舶用エンジンモニタリングシステム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Marine Engine Monitoring System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797827

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

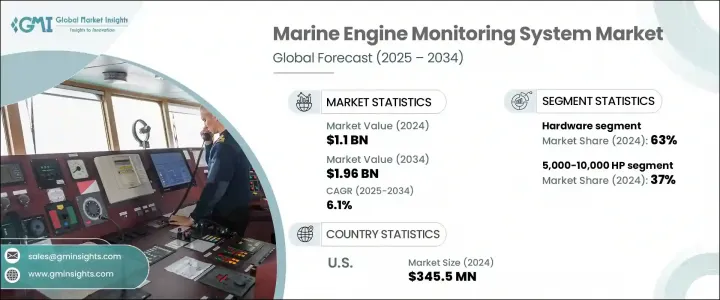

舶用エンジンモニタリングシステムの世界市場規模は、2024年に11億米ドルとなり、CAGR6.1%で成長し、2034年には19億6,000万米ドルに達すると予測されています。

排ガス規制が強化され、舶用エンジン技術が高度化するにつれて、監視システムは基本的なメンテナンスツールから、運用を最適化するための不可欠なプラットフォームへと移行しています。これらのシステムは現在、リアルタイムデータ、デジタル接続、予測機能に依存し、燃料効率、安全性、規制遵守の強化を実現しています。IoT統合、AIベースの分析、インテリジェント・センサー・ネットワークなどの技術は、オペレーターがフリート・パフォーマンスを管理する方法を再構築しています。業界はまた、スマートな海上オペレーションに合わせた高度な訓練エコシステムを構築するOEM主導の取り組みと並んで、海事におけるデジタル化を推進する官民イニシアチブからも勢いを得ています。データ主導の洞察に対する需要は、海運業界全体でインテリジェントなエンジン監視ツールの採用を加速し続けています。

パンデミック(世界的大流行)の後、遠隔診断とモニタリングの採用が加速しました。大規模な商業フリートでは、燃料効率の低下、シリンダーの過度の磨耗、潤滑不良などの問題の早期発見を可能にする、予測および状態ベースのモニタリング機能が標準になりつつあります。これらのシステムは、ダウンタイムを最小限に抑え、世界の持続可能性の目標に沿うものです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 11億米ドル |

| 予測金額 | 19億6,000万米ドル |

| CAGR | 6.1% |

2024年、ハードウェア・セグメントは63%のシェアを占め、2034年までCAGR 5%で成長すると予測されます。このセグメントには、船上でのシームレスなデータ収集とシステム統合を促進する制御ユニット、センサー、データロガー、通信モジュールなどの主要コンポーネントが含まれます。船舶の新設や改造が増加し、特に排ガス規制への対応や予知保全機能が重要になるにつれて、ハードウェアの設置需要が高まっています。シーメンス、ABB、バルチラなどの大手OEMは、先進のセンサー技術を推進システムや補助システムに直接組み込み、総合的な性能監視を可能にしています。

5,000~10,000HPの出力レンジ・セグメントは2024年に37%のシェアを占め、2034年までCAGR6%で成長すると予測されています。このレンジの船舶(主に中型タンカー、オフショア支援船、貨物運搬船)は、運転時間の延長と厳しい規制要件のため、堅牢な監視が必要です。この出力範囲向けの監視システムは、詳細な分析、予測的洞察、AI対応の診断を提供し、予防保全、船隊の最適化、進化する環境基準への準拠をサポートします。このレンジをターゲットとするOEMは、サービス提供に予測ツールを統合する傾向が強まっています。

米国の舶用エンジンモニタリングシステム市場は83%のシェアを占め、2024年には3億4,550万米ドルを稼ぐ。同国の主導的地位は、商業船舶と防衛船舶の大規模な船隊、排出に関する規制圧力、デジタル海事技術の普及によって支えられています。エッジコンピューティング、AIベースのエンジン診断、コネクテッドシステムへの投資は、公共と民間の両方の海洋事業者がパフォーマンスを合理化するのに役立っています。政府との契約や強力な技術インフラへのアクセスにより、米国のOEMやインテグレーターはハイエンドのスマートシステムで国内需要を満たすことができます。MEMSやバイオ燃料電池による現場モニタリングのような技術は、この地域の高度なエンジニアリング能力のおかげで、より広範な用途を見出しています。

世界の舶用エンジンモニタリングシステム市場を積極的に形成している主要企業には、Caterpillar、Wartsila、Cummins、Siemens、ABB、Kongsberg Maritime、MAN Energy Solutionsなどがあります。舶用エンジンモニタリングシステム市場で競合する企業は、デジタル機能の拡大、スマートコンポーネントの開発、世界サービスの強化に注力しています。その多くは、AI、IoT、クラウド接続をエンジン監視ソリューションに統合し、高度な診断、自動レポート、リアルタイムの洞察を提供しています。海運事業者とのパートナーシップにより、これらの企業は、運航効率を向上させるカスタマイズされたソリューションを共同開発することができます。また、ハイブリッド推進システムに注力し、モニタリングツールを活用して燃料消費量と排出量を最適化する企業もあります。トレーニング・プラットフォームやアフターサービス・エコシステムへの投資は、顧客維持の確保に役立っています。

目次

第1章 調査手法

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 燃費効率の高い船舶運航の需要増加

- IMO規制によるコンプライアンスニーズの急増

- リモート診断とIoTベースのソリューションの導入増加

- 海上貿易の増加と船舶艦隊の拡大

- 業界の潜在的リスク&課題

- MEMSシステムの初期投資コストが高め

- システム導入のための熟練した海事技術者の不足

- 市場機会

- ハイブリッドおよび電気推進システムにおけるMEMSの拡張

- 自律型および遠隔操作型船舶プロジェクトの急増

- スマートポートと接続された航路への投資の増加

- 造船所におけるデジタルツイン技術の導入

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- センサー

- 制御ユニット

- ディスプレイ

- コントローラー

- その他

- ソフトウェア

- データ分析ソフトウェア

- 予測メンテナンスソフトウェア

- その他

- サービス

第6章 市場推計・予測:馬力別、2021年~2034年

- 主要動向

- 1,000馬力

- 1,000~5,000馬力

- 5,001~10,000馬力

- 10,000HP以上

第7章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- 現場監視

- リモート監視

第8章 市場推計・予測:推進別、2021年~2034年

- 主要動向

- ディーゼル

- ガスタービン

- その他

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- パフォーマンス監視

- 燃費最適化

- メンテナンス診断

- 安全性と規制遵守

第10章 市場推計・予測:最終用途別、2021年~2034年

- 商用船

- 貨物船

- タンカー

- コンテナ船

- 海軍艦艇

- 旅客船

- クルーズ船

- フェリー

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- フィリピン

- ベトナム

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

第12章 企業プロファイル

- ABB

- AST

- Caterpillar

- CMR

- Cummins

- Emerson Electric

- General Electric

- Hyundai Heavy Industries

- Jason Marine

- Kongsberg Maritime

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- MTU Friedrichshafen

- NORIS

- Rolls-Royce

- Scania

- Siemens

- Volvo Penta

- Wartsila

- Yanmar

目次

The Global Marine Engine Monitoring System Market was valued at USD 1.1 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 1.96 billion by 2034. As emission standards tighten and marine engine technologies become more advanced, monitoring systems have transitioned from basic maintenance tools to essential platforms for optimizing operations. These systems now rely on real-time data, digital connectivity, and predictive capabilities to deliver enhanced fuel efficiency, safety, and regulatory compliance. Technologies like IoT integration, AI-based analytics, and intelligent sensor networks are reshaping how operators manage fleet performance. The industry is also gaining momentum from public-private initiatives pushing digitalization in maritime, alongside OEM-led efforts to create advanced training ecosystems tailored for smart maritime operations. The demand for data-driven insights continues to accelerate the adoption of intelligent engine monitoring tools across the shipping industry.

Remote diagnostics and monitoring saw faster adoption following the pandemic, as restrictions prompted marine operators to adopt cloud-based tools to maintain operational continuity. Predictive and condition-based monitoring features are becoming standard across larger commercial fleets, enabling early detection of issues such as fuel inefficiency, excessive cylinder wear, or lubrication faults. These systems help minimize downtime and align with global sustainability goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.1 Billion |

| Forecast Value | $1.96 Billion |

| CAGR | 6.1% |

In 2024, the hardware segment held 63% share and is forecasted to grow at a CAGR of 5% through 2034. This segment includes key components such as control units, sensors, data loggers, and communication modules that facilitate seamless data collection and system integration onboard. The rise in new vessel construction and retrofitting activities is boosting demand for hardware installations, especially as compliance with emission regulations and predictive maintenance capabilities becomes more critical. Leading OEMs like Siemens, ABB, and Wartsila are embedding advanced sensor technologies directly into propulsion and auxiliary systems to enable comprehensive performance monitoring.

The 5,000-10,000 HP power range segment held 37% share in 2024 and is projected to grow at a CAGR of 6% through 2034. Vessels within this range-typically medium-sized tankers, offshore support ships, and cargo carriers-require robust monitoring due to extended operational hours and strict regulatory requirements. Monitoring systems for this power range offer detailed analytics, predictive insights, and AI-enabled diagnostics that support preventive maintenance, fleet optimization, and compliance with evolving environmental standards. OEMs targeting this range are increasingly integrating predictive tools into their service offerings.

United States Marine Engine Monitoring System Market held 83% share and earned USD 345.5 million in 2024. The country's leadership position is supported by a sizable fleet of commercial and defense vessels, regulatory pressure on emissions, and widespread use of digital maritime technologies. Investments in edge computing, AI-based engine diagnostics, and connected systems are helping both public and private marine operators streamline performance. Access to government contracts and strong tech infrastructure allows US-based OEMs and integrators to meet domestic demand with high-end, smart systems. Technologies like MEMS and on-site monitoring via biofuel cells are finding broader applications thanks to the advanced engineering capabilities of the region.

Key players actively shaping the Global Marine Engine Monitoring System Market include Caterpillar, Wartsila, Cummins, Siemens, ABB, Kongsberg Maritime, and MAN Energy Solutions. Companies competing in the marine engine monitoring system market are focused on expanding digital capabilities, developing smart components, and enhancing global service reach. Many are integrating AI, IoT, and cloud connectivity into engine monitoring solutions to offer advanced diagnostics, automated reporting, and real-time insights. Partnerships with shipping operators allow these firms to co-develop customized solutions that improve operational efficiency. Some companies are also focusing on hybrid propulsion systems, leveraging monitoring tools to optimize fuel consumption and emissions. Investments in training platforms and aftersales service ecosystems help ensure customer retention.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Power

- 2.2.4 Deployment mode

- 2.2.5 Propulsion

- 2.2.6 Application

- 2.2.7 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in demand for fuel-efficient vessel operations

- 3.2.1.2 Surge in compliance needs due to IMO regulations

- 3.2.1.3 Rise in deployment of remote diagnostics and IoT-based solutions

- 3.2.1.4 Rising maritime trade & vessel fleet expansion

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment cost for MEMS systems

- 3.2.2.2 Shortage of skilled maritime technicians for system deployment

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of MEMS in hybrid and electric propulsion systems

- 3.2.3.2 Surge in autonomous and remotely operated vessel projects

- 3.2.3.3 Rising investments in smart ports and connected shipping lanes

- 3.2.3.4 Adoption of digital twin technologies in shipyards

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors

- 5.2.2 Control units

- 5.2.3 Display

- 5.2.4 Controllers

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Data analytics software

- 5.3.2 Predictive maintenance software

- 5.3.3 Others

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Power, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 1,000 HP

- 6.3 1,000-5,000 HP

- 6.4 5,001-10,000 HP

- 6.5 10,000 HP and above

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 On-site monitoring

- 7.3 Remote monitoring

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Diesel

- 8.3 Gas turbines

- 8.4 Others

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Performance monitoring

- 9.3 Fuel efficiency optimization

- 9.4 Maintenance diagnosis

- 9.5 Safety and regulatory compliance

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 10.1 Commercial vessels

- 10.1.1 Cargo ships

- 10.1.2 Tankers

- 10.1.3 Container ships

- 10.2 Naval vessels

- 10.3 Passenger vessels

- 10.3.1 Cruise ships

- 10.3.2 Ferries

- 10.4 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 France

- 11.3.3 Italy

- 11.3.4 Spain

- 11.3.5 Russia

- 11.3.6 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Philippines

- 11.4.7 Vietnam

- 11.4.8 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Egypt

Chapter 12 Company Profiles

- 12.1 ABB

- 12.2 AST

- 12.3 Caterpillar

- 12.4 CMR

- 12.5 Cummins

- 12.6 Emerson Electric

- 12.7 General Electric

- 12.8 Hyundai Heavy Industries

- 12.9 Jason Marine

- 12.10 Kongsberg Maritime

- 12.11 MAN Energy Solutions

- 12.12 Mitsubishi Heavy Industries

- 12.13 MTU Friedrichshafen

- 12.14 NORIS

- 12.15 Rolls-Royce

- 12.16 Scania

- 12.17 Siemens

- 12.18 Volvo Penta

- 12.19 Wartsila

- 12.20 Yanmar

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 192 Pages

- 納期

- 2~3営業日