|

|

市場調査レポート

商品コード

1910612

産業用コンピュータ断層撮影(CT)-市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Industrial Computed Tomography - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 産業用コンピュータ断層撮影(CT)-市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 161 Pages

納期: 2~3営業日

|

概要

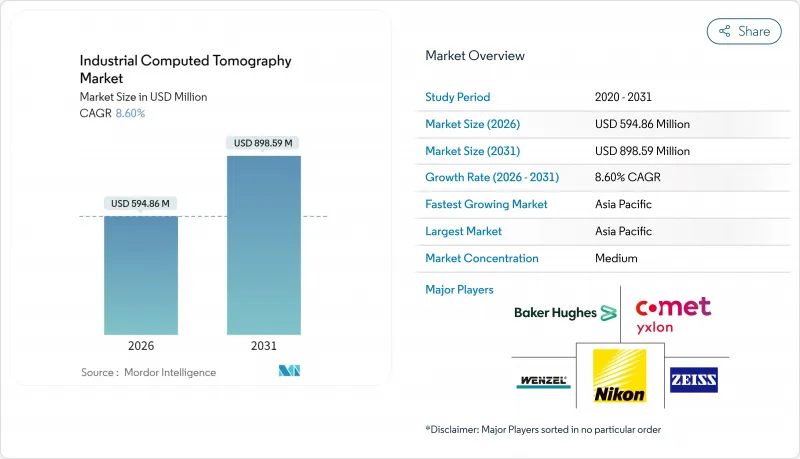

産業用コンピュータ断層撮影(CT)市場は、2025年に5億4,775万米ドルと評価され、2026年の5億9,486万米ドルから2031年までに8億9,859万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは8.60%と見込まれます。

この堅調な拡大は、航空宇宙、自動車、電子機器、積層造形(アディティブ・マニュファクチャリング)のワークフローにおいて、本モダリティがニッチな検査手段から主流の品質保証プラットフォームへと移行していることを反映しています。需要は、電気自動車サプライチェーン向けのバッテリー安全規制の強化、体積検証を必要とする積層造形の急増、サイクルタイムを短縮するAIベースの自動欠陥認識、サブミクロン解像度検査を必要とする小型電子機器によって牽引されています。システムベンダーは、高速化が進む検出器技術、単一スキャンで材料を分離するデュアルエネルギー源、中小メーカーにも導入を可能にするハードウェア価格の低下といった恩恵も受けています。高い初期資本コストと訓練を受けたCTオペレーターの世界的不足が導入を抑制していますが、リースやX線サービスとしての提供といった資金調達モデルが顧客基盤を拡大しています。現在、アジア太平洋地域が収益面で主導的立場にあり、中国、日本、韓国が電子機器および精密製造ラインにCTを導入していることから、最も急激な成長曲線を示しています。

世界の産業用コンピュータ断層撮影(CT)市場の動向と洞察

航空宇宙・自動車分野における非破壊検査の需要増加

民間航空機プログラムでは、複合材製翼や3Dプリント製ブラケットの検証にCTが活用され、この検査手法は補助的な検査から、初回製品検査や量産工程における必須のゲート(検査ポイント)へと位置付けが変化しています。自動車メーカーは、CTをエンジンブロックの鋳造検査からバッテリーパックの検証にまで拡大しており、熱伝播解析には精密な内部形状マッピングが必要です。この技術は、炭素繊維強化部品内のサブミリメートルレベルの空隙を検出できるため、AS9100およびISO/TS 16949品質基準を満たしながら、軽量化の目標達成を支援します。

積層造形品質管理の普及拡大

GE社のLEAPエンジン燃料ノズル量産検査が示すように、産業用CTは3Dプリント金属部品の層別欠陥検出における基準ツールです。リアルタイム再構成と自動欠陥分類により、スキャンから判断までの時間を8時間から2時間に短縮し、CTを大量生産AMラインで実用可能なものにしています。ISO/ASTM 52900規格はCT受入基準を組み込んでおり、この手法は任意のチェックではなく、コンプライアンス要件となっています。

高出力CTシステムの高い取得・運用コスト

10マイクロメートル未満の解像度を実現する装置は、遮蔽設備、安全システム、施設改修を含めると150万~300万米ドルの費用がかかります。年次的な管球交換と100kWの電力消費が運用コストを押し上げます。リース契約は支払いを分散させますが、総所有コストを増加させ、スケジュール調整の柔軟性を制限します。

セグメント分析

2025年時点で、300kV以上の高電圧装置が産業用CT市場の62.15%を占めました。これは航空宇宙用鋼鋳物や厚肉アルミニウム部品など、深い透過性が求められる部品の需要に牽引されたものです。中低電圧装置のシェアは小さいもの、電子部品ラインでデスクトップシステムが注目される中、2031年までCAGRCAGR9.78%で拡大が見込まれます。ルマフィールド社の10万米ドル未満のデスクトップスキャナーは、財務的障壁を低減することで対応可能な市場基盤を拡大しております。構造化陽極技術は放熱性を向上させ、冷却負荷を追加することなく160kVおよび225kVユニットによるポリマーやアルミニウムの撮影を可能にしております。

高電圧装置の所有者は、高密度部品の鮮明な画像を得るために広い設置面積と遮蔽対策を受け入れます。一方、回路基板やプラスチック組立品に特化した研究所では、コンパクトさと運用コスト削減のため低エネルギー装置を選択します。この二層構造の動向が、2031年までのベンダーの製品ポートフォリオと資金調達スキームを形作ります。

欠陥検出は鋳造・複合材検査における確固たる役割により、2025年の需要の47.65%を占めました。一方、組立分析は自動車メーカーや電子機器メーカーが量産ベースの計測へ移行するにつれ、CAGR10.05%で拡大が見込まれます。バッテリーパック製造業者では、熱暴走事故防止のため、パック密封前にセル配置と溶接位置の整合性をマッピングしています。マイクロエレクトロニクスラインでは、ダイスタックデバイスの自動GD&Tレポート作成において、CTボクセルとCADデータを比較しています。

研究機関の故障解析部門はニッチながら重要なユーザー層であり、現場故障発生時のフォレンジック分解にCTを適用しています。新規薬物送達デバイスや医療用インプラントは、非破壊的な内部確認を求めるもう一つの小規模ながら成長中の分野を形成しています。

地域別分析

アジア太平洋地域は2025年の収益の36.85%を占め、中国の電子機器・EVサプライチェーン、日本の精密自動車製造、韓国のメモリ製造工場を背景に、2031年までCAGR11.76%で拡大が見込まれます。中国のGB38031-2025電池規制により、CTは現地EVリーダー向けパック検証セルへの投資を促進しています。日本のOEMは、ハイブリッドプラットフォームの複合材の適合性と仕上げを保証するためにµ-CTを利用しており、韓国のファブは3D NANDスタックを検証するためにマイクロCTを活用しています。

北米は、ボーイングやロッキード・マーティンなどの航空宇宙大手が、複合材製の翼や3DプリントされたTi-6Al-4Vブラケットの高解像度検査を要求しているため、かなりのシェアを占めています。また、米国はAIを活用した欠陥認識の導入もリードしており、スタートアップ企業がクラウドベースの分析をCTワークフローに統合しています。メキシコのEVバッテリーラインとカナダの民間および航空宇宙クラスターが、この地域の需要をさらに支えています。

欧州では、ドイツの自動車メーカーがアルミ製エンジンハウジングやダイキャスト製バッテリー筐体の検証を行うなど、着実な成長を維持しています。EUバッテリー規制2023/1542では、内部短絡を検出するためにCTスキャンを用いて実施されることが多い、より広範な安全性試験が義務付けられています。フランスの航空宇宙業界の一次サプライヤーは、複合材ファンブレードにデュアルエネルギーCTを導入しており、英国のInnovate UKの資金援助により、積層造形部品向けのインラインCTを改良する官民共同研究所が支援されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 航空宇宙および自動車産業における非破壊検査の需要増加

- 積層造形における品質管理の採用拡大

- 検出器解像度と画像再構成技術の進歩

- 電子機器の小型化に伴いマイクロCT検査が必要となる

- AI駆動型自動欠陥認識によるサイクルタイムの短縮

- 電気自動車(EV)サプライチェーン向けバッテリー安全規制

- 市場抑制要因

- 高出力CTシステムの高い導入・運用コスト

- 放射線安全規制への対応負担と施設改修

- 熟練したCTオペレーターおよびデータアナリストの不足

- 新興テラヘルツおよび超音波モダリティとの競合

- 業界サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- マクロ経済的要因の影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 電圧範囲別

- 低・中電圧(300kV未満)

- 高電圧(300kV以上)

- 用途別

- 欠陥検出/検査

- 故障解析

- アセンブリ分析

- その他の用途

- 技術別/スキャン技術別

- ファンビームCT

- コーンビームCT

- その他

- エンドユーザー産業別

- 航空宇宙・防衛産業

- 自動車

- 電子機器および半導体

- 医療機器

- 学術研究機関

- その他産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Baker Hughes Company(Waygate Technologies)

- Carl Zeiss AG

- Nikon Corporation-Nikon Metrology NV

- Comet Group-Yxlon International GmbH

- Wenzel Group GmbH and Co. KG

- North Star Imaging Inc.

- Diondo GmbH

- Werth Messtechnik GmbH

- RX Solutions SAS

- VJ Technologies Inc.

- VisiConsult X-ray Systems and Solutions GmbH

- Rigaku Corporation

- Sanying Precision Instruments Co., Ltd.

- Aolong Radiative Instrument Group Co., Ltd.

- Seamark ZM Technology Co., Ltd.

- Royma Tech(Suzhou)Precision Co., Ltd.

- Shimadzu Corporation

- Hitachi High-Tech Corporation

- Thermo Fisher Scientific Inc.

- Lumafield Inc.