|

市場調査レポート

商品コード

1437501

船舶エンジン監視システムの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Marine Engine Monitoring System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 船舶エンジン監視システムの世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

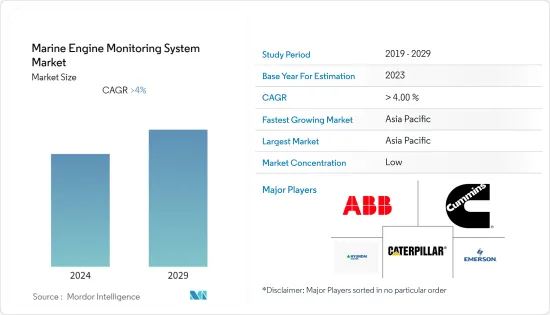

世界の船舶エンジン監視システムの市場規模は、2024年に6億4,463万米ドルと推定され、2029年には7億8,430万米ドルに達し、予測期間中(2024年~2029年)にCAGR4%で成長すると予測されています。

長期的には、市場を牽引する主な要因は、経済間の貿易活動の増加であり、国家間の主要な貿易活動が海上ルートで行われるため、船舶の需要が増加します。たとえば、インドでは、国際貿易総額の90%が海上ルートで行われています。

海洋の安全と汚染の規制に対する政府の厳しい基準の高まりも、船舶エンジン監視システム市場の成長を促進します。操業の安全性とコスト削減を目的とした船舶エンジン監視システムのカスタマイズも、市場の促進要因となっています。しかし、予測期間中、発展途上国からの貿易活動により、これらの貿易活動は増加すると予想されます。

市場はまた、船舶エンジン監視システムにおけるリアルタイムのデータ追跡における技術の進歩からも恩恵を受ける見込みです。さらに、製造、設置、運用に関連するコストが低いため、制御可能なピッチの代替品と比較して、固定プロペラの採用が大幅に促進されています。しかし、市場の拡大は石油・ガスの価格変動によって妨げられています。

船舶エンジン監視システム市場動向

大幅な成長を遂げている旅客タイプ

大手造船所は操業からの排出量ゼロという目標を達成するためにクリーン技術に投資しているため、現在のシナリオでは炭素排出量の削減がほとんどの造船所にとって焦点となっています。例えば、

LNG燃料クルーズ船であるMSCワールド欧州は、固体酸化物燃料電池(SOFC)ソリューションが温室効果を削減できるため、固体酸化物燃料電池(SOFC)技術を組み込んだ50キロワットの実証システムを備えたLNG燃料電池など、環境に優しい先進技術を備えています。排出量は約30%削減されます。このLNGクルーズ船はフランスで建造され、2022年に就航する予定です。

中国当局は排出要件を国際海事機関(IMO)の規制よりもさらに厳しくしました。一般にC1およびC2として知られる中国GB15097規制には、粒子状物質(PM)に対する制限が含まれています。したがって、主要企業はこれらの厳しい排出基準を満たす新しいエンジンを発売しており、それがこの地域の市場をさらに牽引しています。

- 2022年 9月、Wartsila Corporationは、中国で新しく発売されたWartsila 20エンジンの受注を発表しました。これらのエンジンには、中国のステージ II(一般にC2として知られる)排出基準に準拠するために、Wartsila NOR NOX排出削減装置が装備されています。

商品の75%が海外のパートナーから海路で欧州に流入しており、輸送は引き続きサプライヤーから顧客に製品を輸送する最もコスト効率の高い方法です。その結果、海上輸送の需要は年々増加しており、世界中で輸出入量が増加しています。

グローバリゼーションが多くの経済の中核に根を張るにつれて、国際貿易商品がさまざまな価格帯で入手しやすい優れた品目を提供する機会が増えています。

商業価値の観点から見ると、船舶の所有と登録のランキングはトン数の観点よりも不安定です。中国が1.1%ポイント増加し、最もシェアを伸ばし、次いでスイス、中国香港、韓国が続き、いずれも保有船団におけるコンテナ船の割合が高くなりました。

世界中で上記のような発展が見られ、予測期間中に市場は大幅な成長を遂げる可能性があります。

北米は最大の市場

近年、この地域は急速な経済発展と製造業およびエネルギー部門の成長を描いており、それによって海上貿易が加速しており、これらの活動は予測期間中に増加すると予想されます。

その後、海上貿易の増加により、製造品を世界中に輸送するために使用される船舶の需要が増加しました。この地域は、中国やインドなど、世界で最も急速に成長している経済国で構成されています。急速な成長ペースは、この地域での工業化と建設活動の増加によって支えられています。そのためには、この地域からの原材料や完成品の輸出入のための船舶の需要の増加が必要となります。これが市場の成長を促進します。

地方政府は海軍向けの船舶契約を導入しており、国内で防衛艦の需要が生まれる可能性があります。大規模な船舶艦隊を建設するという政府の計画を支援するために、政府はカナダの造船所2社、すなわちアービング造船所(ハリファックス)とシースパンのバンクーバー造船所(バンクーバー)との間で、カナダ海軍の戦闘艦艇とカナダ沿岸警備隊の非戦闘艦艇のために、戦闘艦艇および非戦闘艦艇の建造に関する長期戦略協定を締結しました。

- これに関連して、2023年1月、アービング造船所と連邦政府は、カナダ沿岸警備隊向けに北極および海洋巡視船2隻を追加建造する16億米ドルの契約に合意しました。

カナダの2つの造船所、アービング造船所およびシースパン・バンクーバー造船所とのパートナーシップを確立して、戦闘艦および非戦闘艦のカナダ連邦艦隊を再建します。カナダの造船所や全国の企業には、国家造船戦略(NSS)の第2および第3の柱に基づいて小型船舶の建造、修理、改修、メンテナンスを行う機会が存在します。

- 2022年6月、カナダ政府は、NSSの3番目の戦略的造船パートナーとなるための包括協定に向けて、ケベック州リーバイスのシャンティエ・デイビーと交渉を開始しました。

さらに、大手造船所がさまざまな当局や企業から契約を獲得しており、国内の商海運業は着実なペースで成長しています。国内造船会社の存在感に加え、外国造船会社も徐々に国内での存在感を高めています。

既存の艦隊を新しい船舶に転換することで、船舶からの排出量が削減され、国内の船舶エンジン監視システム市場の成長が促進されると予想されます。

船舶エンジン監視システム業界の概要

船舶エンジン監視システム市場は、ABB Ltd.、Caterpillar Inc.、Cummins Inc.、現代重工業などのいくつかの主要企業によって独占されています。企業は、ユーザーがエンジンを監視して適切な予防および予知保全を行い、エンジンのダウンタイムの可能性を低減できるようにし、新しく先進的な製品と技術の革新のための研究開発に多額の投資を行っています。例えば、

- 2023年 4月、DNVは、海事業界が排出量データを正確に評価して操作できるように設計されたデータ検証エンジンおよびデータ管理プラットフォームであるEmissions Connectを導入しました。このソリューションは、海事バリューチェーンに関与するすべての利害関係者と安全に共有できる、信頼性の高い検証済みの排出データソースを提供します。

- 2022年 3月、ABB Ltd.は、船主に推進効率と排出量レポートの簡素化された管理を提供する包括的なデジタルソリューションであるTekomar XPERT marineを導入しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 海上輸送と海上貿易の増加が市場を牽引すると予想

- 市場抑制要因

- 船舶エンジンに対する規制の強化は市場の成長を妨げると予想

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション(金額ベースの市場規模:米ドル)

- タイプ別

- 船舶

- コンテナ

- 乗客

- その他

- エンジン推進タイプ別

- ディーゼル

- ガスタービン

- その他

- エンドユーザー別

- 旅客船

- クルーズ船

- タンカー

- その他

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- 世界のその他の地域

- 南米

- 中東とアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- ABB Ltd.

- Cummins Inc.

- Caterpillar Inc.

- Emersion Electric Co.

- Hyundai Heavy Industries Co., Ltd.

- MAN Energy Solutions SE

- AST Group

- CMR Group

- Mitsubishi Heavy Industries Group

- Noris Group

- Rolls-Royce plc

- Wartsila Corporation

第7章 市場機会と将来の動向

The Marine Engine Monitoring System Market size is estimated at USD 644.63 million in 2024, and is expected to reach USD 784.30 million by 2029, growing at a CAGR of 4% during the forecast period (2024-2029).

Over the long term, the major factors that will drive the market are increasing trade activities between the economies which will increase the demand for marine vessels as the major trade activities between countries take place through the marine route. For instance, in India, 90% of its total international trade by volume takes place through marine routes.

The rise in stringent government norms for the regulation of marine safety and pollution will drive also the growth of the Marine engine monitoring system market. Customization of marine engine monitoring systems for the safety of operations and cost reduction has also been a driving factor for the market study. However, During the forecast period, it is expected that these trade activities are going to rise owing to the trade activities from the developing nations.

The market will also benefit from technological advancements in real-time data tracking in marine engine monitoring systems. Further, the lower expenses associated with manufacturing, installation, and operation have significantly bolstered the adoption of fixed propellers when contrasted with controllable pitch alternatives. However, the market expansion is being hampered by variations in oil and gas costs.

Marine Engine Monitoring System Market Trends

Passenger Type Witnessing Major Growth

Reduction of carbon emission is the focal point for most of the shipbuilders in the current scenario as major shipbuilders are investing in cleaner technologies to achieve the goal of zero emissions from operations. For instance,

MSC World Europa, an LNG-powered cruise ship features advanced environmentally-friendly technologies, such as an LNG-powered fuel cell, with a 50-kilowatt demonstrator system that incorporates solid oxide fuel cell (SOFC) technology, as SOFC solution can reduce greenhouse emissions by about 30%. The LNG Cruise ship will be built in France and is set to enter service in 2022.

The Chinese authorities have made emission requirements even stricter than the International Maritime Organization (IMO) regulations. The China GB15097 regulation, which is commonly known as C1 and C2, includes limits for particulate matter (PM). Thus, key players are launching new engines that meet these stringent emission norms, which are further driving the market in the region.

- In September 2022, Wartsila Corporation announced orders for its newly launched Wartsila 20 engines in China. These engines are equipped with Wartsila NOR NOX emissions reducer to comply with China's stage II, popularly known as C2, emissions standards.

Shipping continues to be the most cost-effective method of transferring products from supplier to customer, with 75% of commodities entering Europe by sea from foreign partners. As a result, there has been an increase in demand for marine transport throughout the years, resulting in a growth in the quantity of imports and exports worldwide.

With globalization establishing roots in the core of many economies, there are increasing opportunities for international trade goods to provide a superior selection of accessible items at various price points.

In terms of commercial value, the ranking of fleet ownership and registration is more volatile than in terms of tonnage. China increased its share the most, by 1.1 percentage points, followed by Switzerland, Hong Kong China, and the Republic of Korea, all of which have a higher proportion of container ships in their fleets.

The above-menitoned develpment across the globe is likely to witness major growth for the market during the forecast period.

North America is the Largest Market

Over the recent years, this region has depicted rapid economic development as well as the growth of the manufacturing and energy sectors, thereby accelerating maritime trade, these activities are expected to increase in the forecast period.

The rise in seaborne trade has subsequently contributed to a rise in the demand for ships used to transport manufactured goods globally. The region consists of fastest growing economies in the world like China and India. The rapid pace of growth is supported by increasing industrialization and construction activities in the region. This will require an increase in demand for marine vessels for raw materials and finished goods imports and exports from the region. This will drive the growth in the market.

The local government is introducing contracts for ships for the navy, which may generate the demand for defense ships in the country. To support the government's plans to build a large vessel fleet, the government signed a long-term strategic agreement with two Canadian shipyards, namely, Irving Shipbuilding Inc. (Halifax) and Seaspan's Vancouver Shipyards Co. Ltd (Vancouver), for the construction of combat and non-combat naval vessels for the Royal Canadian Navy and non-combat vessels for the Canadian Coast Guard.

- In this regard, in January 2023, Irving Shipbuilding and the federal government agreed to a USD 1.6 billion contract to build two additional Arctic and offshore patrol ships for the Canadian Coast Guard.

To rebuild Canada's federal fleet of combat and non-combat ships, with established partnerships with two Canadian shipyards, Irving Shipbuilding Inc. and Seaspan Vancouver Shipyards. Opportunities exist for Canadian shipyards and enterprises across the nation to build, repair, refit, and maintain small ships under the second and third pillars of the National Shipbuilding Strategy (NSS).

- In June 2022, The Government of Canada began negotiations with ChantierDavie of Levis, Quebec, towards an umbrella agreement to become the NSS's third strategic shipbuilding partner.

Moreover, the commercial shipping industry in the country is growing at a steady pace, as major shipyards are winning contracts from different authorities and companies. In addition to the presence of domestic shipbuilding companies, foreign shipbuilding companies are slowly increasing their presence in the country.

The conversions of the existing fleet with the new ships are anticipated to lower the emissions from the ships and boost the growth of the marine engine monitoring system market in the country.

Marine Engine Monitoring System Industry Overview

The Marine Engine Monitoring system market is dominated by several key players such as ABB Ltd., Caterpillar Inc., Cummins Inc., Hyundai Heavy Industries Co. Ltd., and others. Companies are investing heavily in research and development for the innovation of new and advanced products and technologies that enable users to monitor their engines for proper preventive and predictive maintenance to reduce the probability of engine downtime. For instance,

- In April 2023, DNV introduced Emissions Connect, a data verification engine and data management platform designed to assist the maritime industry in accurately assessing and working with emissions data. The solution provides a reliable, verified source of emissions data that can be securely shared with all stakeholders involved in the maritime value chain.

- In March 2022, ABB Ltd. introduced Tekomar XPERT marine, a comprehensive digital solution that offers shipowners simplified management of propulsion efficiency and emissions reporting.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Maritime Transport and Sea Borne Trade is Expected to Drive the Market

- 4.2 Market Restraints

- 4.2.1 Increased Stringent Regulations for Marine Engines is Expected to Hamper the Growth of the Market

- 4.3 Porters Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Type

- 5.1.1 Vessel

- 5.1.2 Container

- 5.1.3 Passenger

- 5.1.4 Others

- 5.2 By Engine Propulsion Type

- 5.2.1 Diesel

- 5.2.2 Gas Turbine

- 5.2.3 Others

- 5.3 By End User

- 5.3.1 Passenger Vessels

- 5.3.2 Cruise Ships

- 5.3.3 Tankers

- 5.3.4 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 ABB Ltd.

- 6.2.2 Cummins Inc.

- 6.2.3 Caterpillar Inc.

- 6.2.4 Emersion Electric Co.

- 6.2.5 Hyundai Heavy Industries Co., Ltd.

- 6.2.6 MAN Energy Solutions SE

- 6.2.7 AST Group

- 6.2.8 CMR Group

- 6.2.9 Mitsubishi Heavy Industries Group

- 6.2.10 Noris Group

- 6.2.11 Rolls-Royce plc

- 6.2.12 Wartsila Corporation