|

|

市場調査レポート

商品コード

1524208

ファミリーオフィス業界:市場シェア分析、業界動向・統計、成長予測(2024年~2029年)Family Offices Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ファミリーオフィス業界:市場シェア分析、業界動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

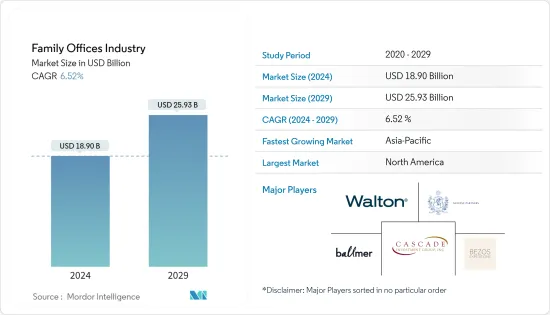

ファミリーオフィス業界は、2024年の189億米ドルから2029年には259億3,000万米ドルに成長し、予測期間中(2024-2029年)のCAGRは6.52%となる見込みです。

ファミリーオフィスは、超富裕層(HNWI)を対象としたプライベートウェルスマネジメントに特化したアドバイザリーファームです。ファミリーオフィスは、富裕層の個人または家族の財務および投資要件を管理するための包括的なソリューションを提供することで、従来の資産管理会社とは一線を画しています。ファイナンシャルプランニングや投資管理の他に、ファミリーオフィスは予算管理、保険、慈善寄付、財産移転計画、税務サービスなどを提供することが多いです。

ファミリーオフィス市場は近年大きな成長を遂げています。その背景には、富裕層(HNWI)の富の増加、財務管理の複雑化、個人に合わせたオーダーメイドの投資戦略への嗜好があります。こうした市場拡大の結果、ファミリーオフィス間の競争は激化し、この市場への参入を目指す投資家や金融機関の関心も高まっています。

ファミリーオフィス市場は、株式や債券、不動産、ヘッジファンドなど、さまざまな投資戦略を包含しており、その多様性が特徴となっています。

ファミリーオフィス市場の動向

シングルファミリーオフィスが市場最大のセグメントを占める

シングルファミリーオフィス(SFO)は、富裕層一家の財務および個人業務を監督するためだけに設立された私的な独立事業体です。SFOが管理する金融資本は一族にのみ帰属します。シングルファミリーオフィス市場は、富裕層の富の増加、個別化された金融サービスへの需要、洗練された資産管理戦略へのニーズなどの要因によって成長を遂げています。この成長は、特に超富裕層が増加している国々における、新たなファミリーオフィスの出現によってさらに加速しています。

シングルファミリーオフィスセクターは、2000年に入ってから大きな成長を遂げ、ファミリーオフィスの大半は2000年以降に設立されました。この傾向は、過去20年間における既存の富の中心地と新興市場の両方における新たな富の創出の大幅な増加と密接に関連しています。新しいテクノロジーとデジタルイノベーションの台頭は、この富の創出の波を推進する上で重要な役割を果たしています。

シングルファミリーオフィスセグメントは、個別化された財務管理へのニーズと、特定の一族の富の管理に集中することによって牽引されています。また、管理、秘密保持、投資戦略や財産計画と家族の価値観や目標との整合性にも大きな重点が置かれています。さらに、シングルファミリーオフィスのモデルは、税金の最適化、法律問題、慈善活動、後継者計画など、様々な財務上のニーズを管理するための全体的なアプローチを提供し、それによって一族の財務上の軌道の全体的な結束と方向性を強化します。

北米がファミリーオフィス市場で最大のシェアを占める

強固な金融インフラ、規制環境、経済政策、テクノロジーの進歩が北米市場に影響を与えています。この地域の富の集中、起業家の成長、安定した政治体制は、ファミリーオフィスにとって魅力的です。投資の嗜好、税制、富裕層向けの専門的サービスの利用可能性といった要素も一役買っています。

この地域は、債券や株式といった伝統的な投資対象から、テクノロジーや持続可能性といった革新的なセクターまで、資産クラス全体に投資機会があり、洗練された投資環境を提供しています。北米のファミリーオフィスのアプローチは、文化的要因や地域の投資哲学によって形成されることもあります。投資判断に社会的責任や倫理的配慮を取り入れることは、この地域でますます重要になってきています。北米の多様でダイナミックな経済は、ファミリーオフィスが投資成果を最適化するためにナビゲートしなければならない機会と課題を提供しています。

ファミリーオフィス業界の概要

ファミリーオフィス市場は細分化され、多くのプレーヤーが存在します。多くのファミリーオフィスは、伝統的なウェルスマネジメントに加え、法律、教育、慈善活動、ライフスタイルマネジメントなど、提供するサービスの幅を広げています。様々な分野の専門企業との提携や協力関係も一般的になりつつあり、顧客が利用できる専門知識も拡大しています。主なプレーヤーとしては、Cascade Investment, Walton Enterprises LLC, Bezos Expeditions, Mousse Partners, Ballmer Groupなどが挙げられます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- カスタムソリューションへの需要

- 各地域における富裕層の増加

- 市場抑制要因

- レガシーシステムへの過度の依存

- 多様な投資ポートフォリオの管理

- 市場機会

- パーソナライズされた金融サービスへの需要の高まり

- インパクト投資への注目の高まり

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 市場における技術的進歩に関する洞察

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 製品別

- シングルファミリーオフィス

- マルチファミリーオフィス

- バーチャルファミリーオフィス

- 投資資産クラス別

- 債券

- 株式

- オルタナティブ投資

- コモディティ

- 現金または現金同等物

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- オーストラリア

- その他アジア太平洋

- ラテンアメリカ

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- その他中東・アフリカ

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- Cascade Investment LLC

- Bezos Expeditions

- Bessemer Trust

- MSD Capital

- Stonehage Fleming

- Glenmede

- Emerson Collective

- U.S. Trust-Bank of America Private Wealth Management

- Bespoke Wealth Management

- JPMorgan Chase Wealth Management

- Goldman Sachs Family Office

- Silvercrest Asset Management

第7章 市場動向

第8章 免責事項および出版社について

The Family Offices Industry is expected to grow from USD 18.90 billion in 2024 to USD 25.93 billion by 2029, at a CAGR of 6.52% during the forecast period (2024-2029).

A family office is a specialized advisory firm in private wealth management catering to ultra-high-net-worth individuals (HNWI). It differs from conventional wealth management firms by providing comprehensive solutions for managing affluent individuals or families' financial and investment requirements. Besides financial planning and investment management, family offices often offer budgeting, insurance, charitable giving, wealth transfer planning, and tax services.

The family office market has experienced significant growth in recent years. It is fueled by rising wealth among high-net-worth individuals (HNWIs), the increasing complexity of managing financial affairs, and a preference for personalized and tailored investment strategies. This expansion has resulted in heightened competition among family offices and greater interest from investors and financial institutions seeking to serve this market.

The family office market is characterized by its diversity, as it embraces a range of investment strategies comprising stocks and bonds, real estate, and hedge funds.

Family Office Market Trends

Single-Family Offices Represent the Largest Segment of the Market

A single-family office (SFO) is a private, independent business entity established solely to oversee the financial and personal affairs of a single affluent family. The financial capital managed by the SFO belongs exclusively to the family. The single-family office market is experiencing growth, driven by factors such as increasing wealth among high-net-worth individuals, a demand for personalized financial services, and the need for sophisticated wealth management strategies. This growth is further fueled by the emergence of new family offices, particularly in countries with a rising number of ultra-high net worth individuals.

The single-family office sector has experienced significant growth since the turn of the millennium, with a majority of family offices being established after 2000. This trend is closely linked to the substantial increase in new wealth generation in both established wealth centers and emerging markets over the past two decades. The rise of new technologies and digital innovations has played an important role in driving this wave of wealth creation.

The single-family offices segment is driven by the need for personalized financial management and a centralized focus on managing a specific family's wealth. There is also a significant emphasis on control, confidentiality, and the alignment of investment strategies and estate planning with the family's values and goals. Additionally, the single-family office model offers a holistic approach to managing various financial needs, including tax optimization, legal matters, philanthropy, and succession planning, thereby enhancing the overall cohesion and direction of a family's financial trajectory.

North America Holds the Largest Market Share in the Family Offices Market

A robust financial infrastructure, regulatory environment, economic policies, and technological advancements influence the North American market. The region's concentration of wealth, entrepreneurial growth, and stable political system make it attractive for family offices. Factors such as investment preferences, taxation policies, and the availability of professional services tailored to high-net-worth individuals also play a role.

The region offers a sophisticated investment landscape with opportunities across asset classes, including traditional investments like bonds and equities and innovative sectors such as technology and sustainability. Cultural factors and local investment philosophies may shape the approach of family offices in North America. Integrating social responsibility and ethical considerations in investment decisions has become increasingly important in the region. North America's diverse and dynamic economy provides opportunities and challenges that family offices must navigate to optimize their investment outcomes.

Family Office Industry Overview

The family office market is fragmented with the presence of many players. Many family offices are broadening their service offerings to encompass traditional wealth management and legal, educational, philanthropic, and lifestyle management services. Collaborations and partnerships with specialized firms in various sectors are becoming more common, expanding the expertise available to clients. The key players include Cascade Investment, Walton Enterprises LLC, Bezos Expeditions, Mousse Partners, and Ballmer Group.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for Customzied Solution

- 4.2.2 Growth In The Number of High Networth Individuals Across Regions

- 4.3 Market Restraints

- 4.3.1 Over Reliance on Legacy Systems

- 4.3.2 Managing a Diverse Portfolio of Investment

- 4.4 Market Opportunities

- 4.4.1 Growing Demand for Personalized Financial Services

- 4.4.2 Increasing Focus on Impact Investing

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Insights on Technological Advancements in the Market

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Product

- 5.1.1 Single Family Office

- 5.1.2 Multi Family Office

- 5.1.3 Virtual Family Office

- 5.2 By Asset Class Of Investment

- 5.2.1 Bonds

- 5.2.2 Equities

- 5.2.3 Alternative Investments

- 5.2.4 Commodities

- 5.2.5 Cash Or Cash Equivalents

- 5.3 By Geography

- 5.4 North America

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

- 5.4.4 Rest of North America

- 5.5 Europe

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Russia

- 5.5.5 Italy

- 5.5.6 Spain

- 5.5.7 Rest of Europe

- 5.6 Asia-Pacific

- 5.6.1 India

- 5.6.2 China

- 5.6.3 Japan

- 5.6.4 Australia

- 5.6.5 Rest of Asia-Pacific

- 5.7 Latin America

- 5.7.1 Brazil

- 5.7.2 Argentina

- 5.7.3 Rest of South America

- 5.8 Middle-East and Africa

- 5.8.1 United Arab Emirates

- 5.8.2 South Africa

- 5.8.3 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Cascade Investment LLC

- 6.2.2 Bezos Expeditions

- 6.2.3 Bessemer Trust

- 6.2.4 MSD Capital

- 6.2.5 Stonehage Fleming

- 6.2.6 Glenmede

- 6.2.7 Emerson Collective

- 6.2.8 U.S. Trust - Bank of America Private Wealth Management

- 6.2.9 Bespoke Wealth Management

- 6.2.10 JPMorgan Chase Wealth Management

- 6.2.11 Goldman Sachs Family Office

- 6.2.12 Silvercrest Asset Management*