|

市場調査レポート

商品コード

1851204

ロボット内視鏡装置:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Robotic Endoscopy Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ロボット内視鏡装置:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月13日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

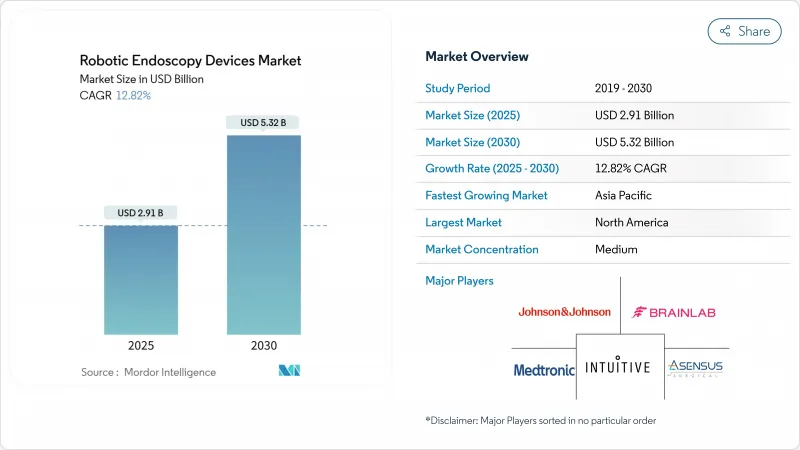

ロボット内視鏡装置市場は、2025年に29億1,000万米ドルに達し、2030年には53億2,000万米ドルに達すると予測されています。

低侵襲手術の採用拡大、画像処理とナビゲーションへの人工知能の急速な統合、院内感染率抑制の必要性などが需要を後押ししています。また、医療システムは、ロボット技術を入院期間の短縮と総手術コストの削減のためのルートと見なしており、設備投資に有利な経済性を生み出しています。特許の崖によってコア技術が民主化され、モジュール式で低コストのプラットフォームが市場に登場するにつれ、競合の激しさは増しています。一方、シングルユース・スコープが交差汚染のリスクを排除することが実証されつつあり、外来患者に対する価値提案が強化されつつあります。これらの要因が相まって、ロボット内視鏡装置市場は今後10年間、2桁成長を維持するものと思われます。

世界のロボット内視鏡装置市場の動向と洞察

低侵襲ロボット手術の急速な普及

臨床エビデンスによると、ロボット支援手術は従来の技術に比べて合併症発生率を50%削減し、回復時間を40%短縮しています。病院は、バリュー・ベース・ケアの義務化に対応するため、このような成果を優先する傾向が強まっており、プラットフォームの導入拡大や手技メニューの拡充につながっています。インテュイティブ・サージカル社の2025年第1四半期の手術件数は17%増加し、世界的な勢いを示しています。強化された3Dビジョン、振戦フィルタリング、人間工学に基づいたコンソールも外科医の疲労を軽減し、外来でのより長く複雑な症例を可能にします。これらの利点を総合すると、対象となる患者層が拡大し、ロボット内視鏡装置市場の経済的魅力が強化されます。

AIを活用したナビゲーションとイメージングが診断の歩留まりを高める

ディープラーニングモデルにより、ロボット気管支鏡検査における診断歩留まりは、従来の67.8%を大きく上回る85%以上となりました。ジョンソン・エンド・ジョンソンのMONARCH QUESTプラットフォームは、260%向上した計算能力とAI主導のパスプランニングを統合し、病変のターゲティングをリアルタイムで改善します。オリンパスCADDIEのようなクラウドベースのシステムは、大腸スクリーニングにも同様の利点をもたらし、AIは余分な処置時間なしに腺腫の検出を向上させる。より高い精度は、再手術を減らし、治療の意思決定を加速し、プラットフォームの所有者に明確な競争力を与えます。

ロボットプラットフォームの高い資本コストと手技ごとのコスト

システムの定価は150万米ドルから250万米ドルであり、さらに年間サービス料は10万米ドル以上であるため、小規模施設にとってはハードルが高いです。比較研究によると、鼠径ヘルニアのロボット手術は2,810ユーロ(3,242.01米ドル)かかるのに対し、腹腔鏡手術は726ユーロ(837.62米ドル)かかります。CMR Surgicalのような新規参入企業は、レガシーシステムを下回る価格のモジュラーアーキテクチャでこのギャップを狙っているが、低所得地域では予算の制約が広がっており、依然として普及が抑制されています。

セグメント分析

治療用ロボット内視鏡は、2024年のロボット内視鏡装置市場の55.52%を占め、診断と介入を一度に行うシステムに対する医療提供者の需要を裏付けています。主要製品は、内視鏡的粘膜下層剥離術や自然開口部経管手術などの複雑な操作を実行し、患者と支払者の双方にアピールする傷跡のない結果を可能にします。ジョンソン・エンド・ジョンソンのMONARCHプラットフォームは、このようなプレミアムなポジショニングを示すものであり、EndoQuestは、消化管処置のための柔軟なシングルポートコンセプトを追求しています。AIを活用した可視化によりがんの早期発見が可能になり、診断機器の売上はCAGR 15.25%で推移しています。カプセルシステムとハイブリッド画像処理ロボットがアクセスを拡大し、1つのコンソールがすべてのケア経路を管理する将来の収束を示唆。治療システムのロボット内視鏡装置市場規模は着実に拡大すると予測されるが、予防医療が政策的に優先されるようになるにつれ、診断イノベーションが上回ることになります。

診断プラットフォームの市場規模は依然として小さいが、投資家はワイヤレスカプセルロボットや、処置時間を短縮するクラウド対応分析に資金を投入しています。嚥下型ポンプジェットカメラのような初期段階のプロジェクトは、消化管スクリーニングの範囲を拡大し、特に完全な検査室が乏しい地方では有効です。これらの機器が規制当局の認可を取得するにつれて、診断ソリューションのロボット内視鏡装置市場シェアは上昇し、同業他社の治療機器との収益格差は縮小すると予想されます。

地域別分析

北米は2024年の売上高の38.82%を占め、メディケアの支払い明確化と成熟した外科医の人材プールに支えられています。米国のフラッグシップセンターでは、次世代コンソールが認可後数カ月で導入されるのが常であり、アップグレードサイクルが堅調です。カナダも同様のパターンをとっており、メキシコの民間病院は医療観光客に先進的な設備導入の資金を供給しています。

欧州のシェアは大きいが、規制の逆風と使い捨てプラスチックに対するグリーン政策の監視に直面しています。ドイツ、フランス、英国が圧倒的な設置台数を誇っているが、医療機器規制の下での複数年にわたる適合性評価が新規参入企業の市場参入を遅らせています。北欧の医療システムはロボットによるヘルニア修復の利点を調査しているが、費用対効果に関する疑問が残っており、急速なスケールアップを抑制しています。

アジア太平洋地域のCAGRは13.62%と最も速いです。中国は、欧米の同業他社に比べて30%~40%の割引価格でコンソールを提供する国内チャンピオンを通して勢いを維持し、第3次病院全体での採用に拍車をかけています。日本は独自のプラットフォームと5G対応遠隔手術のデモンストレーションを開拓し、韓国は国のがん検診プロトコルでロボット工学を重視しています。新興ASEAN諸国とインドの民間チェーンは、ロボティクスをインバウンド医療ツーリズムの差別化要因として捉え、積極的な投資を行っています。その結果、アジア太平洋地域のロボット内視鏡装置市場規模は、見通し期間終了間際には欧州を追い抜くと予測されます。

中東・アフリカは、旗艦病院建設にロボット工学を組み込んだ湾岸協力会議プロジェクトに牽引され、初期ではあるが有望な取り込みを記録しています。サハラ以南では南アフリカが先陣を切る。ラテンアメリカではブラジルとチリで着実な導入が見られるが、為替変動が普及を抑制しています。これらの地域では、ベンダーファイナンスと手技に基づくリースモデルが、需要の増加を引き出す上で重要です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 低侵襲ロボット手術の急速な普及

- 老年人口、肥満人口、糖尿病人口の増加

- ロボット消化器・肺インターベンションに対する有利な償還金

- AIを活用したナビゲーションとイメージングが診断の歩留まりを高める

- 外来専用ロボット気管支鏡検査室の急増

- 感染症抑制のための単回使用ロボット内視鏡の需要

- 市場抑制要因

- ロボットプラットフォームの高い資本コストと1手技あたりコスト

- 患者安全のための厳しい規制承認

- ロボット内視鏡の訓練を受けた外科医の不足

- 使い捨てロボットスコープに対する持続可能性の推進

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- 診断用ロボット内視鏡

- カプセルロボット

- 画像/可視化ロボット

- 治療用ロボット内視鏡

- 外科用内視鏡プラットフォーム

- ロボット気管支鏡

- NOTES&経管ロボット

- 診断用ロボット内視鏡

- 用途別

- 腹腔鏡検査

- 気管支鏡検査

- 大腸内視鏡検査

- その他の用途

- エンドユーザー別

- 病院

- 外来手術センター

- 専門クリニック

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Intuitive Surgical Inc.

- Johnson & Johnson(Auris Health)

- Medtronic PLC

- Olympus Corporation

- Asensus Surgical Inc.

- CMR Surgical Ltd

- Medrobotics Corporation

- Brainlab AG

- Avatera Medical GmbH

- AKTORmed GmbH

- Virtuoso Surgical

- Noah Medical

- EndoQuest Robotics

- Microbot Medical

- Titan Medical

- Fujifilm Holdings Corp.

- SHINVA Medical

- Apollo Endosurgery

- Stryker Corp.

- Karl Storz SE