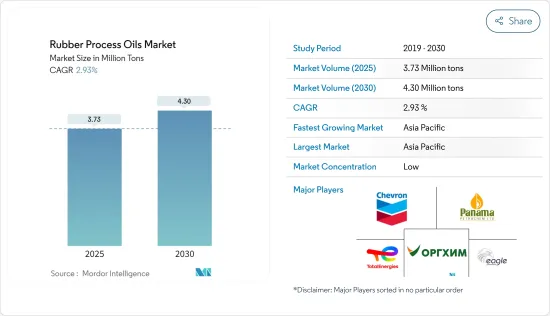

ゴム用プロセスオイルの市場規模は2025年に373万トンと推定され、予測期間(2025-2030年)のCAGRは2.93%で、2030年には430万トンに達すると予測されます。

COVID-19パンデミックは市場にマイナスの影響を与えました。封鎖と規制により製造施設や工場が閉鎖されたためです。サプライチェーンと輸送の混乱はさらに市場に障害をもたらしました。しかし、2021年には業界は回復し、市場の需要は回復しました。

主なハイライト

- 短期的には、自動車産業からのタイヤと自動車部品の需要増加が市場成長の主な要因の1つです。

- その反面、原料価格の変動が市場成長の妨げになると予想されます。

- しかし、バイオベースのゴム用プロセスオイルに対する需要の増加は、予測期間中、市場の成長に様々な機会を提供すると予測されます。

- アジア太平洋地域は最大の市場であり、中国、インド、日本などの国々からの消費増加により、予測期間中に最も急成長する市場になると予想されます。

ゴム用プロセスオイル市場の動向

タイヤと自動車部品からのゴム用プロセスオイルの需要拡大

- ゴム用プロセスオイルは、ゴムコンパウンドを混合する際に使用されます。これらの製品は、充填剤の分散性とコンパウンドの流動性を向上させる。そのため、ゴムをベースとする産業にとって最も重要な成分であると考えられています。

- 機械的特性が向上するため、ゴム用プロセスオイルはタイヤやその他の自動車部品に使用されています。さらに、製品のブレーキ効率と燃費の向上は、タイヤや自動車部品での使用にさらに利益をもたらすと考えられます。

- ゴム用プロセスオイルは、タイヤの製造に使用されるゴムの特性を向上させる。人口増加による生活水準の向上と消費力の増加は、世界的に自動車需要を押し上げる要因となっています。例えば、OICAによると、2022年の世界全体の乗用車生産台数は6,159万台で、2021年比で8%、2020年比で10%の増加を示しています。したがって、乗用車の生産台数の増加は、予測期間においてゴム用プロセスオイル市場に上向きの需要を生み出すと予想されます。

- さらに、ドイツでは、半導体の不足と原材料の限られた供給によって自動車産業が阻害されています。同様に、新しい世界調和小型車試験方法(WLTP)の実施や、国際的な自動車需要を減少させた米国と中国の貿易摩擦、新たに販売される自動車の平均CO2排出量を1キロメートル当たり95グラムにすることを自動車メーカーに義務付けたEU-28の新しい排出ガス基準などの他の要因も、乗用車の生産に悪影響を与えました。

- しかし、2022年には、自動車生産は半導体不足から徐々に回復しました。例えば、OICAによると、2022年にドイツで生産された乗用車は約348万357台で、2021年に比べて12%増加しました。従って、乗用車セグメントの生産台数の増加は、ゴム用プロセスオイル市場に上向きの需要をもたらすと予想されます。

- さらに、米国は世界第2位の自動車販売・生産市場です。例えば、OICAによると、2022年の米国の自動車生産台数は1,006万339台で、2021年比で10%の増加を示しました。その結果、自動車生産台数の増加により、ゴム用プロセスオイル市場の需要増が見込まれます。

- したがって、この地域のこのような良好な動向と投資はすべて、予測期間中にゴム用プロセスオイル市場の需要を促進すると予想されます。

市場を独占するアジア太平洋地域

- 予測期間中、アジア太平洋地域がゴム用プロセスオイル市場を独占すると予想されます。中国、日本、インドなどの新興諸国におけるタイヤや自動車部品からのゴム用プロセスオイル需要の高まりが、この地域のゴム用プロセスオイル需要を牽引すると予想されます。

- ゴム用プロセスオイルの最大の生産者はアジア太平洋地域に位置しています。ゴム用プロセスオイル生産の主要企業には、Total、Chevron Intellectual Property LLC、Panama Petrochem Ltd、ORGKHIM Biochemical Holding、Eagle Petrochemなどがあります。

- 中国の自動車産業は、バッテリー駆動の電気自動車に対する消費者の嗜好が高まるにつれ、動向が変化しています。中国の自動車産業の拡大は、ゴム用プロセスオイル市場に利益をもたらすと期待されています。国際自動車工業会(OICA)によると、中国は世界最大の自動車生産国で、世界生産量の34%近くを占めています。2022年の自動車生産台数は2,702万615台で、2021年の2,612万1,712台に比べ24%増加しました。従って、自動車生産台数の増加は、ゴム用プロセスオイル市場に上向きの需要をもたらすと予想されます。

- インドでは、自動車の排ガス規制の強化、自動車の安全性の向上、自動車へのADAS(先進運転支援システム)の導入、小売・eコマース部門での物流の急成長などが、小型商用車(LCV)の新車・先進車の需要を大きく牽引しています。例えば、OICAによると、2022年のインドの小型商用車生産台数は61万7,398台で、2021年比で27%増加し、2020年比で60%回復しました。

- さらに、インドにおける自動車産業への投資と進歩の増加は、ゴム用プロセスオイル市場の消費を増加させると予想されます。例えば、タタ・モーターズは2022年4月、今後5年間で乗用車事業に30億8,000万米ドルを投資する計画を発表しました。この拡大は、同国のゴム用プロセスオイル市場に好影響を与えると予想されます。

- 工業や建設作業中の電気接触、落下物、有害な化学物質や油の流出、機械の移動などによる怪我から作業者の安全を守るという意識の高まりは、ゴム製履物の需要にプラスに働くと思われます。ゴムを使用した履物の製造において、ゴム用プロセスオイルの使用が増加しています。したがって、ゴム製履物の需要の高まりは、ゴム製プロセスオイル市場をさらに活性化させる。

- 上記の要因から、アジア太平洋地域のゴム用プロセスオイル市場は調査期間中に大きく成長すると予測されます。

ゴム用プロセスオイル産業の概要

ゴム用プロセスオイル市場は細分化されています。この市場の主要企業(順不同)には、TotalEnergies、Chevron Corporation、Panama Petrochem Ltd、ORGKHIM Biochemical Holding、EaglePetrochemなどが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- タイヤと自動車部品の需要増加

- フットウェア需要の増加

- その他

- 抑制要因

- 原材料価格の変動

- その他の抑制要因

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 製品タイプ

- 芳香族系

- パラフィン系

- ナフテン系

- 用途

- タイヤ・自動車部品

- フットウェア

- 消費財

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- APAR Industries

- Chevron Corporation

- CPC Corporation

- EaglePetrochem

- Exxon Mobil Corporation

- HF Sinclair Corporation

- LODHA Petro

- ORGKHIM Biochemical Holding

- Panama Petrochem Ltd

- Repsol

- Sterlite Lubricants

- TotalEnergies

- Witmans Industries Pvt. Ltd

第7章 市場機会と今後の動向

- バイオベースのゴム用プロセスオイルの需要増加

- その他の機会

The Rubber Process Oils Market size is estimated at 3.73 million tons in 2025, and is expected to reach 4.30 million tons by 2030, at a CAGR of 2.93% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market. This was because of the shutdown of the manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the short term, increasing demand for tire and automotive components from the automobile industry is one of the major factors driving the growth of the market studied.

- On the flip side, volatility in raw material prices is expected to hinder the growth of the market.

- However, the increasing demand for bio-based rubber process oil is forecasted to offer various opportunities for the growth of the market over the forecast period.

- Asia-Pacific region represents the largest market and is also expected to be the fastest-growing market over the forecast period owing to the increasing consumption from countries such as China, India, and Japan.

Rubber Process Oil Market Trends

Growing Demand of Rubber Process Oil from Tire and Automobile Components

- Rubber process oils are used while mixing the rubber compounds. These products improve the dispersion of fillers and the flow property of the compound. Hence, it is considered to be the most important ingredient for the rubber-based industry.

- Due to enhanced mechanical properties, rubber process oils are used in the tire and other automotive components. In addition, improved braking efficiency and fuel consumption of the product are likely to further benefit its usage in the tire and automotive components.

- The rubber process oils enhance the rubber properties used in the production of tires. Rising population improved living standards and increased spending power are factors likely to boost the demand for automobiles globally. For instance, according to OICA, in 2022, the total number of passenger cars produced globally was 61.59 million units, which showed an increase of 8% compared to 2021 and 10% compared to 2020. Therefore, an increase in the production of passenger cars is expected to create an upside demand for the rubber process oil market in the forecast period.

- Moreover, in Germany, the automotive industry has been hampered by the shortage of semiconductors and a limited supply of raw materials. Similarly, other factors such as the implementation of the new Worldwide Harmonized Light-Duty Vehicles Test Procedure (WLTP) and US-China trade conflicts which decreased the international automotive demand, EU-28's new emission standard which mandates carmakers to achieve average CO2 emissions of 95 grams per kilometre across newly sold vehicles had negatively affected the production of passenger cars.

- However, in 2022 the automobile production in the country recovered gradually from semiconductor shortages. For instance, according to OICA, around 34,80,357 passenger cars were produced in Germany in 2022, which shows an increase of 12% compared to 2021. Therefore, increase in the production of passeger car segment is expected to create an upside demand for the rubber process oils market.

- Furthermore, the United States is the second-largest market for vehicle sales and production globally. For instance, according to OICA, in 2022, automobile production in the United States amounted to 1,00,60,339 units, which showed an increase of 10% compared to 2021. As a result, an increase in automobile production is expected to create an upside demand for rubber process oils market.

- Therefore, all such favorable trends and investments in the region are expected to drive the demand for rubber process oils market during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the market for rubber process oil during the forecast period. The rising demand for rubber process oil from tire and automobile components in developing countries like China, Japan, and India is expected to drive the demand for rubber process oil in this region.

- The largest producers of rubber process oil are located in the Asia-Pacific region. Some of the leading companies in the production of rubber process oil are Total, Chevron Intellectual Property LLC, Panama Petrochem Ltd, ORGKHIM Biochemical Holding, and Eagle Petrochem among others.

- The automobile industry in China is experiencing shifting trends as consumer preference for battery-powered electric vehicles rises. The expansion of China's automotive sector is expected to benefit the rubber process oil market. According to the International Organization of Motor Vehicle Manufacturers (OICA), China is the world's largest automobile producer, accounting for nearly 34% of global volume. In 2022, the country produced 2,70,20,615 units of automobiles, registering an increase of 24% compared to 2,61,21,712 units in 2021. Therefore, increasing in the production of automobiles is expected to create an upside demand for the rubber process oil market.

- In India, increasing regulations on vehicle emissions, advancement in vehicle safety, the introduction of driver-assist systems in vehicles, and rapidly growing logistics in the retail and e-commerce sectors, have been significantly driving the demand for new and advanced Light commercial vehicles (LCVs). For instance, accroding to OICA, in 2022, light commercial vehicle production in India amounted to 6,17,398 units, which showen an increase of 27% compared to 2021 and a recovery of 60% compared to 2020.

- Furthermore, increased investments and advancements in the automobile industry in India is expected to increase the consumption of rubber process oil market. For instance, in April 2022, Tata Motors announced plans to invest USD 3.08 billion in its passenger vehicle business over the next five years. This expansion is expected to have a positive impact on the rubber process oils market in the country.

- Rising awareness about the worker's safety from injuries due to electrical contacts, falling objects, spilling of harmful chemicals and oils, moving machinery, and others during industrial or construction work is likely to benefit the demand for rubber footwear. Rubber process oil is increasingly used in manufacturing footwear using rubber. Hence, the rising demand for rubber footwear further fuels the rubber process oils market.

- Owing to the above-mentioned factors, the market for rubber process oil in the Asia-Pacific region is projected to grow significantly during the study period.

Rubber Process Oil Industry Overview

The Rubber Process Oil Market is fragmented in nature. The major players in this market (not in a particular order) include TotalEnergies, Chevron Corporation, Panama Petrochem Ltd, ORGKHIM Biochemical Holding, and EaglePetrochem, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Tire and Automotive Components

- 4.1.2 Growing Demand for Footwear

- 4.1.3 Others

- 4.2 Restraints

- 4.2.1 Volatility in Raw Material Price

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Aromatic

- 5.1.2 Paraffinic

- 5.1.3 Naphthenic

- 5.2 Application

- 5.2.1 Tire and Automobile Components

- 5.2.2 Footwear

- 5.2.3 Consumer Goods

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 APAR Industries

- 6.4.2 Chevron Corporation

- 6.4.3 CPC Corporation

- 6.4.4 EaglePetrochem

- 6.4.5 Exxon Mobil Corporation

- 6.4.6 HF Sinclair Corporation

- 6.4.7 LODHA Petro

- 6.4.8 ORGKHIM Biochemical Holding

- 6.4.9 Panama Petrochem Ltd

- 6.4.10 Repsol

- 6.4.11 Sterlite Lubricants

- 6.4.12 TotalEnergies

- 6.4.13 Witmans Industries Pvt. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand of Bio Based Rubber Processing Oil

- 7.2 Other Opportunities