|

市場調査レポート

商品コード

1445480

牛用飼料: 市場シェア分析、業界動向と統計、成長予測(2024~2029年)Cattle Feed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 牛用飼料: 市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

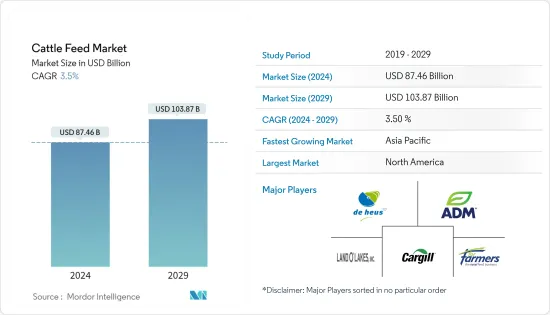

牛用飼料市場規模は2024年に874億6,000万米ドルと推定され、2029年までに1,038億7,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に3.5%のCAGRで成長します。

主なハイライト

- 世界的には、米国、英国、アジアなどの西側諸国での高品質の牛肉の需要の増加や牛肉の消費量の多さなどの要因により、肉用牛セグメントは予測期間中に成長を遂げました。中国は牛肉の最大の消費国であり生産国であり、肉牛の頭数も増加しています。

- 国連食糧農業機関(FAO)は2021年、2050年までに牛製品の需要が前年比1.7%増加し、乳製品の需要は55%、牛肉の需要は70%増加すると予測しました。新興諸国における牛乳および乳製品の需要の増加は、予測期間中に世界市場を押し上げるでしょう。

- 現在、欧州と北米は乳製品と肉の消費シェアを大きく占めていますが、アジア太平洋地域とラテンアメリカ地域では急速な成長が見込まれています。乳製品と牛肉の需要の増加により、牛飼育の工業化が進みました。これは、牛群の規模の拡大、配合飼料の使用の増加、牛の科学的管理の改善につながります。この現象は牛の飼料市場の成長に貢献しています。

牛用飼料市場の動向

新興諸国における畜産業の工業化の推進

新興諸国における人口の増加と、国民の栄養と味覚の好みを満たす必要性により、家畜生産の工業化が進んでいます。新興諸国では、牛の飼育は伝統的に裏庭の仕事でした。しかし、需要が高まり、より大規模な群れを維持することによる規模の経済性に対する認識が高まるにつれて、これらの国々の牛の飼育は変化し始めています。たとえば、FAOによると、インドの牛の頭数は2018年の1億9,190万頭から2021年には1億9,320万頭まで増加しました。また、2021年のインドの牛乳生産量は1億830万トンで、2018年から20.6%増加しました。

FAOによると、内陸新興諸国における牛乳生産量は2021年に4,190万トンでした。さらに、牛の頭数は2018年の2億4,630万頭から2021年には2億6,440万頭まで増加しました。畜産の工業化が進むと、適切な量の配合飼料の使用を含む、高度な管理慣行の採用。これにより、予測期間中に牛の飼料市場の成長が促進されると予想されます。

北米が世界市場を独占

北米では、2021年の牛の頭数は1億4,080万頭でした。人口の増加により、牛の飼料の需要が増加しています。北米では、米国は牛の飼料を含む動物飼料の最大の生産国であり、世界的には人口の多さと畜産業の需要により中国に次ぐ第二位の牛の飼料生産米国です。牛の飼料輸出業者。 ITCによると、2021年に米国は飼料輸出総額の8.9%を占めました。この地域は、北米の飼料生産の90%以上を占めていた米国、カナダ、メキシコ間の自由貿易協定により成長を遂げています。

この地域には世界有数の動物飼料生産者が数多くいます。国内の著名な飼料メーカーには、カーギル、ランドオレイクス、オールテック、ADMアライアンスニュートリション、パーデューファームズ、JDハイスケル&Co.ケントニュートリショングループ、ハイプロフィード、サザンステイツコープなどがあります。

したがって、自由貿易協定、牛の頭数の多さ、輸出用および国内消費用の大手飼料メーカーの存在などの要因により、北米地域は予測期間中に最大の地域となることができました。

牛の飼料産業の概要

牛の飼料市場は非常に細分化されており、多国籍企業の存在感が強い市場で多くの地元および地域の企業が市場シェアの拡大を目指して競い合っています。 Archer Daniels Midland、Cargill Inc.、Land O'Lakes Inc.、De Heus、ForFarmersは、市場の主要企業の一部です。新興国市場では原材料の供給が細分化されており、消費者グループが地理的に分散しているため、地元の飼料メーカーはニッチな顧客グループを維持する大きな機会を得ることができます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 動物の種類

- 乳牛

- 肉牛

- 他の種類の牛

- 材料

- シリアル

- ケーキとミックス

- 食品の無駄遣い

- 飼料添加物

- 他の材料

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- ロシア

- イタリア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 残りのアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他南米

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Archer Daniels Midland Company

- Land O'Lakes Inc.

- De Heus

- For Farmers Inc.

- DBN Group

- Biomin

- New Hope Lihue

- Wen's Food Group

- Godrej Agrovet Limited

第7章 市場機会と将来の動向

The Cattle Feed Market size is estimated at USD 87.46 billion in 2024, and is expected to reach USD 103.87 billion by 2029, growing at a CAGR of 3.5% during the forecast period (2024-2029).

Key Highlights

- Globally, the beef cattle segment has witnessed growth during the forecast period due to factors such as a rise in the demand for high-quality beef meat and high consumption of beef meat in western countries such as the United States, the United Kingdom, and Asia. China is the biggest consumer and producer of beef meat and growth in the beef cattle population.

- In 2021, The United Nations Food & Agriculture Organization (FAO) projected a 1.7% year-on-year increase in the demand for cattle products by 2050, with the demand for dairy products projected to increase by 55% and beef by 70%. The increasing demand for milk and dairy products in developing countries will boost the global market during the forecast period.

- Europe and North America currently have a significant consumption share of dairy products and meat, while rapid growth has been projected in the Asian-Pacific and Latin American regions. Increased demand for dairy products and beef has led to increased industrialization of cattle rearing. This translates to an increase in herd sizes, increased use of compound feed, and better scientific management of cattle. This phenomenon has helped in the growth of the cattle feed market.

Cattle Feed Market Trends

Increasing Industrialization of Livestock Production in Developing Countries

The increasing population and the need to satisfy the nutritional and taste preferences of the population in developing countries have led to increased industrialization of livestock production. In developing countries, cattle rearing has traditionally been a backyard occupation. However, with increased demand and more awareness regarding the economies of scale of maintaining larger herds, cattle rearing in these countries has started to transform. For instance, according to FAO, the cattle population in India has increased to 193.2 million in 2021 from 191.9 million in 2018. Also, in 2021, India produced 108.3 million metric ton of milk, an increase of 20.6% from 2018.

According to FAO, in land-locked developing countries, cow milk production accounted for 41.9 million metric tons in 2021. Moreover, the cattle population increased to 264.4 million heads in 2021 from 246.3 million heads in 2018. Increased industrialization of cattle husbandry would lead to the adoption of advanced management practices, including the usage of compound feed in appropriate dosages. This is expected to boost the growth of the cattle feed market over the forecast period.

North America Dominates the Global Market

In North America, the cattle population was 140.8 million heads in 2021. The increasing population creates an increasing demand for cattle feed. In North America, the United States is the largest producer of animal feed including cattle feed, and globally, the second largest producer of cattle feed after China due to the significant population and demand of its livestock industry, the United States is one of the largest cattle feed exporters. According to ITC, in 2021, the United States contributed 8.9% of the total feed export. The region is witnessing growth due to a free-trade agreement between the United States, Canada and Mexico as these are the countries which accounted for more than 90% of the feed production in the North America.

The region has many of the global leading animal feed producers. The prominent feed manufacturers in the country include Cargill, Land O'Lakes, Alltech, ADM Alliance Nutrition, Perdue Farms, J.D. Heiskell & Co. Kent Nutrition Group, Hi-Pro Feeds, and Southern States Coop.

Therefore, owing to factors such as free-trade agreement, high cattle population and presence of leading feed manufacturers for exporting and domestic consumption has helped the North America region to be a largest region during the forecasted period.

Cattle Feed Industry Overview

The cattle feed market is highly fragmented, with numerous local and regional players vying for increasing market shares in a market that has a strong presence of multinational players. Archer Daniels Midland, Cargill Inc., Land O' Lakes Inc., De Heus, and ForFarmers are some of the major players in the market. The fragmented supply of raw materials and the geographically dispersed consumer group in developing markets provide significant opportunities for local feed manufacturers to maintain a niche group of customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Animal Type

- 5.1.1 Dairy Cattle

- 5.1.2 Beef Cattle

- 5.1.3 Other Cattle Types

- 5.2 Ingredient

- 5.2.1 Cereals

- 5.2.2 Cakes and Mixes

- 5.2.3 Food Wastages

- 5.2.4 Feed Additives

- 5.2.5 Other Ingredients

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Russia

- 5.3.2.6 Italy

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of the Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Archer Daniels Midland Company

- 6.3.2 Land O'Lakes Inc.

- 6.3.3 De Heus

- 6.3.4 For Farmers Inc.

- 6.3.5 DBN Group

- 6.3.6 Biomin

- 6.3.7 New Hope Lihue

- 6.3.8 Wen's Food Group

- 6.3.9 Godrej Agrovet Limited